Recognition: unknown

Exact Likelihood Inference and Robust Filtering for Gauss-Cauchy Convolution Models

Pith reviewed 2026-05-09 16:59 UTC · model grok-4.3

The pith

Exact analytical expressions for the Gauss-Cauchy convolution density enable stable maximum likelihood estimation and robust filtering in state-space models.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

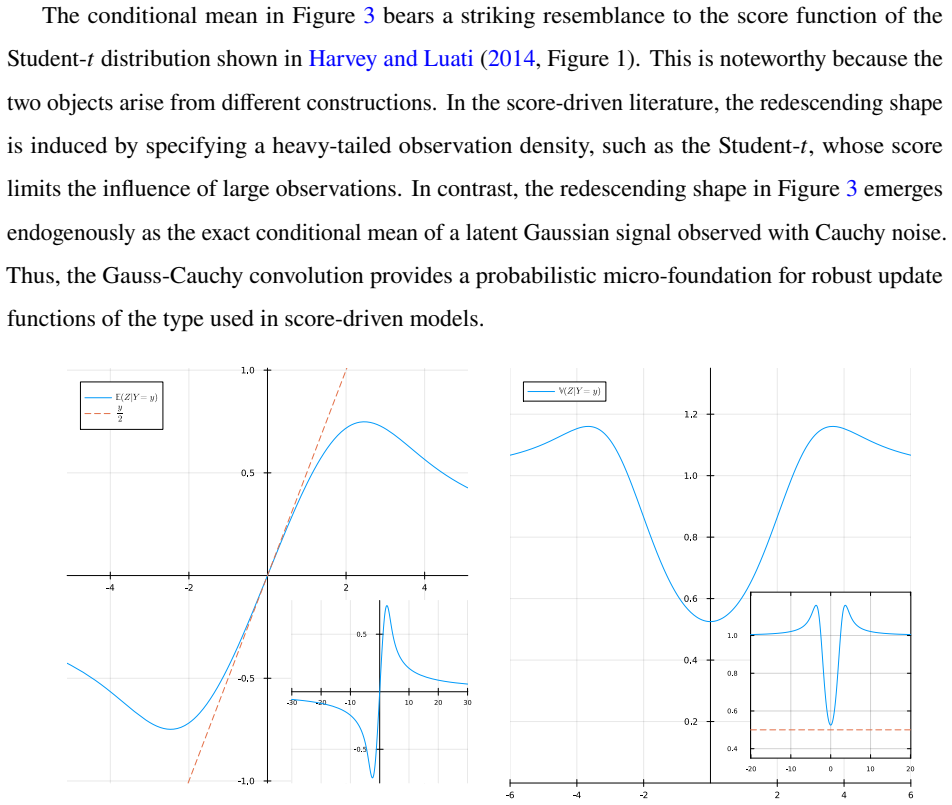

We derive analytical expressions for its density, score, Hessian, and conditional moments using the scaled complementary error function, enabling stable maximum likelihood estimation without numerical convolution, finite-difference derivatives, or pseudo-Voigt approximations. The conditional expectation of the latent Gaussian component is governed by a redescending location score, so extreme observations are automatically discounted rather than propagated. This structure motivates the Gauss-Cauchy Convolution (GCC) filter for state-space models with Gaussian latent dynamics and heavy-tailed measurement errors.

What carries the argument

The scaled complementary error function, which yields exact closed-form formulas for the density, derivatives, and conditional expectations of the Gauss-Cauchy convolution distribution.

If this is right

- Maximum likelihood estimation becomes stable and exact without requiring numerical convolution or derivative approximations.

- The GCC filter discounts extreme observations automatically rather than propagating them through the state.

- In volatility modeling, the filter separates persistent latent variation from transient measurement noise more effectively than Gaussian, Student-t, or Huber alternatives.

Where Pith is reading between the lines

- Similar analytical derivations could apply to other convolution distributions encountered in signal processing or spectroscopy.

- Testing the filter on simulated data with known heavy-tailed noise would confirm its robustness advantages.

- The approach may generalize to multivariate settings or non-linear state dynamics if the conditional moments remain tractable.

Load-bearing premise

The observed data are generated exactly from a convolution of Gaussian and Cauchy distributions, and the complementary error function evaluations remain numerically stable for the parameter values arising in estimation.

What would settle it

Numerical verification that the analytical density matches the result of direct numerical convolution to within machine precision for a range of parameter values, or out-of-sample comparison showing superior filtering performance on data simulated from the model.

