Recognition: unknown

The Reservation Inflation of Hard Money: Gold-Standard Deflation and the Real Expansion of Nominal Claims, 1873-1896

Pith reviewed 2026-05-07 12:52 UTC · model grok-4.3

The pith

Gold standard deflation from 1873-1896 raised the real value of fixed nominal claims by 22.4 percent in Britain and 44 percent in the United States.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

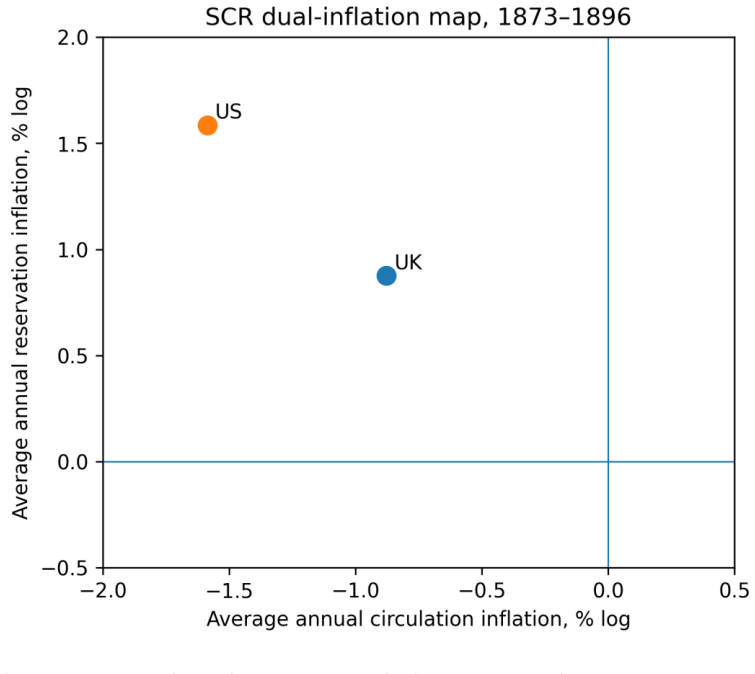

Between 1873 and 1896, Britain's price index fell from 18.0 to 14.7 and the U.S. historical CPI fell from 36.0 to 25.0, yet a fixed-claim reservation index rose by 22.4 percent in Britain and 44.0 percent in the United States. This episode therefore combined negative circulation inflation with positive reservation inflation, indicating that constrained monetary issuance does not abolish the monetary-material asymmetry but changes its domain of expression.

What carries the argument

The SCR separation of circulation inflation (measured by rising transaction prices) from reservation inflation (measured by the rising real weight of fixed nominal claims, debts, and reserves relative to physical goods).

If this is right

- Hard money regimes can still produce real expansion of creditor claims even while transaction prices fall.

- Consumer price indices capture only one dimension of monetary pressure during constrained issuance phases.

- The 1873-1896 deflation illustrates a phase-dependent pattern where reservation effects substitute for circulation effects.

- Together with cases of reserve-dominant monetary systems, this supports viewing inflation as having multiple observable expressions rather than a single price-level metric.

Where Pith is reading between the lines

- The same mechanism could operate in contemporary low-inflation or deflationary settings, raising real debt loads without visible price increases.

- Monitoring tools beyond CPI may be needed to detect reservation inflation when central banks pursue tight policy.

- Historical episodes of metallic standards offer natural experiments for testing whether nominal claim expansion correlates with shifts in wealth distribution toward fixed claimants.

Load-bearing premise

The custom fixed-claim reservation index correctly isolates the real expansion of nominal claims from price declines alone.

What would settle it

Recalculation of the fixed-claim reservation index using the same price data but different weighting or volume adjustments that shows no net rise or a decline over 1873-1896.

