Recognition: unknown

Dynamics of Periodic Bubbles and Crashes: Modeling Market Overheating and Panic Selling via Cubic Momentum

Pith reviewed 2026-05-10 01:51 UTC · model grok-4.3

The pith

A minimal discrete-time model with a cubic momentum function and momentum-linked trading frequency generates periodic financial bubbles and crashes endogenously.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

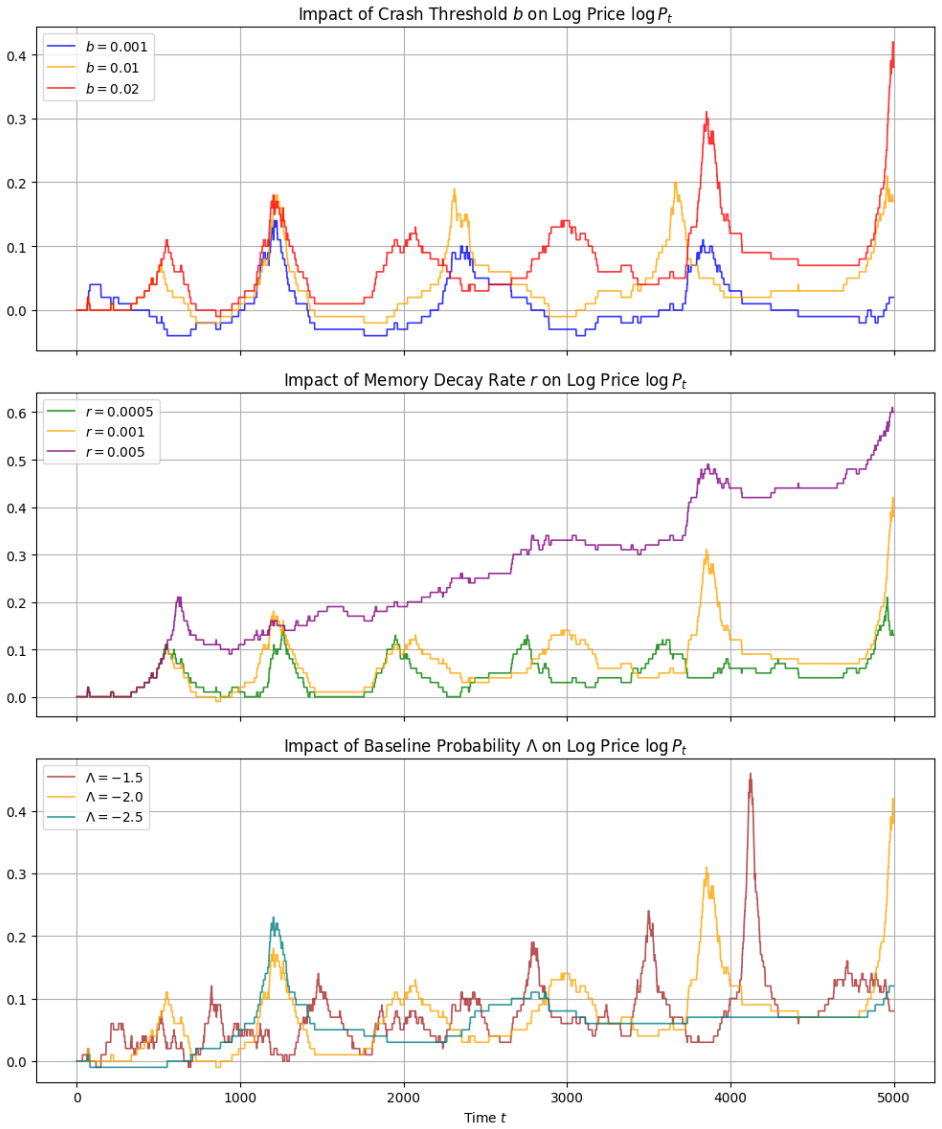

The model employs a cubic function of market momentum to dictate the proportion of buy versus sell trades, promoting trend-following when momentum is moderate and reversing when it exceeds a critical value. Trading intensity is made proportional to the integrated momentum, mimicking self-excitation. Numerical simulations of this system exhibit repeated episodes of rapid price appreciation accompanied by increased trading volume, terminated by abrupt collapses.

What carries the argument

Cubic function of market momentum that sets the buy-sell imbalance, together with trading frequency scaled directly to accumulated momentum.

If this is right

- The model produces simultaneous surges in price and liquidity during the bubble phase without external news.

