Recognition: unknown

Concave Statistical Utility Maximization Bandits via Influence-Function Gradients

Pith reviewed 2026-05-08 10:21 UTC · model grok-4.3

The pith

Infinite-horizon bandits with concave statistical utilities reduce to simplex optimization using influence-function gradients for stochastic updates.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under mild continuity assumptions the infinite-horizon problem reduces to optimizing the concave map U(w) = 𝔘(P^w) over weight vectors w on the simplex, where P^w is the mixture law induced by w. For differentiable statistical utilities, influence-function calculus supplies stochastic gradient estimators observable from bandit feedback; these drive an entropic mirror-ascent algorithm on a truncated simplex implemented by multiplicative-weights updates and plug-in influence estimates. Regret bounds are proved that separate the mirror-ascent optimization error from the bias incurred by estimating the influence function.

What carries the argument

Influence-function calculus that produces stochastic gradient estimators for the utility U(w) from bandit observations of individual arms.

If this is right

- The long-run bandit objective becomes a finite-dimensional concave program over the probability simplex.

- Regret decomposes explicitly into mirror-ascent optimization error and bias from influence estimation.

- The same algorithmic template applies to any differentiable concave distributional utility, including variance and Wasserstein distance.

- Implementation choices (exact versus plug-in influence functions) trade computational cost against estimation bias.

Where Pith is reading between the lines

- The framework may extend to other differentiable statistical functionals such as quantiles or entropies once their influence functions are known.

- In finite-sample regimes the estimation bias term could dominate, suggesting that variance-reduction techniques for influence estimators would improve practical performance.

- Stationary-mixture restriction may limit direct use in non-stationary or adversarial environments where time-varying policies are required.

- The separation of optimization and estimation errors offers a template for analyzing other gradient-based methods that rely on statistical functionals rather than raw expectations.

Load-bearing premise

Mild continuity conditions suffice to reduce the infinite-horizon problem to optimization over stationary mixture policies, together with differentiability of the statistical utility.

What would settle it

A numerical check in which the plug-in influence-function gradient estimator fails to converge in probability to the true gradient of U as the number of samples per arm grows, or in which the observed regret does not decompose additively into an optimization term and an estimation-bias term.