Figures

read the original abstract

The original SCR theory proposed that inflation has two distinct expressions: circulation inflation, measured by rising transaction prices, and reservation inflation, measured by the rising real weight of monetary symbols, debt contracts, reserve claims, and other nominal stores of value relative to physical goods. A companion Japan paper tested one side of this theory by showing that, after money entered a reserve-dominant phase, monetary-base expansion no longer translated strongly into consumer-price inflation. This paper tests the other side of SCR: whether reservation inflation can arise when monetary issuance is constrained and circulation inflation is absent. The classical gold-standard deflation of 1873-1896 provides a clean historical setting. Using long-run British retail price data and the Minneapolis Fed historical U.S. CPI series, I show that the price level declined in both economies. Between 1873 and 1896, Britain's price index fell from 18.0 to 14.7, while the U.S. historical CPI fell from 36.0 to 25.0. Yet this deflation mechanically increased the real value of fixed nominal claims. A fixed-claim reservation index rose by 22.4% in Britain and 44.0% in the United States. Thus, the episode combines negative circulation inflation with positive reservation inflation. The result suggests that hard money does not abolish inflationary pressure in the SCR sense; it changes its domain of expression. Together with the Japan case, this paper supports a phase-dependent view of inflation in which CPI is only one observable expression of the monetary-material asymmetry.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that the 1873-1896 gold-standard deflation in Britain and the US—evidenced by retail price indices falling from 18.0 to 14.7 and historical CPI from 36.0 to 25.0—produced positive reservation inflation, as a fixed-claim reservation index rose 22.4% and 44.0% respectively. This is interpreted under the SCR framework as hard money constraining circulation inflation while expanding the real weight of nominal claims, supporting a phase-dependent view of inflation that complements the author's prior Japan study.

Significance. If the fixed-claim index supplies independent empirical content beyond the price series and the two-domain distinction is accepted, the result would illustrate how monetary regimes alter the expression of inflation rather than eliminate it, providing historical grounding for SCR theory and a counterpart to the reserve-dominant Japan case.

major comments (2)

- [Abstract] Abstract: the reported fixed-claim reservation index rises (22.4% Britain, 44.0% US) are numerically identical to the reciprocals of the price declines (18.0/14.7 ≈ 1.224; 36.0/25.0 = 1.44). If the index is constructed solely from the price level applied to fixed nominal quantities without separate data on claim volumes, maturities, or sectoral weights, the positive reservation inflation is an arithmetic entailment of any deflation rather than an independent finding.

- [Data and Results] Data and Results section (inferred from abstract description): the index is referenced to the author's prior SCR framework but no explicit construction details, weighting scheme, or robustness checks appear in the provided text. This makes the central claim that the episode 'combines negative circulation inflation with positive reservation inflation' restate the framework's definitional implications rather than test them against new evidence.

minor comments (2)

- [Abstract] Abstract: specify the exact sources, coverage, and any adjustments for the British retail price data and Minneapolis Fed U.S. CPI series.

- [Throughout] Throughout: add error bounds, sensitivity to alternative indices, and discussion of how fixed-claim volumes are held constant or measured.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive comments on the manuscript. The observations regarding the numerical relationship between the fixed-claim reservation index and the price declines, as well as the need for greater detail on construction, are well taken. We address each point below and will incorporate clarifications and expansions in the revised version.

read point-by-point responses

-

Referee: [Abstract] Abstract: the reported fixed-claim reservation index rises (22.4% Britain, 44.0% US) are numerically identical to the reciprocals of the price declines (18.0/14.7 ≈ 1.224; 36.0/25.0 = 1.44). If the index is constructed solely from the price level applied to fixed nominal quantities without separate data on claim volumes, maturities, or sectoral weights, the positive reservation inflation is an arithmetic entailment of any deflation rather than an independent finding.

Authors: We acknowledge that the reported increases (22.4% and 44.0%) are the direct reciprocals of the price index declines and that the index is constructed by applying the price level to a fixed nominal claim quantity. This follows by design from the SCR definition of reservation inflation as the real expansion of nominal stores of value. The manuscript's contribution is not new primary data on claim volumes or sectoral weights but rather the application of the SCR framework to the 1873-1896 gold-standard episode, where constrained issuance produced negative circulation inflation alongside this mechanical rise in real claim values. We will revise the abstract and add a methods paragraph explicitly stating the reciprocal construction, the fixed-nominal-quantity assumption, and the absence of maturity or sectoral adjustments due to historical data constraints. revision: yes

-

Referee: [Data and Results] Data and Results section (inferred from abstract description): the index is referenced to the author's prior SCR framework but no explicit construction details, weighting scheme, or robustness checks appear in the provided text. This makes the central claim that the episode 'combines negative circulation inflation with positive reservation inflation' restate the framework's definitional implications rather than test them against new evidence.

