Recognition: unknown

Implied Volatility Expansions for VIX Options in Forward Variance Models

Pith reviewed 2026-05-07 13:58 UTC · model grok-4.3

The pith

Forward variance models admit closed-form expansions for the implied volatility of VIX options.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

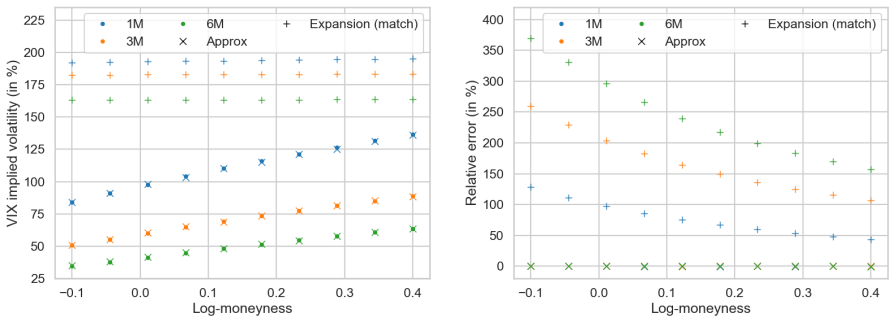

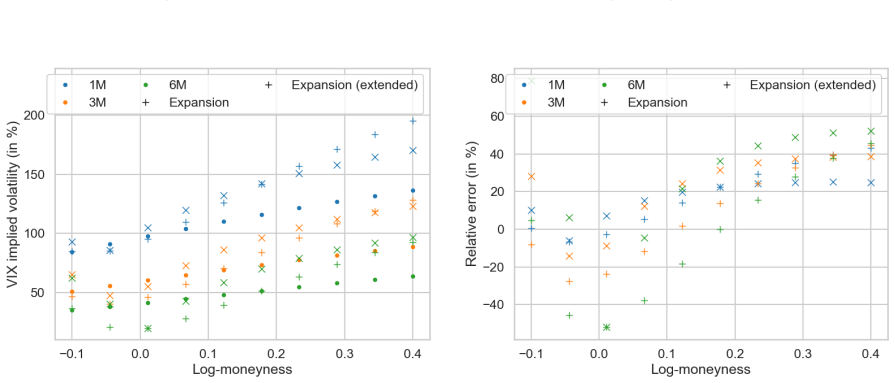

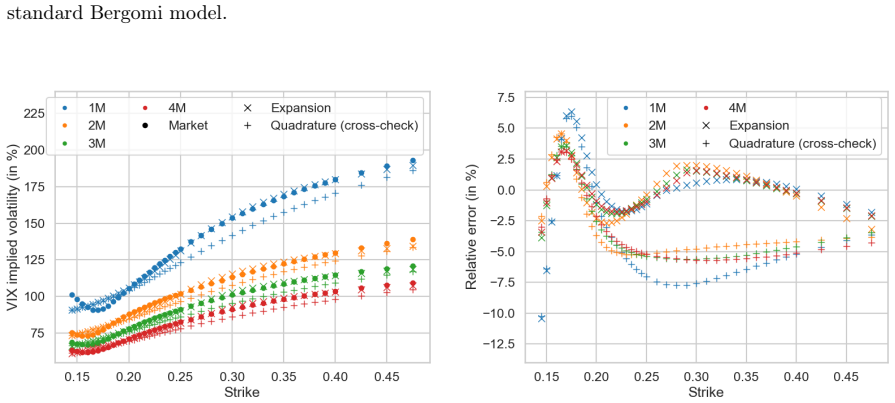

Within the class of forward variance models, closed-form expansions for the implied volatility of VIX options are developed using weak-approximation techniques for VIX option prices. These yield explicit formulas with computable correction terms that enable fast and accurate calibration without requiring numerical root-finding.

What carries the argument

Weak-approximation techniques for VIX option prices, which produce explicit implied volatility expansions with correction terms.