Figures

read the original abstract

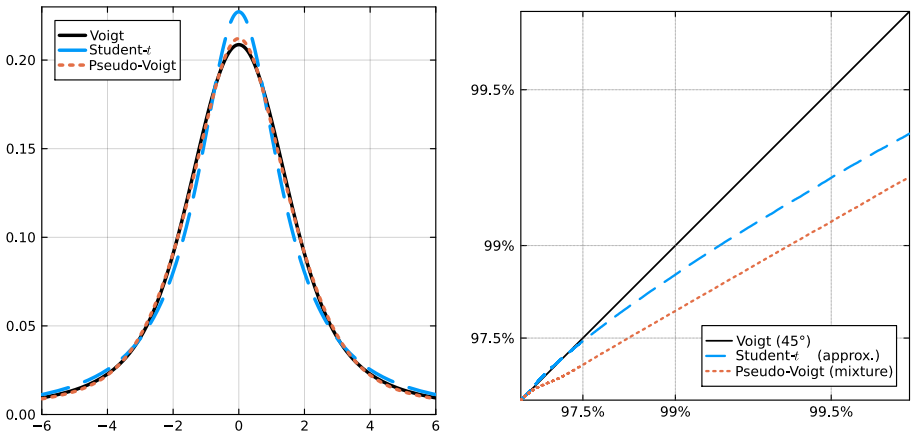

The convolution of a Gaussian and a Cauchy distribution, known as the Voigt distribution, is widely used in spectroscopy and provides a natural framework for modeling heavy-tailed measurement noise. We derive analytical expressions for its density, score, Hessian, and conditional moments using the scaled complementary error function, enabling stable maximum likelihood estimation without numerical convolution, finite-difference derivatives, or pseudo-Voigt approximations. The conditional expectation of the latent Gaussian component is governed by a redescending location score, so extreme observations are automatically discounted rather than propagated. This structure motivates the Gauss-Cauchy Convolution (GCC) filter for state-space models with Gaussian latent dynamics and heavy-tailed measurement errors. In an application to log realized volatility for the Technology Select Sector SPDR Fund, the GCC filter separates persistent latent variation from transient measurement noise and improves on Gaussian, Student-$t$, Huber, and related robust alternatives.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript derives analytical expressions for the density, score, Hessian, and conditional moments of the Gauss-Cauchy convolution (Voigt) distribution using the scaled complementary error function. These closed forms support exact maximum likelihood estimation and motivate the Gauss-Cauchy Convolution (GCC) filter for state-space models with Gaussian latent dynamics and heavy-tailed measurement errors. The conditional expectation exhibits a redescending property that automatically discounts extreme observations. An application to log realized volatility of the Technology Select Sector SPDR Fund compares the GCC filter favorably to Gaussian, Student-t, and Huber alternatives.

Significance. If the derivations are correct, the work provides a useful exact-inference tool for Voigt noise models that avoids numerical convolution and finite-difference derivatives. The redescending conditional expectation is a theoretically attractive robustness feature. The empirical illustration in financial volatility data demonstrates potential practical value, though its strength rests on the stability and accuracy of the analytic expressions across relevant parameter regimes.

major comments (1)

- [§2] §2 (Gauss-Cauchy Convolution Distribution): The central claim of stable MLE without numerical issues rests on the scaled complementary error function remaining well-behaved. The manuscript should supply explicit numerical checks or bounds demonstrating that the density, score, and Hessian expressions do not suffer from underflow, overflow, or loss of precision for scale and location values encountered in the volatility application (e.g., |z| > 10 in the complex plane).

minor comments (3)

- [Abstract] Abstract: The phrase 'pseudo-Voigt approximations' is used without a reference or brief definition; adding one sentence or a citation would improve accessibility for readers outside spectroscopy.

- [§4] §4 (GCC Filter): The state-space recursion for the filter is presented clearly, but the transition from the conditional expectation to the filter update equation would benefit from an explicit one-step-ahead prediction formula to aid replication.

- [§5] §5 (Empirical Application): Table 1 reports likelihood values and parameter estimates; including standard errors derived from the analytic Hessian (rather than only point estimates) would strengthen the comparison with competing filters.

