Recognition: unknown

A phase transition in monetary function explains expansion without inflation

Pith reviewed 2026-05-07 17:44 UTC · model grok-4.3

The pith

Base money expansions fail to raise consumer prices when absorbed as reserves rather than entering circulation.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

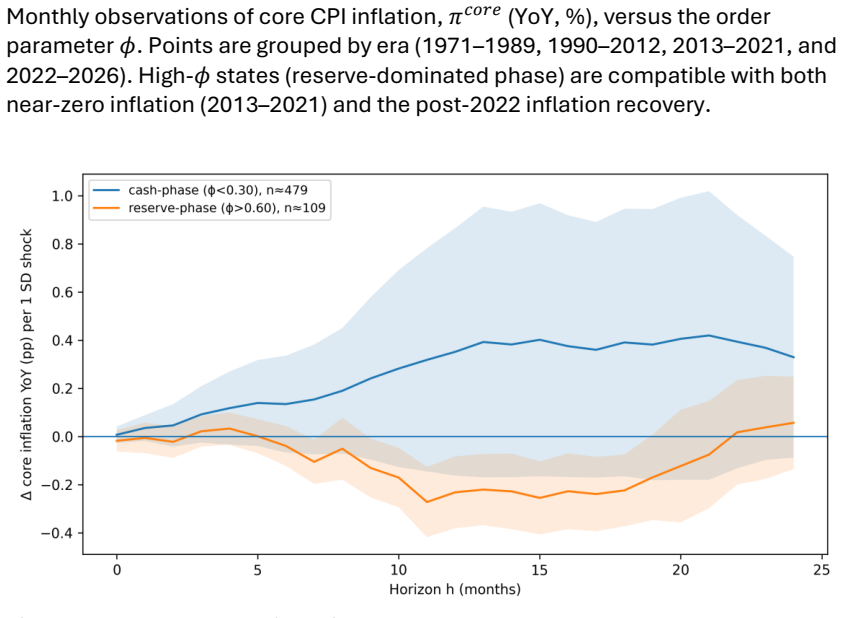

In the post-2013 reserve-dominated regime, unexpected expansions of the monetary base are absorbed primarily as reserve balances, causing phi to rise while the core CPI inflation response is strongly attenuated or reverses sign.

What carries the argument

The reserve-share fraction phi = RB/MB as a measurable order parameter that tracks the compositional phase transition between circulation and reservation compartments of the monetary base.

If this is right

- Unexpected base-growth shocks raise the reserve share phi significantly only in the reserve-dominated phase.

- The inflation response to base expansions is strongly attenuated once phi is high.

- Core CPI can exhibit negative responses to base expansions under reservation-dominant conditions.

- Separate efficiencies can be defined for how reserves absorb incremental money versus how money transmits to CPI.

Where Pith is reading between the lines

- Central banks could monitor phi as a real-time indicator of whether further base expansions are likely to affect consumer prices.

- The same phase logic might apply to other economies that have shifted to large reserve holdings after quantitative easing programs.

- If the transition is reversible, a future decline in reserves could restore stronger inflation transmission from base growth.

Load-bearing premise

That the reserve-share fraction phi directly determines the coupling strength between incremental base money and consumer prices, with the 2013 break marking a genuine phase transition rather than a policy artifact.

What would settle it

A large unexpected base-money expansion in Japan after 2013 in which the reserve share phi does not rise yet core CPI inflation rises substantially would falsify the central claim.

