Recognition: unknown

A Note on the Generalized Cape Cod Reserving Method

Pith reviewed 2026-05-07 06:42 UTC · model grok-4.3

The pith

The generalized Cape Cod reserving method yields an explicit formula for its mean squared error of prediction once placed in a stochastic model.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

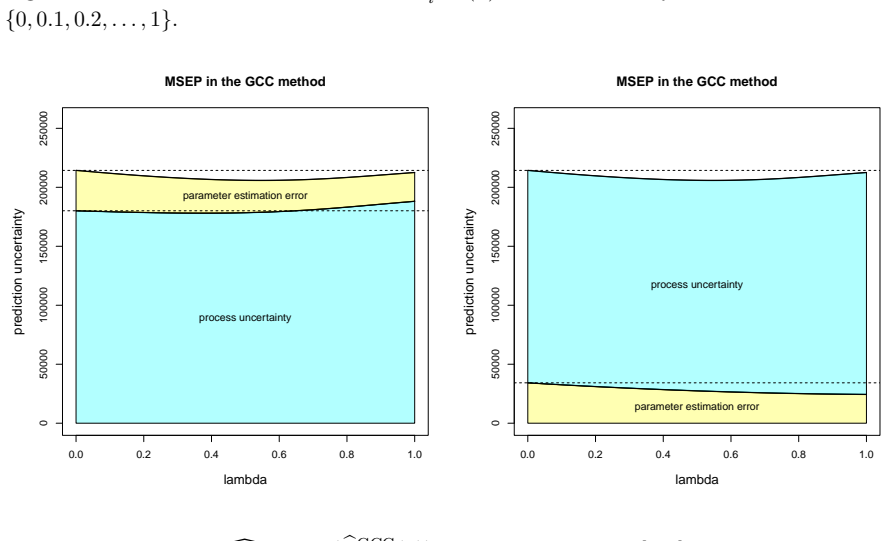

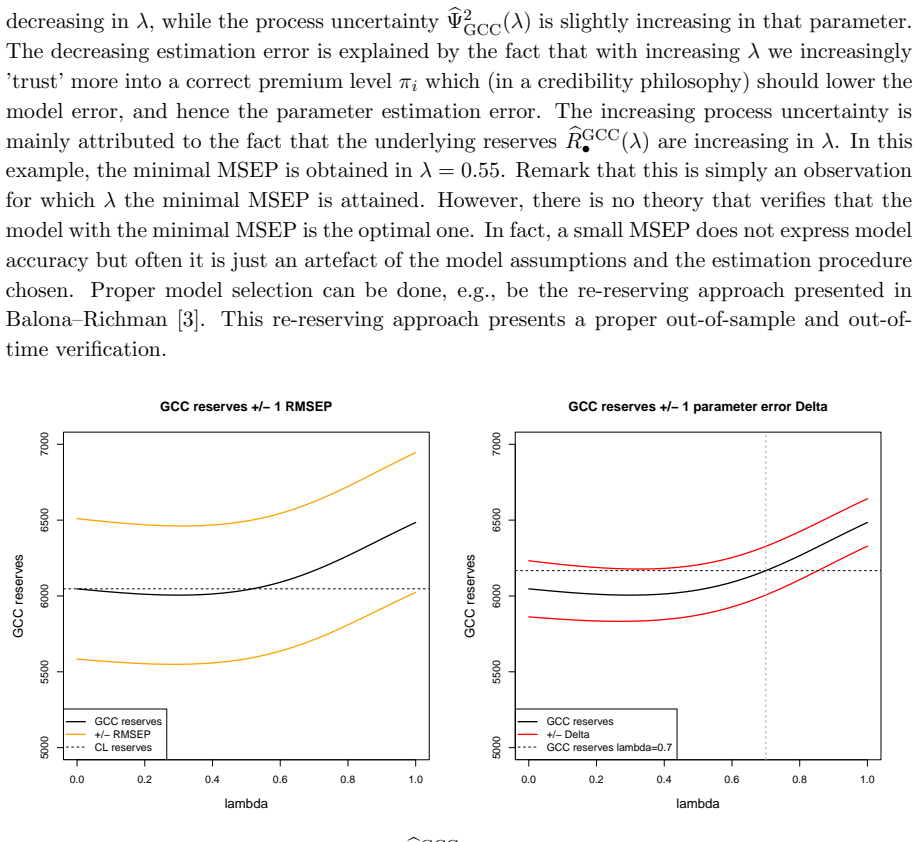

The generalized Cape Cod method can be embedded into a stochastic model that yields a closed-form expression for its mean squared error of prediction. The embedding treats the method as a weighted combination of observed claims and prior expected claims, then propagates the variances through the weighting scheme to obtain the explicit MSEP formula.