Figures

read the original abstract

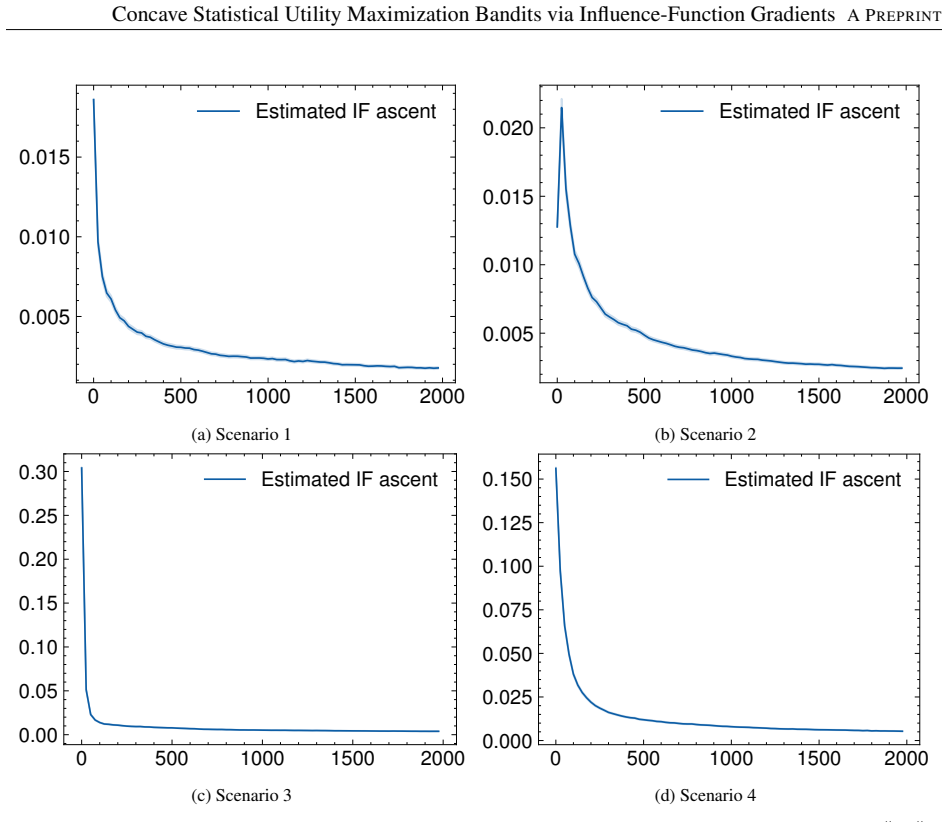

We study stochastic multi-armed bandits in which the objective is a statistical functional of the long-run reward distribution, rather than expected reward alone. Under mild continuity assumptions, we show that the infinite-horizon problem reduces to optimizing over stationary mixed policies: each weight vector \(w\) on the simplex induces a mixture law \(P^w\), and performance is measured by the concave utility \(U(w)=\mathfrak U(P^w)\). For differentiable statistical utilities, we use influence-function calculus to derive stochastic gradient estimators from bandit feedback. This leads to an entropic mirror-ascent algorithm on a truncated simplex, implemented through multiplicative-weights updates and plug-in estimates of the influence function. We establish regret bounds that separate the mirror-ascent optimization error from the bias caused by estimating the influence function. The framework is developed for general concave distributional utilities and illustrated through variance and Wasserstein objectives, with numerical experiments comparing exact and plug-in influence-function implementations.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies stochastic multi-armed bandits where the objective is a concave statistical functional 𝔘 of the long-run reward distribution rather than expected reward. Under mild continuity assumptions, the infinite-horizon problem reduces to optimizing a concave utility U(w)=𝔘(P^w) over stationary mixed policies w on the simplex; influence-function calculus then yields stochastic gradient estimators from bandit feedback, which are used in an entropic mirror-ascent algorithm (multiplicative-weights updates with plug-in influence estimates). Regret bounds are derived that separate mirror-ascent optimization error from bias due to influence-function estimation. The framework is illustrated on variance and Wasserstein objectives with numerical experiments.

Significance. If the reduction and gradient construction hold, the work provides a general, modular approach for optimizing non-linear distributional objectives in bandits, extending beyond mean-based methods. The explicit separation of optimization and estimation errors in the regret analysis, together with the use of influence functions for general concave utilities, is a clear technical contribution with potential applicability to risk-sensitive or fairness-aware settings.

major comments (2)

- [Abstract and §2] Abstract and §2 (Reduction to stationary policies): The load-bearing claim that the infinite-horizon problem reduces exactly to optimizing U(w)=𝔘(P^w) under 'mild continuity assumptions' is stated without explicit conditions (e.g., Lipschitz continuity of 𝔘 w.r.t. weak topology, bounded moments on reward distributions, or absence of transient effects). Without these, it is unclear whether the long-run mixture law P^w coincides with the value of the original discounted or undiscounted objective for every fixed w.

- [§4] §4 (Regret analysis): The decomposition that isolates mirror-ascent error from influence-function bias presupposes that the reduction to U(w) has already occurred and that the influence-function estimator is unbiased for the gradient of U. If the continuity conditions fail for the Wasserstein case (as the skeptic notes), the bounds target the wrong objective and the separation does not apply to the original problem.

minor comments (2)

- [§5] §5 (Experiments): Specify the truncation level of the simplex, the exact form of the plug-in influence estimator, and any additional hyperparameters used in the multiplicative-weights implementation.

