Recognition: unknown

SBCA: Cross-Modal BERT-driven Actor-Critic for Multi-Asset Portfolio Optimization

Pith reviewed 2026-05-10 15:26 UTC · model grok-4.3

The pith

SBCA fuses BERT text features with price data in an actor-critic model to outperform benchmarks in multi-asset portfolio optimization.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

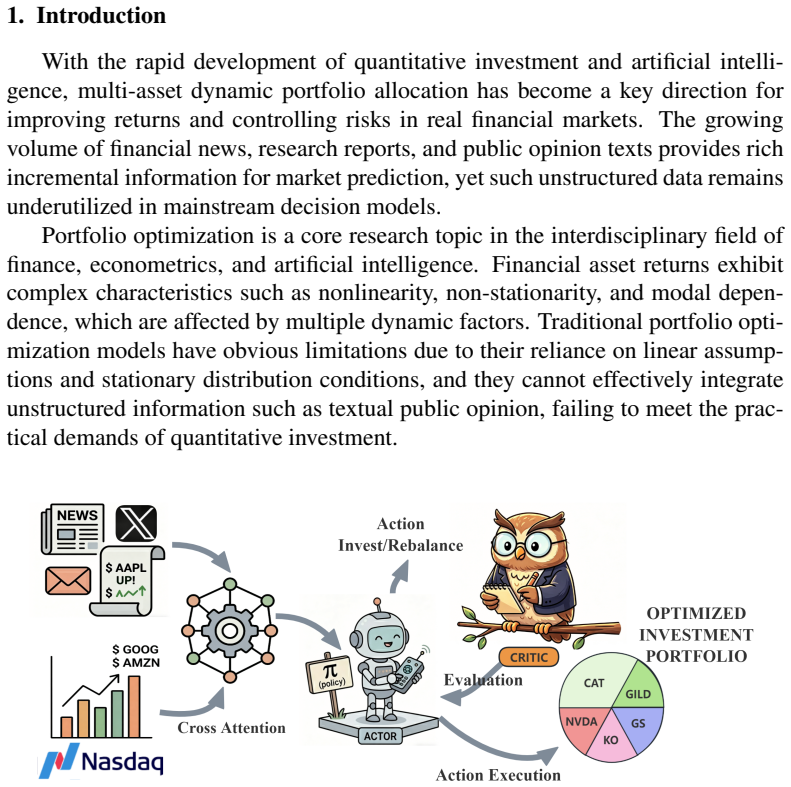

SBCA is a cross-modal BERT-driven Actor-Critic framework that adaptively integrates price time-series features and text semantic features via a gated fusion mechanism, incorporates downside risk and turnover constraints into the reward function, and achieves superior performance in portfolio optimization tasks as validated through extensive experiments on long-term U.S. stock datasets.

What carries the argument

Cross-modal gated fusion mechanism within a BERT-driven Actor-Critic reinforcement learning framework, which adaptively merges multi-modal financial inputs to generate actions under explicit risk and turnover constraints.

If this is right

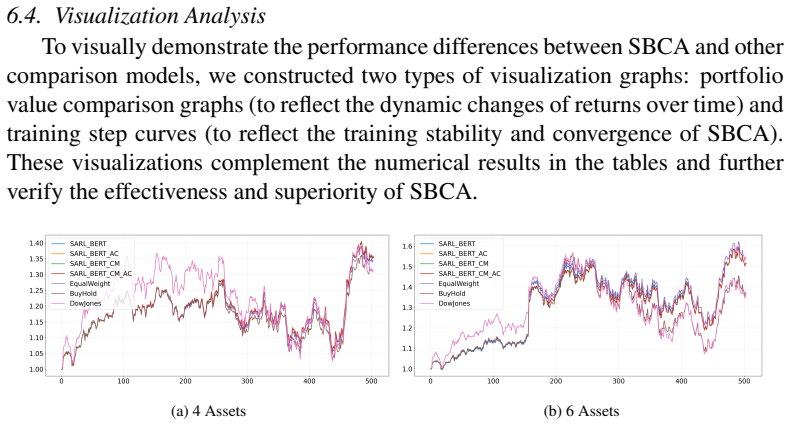

- SBCA generates higher portfolio values and annual returns than equal-weight, buy-and-hold, and market benchmarks.

- The model delivers improved Sharpe ratios indicating better risk-adjusted performance.

- Maximum drawdowns are reduced, offering better downside protection during market stress.

- Performance holds under varying transaction costs, confirming cost robustness.

