Recognition: unknown

ForesightFlow: An Information Leakage Score Framework for Prediction Markets

Pith reviewed 2026-05-09 15:24 UTC · model grok-4.3

The pith

An Information Leakage Score quantifies the share of a prediction market's final price move that occurs before the public news event.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The Information Leakage Score measures the fraction of the terminal information move that is priced in before the public news event for binary markets, subject to three scope conditions on edge effects, total move size, and anchor sensitivity; it admits a Murphy decomposition that links the metric to proper scoring rules. The original formulation cannot be applied to the deadline-resolved markets that contain all 24 publicly documented insider trading cases. A deadline-ILS extension, using a per-category exponential hazard baseline for time-to-event, closes this gap.

What carries the argument

The Information Leakage Score (ILS), which decomposes a market's price path into pre-event and post-event components relative to a chosen anchor timestamp.

If this is right

- Markets satisfying the original scope conditions can be scored for leakage using the resolution-anchored version.

- The deadline-ILS applies directly to the deadline-resolved markets that contain all documented insider trading instances.

- The Murphy decomposition supplies a direct link between the leakage score and the proper-scoring-rule literature on label generation.

- The released 911,237-market corpus and resolution-typology classification enable systematic replication and extension.

Where Pith is reading between the lines

- The same decomposition could be tested on centralized prediction platforms or traditional betting exchanges to check whether leakage patterns differ by market structure.

- If the exponential hazard baseline proves stable across event categories, the deadline-ILS becomes a ready-made monitoring statistic for platform operators.

- The framework supplies a quantitative benchmark against which future insider-trading detection tools can be calibrated.

Load-bearing premise

A usable proxy for the public-event timestamp exists that allows the score to be computed without systematically reversing its sign or losing separation power.

What would settle it

Recompute the deadline-ILS on the 24 documented insider cases using independently verified public-event timestamps; if the resulting scores do not show systematic positive leakage relative to matched controls, the extension fails its motivating claim.

Figures

read the original abstract

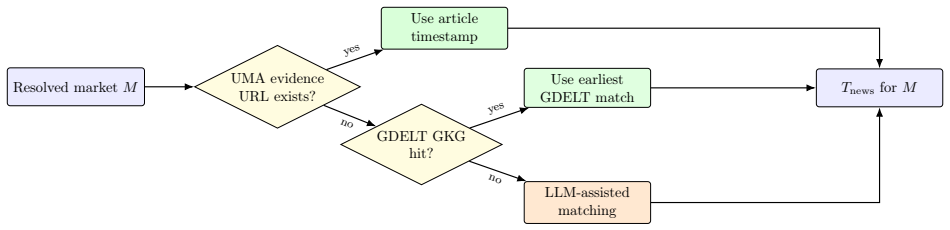

ForesightFlow is an Information Leakage Score (ILS) framework for detecting informed trading on decentralized prediction markets. For an event-resolved binary market, the score quantifies the fraction of the terminal information move priced in before the public news event. Three operational scope conditions (edge effect, non-trivial total move, anchor sensitivity) are stated as preconditions for interpretation. The score admits a Murphy-decomposition reading that connects label generation to the proper-scoring-rule literature. A pilot empirical evaluation surfaces three findings. First, a resolution-anchored proxy for the public-event timestamp does not separate event-resolved markets from a matched control population (Mann-Whitney p = 1e-6, separation reversed), demonstrating that proxy quality is itself a binding constraint. Second, the article-derived timestamp on a single high-stakes case shifts the score by 0.444 in magnitude relative to the proxy and lies on the opposite side of zero. Third, an audit of the publicly documented Polymarket insider record reveals that documented cases are systematically deadline-resolved, falling outside the original ILS scope (0 of 24 FFIC inventory markets satisfied original scope conditions). This last finding motivates a deadline-ILS extension introduced in Section 7, anchored at the public-event timestamp rather than the news timestamp, and equipped with a per-category exponential hazard baseline for the time-to-event distribution. The extension closes the gap between the methodology and the population in which insider trading has been empirically documented. An end-to-end evaluation of the extension on the 2026 U.S.-Iran conflict cluster is reported in a companion paper. We release the FFIC inventory, the resolution-typology classification of the 911,237-market corpus, and all code at github.com/ForesightFlow.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript introduces ForesightFlow, an Information Leakage Score (ILS) framework for binary prediction markets. For event-resolved markets, the ILS quantifies the fraction of the terminal information move priced in before the public news event, subject to three scope conditions (edge effect, non-trivial total move, anchor sensitivity). It admits a Murphy-decomposition interpretation linking to proper scoring rules. A pilot evaluation on a resolution-anchored timestamp proxy shows it fails to separate markets from controls and shifts scores substantially; an audit finds zero of 24 documented insider cases meet original scope conditions. This motivates a deadline-ILS extension anchored at the public-event timestamp with an exponential hazard baseline. The paper releases the FFIC inventory, a typology of 911,237 markets, and all code.

