EvoMarket: A High-Fidelity and Scalable Financial Market Simulator

Pith reviewed 2026-05-10 03:41 UTC · model grok-4.3

The pith

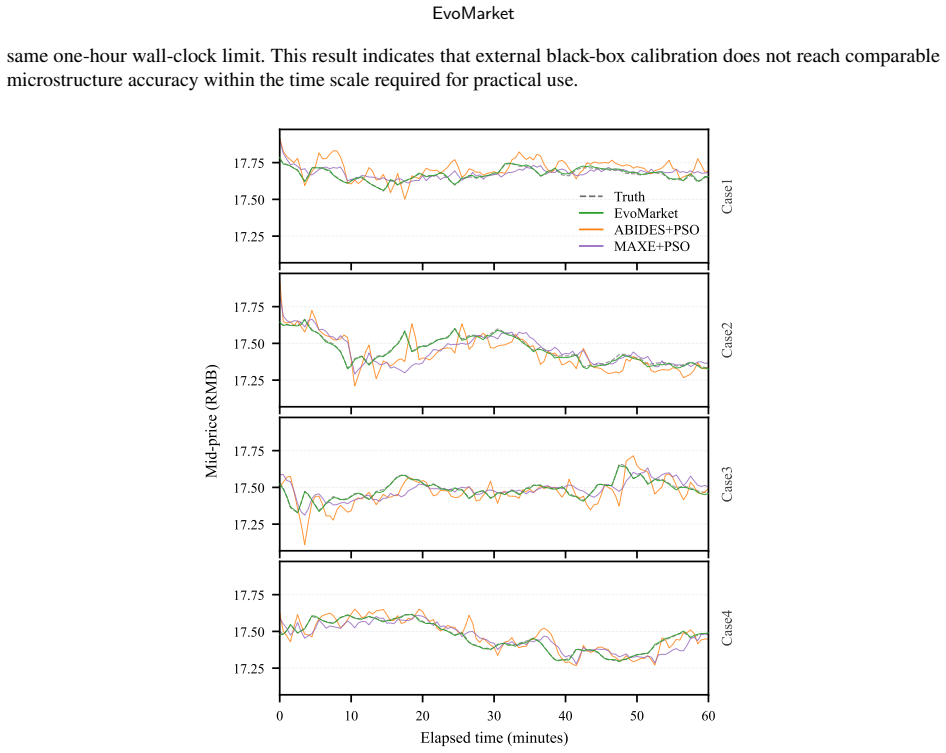

EvoMarket achieves close replay of historical market data over multiple trading days by using an Oracle to add corrective orders when the simulation drifts from real microstructure.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

EvoMarket couples a high-throughput execution core with optimized limit order book data structures, hierarchical scheduling under delays, and asynchronous per-asset matching together with explicit institutional mechanisms including market calendars, opening call auctions, price limits, and T+1 settlement. It introduces an Oracle-guided in-run self-calibration mechanism that interprets microstructure discrepancies as missing order flow and synthesizes corrective orders at recording checkpoints, yielding close replay alignment over five trading days on China A-share data, fidelity improvements across depth levels, broad agent order coverage, and scalable performance as order rates and market宽度

What carries the argument

Oracle-guided in-run self-calibration mechanism that treats differences between simulated and historical limit order book microstructure as missing order flow and generates synthetic corrective orders at fixed recording checkpoints.

If this is right

- Enables intervention-oriented experiments across multiple assets and multiple trading days in one system.

- Delivers measurable fidelity gains from budgeted in-run calibration at varying order-book depth levels.

- Maintains broad coverage of possible agent order placements during simulation.

- Preserves performance scalability when input order rates and overall market breadth grow.

- Produces interpretable event-time responses and cross-asset dependence patterns in event-study style evaluations.

Where Pith is reading between the lines

- The same calibration logic could support counterfactual policy tests by letting an experimenter alter rules mid-run and observe resulting order-flow changes.

- If the corrective orders remain unbiased, the method may extend to other exchanges or asset classes for comparative stress testing.

- High throughput suggests possible integration with streaming market data for near-real-time scenario generation.

- Event-study outputs could help quantify how external shocks transmit through linked assets in multi-market settings.

