Recognition: 2 theorem links

· Lean TheoremThe Cost of a Free Lunch: Evidence from U.S. Derivatives Markets

Pith reviewed 2026-05-11 00:43 UTC · model grok-4.3

The pith

Enforcing put-call parity incurs hidden carry costs from daily settlement and margin risks despite near-zero price residuals.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Put-call parity is a terminal-payoff identity with quoted residuals against traded futures near zero, yet enforcing parity is path-dependent and exposes arbitrageurs to daily settlement, margin, and finite capital. Minute-level NBBO data on S&P 500 and Russell 2000 options are used to extract option-implied discount factors, which are compared with the OIS curve to construct an annualized carry gap. A reduced-form specification centered on a volatility times sqrt(tau) path-risk term links this carry gap to implementation risk, trading frictions, and financial conditions, with coefficient signs stable across leave-one-year-out validation. The carry gap therefore functions as an implementation

What carries the argument

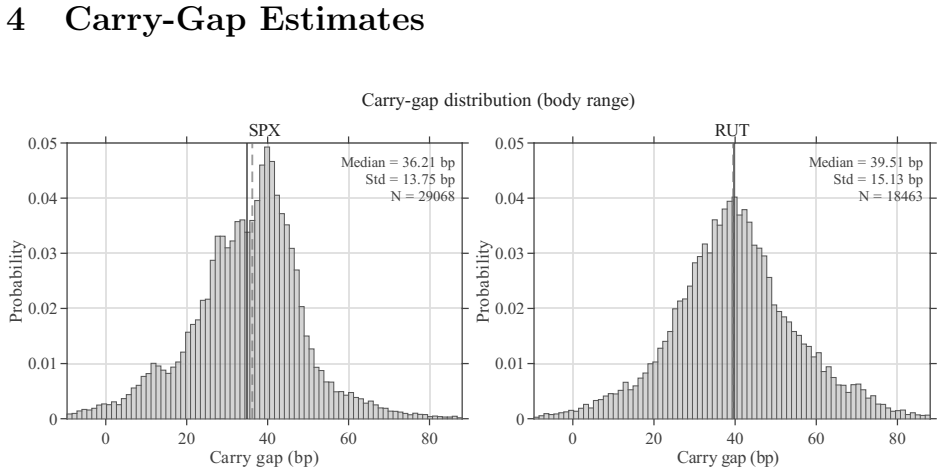

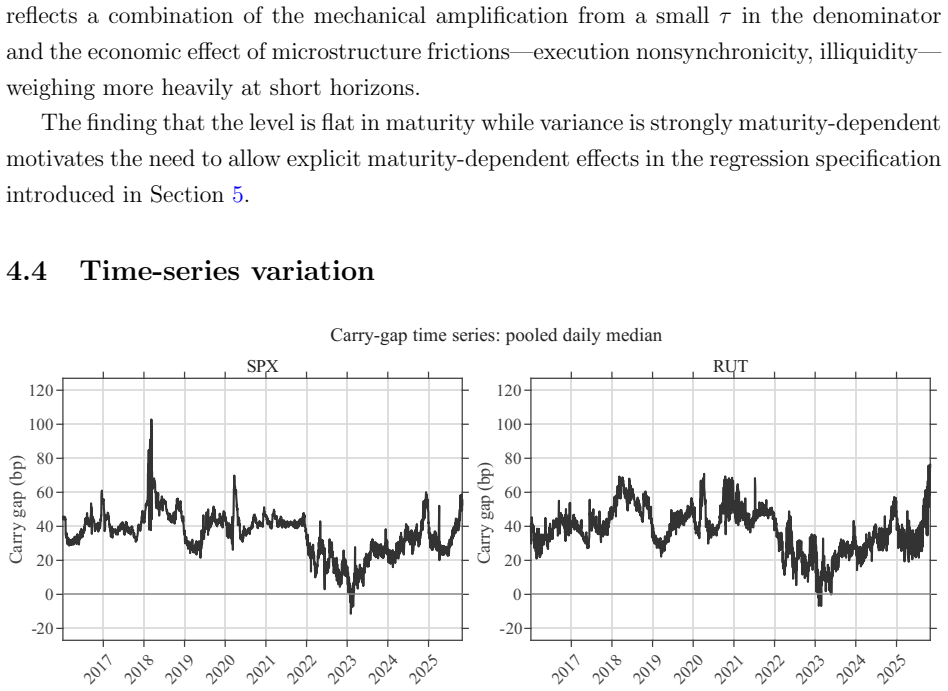

The carry gap, defined as the annualized difference between option-implied discount factors and the OIS curve, which measures the systematic wedge between price-space parity and carry-space implementation costs.

If this is right

- Arbitrage in options markets is bounded by cumulative path costs rather than static price discrepancies alone.

- Market participants must incorporate carry-space metrics when sizing parity trades, not just terminal residuals.

- Financial conditions and volatility levels directly scale the effective cost of maintaining parity positions.

