Recognition: unknown

ESG as Priced Crash Insurance: State-Dependent Tail Risk and Deconfounding Evidence

Pith reviewed 2026-05-08 16:36 UTC · model grok-4.3

The pith

High ESG ratings cut equity crash incidence during systemic drawdowns by shrinking tail losses, acting as priced insurance that costs returns in stable times.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

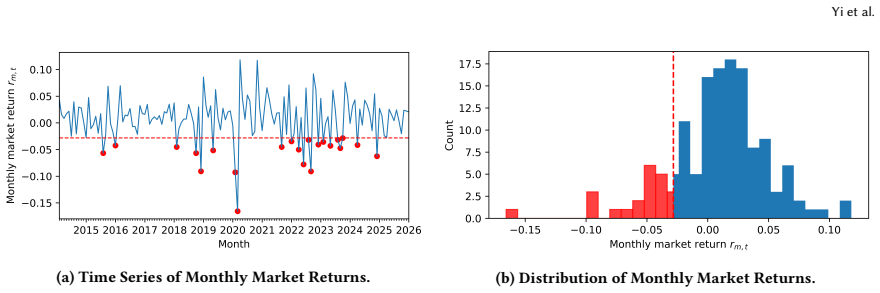

ESG ratings materially reduce the incidence of discrete crash events during systemic drawdowns by attenuating the severity of realized tail losses at the most adverse quantiles. This protection operates as priced insurance that incurs performance drags during stable periods while delivering critical resilience when tail risks materialize. Double machine learning isolates the asymmetric treatment effects by handling complex nuisance parameters and removing high-dimensional confounding between ESG and other firm traits.

What carries the argument

A drawdown-based truncation rule that partitions data into distinct stress and stable economic states, paired with double machine learning that estimates state-dependent treatment effects after removing confounding nuisance parameters.

If this is right

- High-ESG portfolios exhibit lower crash frequency and milder tail losses specifically inside drawdown regimes.

- The insurance cost appears as lower average returns during stable, non-stress periods.

- Standard linear models miss the effect because they do not separate states or remove high-dimensional confounding.

- The benefit concentrates at extreme left-tail quantiles rather than shifting the entire return distribution.

Where Pith is reading between the lines

- Regime-dependent ESG tilts could serve as a dynamic hedging tool for equity portfolios without separate tail-risk instruments.

- The same deconfounding and state-partitioning approach could be applied to other firm attributes to test for analogous state-dependent protections.

- If the pattern holds in credit or fixed-income data, ESG ratings would influence how markets price systemic tail risk across asset classes.

Load-bearing premise

The drawdown-based truncation rule successfully divides market data into distinct stress and stable states without introducing selection bias, and double machine learning fully removes all confounding between ESG ratings and other firm characteristics.

What would settle it

Finding that high-ESG firms experience the same frequency and severity of crashes as low-ESG firms during a subsequent systemic drawdown, even after applying the same double machine learning deconfounding procedure, would falsify the central claim.

Figures

read the original abstract

This research establishes ESG as a state dependent insurance mechanism against equity crashes by addressing the decoupling of unconditional alpha from tail risk resilience. By validating market stress regimes as distinct economic states through a drawdown-based truncation rule, the study demonstrates that high ESG ratings materially reduce the incidence of discrete crash events during systemic drawdowns. To address the selection bias and high-dimensional confounding inherent in traditional linear frameworks, we implement Double Machine Learning as a structural deconfounding layer. Unlike simple predictive modeling, the Double Machine Learning framework utilizes machine learning to handle complex nuisance parameters, allowing us to isolate the asymmetric treatment effects of ESG across different market states. Distributional analysis reveals the underlying mechanism as ESG specifically attenuates the severity of realized tail losses at the most adverse quantiles instead of shifting the entire return distribution. Confirmed by structural estimates, this protection functions as priced insurance that incurs performance drags during stable periods while providing critical resilience when tail risks are most acute.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that ESG ratings function as state-dependent priced insurance against equity crashes: high-ESG firms exhibit materially lower crash incidence during systemic drawdowns identified by a drawdown-based truncation rule, with effects isolated via Double Machine Learning to remove high-dimensional confounding and shown by distributional analysis to concentrate at adverse return quantiles rather than shifting the full distribution, incurring performance costs in stable periods.