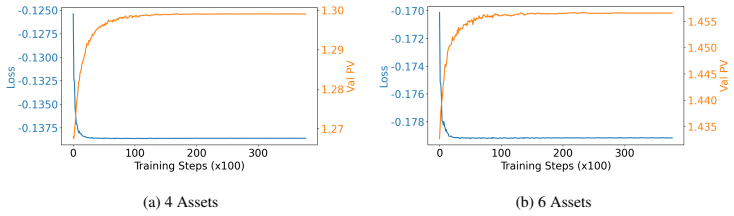

- Ablation removing the fusion module or actor-critic structure degrades results, showing both are necessary.

Where Pith is reading between the lines

- The approach could extend to real-time news feeds to respond faster to events outside the historical test window.

- Similar fusion might incorporate additional data like earnings calls or regulatory filings for broader decision support.

- Embedded constraints allow direct compliance with investor mandates without separate post-trade adjustments.

- The method's end-to-end nature reduces reliance on separate prediction and optimization stages common in quant pipelines.

Load-bearing premise

The gated fusion of price time-series and BERT-derived text features produces meaningfully better portfolio actions than price data alone when risk and turnover penalties are applied.

What would settle it

Running the same 11-year experiments but replacing the cross-modal fusion with price-only inputs and finding no gain in Sharpe ratio or maximum drawdown would falsify the benefit of adding text features.

Figures

read the original abstract

Portfolio optimization is constrained by linear assumptions and insufficient integration of multi-modal information in traditional models. This paper proposes a cross-modal BERT-driven Actor-Critic framework SBCA for multi-asset portfolio optimization to address the deficiencies of existing deep reinforcement learning DRL methods in fusing price data and financial text sentiment, as well as lacking practical trading constraints. The framework adopts a cross-modal gated fusion mechanism to adaptively integrate price time-series features and text semantic features, embeds downside risk and turnover penalty constraints into the reward function, and constructs a complete empirical system for validation. Experiments on 11-year U.S. stock multi-asset datasets show that SBCA outperforms equal weight, buy-and-hold and market benchmark strategies in portfolio value, annual return, Sharpe ratio and maximum drawdown. Ablation studies verify the complementary enhancement of Actor-Critic mechanism and cross-modal fusion module. Cost sensitivity analysis confirms the model's robustness under varying transaction costs. SBCA provides an effective and interpretable end-to-end solution for dynamic quantitative portfolio decision-making.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes SBCA, a cross-modal BERT-driven Actor-Critic framework for multi-asset portfolio optimization. It employs a gated fusion mechanism to integrate price time-series features with BERT-derived text semantic features, embeds downside risk and turnover penalties directly into the reward function, and reports outperformance versus equal-weight, buy-and-hold, and market benchmarks on an 11-year U.S. stock multi-asset dataset in terms of portfolio value, annual return, Sharpe ratio, and maximum drawdown. Ablation studies are said to confirm the value of the Actor-Critic structure and fusion module, while cost-sensitivity tests demonstrate robustness.

Significance. If the empirical claims are supported by verifiable experimental controls and feasible action spaces, the work would offer a practical advance in computational finance by showing how multi-modal DRL can incorporate sentiment alongside price data while respecting trading frictions. The explicit embedding of risk and turnover penalties in the reward is a constructive step beyond purely return-maximizing DRL formulations.

major comments (3)

- [Abstract and framework description] Abstract and framework description: the actor is stated to produce portfolio decisions under embedded risk and turnover penalties, yet no normalization (softmax, simplex projection, or post-processing) is described to enforce non-negative weights that sum to one. Because the central performance claims rest on dynamic allocations that are compared to feasible benchmarks, the absence of a hard feasibility step means the reported Sharpe, return, and drawdown advantages could be artifacts of invalid weight vectors that the soft penalties only discourage rather than forbid.

- [Experiments section] Experiments section: the abstract asserts clear outperformance and robustness from ablation and cost-sensitivity tests, but supplies no information on data splits (train/validation/test periods), statistical significance testing of metric differences, baseline implementation details, or overfitting controls. These omissions leave the central performance claim unsupported by verifiable detail and prevent assessment of whether the 11-year results generalize.

- [Ablation studies] Ablation studies: the claim that the Actor-Critic mechanism and cross-modal fusion module provide complementary enhancement is presented without quantitative isolation of the gated fusion parameters or controls for the additional degrees of freedom they introduce. This weakens the ability to attribute gains specifically to the invented cross-modal component rather than to increased model capacity.

minor comments (1)

- [Title and abstract] The title and abstract introduce the acronym SBCA without an immediate parenthetical expansion, which reduces immediate readability for readers unfamiliar with the framework.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed review. The comments highlight important areas for improving clarity and rigor. We address each major comment point by point below and will revise the manuscript to incorporate the necessary additions and clarifications.

read point-by-point responses

-

Referee: [Abstract and framework description] Abstract and framework description: the actor is stated to produce portfolio decisions under embedded risk and turnover penalties, yet no normalization (softmax, simplex projection, or post-processing) is described to enforce non-negative weights that sum to one. Because the central performance claims rest on dynamic allocations that are compared to feasible benchmarks, the absence of a hard feasibility step means the reported Sharpe, return, and drawdown advantages could be artifacts of invalid weight vectors that the soft penalties only discourage rather than forbid.