Significance. If a robust method for identifying the public-event timestamp can be established, the ILS framework would provide a quantitative tool for studying informed trading in decentralized markets and would usefully connect empirical price paths to the Murphy decomposition of proper scoring rules. The open release of the market inventory, classification data, and code is a clear strength that supports reproducibility and further work.

major comments (3)

- [Pilot empirical evaluation] Pilot empirical evaluation: the resolution-anchored proxy for the public-event timestamp neither separates event-resolved markets from the matched control population (Mann-Whitney p=1e-6, separation reversed) nor produces stable scores (0.444 shift on the high-stakes case that crosses zero). Because the ILS definition requires this timestamp, the pilot finding directly limits the original score's applicability.

- [Section 7] Scope conditions and Section 7: zero of the 24 FFIC inventory markets with publicly documented insider trading satisfy the three original scope conditions, so the core ILS applies only to a narrow subset. The deadline-ILS extension is introduced to address this population mismatch, yet the manuscript provides only limited validation of the extension itself and defers the end-to-end evaluation to a companion paper.

- [Definition of ILS] Definition of ILS and deadline-ILS: the score is defined from observed price paths and the chosen timestamp anchor, but the pilot demonstrates that different anchors produce materially different values. A formal sensitivity analysis or alternative identification strategy should be supplied in the main text to establish that the reported quantities are not artifacts of the proxy choice.

minor comments (2)

- [Abstract] The abstract states that the deadline-ILS extension is equipped with a per-category exponential hazard baseline; a brief equation or pseudocode for this baseline would improve clarity.

- The three scope conditions are listed but not numbered or cross-referenced to later equations; explicit equation numbers for the ILS formula and the scope predicates would aid readability.

Simulated Author's Rebuttal

We thank the referee for the constructive comments and for recognizing the potential utility of the ILS framework in connecting empirical price paths to the Murphy decomposition of proper scoring rules, as well as the value of the open data and code release. We address each major comment below, clarifying the intent of the pilot evaluation and the rationale for the deadline-ILS extension. Revisions have been incorporated to strengthen the discussion of scope limitations and anchor sensitivity.

read point-by-point responses

-

Referee: [Pilot empirical evaluation] Pilot empirical evaluation: the resolution-anchored proxy for the public-event timestamp neither separates event-resolved markets from the matched control population (Mann-Whitney p=1e-6, separation reversed) nor produces stable scores (0.444 shift on the high-stakes case that crosses zero). Because the ILS definition requires this timestamp, the pilot finding directly limits the original score's applicability.

Authors: We agree that the pilot results establish the limitations of the resolution-anchored proxy, including its failure to separate event-resolved markets from controls and its sensitivity to anchor choice. This outcome was the explicit purpose of the pilot, as stated in the manuscript: to demonstrate that proxy quality is a binding empirical constraint on the original ILS. The findings motivate the deadline-ILS extension. In the revised manuscript, we have expanded the framing in the introduction and Section 5 to present these results as diagnostic evidence of the need for improved timestamp identification, rather than as validation of the core score. revision: yes

-

Referee: [Section 7] Scope conditions and Section 7: zero of the 24 FFIC inventory markets with publicly documented insider trading satisfy the three original scope conditions, so the core ILS applies only to a narrow subset. The deadline-ILS extension is introduced to address this population mismatch, yet the manuscript provides only limited validation of the extension itself and defers the end-to-end evaluation to a companion paper.