If this is right

- Fast calibration of forward variance models to VIX options data is enabled.

- The expansions apply to standard Bergomi, rough Bergomi-type, and mixed models.

- Implied volatility computation avoids numerical root-finding entirely.

- Numerical experiments confirm the accuracy of the expansions in practice.

Where Pith is reading between the lines

- The technique may generalize to pricing options on other volatility measures beyond VIX.

- Higher-order correction terms could be derived for improved precision in high-volatility regimes.

- These expansions might enable more efficient real-time hedging strategies for volatility products.

Load-bearing premise

That weak-approximation techniques for VIX option prices remain sufficiently accurate in forward variance models to produce reliable implied volatility expansions with computable corrections across practical parameter ranges.

What would settle it

High-accuracy Monte Carlo simulation of VIX option prices in a forward variance model followed by inversion to implied volatility and comparison to the expansion formula; significant deviation would falsify the accuracy claim.

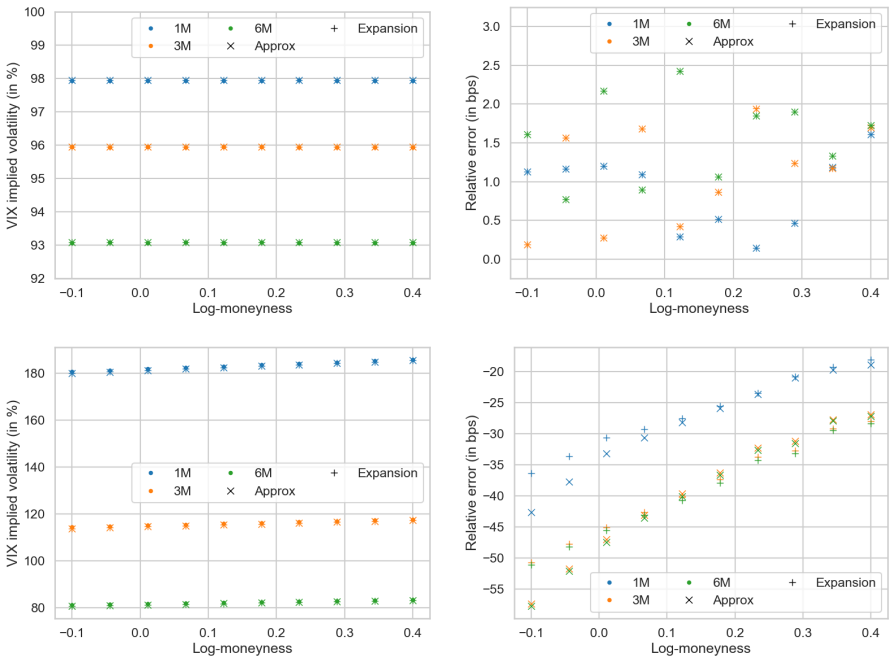