Figures

read the original abstract

Large monetary expansions do not necessarily generate consumer-price inflation, challenging scalar views of "money supply." Here we propose that monetary function is phase-dependent: newly issued base money can occupy distinct functional compartments with different coupling to prices. Starting from an accounting framework that separates reproduction, consumption, and reservation, we operationalize a measurable order parameter, phi=RB/MB, the reserve-share fraction of the monetary base. Using Japan's monthly record (1971-2026), we identify a compositional phase transition after 2013 from a cash-dominated to a reserve-dominated regime, quantitatively captured by a Landau-type order-parameter transition. Phase-conditional local projections using unexpected (residual) base-growth shocks show that, in Japan, unexpected base expansions are absorbed primarily as reserve balances-phi rises significantly-rather than entering the consumption-goods transaction sector; consequently, the core CPI inflation response is strongly attenuated and can even reverse sign. This demonstrates that increases in monetary supply do not necessarily cause inflation: the key is the "phase" in which incremental money accumulates (reservoir versus circulation). We further define function-specific efficiencies for reservation absorption and CPI transmission and provide an operational distinction between circulation-driven and reservation-dominant inflation regimes.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript claims that monetary expansions need not generate consumer-price inflation because newly issued base money can occupy distinct functional compartments (reservoir versus circulation) whose coupling to prices is governed by a phase-dependent order parameter. Using Japanese monthly data 1971-2026, it identifies a compositional phase transition after 2013 from a cash-dominated to a reserve-dominated regime, operationalized by phi = RB/MB and modeled as a Landau-type transition. Phase-conditional local projections on unexpected base-growth shocks then show that, post-2013, incremental base money is absorbed primarily as reserves (raising phi) rather than entering the transaction sector, attenuating or even reversing the core CPI response.

Significance. If the identification and conditional responses hold, the paper supplies a coherent accounting-based explanation for the post-QE inflation puzzle and introduces a measurable, falsifiable order parameter together with function-specific efficiencies. This framework could be applied to other economies and would sharpen the distinction between circulation-driven and reservation-dominant inflation regimes.

major comments (3)

- [Empirical strategy and local-projection section] The 2013 break date coincides with the launch of Abenomics and large-scale QE; the section on empirical strategy and the local-projection results must demonstrate that the observed rise in phi and the attenuation of CPI responses are not artifacts of the specific policy instruments (direct reserve creation at the BoJ) rather than evidence for a general phase transition. Robustness to alternative break dates or a continuous state-variable specification is required.

- [Order-parameter definition and local-projection results] Phi is constructed directly from the same reserve and base series used to measure the inflation response; the claim that base shocks cause phi to rise significantly (and thereby decouple from CPI) therefore requires explicit discussion of whether the result is independent or partly definitional. The identification assumptions for the residual shocks and the precise local-projection specification (lags, controls, error-band construction) need to be stated clearly.

- [Order-parameter transition subsection] The Landau-type transition for phi is asserted to capture a genuine compositional phase transition, but the manuscript must supply the explicit functional form, the estimated parameters, and goodness-of-fit statistics (relevant equation or figure) to show that the 2013 break is not merely a statistical artifact of the policy regime shift.

minor comments (2)

- [Abstract] The abstract lists the sample as ending in 2026; clarify the actual data endpoint and whether any observations are projected.

- [Accounting framework] Notation for the functional compartments (reproduction, consumption, reservation) should be introduced once with consistent symbols throughout the accounting framework section.

Simulated Author's Rebuttal

We appreciate the referee's thorough review and constructive suggestions, which will help improve the clarity and robustness of our analysis. We address each major comment below, indicating the revisions we plan to make.

read point-by-point responses

-

Referee: [Empirical strategy and local-projection section] The 2013 break date coincides with the launch of Abenomics and large-scale QE; the section on empirical strategy and the local-projection results must demonstrate that the observed rise in phi and the attenuation of CPI responses are not artifacts of the specific policy instruments (direct reserve creation at the BoJ) rather than evidence for a general phase transition. Robustness to alternative break dates or a continuous state-variable specification is required.

Authors: We thank the referee for highlighting this important identification concern. To address it, we will augment the empirical strategy section with robustness checks using alternative break dates (e.g., 2012 and 2014) and implement a continuous state-variable specification by interacting the base-growth shocks with a smooth function of lagged phi. These additions will clarify that the phase transition and conditional responses reflect a general compositional shift rather than being specific to the BoJ's direct reserve creation under Abenomics. revision: yes

-

Referee: [Order-parameter definition and local-projection results] Phi is constructed directly from the same reserve and base series used to measure the inflation response; the claim that base shocks cause phi to rise significantly (and thereby decouple from CPI) therefore requires explicit discussion of whether the result is independent or partly definitional. The identification assumptions for the residual shocks and the precise local-projection specification (lags, controls, error-band construction) need to be stated clearly.