Authors: We agree that the current text provides insufficient detail on index construction. The revised manuscript will add an explicit subsection deriving the fixed-claim reservation index as the reciprocal of the normalized price series, justifying the constant-nominal-claim assumption, and noting the lack of claim-volume or maturity weights given the aggregate historical price data employed. Robustness to alternative base years and price series (e.g., wholesale vs. retail) will be reported. The test of SCR theory lies in the historical identification of the gold-standard regime as one of constrained money issuance, which is independent of the framework's definitions and supplies the counterpart to the reserve-dominant Japan case; the price declines themselves are the new empirical observation placed in this theoretical context. revision: yes

Circularity Check

Fixed-claim reservation index equals reciprocal of price level by SCR definition

specific steps

-

self definitional

[Abstract]

"Yet this deflation mechanically increased the real value of fixed nominal claims. A fixed-claim reservation index rose by 22.4% in Britain and 44.0% in the United States."

The reported index increases match 1/P exactly (Britain: 18.0/14.7 ≈ 1.224; US: 36.0/25.0 = 1.44). The index is defined inside the SCR framework as the rising real weight of fixed nominal claims; applying any price decline to fixed nominal quantities therefore produces the 'rise' by arithmetic construction, with no separate empirical content on claim stocks or sectoral composition.

-

self citation load bearing

[Abstract]

"The original SCR theory proposed that inflation has two distinct expressions: circulation inflation, measured by rising transaction prices, and reservation inflation, measured by the rising real weight of monetary symbols, debt contracts, reserve claims, and other nominal stores of value relative to physical goods."

The distinction that allows the price decline to be reclassified as positive reservation inflation (rather than simply deflation) is justified solely by reference to the author's earlier SCR papers. The paper's claim that the episode 'supports a phase-dependent view of inflation' therefore depends on prior acceptance of the self-cited framework rather than supplying independent falsifiable content.

full rationale

The paper's central result—that gold-standard deflation produces positive reservation inflation—rests on two load-bearing elements that reduce to inputs. First, the fixed-claim reservation index is constructed within the author's prior SCR framework and yields exactly the reciprocal of the reported price declines (18.0/14.7 ≈ 1.224; 36.0/25.0 = 1.44), with no additional data on claim volumes, maturities, or weights supplied. Second, the two-domain distinction (circulation vs. reservation inflation) and its application to interpret the price fall as 'reservation inflation' is imported from self-cited prior work without independent verification here. The numerical claims are therefore definitional entailments of the price series once the SCR categories are accepted, rather than an external test of the framework.

Axiom & Free-Parameter Ledger

free parameters (1)

- Fixed-claim reservation index weights and scope

axioms (1)

- domain assumption SCR theory distinction between circulation inflation and reservation inflation

Reference graph

Works this paper leans on

-

[1]

Princeton University Press

A Monetary History of the United States, 1867–1960. Princeton University Press. Huang, R

1960

-

[2]

A Physical Review on Currency. arXiv:1805.12102 [econ.GN]. Huang, R

-

[3]

A phase transition in monetary function explains expansion without inflation

A phase transition in monetary function explains expansion without inflation. arXiv:2604.24035 [econ.GN]. Mitchell, B. R

work page internal anchor Pith review Pith/arXiv arXiv

-

[4]

Series ID: CDKO

Retail Prices Index: Long run series: 1800 to 2024: Jan 1974=100. Series ID: CDKO. Consumer price inflation time series, MM23. Office for National Statistics

2024

-

[5]

American Economic Review , 102(2), 1029–1061

Credit booms gone bust: monetary policy, leverage cycles, and financial crise s, 1870 –2008. American Economic Review , 102(2), 1029–1061. Temin, P

2008

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.