Significance. If the identification holds, the results would help reconcile the absence of unconditional ESG alpha with tail-risk resilience, offering a mechanism for state-dependent pricing of ESG characteristics in asset markets. The use of DML for deconfounding and quantile-focused distributional analysis are methodological strengths that could advance empirical work on asymmetric risk exposures.

major comments (3)

- [State identification via drawdown truncation] Drawdown truncation rule (abstract and state-identification section): the central claim that this rule cleanly partitions data into exogenous systemic-stress versus normal regimes without selection on ESG or crash outcomes is load-bearing, yet aggregate market returns embed the firm-level tail events under study, risking mechanical correlation between state assignment and the outcome; explicit tests for exogeneity (e.g., placebo partitions or firm-exclusion robustness) are required.

- [Double Machine Learning framework] Double Machine Learning implementation (abstract and DML section): the assertion that DML fully removes high-dimensional confounding between ESG and other firm characteristics is central to the deconfounding evidence, but the manuscript supplies no details on nuisance-function estimators, cross-fitting procedure, or sensitivity to hyperparameter choices; without these, it is impossible to verify whether the reported asymmetric tail effects survive alternative nuisance specifications.

- [Distributional analysis] Distributional analysis (abstract and results on tail quantiles): the finding that ESG attenuates severity only at the most adverse quantiles (rather than shifting the entire distribution) underpins the insurance interpretation, yet the paper must specify the exact quantile estimation method, its integration with the state-dependent truncation, and whether standard errors account for the two-stage DML procedure.

minor comments (1)

- [Abstract] The abstract's phrasing of 'decoupling of unconditional alpha from tail risk resilience' could be clarified with a brief definition of the unconditional benchmark used.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed feedback on our manuscript. The comments highlight important areas for clarification and robustness, and we address each major point below. We plan to incorporate revisions that strengthen the identification, methodological transparency, and replicability of the results.

read point-by-point responses

-

Referee: [State identification via drawdown truncation] Drawdown truncation rule (abstract and state-identification section): the central claim that this rule cleanly partitions data into exogenous systemic-stress versus normal regimes without selection on ESG or crash outcomes is load-bearing, yet aggregate market returns embed the firm-level tail events under study, risking mechanical correlation between state assignment and the outcome; explicit tests for exogeneity (e.g., placebo partitions or firm-exclusion robustness) are required.

Authors: We agree that the overlap between aggregate market returns and firm-level outcomes introduces a potential mechanical correlation, and that explicit exogeneity tests are warranted. In the revision we will add a dedicated robustness appendix containing: (i) placebo partitions that randomly assign stress dates while preserving the drawdown magnitude distribution, (ii) firm-exclusion checks that recompute the aggregate drawdown after dropping the largest 10 percent of firms by market capitalization, and (iii) an alternative state definition based on VIX thresholds above the 90th percentile. These tests will be reported alongside the baseline results to demonstrate that the state-dependent ESG tail attenuation is not an artifact of the truncation rule. revision: yes

-

Referee: [Double Machine Learning framework] Double Machine Learning implementation (abstract and DML section): the assertion that DML fully removes high-dimensional confounding between ESG and other firm characteristics is central to the deconfounding evidence, but the manuscript supplies no details on nuisance-function estimators, cross-fitting procedure, or sensitivity to hyperparameter choices; without these, it is impossible to verify whether the reported asymmetric tail effects survive alternative nuisance specifications.

Authors: We acknowledge that the current manuscript lacks sufficient implementation detail for the DML procedure. The revised version will expand the DML section and add an appendix that specifies: the nuisance estimators (random forests for continuous covariates and logistic regression for binary indicators), the cross-fitting scheme (5-fold sample splitting with out-of-fold predictions), and a full set of sensitivity checks that vary key hyperparameters (maximum tree depth, minimum node size, and regularization strength). We will also report the resulting ESG tail coefficients under these alternatives to confirm that the asymmetric attenuation at adverse quantiles remains stable. revision: yes

-

Referee: [Distributional analysis] Distributional analysis (abstract and results on tail quantiles): the finding that ESG attenuates severity only at the most adverse quantiles (rather than shifting the entire distribution) underpins the insurance interpretation, yet the paper must specify the exact quantile estimation method, its integration with the state-dependent truncation, and whether standard errors account for the two-stage DML procedure.

