Recognition: unknown

Multiplicative Contractions, Additive Recoveries: Functional-Form Restrictions on Risk Exposure Dynamics

Pith reviewed 2026-05-08 06:47 UTC · model grok-4.3

The pith

Risk exposures contract multiplicatively when VaR constraints bind and recover additively when slack, as shown in margin debt regressions.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

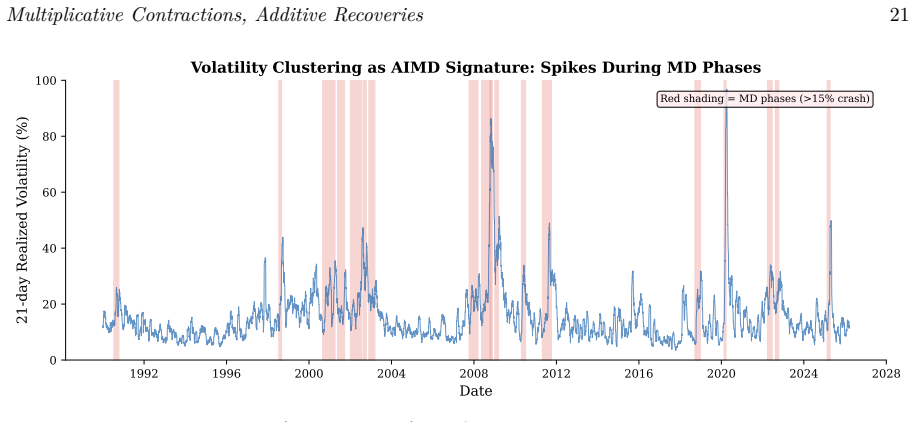

Regime-interacted regressions of detrended margin growth on lagged level produce a near-zero slope in calm periods and a significantly negative slope in stress periods, with a Wald test rejecting equality of the two slopes. This pattern is consistent with multiplicative contraction under binding constraints and additive recovery under slack constraints. The implied restriction on duration ratios is then tested directly: deeper drawdowns exhibit substantially lower recovery hazards in Cox models, with the effect replicating across indices and surviving controls for price-level dynamics alone.

What carries the argument

Regime-conditional functional-form restriction on risk-exposure dynamics: multiplicative contraction (growth rate proportional to lagged level) when VaR constraints bind, additive recovery (level-independent growth) when constraints are slack.

If this is right

- Deeper market crashes produce longer drawdown-to-recovery duration ratios than shallower ones.

- The duration asymmetry strengthens as crash depth increases, with median ratios exceeding 3 for crashes larger than 30 percent.

- Standard price-based models without an explicit exposure state variable cannot reproduce the regime-specific flip in dependence on lagged level.

- The pattern appears consistently across eight additional equity indices beyond the S&P 500.

Where Pith is reading between the lines

- Asset-pricing models that treat exposure adjustment as uniform across regimes would miss an important source of asymmetry in volatility and recovery speeds.

- Direct tests on weekly CFTC positioning data could provide a second, independent check on the same functional-form restriction.

- Regulatory VaR limits may accelerate deleveraging precisely because they enforce multiplicative rather than additive adjustments during stress.

Load-bearing premise

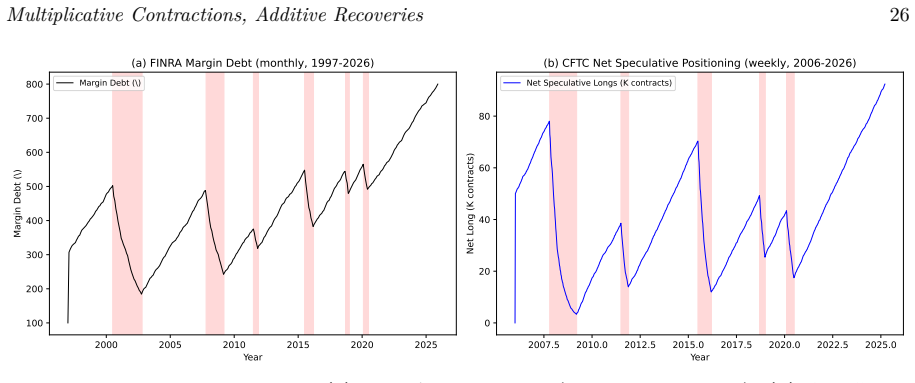

FINRA monthly margin debt serves as a valid proxy for the aggregate risk-exposure dynamics of VaR-constrained intermediaries, and additive recovery follows from constant-rate capital replenishment when constraints are slack.

What would settle it

A regression of margin growth on lagged level that yields statistically indistinguishable slopes across calm and stress regimes, or historical drawdown data in which recovery duration shows no positive relation to crash depth.

