Recognition: unknown

Liquidity provision in CLMMs: evidence from transactions data

Pith reviewed 2026-05-08 12:42 UTC · model grok-4.3

The pith

Only about one in six liquidity providers in WETH/USD CLMM pools on Base avoids losses without hedging or external income.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

By building a complete reconstruction of LP capital changes from transaction logs in WETH/USD pools on Base, the authors find that only about one out of six LPs avoids losses when neither hedging nor off-pool revenue is included. Successful positions concentrate near the prevailing pool price, successful providers often exit early rather than waiting for the full range to be crossed, and a separate class of multi-LP operators appears across several venues.

What carries the argument

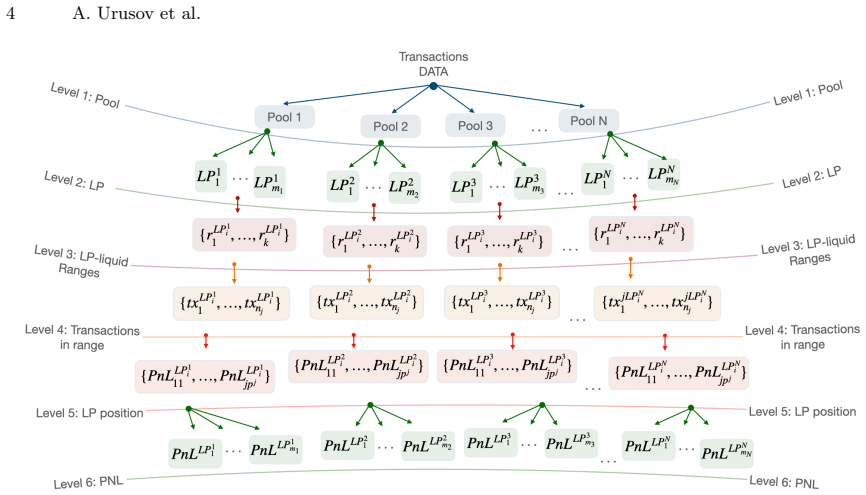

A methodology that reconstructs LP PnL trajectories directly from on-chain events together with a metric that records both terminal capital and the entire path of that capital over time.

If this is right

- Most observed LP activity would require supplementary income sources or risk hedges to be economically sustainable.

- Profitable behavior resembles short-term profit-target strategies rather than passive range holding.

- Position configurations cluster around the current price, implying that range choice is tightly linked to immediate price levels.

- Multi-pool operators constitute a distinct profitable subset whose cross-pool activity may offset single-pool losses.

Where Pith is reading between the lines

- If pool-only losses dominate, CLMM designs may need stronger built-in incentives or simpler tools to retain passive liquidity.

- Early closure patterns could reflect either superior timing or simple risk aversion that current models do not capture.

- The results suggest CLMMs currently reward active monitoring more than capital commitment alone.

Load-bearing premise

The on-chain event reconstruction captures every material capital movement and excludes no hedging trades or external profits that would change the measured outcome.

What would settle it

A wallet-level audit of a random sample of the studied LPs that compares their full off-chain portfolio returns, including any hedging or external income, against the pool-only PnL calculated by the paper.

Figures

read the original abstract

The emergence of Concentrated Liquidity Market Makers (CLMMs) has made liquidity provision on decentralized exchanges an active and risk-sensitive task. However, the standalone profitability of liquidity provision remains unclear for liquidity providers (LPs) who neither hedge their inventory risk nor receive off-pool profits. This paper studies the actual outcomes of LP activity using historical transaction-level data from WETH/USD liquidity pools on the Base chain across the Uniswap, Aerodrome, PancakeSwap and SushiSwap protocols. We propose a methodology for reconstructing LP PnL dynamics from on-chain events and introduce an original metric that captures both the terminal state of LP capital and its path over time. Based on this framework, we estimate the share of successful LPs, classify their behavior and develop a taxonomy of 15 position types as structural components of PnL. We further identify a distinct class of multi-LPs operating across several pools and show that the dominant profitable position configurations are concentrated around the current pool price. The results show that only about one out of six LPs avoids losses in the selected market segment, raising an open question about the true economic motives of LP participation. Evidence also suggests that successful LPs often close positions before the full range is traversed, making observed behavior closer to profit-target-based strategies.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper analyzes liquidity provision outcomes in Concentrated Liquidity Market Makers (CLMMs) using historical on-chain transaction data from WETH/USD pools on the Base chain across Uniswap, Aerodrome, PancakeSwap, and SushiSwap. It proposes a methodology to reconstruct LP profit-and-loss (PnL) dynamics directly from mint/burn/swap events, introduces a metric that incorporates both terminal capital and path-dependent outcomes, reports that only about one in six LPs avoids losses, develops a taxonomy of 15 position types, identifies a class of multi-LPs operating across protocols, and observes that successful LPs tend to close positions early rather than holding until the full range is traversed.