What carries the argument

The stochastic embedding of the GCC algorithm, which converts its deterministic weights into variance-propagating linear combinations and delivers the analytical MSEP.

If this is right

- Actuaries obtain the prediction error directly from the formula rather than from simulation.

- Uncertainty measures become comparable across chain-ladder, Bornhuetter-Ferguson, and generalized Cape Cod on the same portfolio.

- Reserve setting and capital requirements can incorporate the new MSEP expression without additional numerical work.

- The same embedding approach can be applied to other deterministic reserving algorithms that lack an analytical error formula.

Where Pith is reading between the lines

- Reserving software can implement the formula as a standard output option alongside existing CL and BF results.

- The explicit form may allow analytic study of how the GCC predictor behaves when claim volumes or development patterns change.

- Portfolio-level tests on historical data can now check whether the derived MSEP tracks observed reserve run-off errors.

Load-bearing premise

The generalized Cape Cod method must fit inside a linear stochastic model where variances and covariances can be calculated explicitly, the same way they are for the chain-ladder and Bornhuetter-Ferguson methods.

What would settle it

Run a Monte Carlo simulation of the full claims process under the stochastic model used for the derivation, compute the empirical mean squared error of the GCC predictor, and check whether it matches the analytical formula to within sampling error.

Figures

read the original abstract

Claims reserving is one of the most important actuarial tasks in non-life insurance modeling. There are several popular methods to perform claims reserving such as the chain-ladder (CL), the Bornhuetter--Ferguson (BF) or the generalized Cape Cod (GCC) methods. These methods have originally been introduced as deterministic algorithms, and only in a later step, they have been lifted to stochastic models allowing for analyzing claims prediction uncertainty. This holds true for the CL and the BF methods, but not for the GCC method. The purpose of this article is to close this gap and derive an analytical formula for the mean squared error of prediction (MSEP) of the GCC method.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper embeds the generalized Cape Cod (GCC) reserving method into a stochastic over-dispersed Poisson framework with a priori loss ratios and exposure weights. The conditional expectation of the model recovers the deterministic GCC point estimates, and the authors derive an analytical expression for the mean squared error of prediction (MSEP) by calculating the process variance and estimation variance terms.

Significance. This fills a notable gap in the actuarial literature by providing a stochastic model for the GCC method similar to those for chain-ladder and Bornhuetter-Ferguson. The explicit model and direct analytical derivation of MSEP without hidden approximations or simulations is a strength, allowing for rigorous and reproducible uncertainty quantification in claims reserving.

minor comments (3)

- [Abstract] The abstract announces the derivation but could briefly mention the key model assumptions (over-dispersed Poisson) and the structure of the MSEP formula to better inform readers.

- [Model section] The definition of the exposure weights and a priori loss ratios should include a clear statement of how they are estimated from data to avoid ambiguity in implementation.

- [MSEP derivation] It would be useful to include a small numerical example comparing the analytical MSEP to bootstrap estimates to illustrate the formula's behavior.

Simulated Author's Rebuttal

We thank the referee for their positive summary of our paper and for recommending minor revision. The referee correctly identifies the core contribution: embedding the generalized Cape Cod method in an over-dispersed Poisson model with a priori loss ratios and exposure weights, recovering the deterministic point estimates via conditional expectation, and providing a direct analytical MSEP formula without simulation or hidden approximations. We are pleased that this is recognized as filling a gap analogous to the stochastic treatments of chain-ladder and Bornhuetter-Ferguson. No specific major comments were raised in the report.

Circularity Check

No significant circularity in the GCC MSEP derivation

full rationale

The paper specifies an explicit over-dispersed Poisson model with a priori loss ratios and exposure weights. The conditional means of this model are constructed to recover the original deterministic GCC point estimates exactly. From this model the authors then derive closed-form expressions for process variance and estimation variance, yielding an analytical MSEP formula. This construction is the standard, non-circular approach already used for the chain-ladder and Bornhuetter-Ferguson methods; the MSEP is a genuine consequence of the chosen stochastic assumptions rather than a tautological re-labeling of fitted quantities. No load-bearing self-citation, self-definitional step, or renaming of known results appears in the derivation chain.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Alai, D.H., Merz, M., W¨ uthrich, M.V. (2009). Mean square error of prediction in the Bornhuetter- Ferguson claims reserving method.Annals of Actuarial Science4/1, 7-31