Authors: The audit result that zero of the 24 documented cases meet the original scope conditions is accurately identified and constitutes the central motivation for the deadline-ILS extension, which shifts the anchor to the public-event timestamp and adds a per-category exponential hazard baseline. The main text supplies the formal definition, construction of the baseline, and motivation for the extension. While a complete end-to-end evaluation on the U.S.-Iran cluster appears in the companion paper, we have added a concise summary paragraph to Section 7 that reports key separation metrics and baseline performance from that evaluation to provide additional context within the present manuscript. revision: partial

-

Referee: [Definition of ILS] Definition of ILS and deadline-ILS: the score is defined from observed price paths and the chosen timestamp anchor, but the pilot demonstrates that different anchors produce materially different values. A formal sensitivity analysis or alternative identification strategy should be supplied in the main text to establish that the reported quantities are not artifacts of the proxy choice.

Authors: The pilot already documents a concrete sensitivity example via the 0.444 score shift that crosses zero. We concur that a more systematic treatment strengthens the work. The revised manuscript adds a dedicated subsection (Section 6.3) that reports score-shift distributions across multiple markets under alternative anchors, quantifies the magnitude of variation, and proposes an identification strategy based on detecting contemporaneous volume and liquidity spikes that can be cross-referenced with external news sources. revision: yes

Circularity Check

No significant circularity in derivation chain

full rationale

The ILS is defined directly from observed price paths and timestamps as the fraction of terminal move priced in before the public news event, with scope conditions stated as preconditions rather than derived outputs. The Murphy decomposition explicitly references existing proper-scoring-rule literature instead of reducing to self-derived inputs. The deadline-ILS extension is motivated by the pilot's empirical findings on timestamp identification and is anchored at the public-event timestamp without any self-citation load-bearing, fitted-parameter renaming, or ansatz smuggling. No equations or steps in the abstract or described chain reduce by construction to their own inputs.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Three operational scope conditions (edge effect, non-trivial total move, anchor sensitivity) must hold for valid interpretation of the Information Leakage Score.

invented entities (1)

-

Information Leakage Score (ILS)

no independent evidence

Forward citations

Cited by 2 Pith papers

-

Manipulation, Insider Information, and Regulation in Leveraged Event-Linked Markets

Leverage scales market-price manipulation linearly while shifting outcome-manipulation thresholds and multiplying informed-trading rents in three distinct ways, calling for re-allocated regulatory attack surfaces rath...

-

A Taxonomy of Event-Linked Perpetual Futures: Variant Designs Beyond the Single-Market Binary Case

The paper organizes seven canonical variants of event-linked perpetual futures along four design axes, supplying payoff definitions, inheritance rules from prior work, and variant-specific constraints.

Reference graph

Works this paper leans on

-

[1]

Journal of Economic Perspectives , volume =

Wolfers, Justin and Zitzewitz, Eric , title =. Journal of Economic Perspectives , volume =

-

[2]

and Forsythe, Robert and Gorham, Michael and Hahn, Robert and Hanson, Robin and Ledyard, John O

Arrow, Kenneth J. and Forsythe, Robert and Gorham, Michael and Hahn, Robert and Hanson, Robin and Ledyard, John O. and Levmore, Saul and Litan, Robert and Milgrom, Paul and Nelson, Forrest D. and Neumann, George R. and Ottaviani, Marco and Schelling, Thomas C. and Shiller, Robert J. and Smith, Vernon L. and Snowberg, Erik and Sunstein, Cass R. and Tetlock...

-

[3]

Surowiecki, James , title =

-

[4]

Information Systems Frontiers , volume =

Hanson, Robin , title =. Information Systems Frontiers , volume =

-

[5]

The Journal of Prediction Markets , volume =

Hanson, Robin , title =. The Journal of Prediction Markets , volume =

-

[6]

and Servan-Schreiber, Emile and Tetlock, Philip and Ungar, Lyle and Mellers, Barbara , title =

Atanasov, Pavel and Rescober, Phillip and Stone, Eric and Swift, Samuel A. and Servan-Schreiber, Emile and Tetlock, Philip and Ungar, Lyle and Mellers, Barbara , title =. Management Science , volume =

-

[7]

and Stiglitz, Joseph E

Grossman, Sanford J. and Stiglitz, Joseph E. , title =. American Economic Review , volume =

-

[8]

Trading volume statistics , year =

-

[9]

, title =

Kyle, Albert S. , title =. Econometrica , volume =

-

[10]

and Milgrom, Paul R

Glosten, Lawrence R. and Milgrom, Paul R. , title =. Journal of Financial Economics , volume =