Authors: We will clarify the distributional analysis in the revised manuscript. The quantile results are obtained via a two-stage procedure that first applies the DML deconfounding step within each regime (stress versus normal) and then estimates conditional quantiles using the deconfounded residuals. We will explicitly state that we employ Koenker’s linear quantile regression at the 5 percent, 10 percent, and 25 percent levels, integrated with the drawdown truncation, and that standard errors are obtained via a bootstrap that resamples both the first-stage nuisance functions and the second-stage quantile regressions to account for the two-stage estimation. These details, together with the bootstrap code outline, will be added to the results section and a methodological appendix. revision: yes

Circularity Check

No circularity: derivation uses external data partitions and standard DML estimators without reduction to inputs by construction

full rationale

The paper partitions market regimes via a drawdown-based truncation rule applied to aggregate returns and then applies Double Machine Learning to isolate ESG treatment effects on tail quantiles. No quoted equations or claims equate the estimated asymmetric resilience to a fitted parameter or self-defined outcome; the state indicator is constructed from market-wide returns independent of the firm-level ESG-crash regression, and DML nuisance functions are estimated separately from the target parameters. The abstract and described framework rely on observable return series and off-the-shelf ML deconfounding rather than tautological renaming, self-citation load-bearing, or ansatz smuggling. This leaves the central claim falsifiable against external benchmarks and yields no load-bearing circular steps.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Double Machine Learning nuisance-parameter estimators are consistent under standard regularity conditions

- domain assumption Drawdown-based truncation partitions returns into distinct economic regimes without residual selection bias

Reference graph

Works this paper leans on

-

[1]

Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Du- flo, Christian Hansen, Whitney Newey, and James Robins. 2018. Dou- ble/debiased machine learning for treatment and structural parameters

2018

-

[2]

Colin Cameron and Douglas L

A. Colin Cameron and Douglas L. Miller. 2015. A Practitioner’s Guide to Cluster-Robust Inference.Journal of Human Resources50, 2 (2015), 317–372. arXiv:https://jhr.uwpress.org/content/50/2/317.full.pdf doi:10. 3368/jhr.50.2.317

2015

-

[3]

Elizabeth Demers, Jurian Hendrikse, Philip Joos, and Baruch Lev. 2021. ESG did not immunize stocks during the COVID-19 crisis, but invest- ments in intangible assets did.Journal of business finance & accounting 48, 3-4 (2021), 433–462

2021

-

[4]

2010.Strategic management: A stakeholder approach

R Edward Freeman. 2010.Strategic management: A stakeholder approach. Cambridge university press

2010

-

[5]

Shihao Gu, Bryan Kelly, and Dacheng Xiu. 2020. Empirical asset pricing via machine learning.The Review of Financial Studies33, 5 (2020), 2223–2273

2020

-

[6]

Amy P Hutton, Alan J Marcus, and Hassan Tehranian. 2009. Opaque financial reports, R2, and crash risk.Journal of financial Economics94, 1 (2009), 67–86

2009

-

[7]

Li Jin and Stewart C Myers. 2006. R2 around the world: New theory and new tests.Journal of financial Economics79, 2 (2006), 257–292

2006

-

[8]

Roger Koenker and Gilbert Bassett Jr. 1978. Regression quantiles.Econo- metrica: journal of the Econometric Society(1978), 33–50

1978

-

[9]

Hans R. Künsch. 1989. The Jackknife and the Bootstrap for General Stationary Observations.The Annals of Statistics17, 3 (1989), 1217–1241. doi:10.1214/aos/1176347265

-

[10]

Karl V Lins, Henri Servaes, and Ane Tamayo. 2017. Social capital, trust, and firm performance: The value of corporate social responsibility during the financial crisis.the Journal of Finance72, 4 (2017), 1785– 1824

2017

-

[11]

MSCI Solutions LLC. 2026. ESG Ratings: Assess companies on their financially relevant sustainability risks and opportunities. https://www. msci.com/data-and-analytics/sustainability-solutions/esg-ratings

2026

-

[12]

Standard & Poor’s Financial Services LLC. 2026. Compustat North America. https://wrds-web.wharton.upenn.edu/wrds/

2026

- [13]

-

[14]

Sichen Zhao, Zhiming Xue, Yalun Qi, Xianling Zeng, and Zihan Yu

- [15]

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.