- A sharp reversal to net selling occurs automatically once momentum exceeds the critical threshold.

- Periodic repetition of bubbles and crashes arises solely from the internal feedback between momentum and trading rules.

- Liquidity and price move together because trading frequency itself increases with momentum.

Where Pith is reading between the lines

- If the cubic shape matches how real traders respond to momentum, the model offers a way to estimate the location of the panic threshold from observed order-flow data.

- The same minimal rules could be applied to other self-exciting processes such as volatility spikes or liquidity dry-ups.

- Calibrating the threshold and cubic coefficients to historical episodes would test whether actual bubbles display the predicted momentum-triggered flip.

Load-bearing premise

The balance of trading directions is governed by a cubic function of market momentum and trading frequency is directly proportional to accumulated momentum.

What would settle it

A simulation run under the stated cubic and frequency rules that fails to produce repeated surges in price and liquidity followed by crashes, or empirical market data showing no cubic-like reversal in order imbalance near high-momentum thresholds.

Figures

read the original abstract

This paper proposes a simple and parsimonious discrete-time simulation model to describe the endogenous formation and periodic collapse of financial bubbles. While existing literature has extensively explored the statistical properties of locally explosive bubble dynamics, capturing the micro-level interplay of investor herd behavior and panic selling within a unified framework remains a challenge. Our model addresses this by introducing a cubic function of market momentum to determine the balance of trading directions. This mechanism drives both trend-following behavior during the bubble phase and sudden market crashes when the momentum exceeds a critical threshold. Furthermore, inspired by the self-exciting nature of the Hawkes process, the model endogenizes``market frenzy" by linking trading frequency directly to the accumulated momentum. Simulation results demonstrate that this minimal setup successfully replicates the complex, nonlinear dynamics of bubbles, including simultaneous surges in liquidity and price, followed by dramatic crashes.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a discrete-time simulation model for endogenous formation and periodic collapse of financial bubbles. It determines the balance of trading directions via a cubic function of market momentum (driving trend-following and threshold-triggered crashes) and endogenizes trading frequency as directly proportional to accumulated momentum, inspired by Hawkes processes. The central claim is that this minimal setup successfully replicates complex nonlinear bubble dynamics, including simultaneous surges in liquidity and price followed by dramatic crashes.

Significance. If the simulation results and underlying mechanisms prove robust, the model could offer a parsimonious framework linking herd behavior and panic selling in a unified endogenous setup, potentially complementing existing work on locally explosive bubbles. However, the current lack of explicit equations, calibrated parameter values, sensitivity analyses, or empirical comparisons to real data substantially reduces its immediate contribution and reproducibility.

major comments (2)

- [Abstract] Abstract: The claim that 'this minimal setup successfully replicates' the surge-crash patterns rests on the specific cubic mapping from momentum to net trading direction plus the direct proportionality of trading intensity to accumulated momentum. No explicit polynomial coefficients, critical threshold value, or frenzy scaling factor are supplied, nor is any sensitivity analysis to modest changes in these free parameters or to alternative functional forms (e.g., other odd-powered saturating maps) provided. This makes the replication claim unevaluable and raises the possibility that the periodic behavior is an artifact of parameter choices rather than a robust consequence of the proposed mechanism.

- [Simulation Results] Simulation Results section: The manuscript asserts that simulations demonstrate simultaneous liquidity/price surges followed by threshold-triggered crashes, yet supplies no equations, parameter table, robustness checks across initial conditions or stochastic realizations, or quantitative comparison to observed market data. Without these, the central replication claim cannot be assessed for soundness or generality.

minor comments (1)

- [Model Description] The introduction of 'market frenzy' as an invented entity linked to momentum would benefit from a clearer operational definition and distinction from the momentum variable itself to avoid potential notational overlap.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which help clarify how to strengthen the presentation of our simulation model. We will revise the manuscript to supply the missing explicit specifications, parameters, and robustness checks while preserving the paper's focus on endogenous bubble dynamics.

read point-by-point responses

-

Referee: [Abstract] Abstract: The claim that 'this minimal setup successfully replicates' the surge-crash patterns rests on the specific cubic mapping from momentum to net trading direction plus the direct proportionality of trading intensity to accumulated momentum. No explicit polynomial coefficients, critical threshold value, or frenzy scaling factor are supplied, nor is any sensitivity analysis to modest changes in these free parameters or to alternative functional forms (e.g., other odd-powered saturating maps) provided. This makes the replication claim unevaluable and raises the possibility that the periodic behavior is an artifact of parameter choices rather than a robust consequence of the proposed mechanism.