Significance. If the reconstruction pipeline is shown to be complete and unbiased, the study supplies rare large-scale empirical evidence on the standalone profitability of unhedged liquidity provision in CLMMs. The finding that only roughly 17 % of LPs avoid losses, together with the behavioral taxonomy and the concentration of profitable configurations near the current price, directly informs debates about LP incentives, risk management, and the economic rationale for participation in decentralized exchanges. The purely observational, data-driven design and the absence of fitted parameters or self-referential definitions are strengths that allow the results to serve as a benchmark for future theoretical work.

major comments (2)

- [Methodology section describing the PnL reconstruction pipeline] The headline result (only ~1/6 LPs avoid losses) and the associated behavioral classifications rest on the event-reconstruction pipeline correctly computing terminal capital and path-dependent PnL for every position. The manuscript does not describe (a) how mint/burn/swap events are attributed to LP addresses and position IDs without omission or double-counting, (b) inclusion of gas fees and protocol costs, or (c) handling of multi-LP addresses that operate across the four protocols. Without explicit validation against synthetic test cases or known benchmarks, it remains possible that off-pool hedging, partial closures, or unrecorded costs are omitted, which would systematically overstate the success rate. This issue is load-bearing for the central claim and for the taxonomy of 15 position types.

- [Results and taxonomy sections] The claim that successful LPs close positions before the full range is traversed is presented as evidence of profit-target behavior. This interpretation presupposes that the reconstructed trajectories are faithful up to the moment of closure. Any truncation or mis-attribution in the on-chain event stream would directly affect both the measured share of successful LPs and the structural classification of position types.

minor comments (1)

- [Abstract] The abstract states that the methodology reconstructs PnL from on-chain events but provides no high-level summary of the key implementation choices (event attribution, cost inclusion, multi-protocol handling). Adding one or two sentences would improve readability for readers who do not immediately consult the methods section.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive comments. Below we respond point by point to the major remarks, indicating where we will revise the manuscript to improve clarity and robustness.

read point-by-point responses

-

Referee: [Methodology section describing the PnL reconstruction pipeline] The headline result (only ~1/6 LPs avoid losses) and the associated behavioral classifications rest on the event-reconstruction pipeline correctly computing terminal capital and path-dependent PnL for every position. The manuscript does not describe (a) how mint/burn/swap events are attributed to LP addresses and position IDs without omission or double-counting, (b) inclusion of gas fees and protocol costs, or (c) handling of multi-LP addresses that operate across the four protocols. Without explicit validation against synthetic test cases or known benchmarks, it remains possible that off-pool hedging, partial closures, or unrecorded costs are omitted, which would systematically overstate the success rate. This issue is load-bearing for the central claim and for the taxonomy of 15 position types.