Authors: We agree that the framework description in the original manuscript does not explicitly detail the normalization procedure for the actor outputs. In our implementation the actor applies a softmax activation to produce weights that are non-negative and sum to one; this hard constraint operates alongside the soft risk and turnover penalties in the reward. We will revise the relevant sections (including the framework description and, space permitting, the abstract) to clearly state this normalization step and confirm that all reported allocations satisfy the simplex constraint. revision: yes

-

Referee: [Experiments section] Experiments section: the abstract asserts clear outperformance and robustness from ablation and cost-sensitivity tests, but supplies no information on data splits (train/validation/test periods), statistical significance testing of metric differences, baseline implementation details, or overfitting controls. These omissions leave the central performance claim unsupported by verifiable detail and prevent assessment of whether the 11-year results generalize.

Authors: We acknowledge that the experiments section lacks these essential details. In the revised manuscript we will specify the exact temporal train/validation/test splits, report statistical significance tests (e.g., paired t-tests or bootstrap confidence intervals) for the reported metric differences, provide additional implementation details for the baselines, and describe the overfitting controls employed (regularization, early stopping, and any cross-validation procedures). revision: yes

-

Referee: [Ablation studies] Ablation studies: the claim that the Actor-Critic mechanism and cross-modal fusion module provide complementary enhancement is presented without quantitative isolation of the gated fusion parameters or controls for the additional degrees of freedom they introduce. This weakens the ability to attribute gains specifically to the invented cross-modal component rather than to increased model capacity.

Authors: We accept that the ablation analysis would be strengthened by explicit controls for model capacity and isolation of the fusion mechanism. We will revise the ablation section to report parameter counts for each variant, provide quantitative values for the learned gated fusion parameters, and include an additional controlled comparison that matches capacity while varying only the cross-modal component. revision: yes

Circularity Check

No circularity: SBCA is an empirical proposal validated by experiments

full rationale

The paper introduces SBCA as a practical Actor-Critic architecture that fuses BERT text features with price time-series via gated cross-modal fusion and embeds risk/turnover penalties directly into the reward. All central claims rest on reported outperformance versus equal-weight, buy-and-hold and market benchmarks on an 11-year multi-asset dataset, plus ablation and cost-sensitivity checks. No derivation chain exists that reduces a claimed result to a fitted parameter or self-citation by construction; the framework is presented as an end-to-end trainable system whose merit is external to its own definitions.

Axiom & Free-Parameter Ledger

free parameters (1)

- gated fusion parameters

axioms (1)

- domain assumption Actor-Critic reinforcement learning is suitable for sequential multi-asset portfolio decisions under uncertainty

invented entities (1)

-

cross-modal gated fusion mechanism

no independent evidence

Reference graph

Works this paper leans on

- [1]

-

[2]

arXiv preprint arXiv:1901.08740 , year=

Model-based deep reinforcement learning for dynamic portfolio optimization , author=. arXiv preprint arXiv:1901.08740 , year=

-

[3]

IEEE Transactions on Knowledge and Data Engineering , year=

Cost-sensitive portfolio selection via deep reinforcement learning , author=. IEEE Transactions on Knowledge and Data Engineering , year=

-

[4]

Neural Computing and Applications , volume=

Dynamic portfolio rebalancing through reinforcement learning , author=. Neural Computing and Applications , volume=

-

[5]

Annals of Operations Research , year=

A reinforcement learning approach to dynamic portfolio optimization , author=. Annals of Operations Research , year=

-

[6]

arXiv preprint arXiv:2405.01604 , year=

Portfolio management using deep reinforcement learning , author=. arXiv preprint arXiv:2405.01604 , year=

-

[7]

arXiv preprint arXiv:2511.20678 , year=

Reinforcement learning-based cryptocurrency portfolio management using soft actor--critic and deep deterministic policy gradient algorithms , author=. arXiv preprint arXiv:2511.20678 , year=

-

[8]

International Journal of Computational Intelligence Systems , volume=

Risk-adjusted deep reinforcement learning for portfolio optimization: A multi-reward approach , author=. International Journal of Computational Intelligence Systems , volume=

-

[9]

arXiv preprint arXiv:2602.17098 , year=

Deep reinforcement learning for optimal portfolio allocation: A comparative study with mean-variance optimization , author=. arXiv preprint arXiv:2602.17098 , year=

-

[10]

Proceedings of the 3rd ACM International Conference on AI in Finance , pages=

Finrl: Deep reinforcement learning framework to automate trading in quantitative finance , author=. Proceedings of the 3rd ACM International Conference on AI in Finance , pages=