Load-bearing premise

The Oracle-guided in-run self-calibration mechanism can interpret microstructure discrepancies as missing order flow and synthesize corrective orders at recording checkpoints without introducing systematic biases or artifacts into the simulated market dynamics.

What would settle it

Run the simulator on a held-out multi-day China A-share dataset and measure whether price paths, trade volumes, and order-book depth profiles stay aligned with the real records at multiple time points after each calibration checkpoint, with divergence remaining below a small threshold.

Figures

read the original abstract

High-fidelity, scalable market simulation is a key instrument for mechanism evaluation, stress testing, and counterfactual policy analysis. Yet existing simulators rarely achieve \emph{mechanism fidelity} beyond single-asset intraday settings, \emph{microstructure fidelity} against historical limit order books (LOB), and \emph{computational tractability} at market scale in a single system. This paper presents \textit{EvoMarket}, a discrete-event, multi-agent financial market simulator designed for intervention-oriented experiments in multi-asset and cross-day environments. EvoMarket couples a high-throughput execution core (optimized LOB data structures, hierarchical scheduling under propagation delays, and asynchronous per-asset matching) with explicit institutional mechanisms (market calendars, opening call auctions, price limits, and T+1 settlement). To avoid expensive black-box calibration, EvoMarket introduces an Oracle-guided in-run self-calibration mechanism that interprets microstructure discrepancy as missing order flow and synthesizes corrective orders at recording checkpoints. Experiments on China A-share order-flow and LOB data show close replay alignment over five trading days, fidelity gains from budgeted in-run calibration across depth levels, broad agent order-space coverage, and scalable performance under increasing input order rates and market breadth. We further demonstrate cross-asset linkage and event-study style intervention evaluation that produces structured dependence and interpretable event-time responses.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript presents EvoMarket, a discrete-event multi-agent financial market simulator for multi-asset and cross-day environments. It couples an optimized LOB execution core and explicit institutional mechanisms (calendars, call auctions, price limits, T+1) with an Oracle-guided in-run self-calibration that treats microstructure discrepancies as missing order flow and synthesizes corrective orders at checkpoints. Experiments on China A-share order-flow and LOB data are reported to demonstrate close replay alignment over five trading days, fidelity gains from budgeted calibration, broad agent coverage, scalability with input rates and breadth, plus cross-asset linkage and event-study intervention evaluation.

Significance. If the self-calibration can be shown not to introduce systematic biases into matching, depth evolution, or agent behavior, the simulator would offer a useful platform for mechanism evaluation and counterfactual policy analysis at market scale. The explicit handling of multi-asset and institutional rules addresses a recognized gap in existing simulators; however, the reliance on oracle-driven corrections risks reducing the system to a hybrid replay tool rather than a fully generative model.

major comments (3)

- [Abstract] Abstract: The central claim of 'close replay alignment' and 'fidelity gains from budgeted in-run calibration' is presented without any quantitative error metrics (e.g., RMSE on depth profiles, Kolmogorov-Smirnov statistics on order sizes/timings, or ablation results comparing calibrated vs. uncalibrated runs). This absence prevents assessment of whether the alignment is statistically meaningful or merely visual.

- [Abstract] Abstract (Oracle-guided in-run self-calibration): The mechanism interprets all LOB discrepancies as missing order flow and synthesizes corrective orders, yet no rule is supplied for choosing correction timing, size, type, or price (e.g., whether limits or T+1 constraints are enforced, or how parameters are sampled to preserve statistical indistinguishability from real flow). Because this step is load-bearing for the fidelity claim, the lack of specification leaves open the possibility that corrections alter subsequent dynamics or mask model deficiencies.

- [Abstract] Abstract: The paper advertises utility for 'counterfactual policy analysis' and 'intervention evaluation,' but the oracle calibration depends on historical LOB checkpoints; it is unclear how the system would generate independent trajectories for true counterfactuals without the oracle, undermining the advertised use case.

minor comments (1)

- [Abstract] The abstract states 'broad agent order-space coverage' without defining the coverage metric or the agent types employed.