Authors: We agree that greater transparency is needed here. In the revised version, we will add a detailed discussion explaining that although phi shares components with the base money series, the unexpected shocks are residuals from a forecasting equation for base growth that conditions on lagged variables, making the subsequent response of phi a test of allocation dynamics. We will explicitly state the local-projection specification, including the number of lags, additional controls (such as output gap and interest rates), and the method for constructing error bands (e.g., Newey-West or bootstrap). This will demonstrate that the decoupling from CPI is an empirical outcome, not definitional. revision: yes

-

Referee: [Order-parameter transition subsection] The Landau-type transition for phi is asserted to capture a genuine compositional phase transition, but the manuscript must supply the explicit functional form, the estimated parameters, and goodness-of-fit statistics (relevant equation or figure) to show that the 2013 break is not merely a statistical artifact of the policy regime shift.

Authors: We will revise the order-parameter transition subsection to include the explicit Landau functional form (e.g., the standard tanh-based transition equation), the estimated parameters with standard errors, and goodness-of-fit statistics such as R-squared and residual diagnostics. A supplementary figure will overlay the fitted transition on the observed phi series to illustrate that the 2013 shift is well-captured by the model and not solely an artifact of the policy change. These details will be added to the main text or an appendix. revision: yes

Circularity Check

No significant circularity; derivation is empirically self-contained

full rationale

The paper defines the order parameter phi = RB/MB directly from accounting identities in the monetary base data and identifies the 2013 compositional break from the observed time series of phi itself. It then applies phase-conditional local projections to estimate the impulse responses of both phi and core CPI to unexpected base-growth shocks. These estimated responses are not algebraically forced by the definition of phi; the local-projection coefficients are identified from the timing and magnitude of the residual shocks and the conditional variation in the outcome series. No load-bearing step reduces to a self-citation, an imported uniqueness theorem, or a fitted parameter that is merely renamed as a prediction. The central claim—that post-2013 base expansions are absorbed into reserves with attenuated CPI transmission—is therefore an empirical finding rather than a definitional identity, and the derivation remains self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

free parameters (1)

- 2013 transition date

axioms (1)

- domain assumption Newly issued base money occupies distinct functional compartments with different coupling to consumer prices

invented entities (1)

-

functional compartments (reservoir versus circulation)

no independent evidence

Forward citations

Cited by 1 Pith paper

-

The Reservation Inflation of Hard Money: Gold-Standard Deflation and the Real Expansion of Nominal Claims, 1873-1896

Gold-standard deflation from 1873-1896 raised the real value of nominal claims 22-44% despite falling prices, showing reservation inflation separate from circulation inflation under constrained money issuance.

Reference graph

Works this paper leans on

-

[1]

Monetary Base (Average Amounts Outstanding), Long-Term Time Series (mblong.xlsx)

Bank of Japan. Monetary Base (Average Amounts Outstanding), Long-Term Time Series (mblong.xlsx)

-

[2]

Consumer Price Index (2020 Base), Time Series, Indices of Items, Japan, Monthly

Statistics Bureau of Japan. Consumer Price Index (2020 Base), Time Series, Indices of Items, Japan, Monthly

2020

-

[3]

Monetary Policy and Forward Guidance in Japan

Shirai, S. Monetary Policy and Forward Guidance in Japan. Bank of Japan speech / policy document (2013)

2013

-

[4]

& Soma, N

Shintani, M. & Soma, N. The Effects of QQE on Long-run Inflation Expectations in Japan. Working paper

-

[5]

Huang, R. A Physical Review on Currency. SSRN preprint (2018). DOI: 10.2139/SSRN.3163954