-

[11]

and O'Hara, Maureen and Paperman, Joseph B

Easley, David and Kiefer, Nicholas M. and O'Hara, Maureen and Paperman, Joseph B. , title =. Journal of Finance , volume =

-

[12]

and O'Hara, Maureen , title =

Easley, David and Kiefer, Nicholas M. and O'Hara, Maureen , title =. Review of Financial Studies , volume =

-

[13]

Journal of Finance , volume =

Easley, David and Hvidkjaer, Soeren and O'Hara, Maureen , title =. Journal of Finance , volume =

-

[14]

Journal of Financial Economics , volume =

Duarte, Jefferson and Young, Lance , title =. Journal of Financial Economics , volume =

-

[15]

Flow Toxicity and Liquidity in a High-Frequency World , journal =

Easley, David and L. Flow Toxicity and Liquidity in a High-Frequency World , journal =

-

[16]

and Bondarenko, Oleg , title =

Andersen, Torben G. and Bondarenko, Oleg , title =. Journal of Financial Markets , volume =

-

[17]

and Ready, Mark J

Lee, Charles M.\ C. and Ready, Mark J. , title =. Journal of Finance , volume =

-

[18]

, title =

Hawkes, Alan G. , title =. Biometrika , volume =

-

[19]

Quarterly Journal of Economics , volume =

Budish, Eric and Cramton, Peter and Shim, John , title =. Quarterly Journal of Economics , volume =

-

[20]

, title =

Platt, John C. , title =. Advances in Large Margin Classifiers , publisher =. 1999 , pages =

1999

-

[21]

Proceedings of the 22nd International Conference on Machine Learning (ICML) , pages =

Niculescu-Mizil, Alexandru and Caruana, Rich , title =. Proceedings of the 22nd International Conference on Machine Learning (ICML) , pages =

-

[22]

arXiv preprint arXiv:2508.03474 , year =

Saguillo, Oriol and Ghafouri, Vahid and Kiffer, Lucianna and Suarez-Tangil, Guillermo , title =. arXiv preprint arXiv:2508.03474 , year =

-

[23]

2026 , howpublished =

Mitts, Joshua and Ofir, Moran , title =. 2026 , howpublished =

2026

-

[24]

2020 IEEE Symposium on Security and Privacy (S&P) , pages =

Daian, Philip and Goldfeder, Steven and Kell, Tyler and Li, Yunqi and Zhao, Xueyuan and Bentov, Iddo and Breidenbach, Lorenz and Juels, Ari , title =. 2020 IEEE Symposium on Security and Privacy (S&P) , pages =

2020

-

[25]

and Tetlock, Philip E

Schoenegger, Philipp and Tuminello, Peter S. and Tetlock, Philip E. and Karger, Ezra and Atanasov, Pavel , title =. Science Advances , volume =. 2024 , doi =

2024

-

[26]

, title =

Leetaru, Kalev and Schrodt, Philip A. , title =. Annual Convention of the International Studies Association , year =

-

[27]

2026 , month = apr, note =

Nechepurenko, Maksym , title =. 2026 , month = apr, note =

2026

-

[28]

2026 , note =

Nechepurenko, Maksym and Shuvalov, Pavel , title =. 2026 , note =

2026

-

[29]

Soros, George , title =

-

[30]

, title =

Schelling, Thomas C. , title =

-

[31]

, title =

Manski, Charles F. , title =. Economics Letters , volume =

-

[32]

2026 , note =

Tsang, Kwok Ping and Yang, Zichao , title =. 2026 , note =

2026

-

[33]

and Peng, L

Ng, H. and Peng, L. and Tao, Y. and Zhou, D. , title =. 2026 , note =

2026

-

[34]

and Huang, Taeyoung , title =

Clinton, Joshua D. and Huang, Taeyoung , title =. 2025 , note =

2025

-

[35]

, title =

Murphy, Allan H. , title =. Journal of Applied Meteorology , volume =

-

[36]

, title =

Brier, Glenn W. , title =. Monthly Weather Review , volume =

-

[37]

, title =

Gneiting, Tilmann and Raftery, Adrian E. , title =. Journal of the American Statistical Association , volume =

-

[38]

2026 , note =

Nechepurenko, Maksym , title =. 2026 , note =

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.