Simulated Author's Rebuttal

We thank the referee for the careful review and valuable feedback on our manuscript. We address the major comment below and will incorporate the suggested improvements in the revised version.

read point-by-point responses

-

Referee: [§2] §2 (Gauss-Cauchy Convolution Distribution): The central claim of stable MLE without numerical issues rests on the scaled complementary error function remaining well-behaved. The manuscript should supply explicit numerical checks or bounds demonstrating that the density, score, and Hessian expressions do not suffer from underflow, overflow, or loss of precision for scale and location values encountered in the volatility application (e.g., |z| > 10 in the complex plane).

Authors: We appreciate the referee's emphasis on verifying the numerical stability of our analytic expressions. The use of the scaled complementary error function is motivated by its known numerical properties that prevent overflow for large complex arguments, as documented in the numerical analysis literature. Nevertheless, to strengthen the manuscript, we will add explicit numerical checks in a new subsection of §2. These will include evaluations of the density, score, and Hessian for parameter values typical of the volatility application, covering |z| > 10 in the complex plane, demonstrating absence of underflow, overflow, or significant loss of precision. We will also provide bounds where possible based on the asymptotic behavior of the erfcx function. revision: yes

Circularity Check

No significant circularity; derivations are self-contained

full rationale

The paper's central contribution is the derivation of closed-form expressions for the Voigt density, score, Hessian, and conditional moments expressed via the scaled complementary error function (a standard special function equivalent to the real part of the Faddeeva function). These follow directly from the definition of the Gauss-Cauchy convolution and known analytic properties of the erfc function; no step reduces a claimed prediction or uniqueness result to a fitted parameter, self-definition, or load-bearing self-citation. The redescending conditional expectation is a direct consequence of the Cauchy tail and does not rely on data-dependent fitting or prior author results as an unverified axiom. The application to realized volatility is presented as an illustration, not as the source of the analytic forms. The derivation chain is therefore independent of its own outputs.

Axiom & Free-Parameter Ledger

axioms (1)

- standard math The convolution integral of Gaussian and Cauchy densities admits an exact closed-form representation via the scaled complementary error function.

invented entities (1)

-

GCC filter

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =

Ole E. Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =. Econometrica , volume =

-

[2]

Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =

Ole E. Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =. Econometrics Journal , volume =

-

[3]

Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =

Ole E. Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =. Journal of Econometrics , volume =

-

[4]

Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =

Ole E. Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =. Jounal of Econometrics , volume =

-

[5]

Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =

Ole E. Barndorff-Nielsen and Peter Reinhard Hansen and Asger Lunde and Neil Shephard , title =. 2004 , note =

2004

-

[6]

Central Limit Theorems for Dependent Heterogeneous Random Variables , journal =

Robert. Central Limit Theorems for Dependent Heterogeneous Random Variables , journal =. 1997 , volume =

1997

-

[7]

2003 , author =

Dynamic economics , publisher =. 2003 , author =

2003

-

[8]

Balladurette and Juppette: A Discrete Analysis of Scrapping Subsidies , journal =

Adda, Jerome and Cooper,. Balladurette and Juppette: A Discrete Analysis of Scrapping Subsidies , journal =. 2000 , volume =

2000

-

[9]

Review of Financial Studies , year =

Anat Admati and Paul Pfleiderer , title =. Review of Financial Studies , year =

-

[10]

S. K. Ahn and G. C. Reinsel , title =. Journal of the American Statistical Association , year =

-

[11]

G. P. Aielli , title =. Journal of Business and Economic Statistics , year =

-

[12]

Testing Continuous-Time Models of the Spot Interest Rate , journal =

A. Testing Continuous-Time Models of the Spot Interest Rate , journal =. 1996 , volume =

1996

-

[13]

High-Frequency Covariance Estimates With Noisy and Asynchronous Financial Data , journal =

A. High-Frequency Covariance Estimates With Noisy and Asynchronous Financial Data , journal =

-

[14]

and Kalnina, I

Ait-Sahalia, Y. and Kalnina, I. and Xiu, D. , title =. Working Paper , year =

-

[15]

1974 , volume =

Hirotugu Akaike , title =. 1974 , volume =

1974

-

[16]

Journal of the Royal Statistical Society: Series D (The Statistician) , year =

Hirotugu Akaike , title =. Journal of the Royal Statistical Society: Series D (The Statistician) , year =

-

[17]

Jounalisten, Sept

Jakob Albrecht , title =. Jounalisten, Sept. 20, 2013 , year =

2013

-

[18]

Alexander and Jane F

Lorraine N. Alexander and Jane F. Seward and Tammy A. Santibanez and Mark A. Pallansch and Olen M. Kew and D. Rebecca Prevots and Peter M. Strebel and Joanne Cono and Melinda Wharton and Walter A. Orenstein and Roland W. Sutter , title =. Journal of the American Medical Association , year =