Authors: We agree that the abstract is too high-level and does not supply the concrete coefficients or thresholds needed for evaluation. In the revised version we will state the exact cubic mapping (including all polynomial coefficients), the critical momentum threshold that triggers the sign reversal, and the proportionality constant linking accumulated momentum to trading intensity. We will also add a sensitivity analysis subsection that varies these parameters over modest ranges and tests an alternative saturating odd-powered map to confirm that the periodic surge-crash cycle is a robust outcome of the mechanism rather than a narrow parameter artifact. revision: yes

-

Referee: [Simulation Results] Simulation Results section: The manuscript asserts that simulations demonstrate simultaneous liquidity/price surges followed by threshold-triggered crashes, yet supplies no equations, parameter table, robustness checks across initial conditions or stochastic realizations, or quantitative comparison to observed market data. Without these, the central replication claim cannot be assessed for soundness or generality.

Authors: We accept that the Simulation Results section must be expanded for reproducibility. The revised manuscript will present the full discrete-time update equations, a table of all parameter values used, and new figures showing trajectories under varied initial conditions and multiple independent stochastic realizations. Because the study is a parsimonious theoretical simulation whose primary goal is to illustrate endogenous periodicity, we will not add a full empirical calibration exercise; however, we will include a short discussion that qualitatively maps the simulated liquidity-price co-movements and crash thresholds onto well-documented historical episodes. revision: partial

Circularity Check

Replication of surge-crash dynamics is by construction of the cubic trading-balance rule and momentum-proportional frequency

specific steps

-

self definitional

[Abstract]

"Our model addresses this by introducing a cubic function of market momentum to determine the balance of trading directions. This mechanism drives both trend-following behavior during the bubble phase and sudden market crashes when the momentum exceeds a critical threshold. Furthermore, inspired by the self-exciting nature of the Hawkes process, the model endogenizes market frenzy by linking trading frequency directly to the accumulated momentum. Simulation results demonstrate that this minimal setup successfully replicates the complex, nonlinear dynamics of bubbles, including simultaneous surg"

The cubic function and proportionality rule are introduced precisely because they 'drive' the desired behaviors (trend-following, threshold crashes, frenzy). The subsequent claim that simulations 'successfully replicate' those same behaviors is therefore tautological: the output patterns are the direct, intended consequence of the input functional forms and threshold rather than a derived or emergent result.

full rationale

The paper defines its core mechanisms (cubic mapping from momentum to net trading direction plus direct proportionality of trading intensity to accumulated momentum, with an explicit critical threshold) expressly to generate trend-following, liquidity surges, threshold-triggered panic selling, and self-exciting frenzy. The central claim that 'this minimal setup successfully replicates' the observed bubble-crash patterns therefore reduces directly to the outcome of those definitional choices rather than emerging as an independent consequence. No external validation, robustness checks against alternative functional forms, or parameter-free derivation is supplied.

Axiom & Free-Parameter Ledger

free parameters (3)

- cubic coefficients

- critical momentum threshold

- frenzy scaling factor

axioms (2)

- domain assumption Investor trading direction is fully determined by a cubic polynomial of current momentum.

- domain assumption Trading intensity increases linearly with accumulated momentum.

invented entities (1)

-

market frenzy

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Mathematical and Computer Modelling , volume=

Nabla discrete fractional calculus and nabla inequalities , author=. Mathematical and Computer Modelling , volume=. 2010 , publisher=

2010

-

[2]

Right nabla discrete fractional calculus , author=. Int. J. Difference Equ , volume=

-

[3]

The Rocky Mountain Journal of Mathematics , pages=

Linear systems of fractional nabla difference equations , author=. The Rocky Mountain Journal of Mathematics , pages=. 2011 , publisher=

2011

-

[4]

Statistics & Probability Letters , volume=

Large deviations for fractional Poisson processes , author=. Statistics & Probability Letters , volume=. 2013 , publisher=

2013

-

[5]

Journal of Applied Probability , volume=

Fractional Poisson process: long-range dependence and applications in ruin theory , author=. Journal of Applied Probability , volume=. 2014 , publisher=

2014

-

[6]

1982 , publisher=

Bubbles, rational expectations and financial markets , author=. 1982 , publisher=

1982

-

[7]