-

[11]

arXiv preprint arXiv:2011.09607v2 , year=

FinRL: A deep reinforcement learning library for automated stock trading in quantitative finance , author=. arXiv preprint arXiv:2011.09607v2 , year=

-

[12]

Advances in Neural Information Processing Systems , volume=

FinRL-meta: Market environments and benchmarks for data-driven financial reinforcement learning , author=. Advances in Neural Information Processing Systems , volume=

-

[13]

Finbert: Financial sentiment analysis with pre-trained language models

Finbert: Financial sentiment analysis with pre-trained language models , author=. arXiv preprint arXiv:1908.10063 , year=

-

[14]

Finbert: A pretrained language model for financial communications , author=. arXiv preprint arXiv:2006.08097 , year=

-

[15]

Proceedings of the Twenty-Ninth International Joint Conference on Artificial Intelligence , pages=

Finbert: A pre-trained financial language representation model for financial text mining , author=. Proceedings of the Twenty-Ninth International Joint Conference on Artificial Intelligence , pages=

-

[16]

Bert: Pre-training of deep bidirectional transformers for language understanding , author=. Proceedings of the 2019 Conference of the North American Chapter of the Association for Computational Linguistics: Human Language Technologies, Volume 1 (Long and Short Papers) , pages=

2019

-

[17]

arXiv preprint arXiv:2107.08721 , year=

Stock movement prediction with financial news using contextualized embedding from BERT , author=. arXiv preprint arXiv:2107.08721 , year=

-

[18]

International Conference on Knowledge Discovery and Information Retrieval , pages=

Stock trend prediction using financial market news and BERT , author=. International Conference on Knowledge Discovery and Information Retrieval , pages=

-

[19]

Neural Computing and Applications , volume=

Applying BERT to analyze investor sentiment in stock market , author=. Neural Computing and Applications , volume=

-

[20]

arXiv preprint arXiv:2410.01987 , year=

Financial sentiment analysis on news and reports using large language models and FinBERT , author=. arXiv preprint arXiv:2410.01987 , year=

-

[21]

Computational Economics , volume=

Enhancing sentiment analysis in stock market tweets through BERT-based knowledge transfer , author=. Computational Economics , volume=

-

[22]

arXiv preprint arXiv:2412.17293 , year=

Multimodal deep reinforcement learning for portfolio optimization , author=. arXiv preprint arXiv:2412.17293 , year=

-

[23]

European Conference on Artificial Intelligence , journal=

Cross-modal temporal fusion for financial market forecasting , author=. European Conference on Artificial Intelligence , journal=

-

[24]

Proceedings of the 6th ACM International Conference on AI in Finance , pages=

Modality-aware transformer for financial time series forecasting , author=. Proceedings of the 6th ACM International Conference on AI in Finance , pages=

-

[25]

IEEE Access , volume=

Sentiment-aware portfolio optimization: CVaR-based diversification with deep reinforcement learning , author=. IEEE Access , volume=

-

[26]

IEEE Access , volume=

A multimodal deep fusion method for stock movement prediction using heterogeneous data source , author=. IEEE Access , volume=

-

[27]

Proceedings of the 63rd Annual Meeting of the Association for Computational Linguistics , volume=

FLAG-TRADER: Fusion LLM-agent with gradient-based reinforcement learning for financial trading , author=. Proceedings of the 63rd Annual Meeting of the Association for Computational Linguistics , volume=

-

[28]

The Journal of Finance , volume=

Portfolio selection , author=. The Journal of Finance , volume=

-

[29]

The Review of Financial Studies , volume=

Optimal versus naive diversification: How inefficient is the 1/N portfolio strategy? , author=. The Review of Financial Studies , volume=

-

[30]

Journal of Economic Theory , volume=

Portfolio selection with transactions costs , author=. Journal of Economic Theory , volume=

-

[31]

Portfolio Selection

Markowitz's “Portfolio Selection”: A fifty-year retrospective , author=. The Journal of Finance , volume=

-

[32]

Proceedings of the National Academy of Sciences , year =

Richard Bellman and Robert Kalaba , title =. Proceedings of the National Academy of Sciences , year =

-

[33]

1998 , publisher =

Reinforcement Learning: An Introduction , author =. 1998 , publisher =

1998

-

[34]

2016 , publisher=

Deep learning , author=. 2016 , publisher=

2016

-

[35]

Proceedings of the AAAI Conference on Artificial Intelligence , volume=

Deeptrader: A deep reinforcement learning approach for risk-return balanced portfolio management with market conditions embedding , author=. Proceedings of the AAAI Conference on Artificial Intelligence , volume=

-

[36]

1948 , publisher=

Handbook of mathematical functions with formulas, graphs, and mathematical tables , author=. 1948 , publisher=

1948

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.