- [Notation] Notation throughout: Ensure consistent definition of the mixture law P^w and the functional 𝔘 before their first use; a short table of notation would improve readability.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive report. The two major comments raise important points about the rigor of the reduction to stationary policies and the scope of the regret analysis. We address each below and indicate the revisions we will make.

read point-by-point responses

-

Referee: [Abstract and §2] Abstract and §2 (Reduction to stationary policies): The load-bearing claim that the infinite-horizon problem reduces exactly to optimizing U(w)=𝔘(P^w) under 'mild continuity assumptions' is stated without explicit conditions (e.g., Lipschitz continuity of 𝔘 w.r.t. weak topology, bounded moments on reward distributions, or absence of transient effects). Without these, it is unclear whether the long-run mixture law P^w coincides with the value of the original discounted or undiscounted objective for every fixed w.

Authors: We agree that the reduction requires explicit conditions to be fully rigorous. In the current manuscript, §2 invokes continuity of 𝔘 with respect to the weak topology together with uniform integrability of the reward distributions to ensure that the long-run empirical measure converges to P^w for any stationary w. To strengthen the presentation, we will insert a new lemma (Lemma 2.1) that states the precise hypotheses: (i) 𝔘 is Lipschitz continuous on the space of probability measures equipped with the weak topology, (ii) all reward distributions have uniformly bounded second moments, and (iii) the policy is stationary so that transient effects vanish in the infinite-horizon limit. Under these conditions the equality between the original objective and U(w) holds exactly. The revised version will also include a short appendix paragraph verifying that the stated assumptions are satisfied by the variance and Wasserstein examples. revision: yes

-

Referee: [§4] §4 (Regret analysis): The decomposition that isolates mirror-ascent error from influence-function bias presupposes that the reduction to U(w) has already occurred and that the influence-function estimator is unbiased for the gradient of U. If the continuity conditions fail for the Wasserstein case (as the skeptic notes), the bounds target the wrong objective and the separation does not apply to the original problem.

Authors: The regret theorem in §4 is explicitly conditioned on the reduction of §2; the decomposition therefore applies to the original infinite-horizon objective precisely when the continuity and moment conditions hold. For the Wasserstein utility we verify in the supplementary material (Proposition B.3) that the 1-Wasserstein distance is Lipschitz with respect to the weak topology on the compact support assumed for the rewards, so the influence function exists and the plug-in estimator is unbiased for ∇U(w). Consequently the bias term in the regret bound remains valid and the separation between optimization error and estimation bias continues to hold for the original problem. We will add a clarifying sentence in §4 and a cross-reference to Proposition B.3 to make this dependence explicit. revision: partial

Circularity Check

No circularity: reduction and gradient derivation are independent of fitted inputs or self-citations

full rationale

The paper's central step is a modeling reduction of the infinite-horizon bandit problem to optimization of U(w) = 𝔘(P^w) over stationary mixtures w, justified by mild continuity assumptions on the utility functional. This is followed by a direct application of influence-function calculus (a standard statistical tool) to obtain stochastic gradients from bandit samples, and regret bounds that explicitly separate mirror-ascent error from estimation bias. No equation reduces a claimed prediction to a fitted parameter by construction, no load-bearing uniqueness theorem is imported via self-citation, and the derivation chain does not rename or smuggle in prior results as new content. The framework remains self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption mild continuity assumptions

Reference graph

Works this paper leans on

-

[1]

Mirror descent and nonlinear projected subgradient methods for convex optimization , volume =

doi: 10.1016/S0167-6377(02)00231-6. Albert Benveniste, Michel Métivier, and Pierre Priouret.Adaptive Algorithms and Stochastic Approximations. Springer, Berlin, Heidelberg,

-

[2]

doi: 10.1007/978-3-642-75894-2. Vivek S. Borkar.Stochastic Approximation: A Dynamical Systems Viewpoint, volume 48 ofTexts and Readings in Mathematics. Hindustan Book Agency,

-

[3]

