Recognition: unknown

Dynamic Collateral Control for Permissionless Spot Perpetual Basis Trading

Pith reviewed 2026-05-09 16:10 UTC · model grok-4.3

The pith

Risk-constrained collateral allocation offers a more robust benchmark than economic optimization for spot-perpetual basis trades as volatility increases.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

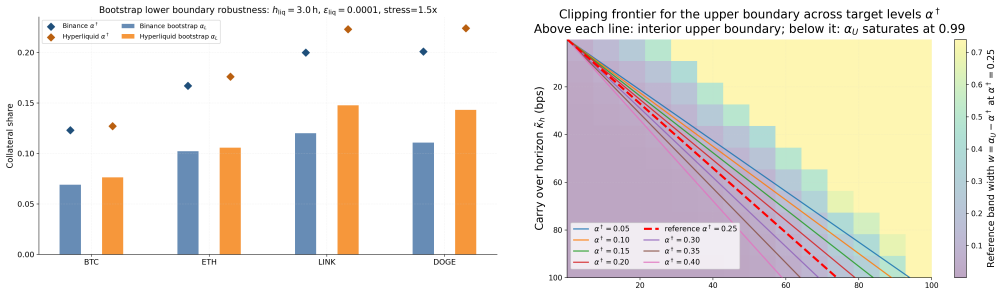

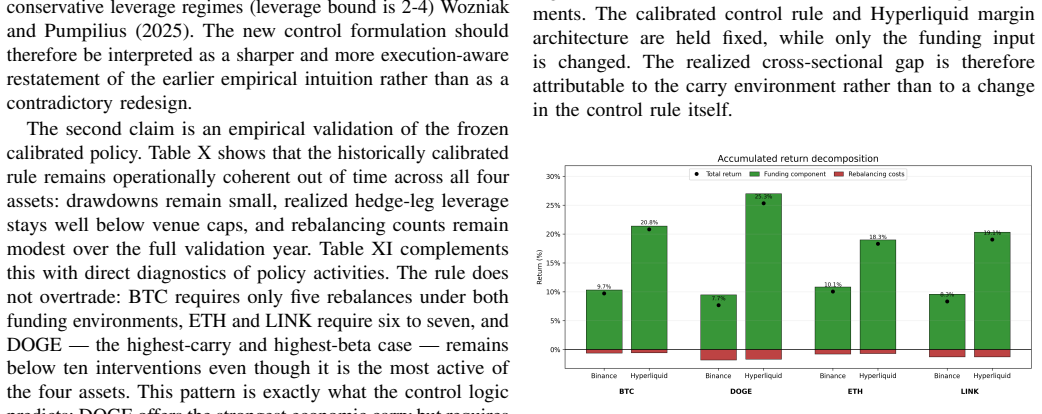

The risk-constrained formulation of the collateral share provides a more robust operating benchmark relative to the economic optimum, with the required collateral rising monotonically under volatility stress, while the asymmetric dynamic extension keeps the solvency-driven lower boundary structurally relevant and the upper boundary active only in high-carry low-cost regimes, and live validation shows funding environment as the dominant driver of performance.

What carries the argument

The collateral share allocated between spot inventory and derivative margin, controlled statically by risk constraints and dynamically by asymmetric solvency and carry-rebalancing boundaries.

If this is right

- Required collateral increases monotonically with volatility stress across assets.

- Collateral needs stay lowest for BTC and rise substantially for long-tail assets such as LINK and DOGE.

- The solvency-driven lower intervention boundary remains relevant across Monte Carlo regimes.

- Upper intervention triggers driven by carry-rebalancing trade-offs activate mainly under high carry and low costs.

- Realized performance under a fixed control rule is predominantly explained by the funding environment, with larger execution wedges when selling the basis.

Where Pith is reading between the lines

- Similar risk-constrained allocation could be applied to other DeFi margin strategies to test whether volatility sensitivity varies by asset class.

- Live monitoring of funding rates could be prioritized over other signals when setting dynamic rebalancing thresholds.

- Platform-level execution improvements that reduce selling wedges might expand the set of regimes where upper triggers become active.

Load-bearing premise

Monte Carlo simulations and historical backtests accurately reflect the liquidity frictions, execution costs, and market conditions of live on-chain spot-perpetual trading.

What would settle it

A side-by-side live implementation on a permissionless venue during a volatility spike that compares liquidation frequency and risk-adjusted returns between the risk-constrained collateral share and the economic optimum share.