2009

-

[2]

Alai, D.H., Merz, M., W¨ uthrich, M.V. (2010). Prediction uncertainty in the Bornhuetter-Ferguson claims reserving method: revisited.Annals of Actuarial Science5/1, 7-17

2010

-

[3]

Balona, C., Richman, R. (2020). The actuary and IBNR techniques: a machine learning approach. SSRN ManuscriptID 3697256

2020

-

[4]

Benktander, G. (1976). An approach to credibility in calculating IBNR for casualty excess reinsur- ance.The Actuarial Review, April 1976,312, 7

1976

-

[5]

Bornhuetter, R.L., Ferguson, R.E. (1972). The actuary and IBNR.Proceedings of the Casualty Actuarial Society59, 181-195

1972

-

[6]

B¨ uhlmann, H. (1983). Estimation of IBNR reserves by the methods chain ladder, Cape Cod and complimentary loss ratio.International Summer School 1983.SSRN Manuscript2752387

1983

-

[7]

England, P.D., Verrall, R.J. (2002). Stochastic claims reserving in general insurance.British Actu- arial Journal8/3, 443-518

2002

-

[8]

England, P.D., Verrall, R.J. (2006). Predictive distributions of outstanding liabilities in general insurance.Annals of Actuarial Science1/2, 221-270

2006

-

[9]

England, P.D., Verrall, R.J., W¨ uthrich, M.V. (2012). Bayesian overdispersed Poisson model and the Bornhuetter–Ferguson claims reserving method.Annals of Actuarial Science6/2, 258-283

2012

-

[10]

Gluck, S.M. (1997). Balancing development and trend in loss reserve analysis.Proceeding of the Casualty Actuarial Society84, 482-532

1997

-

[11]

Hovinen, E. (1981). Additive and continuous IBNR.ASTIN Colloquium 1981, Loen, Norway

1981

-

[12]

Mack, T. (1993). Distribution-free calculation of the standard error of chain ladder reserve esti- mates.ASTIN Bulletin - The Journal of the IAA23/2, 213-225

1993

-

[13]

Mack, T. (2000). Credible claims reserves: the Benktander method.ASTIN Bulletin - The Journal of the IAA30/2, 333-347

2000

-

[14]

Mack, T. (2008). The prediction error of Bornhuetter/Ferguson.ASTIN Bulletin - The Journal of the IAA38/1, 87-103

2008

-

[15]

Renshaw, A.E., Verrall, R.J. (1998). A stochastic model underlying the chain-ladder technique. British Actuarial Journal4/4, 903-923. 18

1998

-

[16]

R¨ ohr, A. (2016). Chain ladder and error propagation.ASTIN Bulletin - The Journal of the IAA 46/2, 293-330

2016

-

[17]

Saluz, A. (2015). Prediction uncertainties in the Cape Cod reserving methodAnnals of Actuarial Science9/2, 239-263

2015

-

[18]

Saluz, A., Gisler, A., W¨ uthrich, M.V. (2011). The stochastic Bornhuetter–Ferguson claims reserving method.ASTIN Bulletin - The Journal of the IAA.41/2, 279-313

2011

-

[19]

Schmidt, K.D., Zocher, M. (2008). The Bornhuetter–Ferguson principle.Variance2/1, 85-110

2008

-

[20]

Verrall, R.J. (1990). Bayes and empirical Bayes estimation for the chain ladder model.ASTIN Bulletin - The Journal of the IAA20/2, 217-243

1990

-

[21]

(2008).Stochastic Claims Reserving Methods in Insurance

W¨ uthrich, M.V., Merz, M. (2008).Stochastic Claims Reserving Methods in Insurance. Wiley

2008

-

[22]

IX l=1 Cl,I−l λ|i−l| PI k=1 QJ−1 j=I−k f −1 j πk λ|i−k| # πi =1 {t≥I−i} J−1Y j=I−i f −1 j

W¨ uthrich, M.V., Merz, M. (2015).Stochastic Claims Reserving Manual: Advances in Dynamic Modeling. SSRN Manuscript 2649057. 19 A Proofs Proof of Theorem 3.1.The GCC predictor over all accident years is given by IX i=1 bC GCC i,J (fj)J−1 j=0 = IX i=1 Ci,I−i + 1− J−1Y j=I−i f −1 j !" IX l=1 Cl,I−l λ|i−l| PI k=1 QJ−1 j=I−k f −1 j πk λ|i−k| # πi.(A.1) The ri...

2015

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.