- Standard no-arbitrage tests that ignore daily settlement frictions understate the true barriers to enforcement.

Where Pith is reading between the lines

- Similar hidden wedges may appear in other terminal identities such as covered-interest parity once path-dependent margin flows are measured.

- High-frequency market makers could reduce but not eliminate the gap if their own capital and settlement constraints scale with volatility.

- Regulators monitoring derivatives could add carry-gap series to existing volatility and margin-stress indicators to detect rising implementation friction.

Load-bearing premise

The reduced-form regression centered on the volatility times sqrt(tau) path-risk term correctly isolates implementation risk without omitted-variable bias or post-hoc functional-form choices.

What would settle it

If the carry gap shows no positive correlation with the volatility times sqrt(tau) term in out-of-sample periods or if the regression coefficients flip sign when any single year is dropped from the sample, the claim that the gap reflects path-dependent implementation risk would be refuted.

Figures

read the original abstract

Put-call parity is a terminal-payoff identity; quoted residuals against traded futures are near zero. Yet enforcing parity is path-dependent, exposing arbitrageurs to daily settlement, margin, and finite capital. Using minute-level NBBO data on S&P 500 and Russell 2000 options, I extract option-implied discount factors, compare them with the OIS curve, and construct an annualized carry gap. A reduced-form specification centered on a volatility times sqrt(tau) path-risk term links the carry gap to implementation risk, trading frictions, and financial conditions, with coefficient signs stable across leave-one-year-out validation. The carry gap is an implementation wedge invisible in price space but systematic in carry space.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper extracts option-implied discount factors from minute-level NBBO quotes on S&P 500 and Russell 2000 options, compares them to the OIS curve to construct an annualized carry gap, and estimates a reduced-form regression that attributes variation in this gap to a volatility times sqrt(tau) path-risk term plus controls for frictions and financial conditions. Coefficient signs are reported as stable under leave-one-year-out validation. The central claim is that the carry gap constitutes a systematic implementation wedge invisible in price space but detectable in carry space.

Significance. If the attribution holds, the result would document a previously unmeasured path-dependent cost of enforcing put-call parity in index options markets, with potential implications for arbitrage bounds, margin requirements, and the design of reduced-form pricing models that incorporate implementation risk. The high-frequency data extraction and out-of-sample stability checks are positive features.

major comments (2)

- [regression specification / methods] The reduced-form specification centers on a volatility times sqrt(tau) term without an explicit a priori derivation from a structural model of margin or settlement risk. Section describing the regression (or the methods paragraph following the gap construction) should clarify whether this functional form was selected before or after inspecting the data; if post-hoc, the attribution to implementation risk is vulnerable to omitted-variable bias from correlated liquidity or funding factors.

- [validation and robustness] Leave-one-year-out validation shows stable signs but does not address functional-form sensitivity or omitted-variable tests. The manuscript should report results under alternative specifications (e.g., linear volatility, log(tau), or interactions with margin requirements) and include a formal test for whether the vol*sqrt(tau) coefficient remains significant after adding proxies for liquidity premia or funding shocks.

minor comments (2)

- [data construction] Clarify the exact data filters applied to NBBO quotes (e.g., minimum quote size, time-to-expiration cutoffs, or handling of stale quotes) in the data section.

- [gap construction] The abstract refers to 'option-implied discount factors' but the full text should explicitly state the formula used to back out the implied rate from put-call parity residuals.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which help clarify the empirical approach and strengthen the robustness section. We respond to each major comment below and indicate planned revisions.

read point-by-point responses

-

Referee: [regression specification / methods] The reduced-form specification centers on a volatility times sqrt(tau) term without an explicit a priori derivation from a structural model of margin or settlement risk. Section describing the regression (or the methods paragraph following the gap construction) should clarify whether this functional form was selected before or after inspecting the data; if post-hoc, the attribution to implementation risk is vulnerable to omitted-variable bias from correlated liquidity or funding factors.

Authors: The vol × √τ term is motivated by the economic reasoning that path-dependent implementation risks (daily settlement, margin calls) accumulate with the square root of horizon length under standard diffusion assumptions for the underlying price process. This functional form was selected on theoretical grounds prior to full regression estimation. We will revise the methods section to state this motivation explicitly and confirm the ex-ante choice of specification, reducing concerns about post-hoc selection while retaining the reduced-form nature of the analysis. revision: yes

-

Referee: [validation and robustness] Leave-one-year-out validation shows stable signs but does not address functional-form sensitivity or omitted-variable tests. The manuscript should report results under alternative specifications (e.g., linear volatility, log(tau), or interactions with margin requirements) and include a formal test for whether the vol*sqrt(tau) coefficient remains significant after adding proxies for liquidity premia or funding shocks.