Simulated Author's Rebuttal

We thank the referee for the constructive comments on our manuscript. We address each major point below, providing clarifications from the full text and proposing targeted revisions to improve clarity and completeness without altering the core contributions.

read point-by-point responses

-

Referee: [Abstract] Abstract: The central claim of 'close replay alignment' and 'fidelity gains from budgeted in-run calibration' is presented without any quantitative error metrics (e.g., RMSE on depth profiles, Kolmogorov-Smirnov statistics on order sizes/timings, or ablation results comparing calibrated vs. uncalibrated runs). This absence prevents assessment of whether the alignment is statistically meaningful or merely visual.

Authors: The experimental results section of the manuscript reports quantitative metrics supporting these claims, including RMSE values on depth profiles across multiple levels and Kolmogorov-Smirnov statistics comparing order size and timing distributions between simulated and real data, with explicit ablations showing fidelity gains from calibration. We agree the abstract would benefit from including key quantitative highlights and will revise it accordingly to reference these metrics and their statistical significance. revision: yes

-

Referee: [Abstract] Abstract (Oracle-guided in-run self-calibration): The mechanism interprets all LOB discrepancies as missing order flow and synthesizes corrective orders, yet no rule is supplied for choosing correction timing, size, type, or price (e.g., whether limits or T+1 constraints are enforced, or how parameters are sampled to preserve statistical indistinguishability from real flow). Because this step is load-bearing for the fidelity claim, the lack of specification leaves open the possibility that corrections alter subsequent dynamics or mask model deficiencies.

Authors: The methods section details the calibration rules: corrections occur at fixed recording checkpoints, sizes are computed directly from the observed discrepancy volume, order types are selected to match empirical frequencies in the real flow (with limits enforced and T+1 settlement respected), and prices are drawn from the current LOB state or sampled from historical conditional distributions to preserve statistical properties. We will add a concise summary of these rules to the abstract to address the concern. revision: yes

-

Referee: [Abstract] Abstract: The paper advertises utility for 'counterfactual policy analysis' and 'intervention evaluation,' but the oracle calibration depends on historical LOB checkpoints; it is unclear how the system would generate independent trajectories for true counterfactuals without the oracle, undermining the advertised use case.

Authors: The simulator architecture supports an independent generative mode in which the oracle and self-calibration are disabled, allowing agents and mechanisms to produce trajectories based solely on their internal models and random seeds. This mode is used for the intervention evaluation experiments described in the results. We will revise the abstract and discussion to explicitly distinguish replay (oracle-enabled) and generative (oracle-disabled) modes to clarify applicability to counterfactual analysis. revision: yes

Circularity Check

No circularity: simulator description and empirical alignment claims contain no derivations, equations, or self-referential reductions.

full rationale

The paper introduces a discrete-event multi-agent simulator with an Oracle-guided in-run self-calibration step that synthesizes corrective orders from observed LOB discrepancies. No equations, first-principles derivations, or parameter-fitting procedures are described that would reduce the reported replay alignment to the calibration inputs by construction. The calibration is presented as an external correction mechanism rather than a tautological definition of the target fidelity metric. No self-citations, uniqueness theorems, or ansatzes imported from prior author work appear in the provided text to support core claims. Experimental results are framed as empirical outcomes against external China A-share data, satisfying the self-contained benchmark criterion.

Axiom & Free-Parameter Ledger

invented entities (1)

-

Oracle-guided in-run self-calibration

no independent evidence

Reference graph

Works this paper leans on

- [1]

-

[2]

O. Hussain, T. Dillon, F. K. Hussain, E. Chang, Probabilistic assessment of financial risk in e-business associations, Simulation Modelling Practice and Theory 19 (2) (2011) 704–717

work page 2011

-

[3]

C. Daah, A. Qureshi, I. Awan, S. Konur, Simulation-based evaluation of advanced threat detection and response in financial industry networks using zero trust and blockchain technology, Simulation Modelling Practice and Theory 138 (2025) 103027

work page 2025

-

[4]

J. Hasbrouck, Empirical market microstructure: The institutions, economics, and econometrics of securities trading, Oxford University Press, 2007

work page 2007

-

[5]