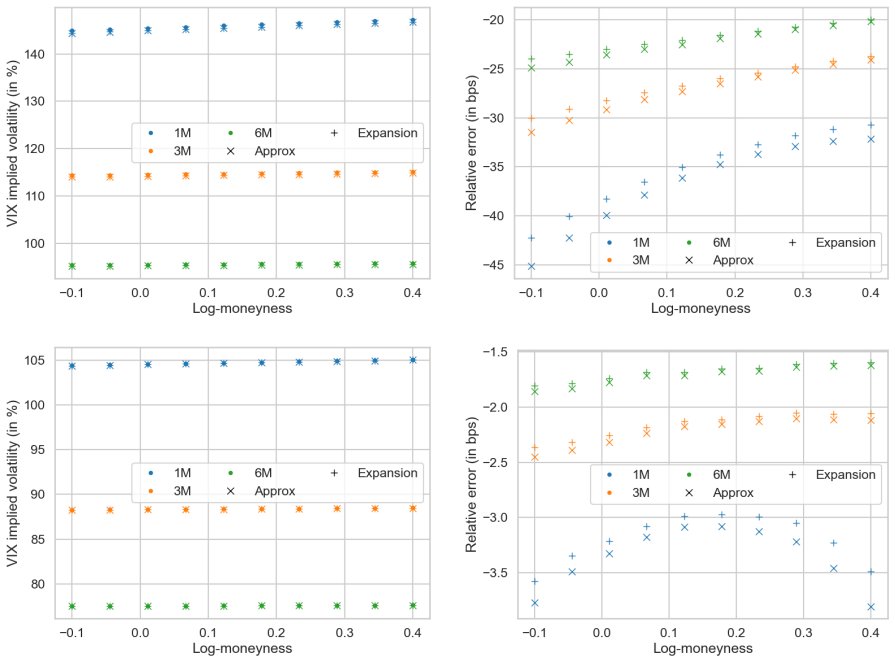

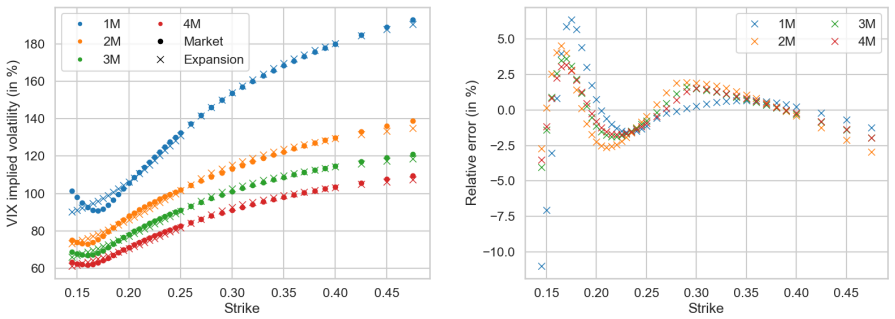

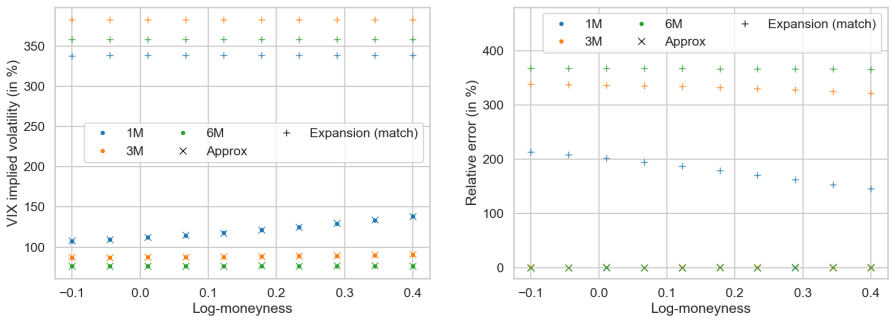

Figures

read the original abstract

We develop closed-form expansions for the implied volatility of VIX options within the class of forward variance models. Our approach builds on weak-approximation techniques for VIX option prices and yields explicit implied volatility expansions with computable correction terms. The resulting formulas enable fast and accurate calibration without requiring numerical root-finding. We illustrate the performance of the proposed expansions in both standard and rough Bergomi-type models, as well as in mixed specifications, and demonstrate their accuracy through numerical experiments.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops closed-form asymptotic expansions for the implied volatility of VIX options within forward variance models, including rough Bergomi-type specifications. It applies weak-approximation techniques to VIX option prices to obtain explicit IV formulas with computable correction terms that avoid numerical root-finding during calibration, and reports numerical experiments demonstrating accuracy in standard, rough, and mixed models.