Figures

read the original abstract

We test a regime-conditional functional-form restriction on aggregate risk-exposure dynamics implied by VaR-constrained intermediary models: exposures contract multiplicatively when capital constraints bind and grow additively (level-independent) when slack. The contraction half follows from binding VaR constraints (Brunnermeier and Pedersen 2009; Adrian and Shin 2010; He and Krishnamurthy 2013). The additive-rebuild prediction is derived under constant-rate capital replenishment; we test the joint restriction on FINRA monthly margin debt (1997-2026). Two findings. First, regime-interacted regression of detrended margin growth on lagged level (T=350 months) yields calm slope -0.040 (p=0.082, additive) and stress slope -0.205 (p<0.001, multiplicative); Wald test on regime x level interaction rejects equal dependence (p=0.0016). Second, the restriction implies drawdown-recovery duration ratio increases with crash depth. On 73 S&P 500 episodes (1950-2026), Cox model gives depth coefficient -13.75 (p<10^{-7}): 75% lower recovery hazard per 10pp deeper drawdown. Continuous-depth regression yields beta=1.22 (p=0.047); beta=1.59 (p<0.001) excluding 1980-82 Volcker. Median duration ratio for crashes >30% is 3.1x; replicates across eight other equity indices. Calibrated Heston, Markov-switching, and block bootstrap nulls match price-level duration asymmetry but lack an exposure state variable, so cannot speak to the regime-conditional flip on direct exposures. We do not claim the exposure test identifies the intermediary mechanism: FINRA margin debt is a noisy proxy. We claim only that the regime-conditional functional form is a sharper target than return-level moments alone, and confirming it on margin debt is consistent with -- not proof of -- the constrained-intermediary mechanism. A companion test on CFTC weekly speculative positioning is left for future work (Sections 5.2 and F).

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript tests a regime-conditional functional-form restriction on aggregate risk-exposure dynamics implied by VaR-constrained intermediary models: multiplicative contraction when capital constraints bind and additive (level-independent) growth when slack. The contraction follows from binding VaR models; the additive recovery is derived from an explicit constant-rate capital replenishment assumption. Using FINRA monthly margin debt (1997-2026) as proxy, regime-interacted regressions of detrended margin growth on lagged level yield a calm-period slope of -0.040 (p=0.082) and stress-period slope of -0.205 (p<0.001), with Wald test rejecting equal slopes (p=0.0016). The restriction implies depth-dependent drawdown-recovery duration ratios, tested via Cox models on 73 S&P 500 episodes (1950-2026) and replicated across eight other equity indices, with depth coefficient -13.75 (p<10^{-7}). The paper explicitly caveats that margin debt is a noisy proxy and does not claim identification of the intermediary mechanism.

Significance. If the central empirical patterns hold, the paper supplies a sharper, falsifiable target for constrained-intermediary models than return-level moments alone. Strengths include the explicit derivation of the additive recovery from a stated assumption, the use of independent data for the duration test, the Wald interaction test, and replication of the duration asymmetry across indices. The modest framing (consistent with, not proof of, the mechanism) and acknowledgment that calibrated null models match price asymmetries without an exposure state variable are appropriate.

major comments (2)

- [Empirical implementation on FINRA margin debt (abstract and §4)] The central claim requires that the regime-conditional slopes on detrended margin growth test the VaR-binding multiplicative contraction versus constant-rate additive recovery. However, FINRA margin debt aggregates customer margin accounts at broker-dealers, reflecting retail and institutional borrowing for long positions rather than the intermediaries' own balance-sheet risk exposures or capital dynamics (as in the cited Brunnermeier-Pedersen 2009, Adrian-Shin 2010, and He-Krishnamurthy 2013 channels). Client deleveraging may be driven by liquidity, redemption, or sentiment factors uncorrelated with supply-side VaR constraints, so the significant Wald interaction (p=0.0016) and implied depth-dependent recovery durations may not map to the theoretical restriction. The manuscript correctly notes the proxy is noisy but does not secure the link from data pattern to model prediction.

- [Duration analysis on equity indices (abstract and §5)] The second finding tests an implication of the restriction (drawdown-recovery duration ratio increases with crash depth) via Cox models on equity price episodes, yielding depth coefficient -13.75 (p<10^{-7}) and continuous-depth beta=1.22 (p=0.047). Yet the manuscript acknowledges that calibrated Heston, Markov-switching, and block-bootstrap nulls reproduce the price-level duration asymmetry without an exposure state variable, so these results cannot directly validate the regime-conditional flip on direct exposures. This indirect test therefore provides weaker support for the functional-form claim on risk exposures than the margin-debt regressions.

minor comments (2)

- [Regression results] The calm-period slope of -0.040 has p=0.082; the manuscript interprets this as consistent with additive recovery, but a brief discussion of whether this meets a conventional threshold for 'near-zero' or additive behavior would clarify the strength of evidence for the calm regime.