L. De Natale, G. Fargetta, L. R. Scrimali, S. Battiato, Multi-agent reinforcement learning and variational inequality models for international trade networks under crisis, Simulation Modelling Practice and Theory 146 (2026) 103219

work page 2026

- [6]

-

[7]

M. K. Brunnermeier, L. H. Pedersen, Market liquidity and funding liquidity, The Review of Financial Studies 22 (6) (2008) 2201–2238

work page 2008

- [8]

-

[9]

J. Li, L. Cheng, X. Zheng, F.-Y. Wang, Analyzing the stock volatility spillovers in chinese financial and economic sectors, IEEE Transactions on Computational Social Systems 10 (1) (2023) 269–284

work page 2023

-

[10]

A. G. Haldane, R. M. May, Systemic risk in banking ecosystems, Nature 469 (7330) (2011) 351–355

work page 2011

-

[11]

G. W. Imbens, Causal inference in the social sciences, Annual Review of Statistics and Its Application 11 (Volume 11, 2024) (2024) 123–152

work page 2024

-

[12]

Kmenta, Mastering ‘metrics’: The path from cause to effect, Business Economics 50 (4) (2015) 230–231

J. Kmenta, Mastering ‘metrics’: The path from cause to effect, Business Economics 50 (4) (2015) 230–231

work page 2015

-

[13]

S. D. Campbell, A review of backtesting and backtesting procedures, Finance and Economics Discussion Series 2005-21, Board of Governors of the Federal Reserve System (U.S.) (2005)

work page 2005

-

[14]

K. Luo, N. Jin, J. Ma, Concentrated liquidity in ethereum blockchain’s digital asset trading: Insights from innovative back-testing algorithms, Computational Economics 66 (5) (2025) 3607–3635. Zhong et al.:Preprint submitted to ElsevierPage 18 of 20 EvoMarket

work page 2025

-

[15]

X. Xue, F. Chen, D. Zhou, X. Wang, M. Lu, F.-Y. Wang, Computational experiments for complex social systems—part i: The customization of computational model, IEEE Transactions on Computational Social Systems 9 (5) (2022) 1330–1344

work page 2022

-

[16]

M. D. Gould, M. A. Porter, S. Williams, M. McDonald, D. J. Fenn, S. D. Howison, Limit order books, Quantitative Finance 13 (11) (2013) 1709–1742

work page 2013

-

[17]

X. Xue, D. Zhou, X. Yu, G. Wang, J. Li, X. Xie, L. Cui, F.-Y. Wang, Computational experiments for complex social systems: Experiment design and generative explanation, IEEE/CAA Journal of Automatica Sinica 11 (4) (2024) 1022–1038

work page 2024

-

[18]

B. M. G, P. K. R, V. J. D. V, P. R, V. Maniappan, S. Doss, Enhancing algorithmic trading strategies with sentiment analysis: A reinforcement learning approach, in: 2024 IEEE 3rd World Conference on Applied Intelligence and Computing (AIC), 2024, pp. 107–112

work page 2024

-

[19]

Charles Schwab & Co., Paper trading (thinkorswim papermoney), Web page, accessed: 2026-01-11 (2023)

work page 2026

-

[20]

Nasdaq, Nasdaq Test Facility (NTF) Guide, version 1.3.1 (Dec. 2018)

work page 2018

-

[21]

T. Hendershott, M. Wee, Y. Wen, Transparency in fragmented markets: Experimental evidence, Journal of Financial Markets 59 (2022) 100732

work page 2022

-

[22]

T. H. Balch, M. Mahfouz, J. Lockhart, M. Hybinette, D. Byrd, How to evaluate trading strategies: Single agent market replay or multiple agent interactive simulation? (2019)

work page 2019

- [23]

-

[24]

D. Byrd, M. Hybinette, T. H. Balch, Abides: Towards high-fidelity multi-agent market simulation, in: Proceedings of the 2020 ACM SIGSIM Conference on Principles of Advanced Discrete Simulation, SIGSIM-PADS ’20, Association for Computing Machinery, New York, NY, USA, 2020, p. 11–22

work page 2020

-

[25]