-

[19]

Alizadeh and M

S. Alizadeh and M. Brandt and Frank X. Diebold , title =. Journal of Finance , year =

-

[20]

Journal of Economic Perspectives , year =

Hunt Allcott and Matthew Gentzkow , title =. Journal of Economic Perspectives , year =

-

[21]

1985 , author =

Advanced Econometrics , publisher =. 1985 , author =

1985

-

[22]

Journal of Business and Economic Statistics , year =

Amisano, Gianni and Giacomini, Raffaella , title =. Journal of Business and Economic Statistics , year =

-

[23]

Journal of Health Economics , year =

Dan Anderberg and Arnaud Chevalier and Jonathan Wadsworth , title =. Journal of Health Economics , year =

-

[24]

Diebold , title =

Torben Andersen and Tim Bollerslev and Francis X. Diebold , title =. Review of Economics and Statistics , year =

-

[25]

Diebold and Paul Labys , title =

Torben Andersen and Tim Bollerslev and Francis X. Diebold and Paul Labys , title =. NBER Working Paper 8160 , year =

-

[26]

Journal of Econometrics , year =

Torben Andersen and Dobrislav Dobrev and Ernst Schaumburg , title =. Journal of Econometrics , year =

-

[27]

Working paper , year =

Torben Andersen and Dobrislav Dobrev and Ernst Schaumburg , title =. Working paper , year =

-

[28]

Andersen and Tim Bollerslev , title =

Torben G. Andersen and Tim Bollerslev , title =. Journal of Finance , volume =

-

[29]

International Economic Review , volume =

Andersen, Torben G and Bollerslev, Tim , title =. International Economic Review , volume =

-

[30]

and Bollerslev, Tim , title =

Andersen, Torben G. and Bollerslev, Tim , title =. Journal of Empirical Finance , year =

-

[31]

and Bollerslev, Tim and Cai, Jun , title =

Andersen, Torben G. and Bollerslev, Tim and Cai, Jun , title =. Journal of International Financial Markets, Institutions and Money , year =

-

[32]

Andersen and Tim Bollerslev and Francis X

Torben G. Andersen and Tim Bollerslev and Francis X. Diebold , title =. Handbook of Financial Econometrics , publisher =. 2002 , editor =

2002

-

[33]

Andersen and Tim Bollerslev and Francis X

Torben G. Andersen and Tim Bollerslev and Francis X. Diebold , series =. 2010 , editor =

2010

-

[34]

Andersen and Tim Bollerslev and Francis X

Torben G. Andersen and Tim Bollerslev and Francis X. Diebold , title =. The Review of Economics and Statistics , year =

-

[35]

and Bollerslev, Tim and Diebold, Francis X

Andersen, Torben G. and Bollerslev, Tim and Diebold, Francis X. and Ebens, Heiko , title =. Journal of Financial Economics , year =

-

[36]

Andersen and Tim Bollerslev and Francis X

Torben G. Andersen and Tim Bollerslev and Francis X. Diebold and Paul Labys , title =. Econometrica , year =

-

[37]

G and Bollerslev, T

Andersen, T. G and Bollerslev, T. and Diebold, F. X and Labys, P. , title =. Journal of the American Statistical Association , year =

-

[38]

Andersen and Tim Bollerslev and Francis X

Torben G. Andersen and Tim Bollerslev and Francis X. Diebold and Paul Labys , title =. Risk , year =

-

[39]

Andersen and Tim Bollerslev and Francis X

Torben G. Andersen and Tim Bollerslev and Francis X. Diebold and Clara Vega , title =. American Economic Review , year =

-

[40]

Andersen and Tim Bollerslev and Francis X

Torben G. Andersen and Tim Bollerslev and Francis X. Diebold and Jin Wu , title =. Advances in Econometrics: Econometric Analysis of Economic and Financial Time Series in Honor of R.F. Engle, and C.W.J. Granger , year =

-

[41]

Andersen and Tim Bollerslev and Francis X

Torben G. Andersen and Tim Bollerslev and Francis X. Diebold and Jin Wu , title =. American Economic Review , year =

-

[42]

Andersen and Tim Bollerslev and Xin Huang , title =

Torben G. Andersen and Tim Bollerslev and Xin Huang , title =. Jounal of Econometrics , year =

-

[43]

Andersen and Tim Bollerslev and Nour Meddahi , title =

Torben G. Andersen and Tim Bollerslev and Nour Meddahi , title =. Journal of Econometrics , year =