Significance. If the expansions prove reliable, the work would supply a practical, fast calibration tool for VIX options in modern stochastic-volatility frameworks that are widely used in volatility trading and risk management. The explicit correction terms and extension to rough forward-variance dynamics represent a concrete computational advance over purely numerical methods.

major comments (2)

- [§3] §3 (Weak approximation for VIX prices): the derivation invokes a weak-approximation expansion for the VIX option price (a functional of the square root of integrated forward variance) but supplies neither explicit remainder bounds nor uniformity statements with respect to strike, tenor, or Hölder index H < 1/2. Because the subsequent IV inversion step amplifies any price-level error, the absence of these controls is load-bearing for the claim that the resulting IV expansions remain accurate across practical parameter ranges.

- [§5] §5 (Numerical experiments): the reported tests illustrate pointwise accuracy but do not tabulate or plot the approximation error as a function of vol-of-vol, H near 0.05, or short expiries; without such quantification or comparison against a high-precision benchmark, it is impossible to verify that the inversion step preserves the claimed accuracy uniformly.

minor comments (2)

- [§2] Notation for the forward-variance curve and the VIX functional should be introduced once with a single consistent symbol set rather than re-defined in each section.

- [Abstract] The abstract states that the expansions are 'closed-form' yet the correction terms involve integrals that must be evaluated numerically; a brief clarification of what 'closed-form' means in this context would avoid reader confusion.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive review of our manuscript. The comments highlight important aspects of the theoretical justification and numerical validation of our implied volatility expansions. We address each major comment below and outline the revisions we will make to strengthen the paper.

read point-by-point responses

-

Referee: [§3] §3 (Weak approximation for VIX prices): the derivation invokes a weak-approximation expansion for the VIX option price (a functional of the square root of integrated forward variance) but supplies neither explicit remainder bounds nor uniformity statements with respect to strike, tenor, or Hölder index H < 1/2. Because the subsequent IV inversion step amplifies any price-level error, the absence of these controls is load-bearing for the claim that the resulting IV expansions remain accurate across practical parameter ranges.

Authors: We acknowledge that the weak-approximation derivation in §3 is presented formally without explicit remainder bounds or uniformity statements in strike, tenor, or H. The expansion follows standard techniques for weak approximations of functionals of integrated variance processes, as used in related forward-variance and rough-volatility literature. Deriving fully rigorous, uniform error bounds that hold for all relevant strikes, short tenors, and H near 0 is technically involved and lies outside the paper's primary focus on obtaining explicit, computable IV formulas for calibration. Nevertheless, the subsequent numerical experiments provide empirical support for accuracy in practical regimes. In the revision we will add a dedicated paragraph in §3 that (i) states the formal character of the expansion, (ii) cites relevant results on weak convergence rates for rough paths, and (iii) explicitly notes the lack of proven uniformity as a limitation, thereby clarifying the theoretical scope without changing the main formulas. revision: partial

-

Referee: [§5] §5 (Numerical experiments): the reported tests illustrate pointwise accuracy but do not tabulate or plot the approximation error as a function of vol-of-vol, H near 0.05, or short expiries; without such quantification or comparison against a high-precision benchmark, it is impossible to verify that the inversion step preserves the claimed accuracy uniformly.

Authors: We agree that the current numerical section would benefit from a more systematic error analysis. The experiments already cover representative values of vol-of-vol and H (including H = 0.1) across several tenors, with pointwise IV errors typically below 0.5 %. To directly address the referee's request, we will expand §5 with additional tables and a new figure that plot the absolute and relative IV approximation error against vol-of-vol, H down to 0.05, and short expiries (e.g., 1 week). These will be computed against a high-precision Monte-Carlo benchmark (10^6 paths with antithetic variates and control variates). The revised experiments will confirm that the price-to-IV inversion step preserves the accuracy of the underlying weak approximation uniformly in the tested ranges. revision: yes