P. Belcak, J.-P. Calliess, S. Zohren, Fast agent-based simulation framework with applications to reinforcement learning and the study of trading latency effects, in: K. H. Van Dam, N. Verstaevel (Eds.), Multi-Agent-Based Simulation XXII, Springer International Publishing, Cham, 2022, pp. 42–56

work page 2022

-

[26]

S. Y. Frey, K. Li, P. Nagy, S. Sapora, C. Lu, S. Zohren, J. Foerster, A. Calinescu, Jax-lob: A gpu-accelerated limit order book simulator to unlock large scale reinforcement learning for trading, in: Proceedings of the Fourth ACM International Conference on AI in Finance, ICAIF ’23, Association for Computing Machinery, New York, NY, USA, 2023, p. 583–591

work page 2023

-

[27]

F. Abergel, M. Anane, A. Chakraborti, A. Jedidi, I. M. Toke, Limit Order Books, Cambridge University Press, Cambridge, UK, 2016

work page 2016

-

[28]

B. LeBaron, Agent-based financial markets: Matching stylized facts with style, Post Walrasian Macroeconomics: Beyond the DSGE Model 221 (2006) 235

work page 2006

-

[29]

K. Goosen, Calibrating high frequency trading data to agent based models using approximate bayesian computation (2021)

work page 2021

-

[30]

J. Dyer, P. Cannon, J. D. Farmer, S. M. Schmon, Black-box bayesian inference for agent-based models, Journal of Economic Dynamics and Control 161 (2024) 104827

work page 2024

-

[31]

D. Platt, A comparison of economic agent-based model calibration methods, Journal of Economic Dynamics and Control 113 (2020) 103859

work page 2020

-

[32]

M. Lu, S. Chen, X. Xue, X. Wang, Y. Zhang, Y. Zhang, F.-Y. Wang, Computational experiments for complex social systems—part ii: The evaluation of computational models, IEEE Transactions on Computational Social Systems 9 (4) (2022) 1224–1236

work page 2022

-

[33]

X. Xue, X. Yu, D. Zhou, C. Peng, X. Wang, D. Liu, F.-Y. Wang, Computational experiments for complex social systems—part iii: The docking of domain models, IEEE Transactions on Computational Social Systems 11 (2) (2024) 1766–1780

work page 2024

-

[34]

N. Ehrentreich, Agent-based modeling: The Santa Fe Institute artificial stock market model revisited, Springer, 2008

work page 2008

-

[35]

W. B. Arthur, J. H. Holland, B. LeBaron, R. Palmer, P. Tayler, Asset pricing under endogenous expectations in an artificial stock market, in: The economy as an evolving complex system II, CRC Press, 2018, pp. 15–44

work page 2018

-

[36]

S. Sagwal, P. Kayal, K. Vemuri, Analyzing herding, stylized facts, and information cascades via self-organized criticality in an agent-based speculation game, Simulation Modelling Practice and Theory 144 (2025) 103190.doi:https://doi.org/10.1016/j.simpat.2025.10 3190. URLhttps://www.sciencedirect.com/science/article/pii/S1569190X2500125X

-

[37]

C. Mascioli, A. Gu, Y. Wang, M. Chakraborty, M. Wellman, A financial market simulation environment for trading agents using deep reinforcement learning, in: Proceedings of the 5th ACM International Conference on AI in Finance, ICAIF ’24, Association for Computing Machinery, New York, NY, USA, 2024, p. 117–125

work page 2024

- [38]

-

[39]

V. Bogousslavsky, D. Muravyev, Who trades at the close? implications for price discovery and liquidity, Journal of Financial Markets 66 (2023) 100852

work page 2023

-

[40]

C.-C. Chen, A.-P. Chen, P.-Y. Yeh, Modeling and simulation of the open-end equity mutual fund market in taiwan by using self-organizing map, Simulation Modelling Practice and Theory 36 (2013) 60–73

work page 2013

-

[41]

O. U. Aktas, L. Kryzanowski, J. Zhang, Volatility spillover around price limits in an emerging market, Finance Research Letters 39 (2021) 101610

work page 2021

-

[42]

N. Hautsch, A. Horvath, How effective are trading pauses?, Journal of Financial Economics 131 (2) (2019) 378–403

work page 2019

-

[43]