23 Concave Statistical Utility Maximization Bandits via Influence-Function GradientsA PREPRINT L

doi: 10.1007/978-93-86279-38-5. 23 Concave Statistical Utility Maximization Bandits via Influence-Function GradientsA PREPRINT L. M. Bregman. The relaxation method of finding the common point of convex sets and its application to the solution of problems in convex programming.USSR Computational Mathematics and Mathematical Physics, 7(3):200–217,

-

[4]

doi: 10.1016/0041-5553(67)90040-7. Sébastien Bubeck and Nicolò Cesa-Bianchi. Regret analysis of stochastic and nonstochastic multi-armed bandit problems.Foundations and Trends in Machine Learning, 5(1):1–122,

-

[5]

Asaf Cassel, Shie Mannor, and Assaf Zeevi

doi: 10.1561/2200000024. Asaf Cassel, Shie Mannor, and Assaf Zeevi. A general framework for bandit problems beyond cumulative objectives. Mathematics of Operations Research, 48(4):2196–2232,

-

[6]

Charlie Frogner, Chiyuan Zhang, Hossein Mobahi, Mauricio Araya, and Tomaso A Poggio

doi: 10.1214/aoms/1177728174. Charlie Frogner, Chiyuan Zhang, Hossein Mobahi, Mauricio Araya, and Tomaso A Poggio. Learning with a wasserstein loss.Advances in neural information processing systems, 28,

-

[7]

Anmol Kagrecha, Jayakrishnan Nair, and Krishna P Jagannathan

doi: 10.3182/20080706-5-KR-1001.01959. Anmol Kagrecha, Jayakrishnan Nair, and Krishna P Jagannathan. Distribution oblivious, risk-aware algorithms for multi-armed bandits with unbounded rewards. InNeurIPS, pages 11269–11278,

-

[8]

doi: 10.1109/CDC.2015. 7402714. Harold J. Kushner and G. George Yin.Stochastic Approximation and Recursive Algorithms and Applications. Springer, New York, 2 edition,

-

[9]

Tor Lattimore and Csaba Szepesvári.Bandit algorithms

doi: 10.1007/b97441. Tor Lattimore and Csaba Szepesvári.Bandit algorithms. Cambridge University Press,

-

[10]

A Modern Introduction to Online Learning

doi: 10.1137/070704277. Francesco Orabona. A modern introduction to online learning.arXiv preprint arXiv:1912.13213,

work page internal anchor Pith review Pith/arXiv arXiv doi:10.1137/070704277 1912

-

[11]

doi: 10.1007/978-3-319-20828-2. URLhttps://link.springer.com/book/10.1007/978-3-319-20828-2. Peter Z Schochet, Mike Puma, John Deke, et al. Understanding variation in treatment effects in education impact evaluations: An overview of quantitative methods.US Department of Education, Washington, DC. Report No. NCEE, 4017,

-

[12]

doi: 10.1561/2200000018. Richard S. Sutton, David A. McAllester, Satinder P. Singh, and Yishay Mansour. Policy gradient methods for reinforcement learning with function approximation. In S. A. Solla, T. K. Leen, and K.-R. Müller, editors,Advances in Neural Information Processing Systems 12, pages 1057–1063. MIT Press,

-

[13]

Meltem Tatlı, Arpan Mukherjee, Karthikeyan Shanmugam, Ali Tajer, et al. Preference-centric bandits: Optimality of mixtures and regret-efficient algorithms.arXiv preprint arXiv:2504.20877, 2025a. Meltem Tatlı, Arpan Mukherjee, Karthikeyan Shanmugam, Ali Tajer, et al. Risk-sensitive bandits: Arm mixture optimality and regret-efficient algorithms.arXiv prepr...

-

[14]

doi: 10.1007/BF00992696. Massimiliano Zanin, Juan Manuel Tuñas, and Ernestina Menasalvas. Understanding diseases as increased heterogeneity: a complex network computational framework.Journal of The Royal Society Interface, 15(145),

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.