Circularity Check

Derivations rely on established weak approximations without self-referential reduction or fitted predictions

full rationale

The paper develops closed-form IV expansions for VIX options by applying weak-approximation techniques to option prices in forward variance models, then inverting to obtain explicit correction terms. These techniques are described as pre-existing methods rather than derived within the paper, and numerical experiments are used for validation across Bergomi-type and mixed models. No load-bearing step reduces by the paper's own equations to a quantity defined via its fitted parameters, self-citations, or ansatz smuggled from prior author work. The central claim remains independent of the target IV expansions.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Weak-approximation techniques yield accurate VIX option prices in forward variance models

Reference graph

Works this paper leans on

-

[1]

Pricing Under Rough Volatility

Christian Bayer, Peter Friz, and Jim Gatheral. “Pricing Under Rough Volatility”. In:Quan- titative Finance16.6 (June 2016), pp. 887–904.issn: 1469-7688

2016

-

[2]

Smile dynamics I

Lorenzo Bergomi. “Smile dynamics I”. In:Risk(2004)

2004

-

[3]

Smile Dynamics II

Lorenzo Bergomi. “Smile Dynamics II”. In:Risk(2005)

2005

-

[4]

Smile dynamics III

Lorenzo Bergomi. “Smile dynamics III”. In:Risk(2008)

2008

-

[5]

Stochastic Expansion for the Diffusion Processes and Applications to Option Pricing

Romain Bompis. “Stochastic Expansion for the Diffusion Processes and Applications to Option Pricing”. PhD thesis. Ecole Polytechnique X, Dec. 2013

2013

-

[6]

AnalyticalApproximationsofLocal-HestonVolatil- ity Model and Error Analysis

RomainBompisandEmmanuelGobet.“AnalyticalApproximationsofLocal-HestonVolatil- ity Model and Error Analysis”. In:Mathematical Finance28.3 (2018), pp. 920–961

2018

-

[7]

Stochastic approximations for financial risk computations

Florian Bourgey. “Stochastic approximations for financial risk computations”. PhD thesis. Institut Polytechnique de Paris, 2020

2020

-

[8]

Smile Dynamics and Rough Volatility

Florian Bourgey, Stefano De Marco, and Jules Delemotte. “Smile Dynamics and Rough Volatility”. In:Available at SSRN 4911186(2024)

2024

-

[9]

Weak Approximations and VIX Option Price Expansions in Forward Variance Curve Models

Florian Bourgey, Stefano De Marco, and Emmanuel Gobet. “Weak Approximations and VIX Option Price Expansions in Forward Variance Curve Models”. In:Quantitative Fi- nance23.9 (Sept. 2023), pp. 1259–1283.issn: 1469-7688

2023

-

[10]

Place: Dublin Published: Presentation at the Bachelier World Congress

Stefano De Marco.Volatility derivatives in (rough) forward variance models. Place: Dublin Published: Presentation at the Bachelier World Congress. July 2018

2018

-

[11]

Place: Dublin Published: Presentation at the Bachelier World Congress

Julien Guyon.On the joint calibration of SPX and VIX options. Place: Dublin Published: Presentation at the Bachelier World Congress. July 2018

2018

-

[12]

The VIX Future in Bergomi Models: Fast Approximation Formulas and Joint Calibration with S&P 500 Skew

Julien Guyon. “The VIX Future in Bergomi Models: Fast Approximation Formulas and Joint Calibration with S&P 500 Skew”. In:SIAM Journal on Financial Mathematics13.4 (Dec. 2022). Publisher: Society for Industrial and Applied Mathematics, pp. 1418–1485

2022

-

[13]

VolatilityOptionsinRoughVolatil- ity Models

BlankaHorvath,AntoineJacquier,andPeterTankov.“VolatilityOptionsinRoughVolatil- ity Models”. In:SIAM Journal on Financial Mathematics11.2 (Jan. 2020). Publisher: Society for Industrial and Applied Mathematics, pp. 437–469. A Proof of Proposition 3 Proof.By Remark 3, theNth-order Hermite approximations of the corresponding correction terms in the VIX call p...

2020

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.