D. Bongaerts, S. D. De Luca, M. Van Achter, Circuit breakers and market runs, Review of Finance 28 (6) (2024) 1953–1989

work page 2024

-

[44]

Madhavan, Market microstructure: A survey, Journal of Financial Markets 3 (3) (2000) 205–258

A. Madhavan, Market microstructure: A survey, Journal of Financial Markets 3 (3) (2000) 205–258

work page 2000

-

[45]

R. Cont, M. Cucuringu, C. Zhang, Cross-impact of order flow imbalance in equity markets, Quantitative Finance 23 (10) (2023) 1373–1393

work page 2023

-

[46]

H. Ham, D. Ryu, R. I. Webb, The effects of overnight events on daytime trading sessions, International Review of Financial Analysis 83 (2022) 102228

work page 2022

- [47]

-

[48]

Zhong et al.:Preprint submitted to ElsevierPage 19 of 20 EvoMarket

H.Tian,X.Zhang,X.Zheng,Z.Zhang,D.D.Zeng,Graphrepresentationlearningofmultilayerspatial–temporalnetworksforstockpredictions, IEEE Transactions on Computational Social Systems 12 (5) (2025) 2228–2241. Zhong et al.:Preprint submitted to ElsevierPage 19 of 20 EvoMarket

work page 2025

-

[49]

Y.Li,Y.Wu,M.Zhong,S.Liu,P.Yang,Simlob:Learningrepresentationsoflimitorderbookforfinancialmarketsimulation,IEEETransactions on Artificial Intelligence (2025) 1–16

work page 2025

-

[50]

A. V. Contreras, A. Llanes, A. Pérez-Bernabeu, S. Navarro, H. Pérez-Sánchez, J. J. López-Espín, J. M. Cecilia, Enmx: An elastic network model to predict the forex market evolution, Simulation Modelling Practice and Theory 86 (2018) 1–10

work page 2018

-

[51]

F. Lamperti, A. Roventini, A. Sani, Agent-based model calibration using machine learning surrogates, Journal of Economic Dynamics and Control 90 (2018) 366–389

work page 2018

- [52]

-

[53]

N. R. Stillman, R. Baggott, J. Lyon, J. Zhang, D. Zhu, T. Chen, P. Vytelingum, Deep calibration of market simulations using neural density estimators and embedding networks, in: Proceedings of the Fourth ACM International Conference on AI in Finance, ICAIF ’23, Association for Computing Machinery, New York, NY, USA, 2023, p. 46–54

work page 2023

-

[54]

P. Yang, Z. Yang, B. Jiang, C. Wang, K. Tang, X. Yao, Posterior distribution-assisted evolutionary dynamic optimization as an online calibrator for complex social simulations (2026)

work page 2026

-

[55]

C. Wang, J. Ren, P. Yang, Alleviating nonidentifiability: A high-fidelity calibration objective for financial market simulation with multivariate time series data, IEEE Transactions on Computational Social Systems 12 (6) (2025) 4910–4922

work page 2025

-

[56]

K. Cranmer, J. Brehmer, G. Louppe, The frontier of simulation-based inference, Proceedings of the National Academy of Sciences 117 (48) (2020) 30055–30062

work page 2020

-

[57]

H.Fang,B.Li,P.Yang,Efficientparametercalibrationofnumericalweatherpredictionmodelsviaevolutionarysequentialtransferoptimization (2026)

work page 2026

-

[58]

R. M. Fujimoto, Parallel discrete event simulation, Commun. ACM 33 (10) (1990) 30–53

work page 1990

- [59]

-

[60]

P. Richmond, R. Chisholm, P. Heywood, M. K. Chimeh, M. Leach, Flame gpu 2: A framework for flexible and performant agent based simulation on gpus, Software: Practice and Experience 53 (8) (2023) 1659–1680

work page 2023

-

[61]

E. Samanidou, E. Zschischang, D. Stauffer, T. Lux, Agent-based models of financial markets, Reports on Progress in Physics 70 (3) (2007) 409. Zhong et al.:Preprint submitted to ElsevierPage 20 of 20

work page 2007

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.