-

[6]

Outline of the 2020-Base Consumer Price Index

Statistics Bureau of Japan. Outline of the 2020-Base Consumer Price Index

2020

-

[7]

Japan—Consumer Price Index, SDDS Plus / DQAF Metadata

International Monetary Fund. Japan—Consumer Price Index, SDDS Plus / DQAF Metadata

-

[8]

Estimation and Inference of Impulse Responses by Local Projections

Jordà, Ò . Estimation and Inference of Impulse Responses by Local Projections. American Economic Review 95, 161–182 (2005). Figures Fig. 1. Monetary base expansion, CPI, and the compositional shift in the phase of money in Japan (1971–2026). (A) Indexed trajectories (start = 100; log scale) of the seasonally adjusted monetary base (𝑀𝐵𝑆𝐴), headline CPI, an...

2005

-

[9]

All items

Responses are significantly positive in both phases, indicating that base-money expansions preferentially populate the reserve reservoir. Shaded bands indicate 95% HAC(12) confidence intervals. Supplementary Materials I for: A phase transition in monetary function explains expansion without inflation Contents • S1. Data sources and preprocessing • S2. Bre...

2020

-

[10]

𝜋𝑡 𝑐𝑜𝑟𝑒 These variables represent, respectively, the scale of the monetary base, the composition of the monetary base, and the core inflation outcome that the main text seeks to explain. S2.2 Automatic single-break detection Within a sample window [𝑡𝑎, 𝑡𝑏], we estimate a single breakpoint 𝜏 by fitting a two- segment linear model and selecting the breakpoi...

1990

-

[11]

the response kernel differs across phases

-

[12]

unexpected base-growth shocks are absorbed into reserves, raising 𝜙𝑡

-

[13]

We do not claim a fully structural decomposition of the mechanisms underlying the sign and shape differences

the qualitative contrast between phases is robust to reasonable variations in thresholds and specification (S5). We do not claim a fully structural decomposition of the mechanisms underlying the sign and shape differences. Rather, we document a robust phase dependence consistent with the phase-transition interpretation developed in the main text. S4. Full...

-

[14]

AR residuals with alternative lag orders, including AR(6) and AR(18), in place of the baseline AR(12)

-

[15]

The resulting IRFs are reported in Fig

a detrended-growth residual in which 𝑔𝑡 𝑀𝐵 is regressed on a time trend and lagged terms within phase, and the residual is used as the shock. The resulting IRFs are reported in Fig. S5. The reserve-phase response remains distinct from the cash-phase response, and the positive response of 𝜙𝑡 to unexpected base-growth shocks is preserved. These results indi...

-

[16]

the post-2013 episode is robustly associated with a compositional shift in 𝜙𝑡

2013

-

[17]

positive monetary-base shocks are absorbed into reserves, raising 𝜙𝑡 rather than transmitting proportionally into prices

-

[18]

Supplementary figure captions Fig

the inflation-response kernel differs systematically between the cash phase and reserve phase across a range of reasonable thresholds and specifications. Supplementary figure captions Fig. S1. Breakpoint robustness across alternative windows (automatic detection). Automatic single-break estimates are obtained by minimizing the residual sum of squares of a...

1990

-

[19]

the system is driven by a control parameter 𝜃,

-

[20]

the effective potential 𝐹(𝑚; 𝜃) changes shape across threshold,

-

[21]

the equilibrium order parameter crosses 𝑚 = 0,

-

[22]

crossing 𝑚 = 0 means 𝜙 crosses 𝜙𝑐,

-

[23]

money supply does not necessarily cause inflation

once 𝜙 > 𝜙𝑐, the CPI coupling kernel can weaken or reverse sign. The physical significance of the critical point is that it also governs the sign of CPI transmission. The effective CPI coupling is positive when 𝜙‾ < 𝜙𝑐 and negative when 𝜙‾ > 𝜙𝑐. The Japan calibration therefore supports a unified interpretation: the cash phase and reserve phase do not requ...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.