Authors: We agree that expanded robustness analysis is warranted. The revised manuscript will report coefficient estimates under alternative functional forms, including linear volatility, log(τ), and interactions with margin-requirement proxies. We will also estimate an augmented regression that adds proxies for liquidity premia and funding shocks, and we will test and report the statistical significance of the vol × √τ coefficient in that specification. revision: yes

Circularity Check

No significant circularity in empirical construction and reduced-form regression

full rationale

The paper measures the carry gap directly from minute-level NBBO data by extracting option-implied discount factors and subtracting the OIS curve, then annualizing the difference. It subsequently estimates a reduced-form regression that associates this independently constructed gap with a volatility times sqrt(tau) term plus controls. No step in the provided abstract or description reduces a claimed result to its inputs by definition, renames a fitted parameter as a prediction, or relies on self-citation for a uniqueness theorem. The functional form is presented as centered on path-risk without evidence that the regression outcome is forced tautologically. This is a standard empirical workflow with separate measurement and testing stages.

Axiom & Free-Parameter Ledger

free parameters (1)

- coefficients on volatility*sqrt(tau) and other regressors

axioms (1)

- standard math Put-call parity holds exactly as a terminal-payoff identity

Lean theorems connected to this paper

-

IndisputableMonolith.Cost.FunctionalEquationwashburn_uniqueness_aczel unclearThe GBM term used in this paper translates this structure into basis points... GBM_OIS,1Y_i,t = 10^4 * OIS_1Y_t/100 * 2/3 * Vol_i,t/100 * sqrt(2 tau_i,t / pi)

-

IndisputableMonolith.Foundation.RealityFromDistinctionreality_from_one_distinction unclearA reduced-form specification centered on a volatility times sqrt(tau) path-risk term links the carry gap to implementation risk

Reference graph

Works this paper leans on

-

[1]

Stoll, H. R. (1969). The Relationship between Put and Call Option Prices.The Journal of Finance, 24(5), 801–824.https://doi.org/10.1111/j.1540-6261.1969.tb01694.x

-

[2]

P., & Galai, D

Gould, J. P., & Galai, D. (1974). Transaction Costs and the Relationship between Put and Call Prices.Journal of Financial Economics, 1(2), 105–129.https://doi.org/10.1016/ 0304-405X(74)90001-4

1974

-

[3]

Klemkosky, R. C., & Resnick, B. G. (1979). Put–Call Parity and Market Efficiency.The Journal of Finance, 34(5), 1141–1155.https://doi.org/10.1111/j.1540-6261.1979. tb00061.x

-

[4]

Brenner, M., & Galai, D. (1986). Implied Interest Rates.The Journal of Business, 59(3), 493–507.https://doi.org/10.1086/296349

-

[5]

Shleifer, A., & Vishny, R. W. (1997). The Limits of Arbitrage.The Journal of Finance, 52(1), 35–55.https://doi.org/10.1111/j.1540-6261.1997.tb03807.x

-

[6]

F., & Tian, Y

Ackert, L. F., & Tian, Y. S. (2001). Efficiency in Index Options Markets and Trading in Stock Baskets.Journal of Banking & Finance, 25(9), 1607–1634.https://doi.org/10. 1016/S0378-4266(00)00145-X

2001

-

[7]

Gromb, D., & Vayanos, D. (2002). Equilibrium and Welfare in Markets with Financially Constrained Arbitrageurs.Journal of Financial Economics, 66(2–3), 361–407.https:// doi.org/10.1016/S0304-405X(02)00228-3

-

[8]

Ofek, E., Richardson, M., & Whitelaw, R. F. (2004). Limited arbitrage and short sales restrictions: evidence from the options markets.Journal of Financial Economics, 74(2), 305–342.https://doi.org/10.1016/j.jfineco.2003.05.008

-

[9]

Brunnermeier, M. K., & Pedersen, L. H. (2009). Market Liquidity and Funding Liquidity.The Review of Financial Studies, 22(6), 2201–2238.https://doi.org/10.1093/rfs/hhn098

-

[10]

Mitchell, M., & Pulvino, T. (2012). Arbitrage Crashes and the Speed of Capital.Journal of Financial Economics, 104(3), 469–490.https://doi.org/10.1016/j.jfineco.2011. 09.002

-

[11]

Azzone, M., & Baviera, R. (2021). Synthetic Forwards and Cost of Funding in the Equity Derivative Market.Finance Research Letters, 41, 101841.https://doi.org/10.1016/j. frl.2020.101841 26 Board of Governors of the Federal Reserve System (US) (2026a). Federal Reserve Bank of Chicago, Chicago Fed National Financial Conditions Index [NFCI], retrieved from

work page doi:10.1016/j 2021

-

[12]

Louis, April 3, 2026.https://fred.stlouisfed

FRED, Federal Reserve Bank of St. Louis, April 3, 2026.https://fred.stlouisfed. org/series/NFCI. Board of Governors of the Federal Reserve System (US) (2026b). Federal Reserve Bank of New York, Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis [DGS1MO, DGS3MO, DGS6MO, DGS1, DGS2, DGS3, DGS5, DGS7, DGS10],...

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.