-

[44]

Andersen and Tim Bollerslev and Nour Meddahi , title =

Torben G. Andersen and Tim Bollerslev and Nour Meddahi , title =. Econometrica , year =

-

[45]

T. W. Anderson and H. Rubin , title =. Annals of Mathematical Statistics , year =

-

[46]

T. W. Anderson , title =. Journal of Econometrics , year =

-

[47]

T. W. Anderson , title =. Annals of Statistics , year =

-

[48]

1984 , author =

An Introduction to Multivariate Statistical Analysis , publisher =. 1984 , author =

1984

-

[49]

Anderson, T. W. , title =. Annals of Mathematical Statistics , year =

-

[50]

Anderson , title =

Theodore W. Anderson , title =

-

[51]

T. W. Anderson and A. Takemura , title =. Journal of Time Series Analysis , year =

-

[52]

Donald W. K. Andrews , title =. Econometrica , year =

-

[53]

Donald W. K. Andrews , title =. Journal of Econometrics , year =

-

[54]

Donald W. K. Andrews , title =. Econometrica , volume =

-

[55]

Donald W. K. Andrews and Moshe Buchinsky , title =. Econometrica , year =

-

[56]

Donald W. K. Andrews and J. C. Monahan , title =. Econometrica , volume =

-

[57]

Andrews, D. W. K. and Ploberger, W. , title =. Econometrica , volume =

-

[58]

Journal of Financial Economics , year =

Ang, Andrew and Kristensen, Dennis , title =. Journal of Financial Economics , year =

-

[59]

Ang and J

A. Ang and J. Liu and K. Schwarz , title =. 2016 , owner =

2016

-

[60]

Ang and J

A. Ang and J. Liu and K. Schwarz , title =. 2010 , type =

2010

-

[61]

Angel, J. J. , title =. Journal of Finance , year =

-

[62]

, title =

Arellano, M. , title =. Oxford Bulletin of Economics and Statistics , year =

-

[63]

Arnheim-Dahlstr\"

L. Arnheim-Dahlstr\". Autoimmune, neurological, and venous thromboembolic adverse events after immunisation of adolescent girls with quadrivalent human papillomavirus vaccine in. BMJ , year =

-

[64]

Boragan and Diebold, Francis X

Aruoba, S. Boragan and Diebold, Francis X. and Scotti, Chiara , title =. Journal of Business and Economic Statistics , year =

-

[65]

Journal of Time Series Econometrics , year =

Manabu Asai and Mike So , title =. Journal of Time Series Econometrics , year =

-

[66]

Journal of Business and Economic Statistics , year =

Richard Ashley and David Vaughan , title =. Journal of Business and Economic Statistics , year =

-

[67]

Asness and A

C. Asness and A. Frazzini and L. Pedersen , title =. 2014 , type =

2014

-

[68]

Asness and A

C. Asness and A. Frazzini and L. Pedersen , title =. 2014 , owner =

2014

-

[69]

Ohanian , title =

Andrew Atkeson and Lee E. Ohanian , title =. Federal Reserve Bank of Minneapolis Quarterly Review , year =

-

[70]

G. J. Babu and K. Singh , title =. Annals of Statistics , year =

-

[71]

R. R. Bahadur and L. J. Savage , title =. Annals of mathematical statistics , year =

-

[72]

Journal of Econometrics , year =

Jushan Bai , title =. Journal of Econometrics , year =

-

[73]

Econometric Theory , year =

Jushan Bai , title =. Econometric Theory , year =

-

[74]

Lumsdaine and James Stock , title =

Jushan Bai and Robin L. Lumsdaine and James Stock , title =. Review of Economic Studies , year =

-

[75]

2007 , note =

Jushan Bai and Serena Ng , title =. 2007 , note =

2007

-

[76]

Econometrica , year =

Jushan Bai and Serena Ng , title =. Econometrica , year =

-

[77]

Econometrica , year =

Jushan Bai and Pierre Perron , title =. Econometrica , year =

-

[78]

Bali and Robert F

Turan G. Bali and Robert F. Engle and Yi Tang , title =. Management Science , year =

-

[79]

and Dumitrescu, E

Balter, J. and Dumitrescu, E. and Hansen, P.R. , title =. 2015 , type =

2015

-

[80]

Bandi and Jeffrey R

Federico M. Bandi and Jeffrey R. Russell , title =. 2005 , type =

2005

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.