The European Physical Journal B-Condensed Matter and Complex Systems , volume=

A Langevin approach to stock market fluctuations and crashes , author=. The European Physical Journal B-Condensed Matter and Complex Systems , volume=. 1998 , publisher=

1998

-

[8]

1988 , publisher=

An Introduction to the Theory of Point Processes , author=. 1988 , publisher=

1988

-

[9]

Journal of Economic Dynamics and control , volume=

A simple discrete-time approximation of continuous-time bubbles , author=. Journal of Economic Dynamics and control , volume=. 1998 , publisher=

1998

-

[10]

Communications in nonlinear science and numerical simulation , volume=

Fractional poisson process , author=. Communications in nonlinear science and numerical simulation , volume=. 2003 , publisher=

2003

-

[11]

Probability in the Engineering and Informational Sciences , volume=

On a Poisson hyperbolic staircase , author=. Probability in the Engineering and Informational Sciences , volume=. 1999 , publisher=

1999

-

[12]

Journal of Applied Probability , volume=

On the long-range dependence of fractional Poisson and negative binomial processes , author=. Journal of Applied Probability , volume=. 2016 , publisher=

2016

-

[13]

The fractional Poisson process and the inverse stable subordinator , author=

-

[14]

RIMS Kokyuroku , volume=

Discrete Mittag-Leffler function and its applications (New , author=. RIMS Kokyuroku , volume=. 2003 , publisher=

2003

-

[15]

Advances in Difference Equations , volume=

Caputo type fractional difference operator and its application on discrete time scales , author=. Advances in Difference Equations , volume=. 2015 , publisher=

2015

-

[16]

Abstract and Applied Analysis , volume=

Discrete Mittag-Leffler functions in linear fractional difference equations , author=. Abstract and Applied Analysis , volume=. 2011 , organization=

2011

-

[17]

1991 , publisher=

Probability with Martingales , author=. 1991 , publisher=

1991

-

[18]

arXiv preprint arXiv:2401.07038 , year=

Bubble Modeling and Tagging: A Stochastic Nonlinear Autoregression Approach , author=. arXiv preprint arXiv:2401.07038 , year=

-

[19]

The American Economic Review , volume=

Explosive rational bubbles in stock prices? , author=. The American Economic Review , volume=. 1988 , publisher=

1988

-

[20]

International economic review , volume=

Explosive behavior in the 1990s Nasdaq: When did exuberance escalate asset values? , author=. International economic review , volume=. 2011 , publisher=

2011

-

[21]

International economic review , volume=

Testing for multiple bubbles: Historical episodes of exuberance and collapse in the S&P 500 , author=. International economic review , volume=. 2015 , publisher=

2015

-

[22]

Biometrika , volume=

Spectra of some self-exciting and mutually exciting point processes , author=. Biometrika , volume=. 1971 , publisher=

1971

-

[23]

Quantitative Finance , volume=

Quadratic Hawkes processes for financial prices , author=. Quantitative Finance , volume=. 2017 , publisher=

2017

-

[24]

The European Journal of Finance , volume=

Non-parametric estimation of quadratic Hawkes processes for order book events , author=. The European Journal of Finance , volume=. 2022 , publisher=

2022

-

[25]

Journal of political Economy , volume=

Market fundamentals versus price-level dynamics , author=. Journal of political Economy , volume=. 1980 , publisher=

1980

-

[26]

Econometrica: Journal of the Econometric Society , volume=

Asset bubbles and overlapping generations , author=. Econometrica: Journal of the Econometric Society , volume=. 1985 , publisher=

1985

-

[27]

The American Economic Review , volume=

Pitfalls in testing for explosive bubbles in asset prices , author=. The American Economic Review , volume=. 1991 , publisher=

1991

-

[28]

The American Economic Review , volume=

Intrinsic bubbles: The case of stock prices , author=. The American Economic Review , volume=. 1991 , publisher=

1991

-

[29]

Quantitative Finance , volume=

A simple mechanism for financial bubbles: time-varying momentum horizon , author=. Quantitative Finance , volume=. 2019 , publisher=

2019

-

[30]

1975 , publisher=

Statistical theory of reliability and life testing: probability models , author=. 1975 , publisher=

1975

-

[31]

1998 , publisher=

Records , author=. 1998 , publisher=

1998

-

[32]

Annals of Mathematical Statistics , volume=

Extremal processes , author=. Annals of Mathematical Statistics , volume=. 1964 , publisher=

1964

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.