Authors: We agree that greater transparency on the reconstruction pipeline is required. In the revised manuscript we will expand the Methodology section with three new paragraphs that (a) detail the attribution logic, showing how position IDs and LP addresses are used to link mint/burn/swap events while applying deduplication checks across the four protocols, (b) explicitly state that gas fees are subtracted from terminal capital using the gas_used and gas_price fields from the transaction receipts and that protocol fees are incorporated via the feeGrowthInside variables, and (c) describe the multi-LP identification procedure, which flags addresses active in more than one protocol and treats each pool-specific position separately to avoid double-counting. We will also add a validation subsection that reports results from synthetic test cases in which we replay known LP strategies (full-range, narrow-range, and rebalancing) on a simulated pool and confirm that the pipeline recovers the expected PnL within rounding error. These additions directly address the possibility of systematic bias in the success-rate estimate. revision: yes

-

Referee: [Results and taxonomy sections] The claim that successful LPs close positions before the full range is traversed is presented as evidence of profit-target behavior. This interpretation presupposes that the reconstructed trajectories are faithful up to the moment of closure. Any truncation or mis-attribution in the on-chain event stream would directly affect both the measured share of successful LPs and the structural classification of position types.

Authors: We accept that the profit-target interpretation is conditional on the completeness of the observed event streams. In the revised Results section we will insert a dedicated limitations paragraph that (i) reiterates that all trajectories are constructed exclusively from on-chain mint/burn/swap events and therefore exclude any off-chain hedging or private transfers, (ii) reports a robustness check in which we restrict the sample to positions whose entire event history is present in our data extract, and (iii) notes that the 15-type taxonomy is defined solely by the sequence of observed on-chain actions. These clarifications will qualify the behavioral claim without altering the reported statistics. revision: partial

Circularity Check

No significant circularity; purely observational data analysis

full rationale

The paper's core contribution is an empirical reconstruction of LP PnL trajectories from on-chain mint/burn/swap events across four protocols, followed by direct computation of the fraction of positions that end with positive terminal capital. The methodology and 15-type taxonomy are definitional tools applied to the event stream; the headline statistic (approximately one in six LPs avoid losses) is a simple count of reconstructed outcomes rather than a fitted prediction or self-referential definition. No equations reduce a claimed result to its own inputs, no parameters are estimated and then relabeled as predictions, and no load-bearing claims rest on self-citations. The derivation chain consists of transparent data-processing steps whose outputs are falsifiable against the raw transaction logs.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption All relevant components of LP profit and loss are captured in the recorded on-chain events

invented entities (1)

-

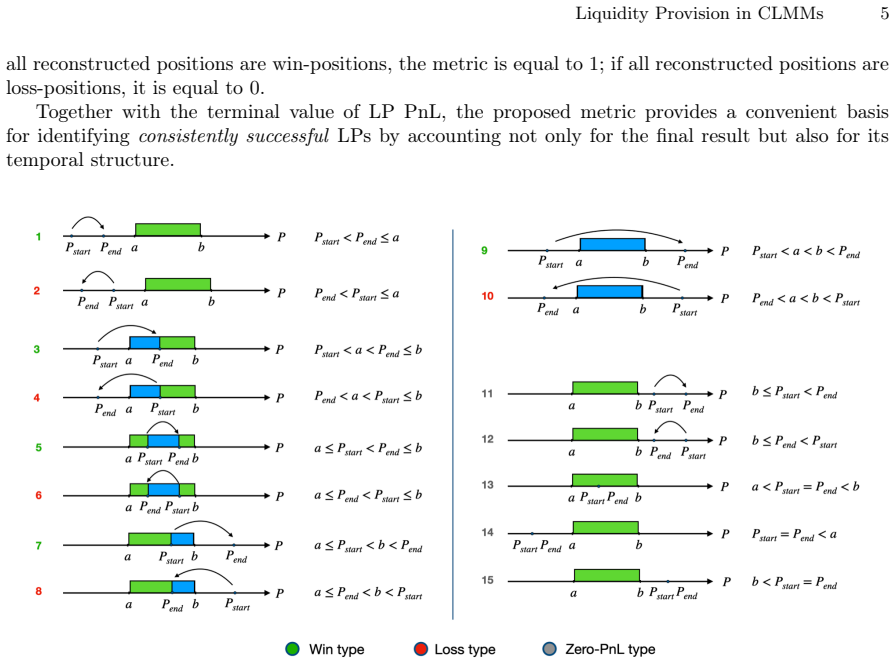

taxonomy of 15 position types

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Bitcoin: A Peer-to-Peer Electronic Cash System, 2008

Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System, 2008

2008

-

[2]

A next-generation smart contract and decentralized application platform

Buterin, V. A next-generation smart contract and decentralized application platform. White paper, 2014

2014

-

[3]

Schär, F. Decentralized Finance: On Blockchain- and Smart Contract-Based Financial Markets, Federal Reserve Bank of St. Louis Review, Second Quarter 2021, pp. 153-74. https://doi.org/10.20955/r.103.153-74

-

[4]

Uniswap v3 Core, 2021

Adams, H., Zinsmeister, N., Salem, M., Keefer, R., and Robinson, D. Uniswap v3 Core, 2021. Tech. Rep. https://uniswap.org/whitepaper-v3.pdf

2021

-

[5]

Risks and returns of uniswap v3 liquidity providers

Heimbach, L., Schertenleib, E., and Wattenhofer, R. Risks and returns of uniswap v3 liquidity providers. In Proceedings of the 4th ACM Conference on Advances in Financial Technologies (pp. 89-101), 2022, September

2022

-

[6]

Predictable losses of liquidity provision in constant function markets and concentrated liquidity markets

Cartea, Á., Drissi, F., and Monga, M. Predictable losses of liquidity provision in constant function markets and concentrated liquidity markets. Applied Mathematical Finance, 30(2), 69-93, 2023

2023

- [7]

-

[8]

Liquidity Math in Uniswap v3

Elsts, A. Liquidity Math in Uniswap v3. Available at SSRN 4575232, 2021

2021

-

[9]

Echenim, M., Gobet, E., and Maurice, A. C. Thorough mathematical modelling and analysis of Uniswap v3. hal-04214315v2, 2023

2023

-

[10]

DEX Specs: A Mean Field Approach to DeFi Currency Exchanges

Bayraktar, E., Cohen, A., and Nellis, A. DEX Specs: A Mean Field Approach to DeFi Currency Exchanges. arXiv preprint arXiv:2404.09090, 2024

-

[11]

Capponi, Agostino and Jia, Ruizhe, Liquidity provision on blockchain-based decentralized exchanges. (2025). The Review of Financial Studies, 38(10), 3040-3085

2025

-

[12]

J., Altschuler, B., Sun, H., Wang, X., and Parkes, D

Fan, Z., Marmolejo-Cossío, F. J., Altschuler, B., Sun, H., Wang, X., and Parkes, D. Differential Liquid- ity Provision in Uniswap v3 and Implications for Contract Design. In Proceedings of the Third ACM International Conference on AI in Finance (pp. 9-17), 2022

2022

-

[13]

Backtesting Framework for Concentrated Liquidity Market Makers on Uniswap V3 Decentralized Exchange

Urusov, A., Berezovskiy, R., and Yanovich, Y. Backtesting Framework for Concentrated Liquidity Market Makers on Uniswap V3 Decentralized Exchange. Blockchain: Research and Applications, 100256, ISSN 2096-7209, 2025

2096

- [14]

-

[15]

Loesch, S., Hindman, N., Richardson, M. B., and Welch, N. Impermanent loss in uniswap v3. arXiv preprint arXiv:2111.09192, 2021

-

[16]

Moallemi, Tim Roughgarden, and Anthony Lee Zhang

Milionis, J., Moallemi, C. C., Roughgarden, T., and Zhang, A. L. Automated market making and loss- versus-rebalancing. arXiv preprint arXiv:2208.06046, 2022

- [17]

- [18]

-

[19]

H., Chan, E., and Fanti, G

Tang, W., El-Azouzi, R., Lee, C. H., Chan, E., and Fanti, G. (2025). Game theoretic liquidity provision- ing in concentrated liquidity market makers. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 9(1), 1-45

2025

-

[20]

A. Urusov. Base LP Research: source code, data and scripts. 14 A. Urusov et al. Appendix A Win-score metric methodology. To identifyconsistently successfulLPs, we introduce thewin-scoremetric. For the set of reconstructed position-level PnL values ofLPc i , ordered by position closing time, we will use the notation P nLPos = P nLjMα We then split this set...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.