- [Data description] The sample period is listed as 1997-2026; confirm the terminal date and any data revisions or updates through 2024 or later in the data section.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive report. We address the two major comments below, clarifying the scope of our empirical claims while preserving the manuscript's modest framing that the results are consistent with—not identification of—the constrained-intermediary mechanism.

read point-by-point responses

-

Referee: [Empirical implementation on FINRA margin debt (abstract and §4)] The central claim requires that the regime-conditional slopes on detrended margin growth test the VaR-binding multiplicative contraction versus constant-rate additive recovery. However, FINRA margin debt aggregates customer margin accounts at broker-dealers, reflecting retail and institutional borrowing for long positions rather than the intermediaries' own balance-sheet risk exposures or capital dynamics (as in the cited Brunnermeier-Pedersen 2009, Adrian-Shin 2010, and He-Krishnamurthy 2013 channels). Client deleveraging may be driven by liquidity, redemption, or sentiment factors uncorrelated with supply-side VaR constraints, so the significant Wald interaction (p=0.0016) and implied depth-dependent recovery durations may not map to the theoretical restriction. The manuscript correctly notes the proxy is noisy but does

Authors: We agree that FINRA margin debt is an indirect proxy capturing customer borrowing rather than intermediaries' proprietary capital or VaR positions directly. The manuscript already states explicitly that we do not claim identification of the intermediary mechanism and that the series is noisy. Our test instead asks whether the theoretically predicted regime-conditional functional form—multiplicative contraction under stress and additive recovery when slack—appears in this observable aggregate exposure proxy, which remains the most comprehensive public measure of leveraged market positions. The statistically significant regime interaction (p=0.0016) documents a descriptive pattern in the data that matches the restriction's qualitative prediction. We have made a partial revision to Section 4 to discuss how demand-side client factors could interact with supply-side constraints while underscoring that the result supplies a sharper, falsifiable target than unconditional return moments. revision: partial

-

Referee: [Duration analysis on equity indices (abstract and §5)] The second finding tests an implication of the restriction (drawdown-recovery duration ratio increases with crash depth) via Cox models on equity price episodes, yielding depth coefficient -13.75 (p<10^{-7}) and continuous-depth beta=1.22 (p=0.047). Yet the manuscript acknowledges that calibrated Heston, Markov-switching, and block-bootstrap nulls reproduce the price-level duration asymmetry without an exposure state variable, so these results cannot directly validate the regime-conditional flip on direct exposures. This indirect test therefore provides weaker support for the functional-form claim on risk exposures than the margin-debt regressions.

Authors: We concur that the duration analysis tests an implication of the restriction rather than directly validating an exposure state variable, and the manuscript already notes that calibrated null models without such a variable can generate similar price asymmetries. The functional-form restriction nonetheless yields a specific, depth-dependent prediction for recovery hazard that is distinct from the unconditional asymmetries produced by the cited nulls. The depth coefficient of -13.75 (p<10^{-7}) and its replication across eight equity indices document a robust empirical pattern that any model of risk-exposure dynamics—intermediary or otherwise—should match. We have made a partial revision to Section 5 to frame this test more explicitly as a consistency check on the restriction's implication rather than standalone evidence for the mechanism. revision: partial

Circularity Check

No significant circularity; derivation imports external theory and tests on independent data

full rationale

The multiplicative contraction is taken from external citations (Brunnermeier-Pedersen 2009, Adrian-Shin 2010, He-Krishnamurthy 2013) rather than derived internally. The additive recovery follows from an explicitly stated assumption of constant-rate capital replenishment when constraints are slack, which is not fitted to or defined by the test data. Regime-conditional regressions on FINRA margin debt and Cox models on S&P 500 drawdowns are standard empirical specifications that do not reduce the functional-form restriction to a tautology or self-citation chain. The paper explicitly disclaims identification of the intermediary mechanism and treats the margin-debt proxy as noisy. No self-definitional, fitted-input-called-prediction, or load-bearing self-citation steps are present.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption VaR constraints bind and imply multiplicative contraction of exposures

- ad hoc to paper Capital is replenished at a constant rate when constraints are slack

Reference graph

Works this paper leans on

-

[1]

Liquidity and leverage.Journal of Financial Intermediation, 19(3):418–437, 2010

Tobias Adrian and Hyun Song Shin. Liquidity and leverage.Journal of Financial Intermediation, 19(3):418–437, 2010. Tobias Adrian, Erkko Etula, and Tyler Muir. Financial intermediaries and the cross-section of asset returns.The Journal of Finance, 69(6):2557–2596, 2014. Andrew Ang and Geert Bekaert. Regime switches in interest rates.Journal of Business and...

2010

-

[2]

Tim Bollerslev

Association, Business and Economic Statistics Section, pages 177–181, 1976. Tim Bollerslev. Generalized autoregressive conditional heteroskedasticity.Journal of Economet- rics, 31(3):307–327, 1986. Markus K Brunnermeier and Lasse Heje Pedersen. Market liquidity and funding liquidity.The Review of Financial Studies, 22(6):2201–2238, 2009. Alexei Chekhlov, ...

1976

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.