Figures

read the original abstract

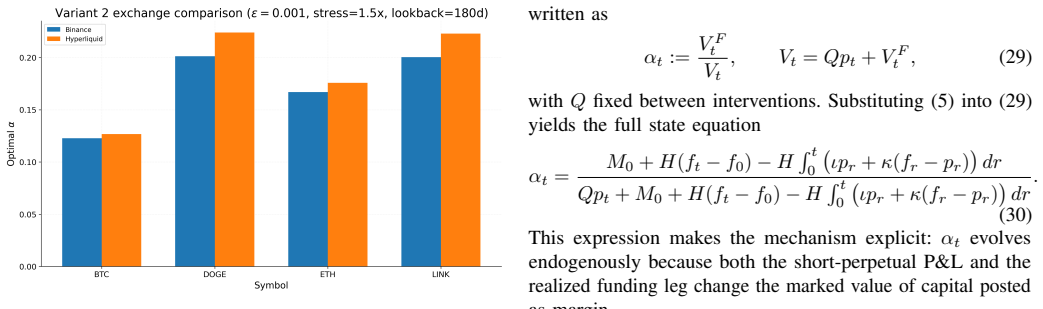

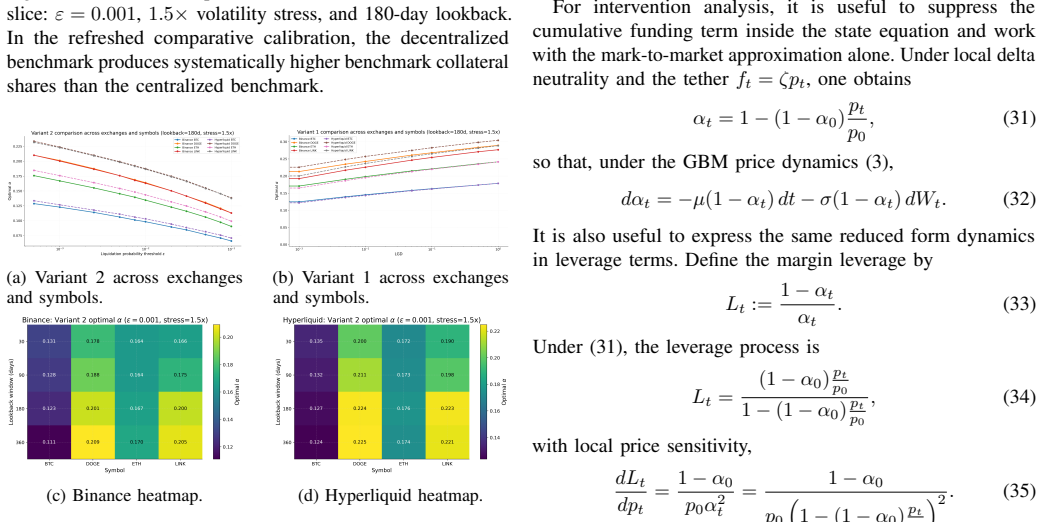

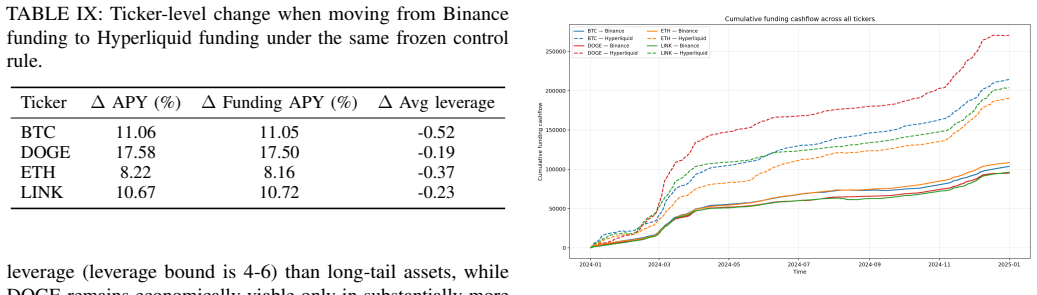

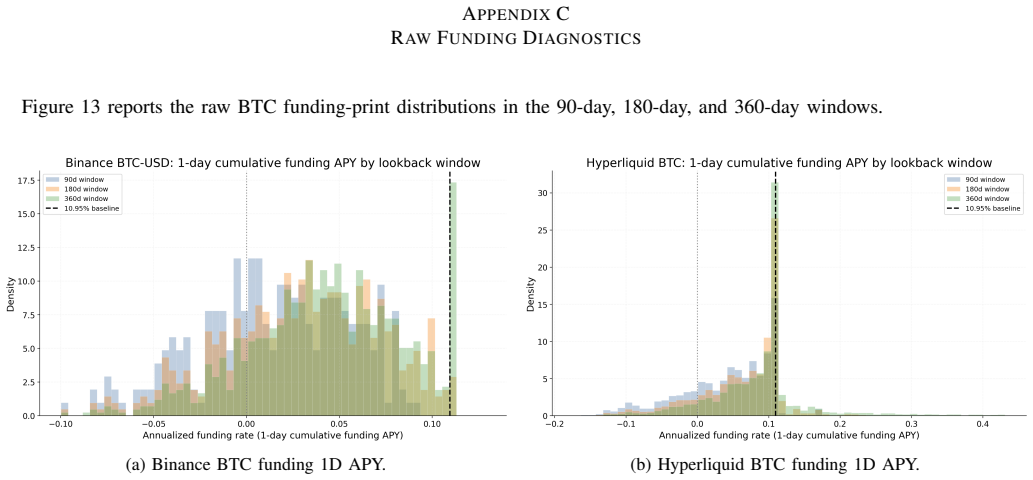

We study permissionless spot--perpetual basis trading in decentralized finance as a collateral control problem. The strategy holds spot inventory, hedges directional exposure with a short perpetual, and allocates capital between spot inventory and derivative margin under on-chain liquidity and execution frictions. The paper delivers three results. First, it solves a static control problem for the collateral share and shows that the risk-constrained formulation provides a more robust operating benchmark relative to the economic optimum. In comparative calibration, the required collateral rises monotonically under volatility stress. The collateral is the lowest for BTC and increases significantly for long tail assets such as LINK and DOGE. Second, the paper derives an asymmetric dynamic extension in which the lower boundary of intervention is solvency driven, and the upper boundary is determined by a trade-off between carry-loss and the cost of rebalancing. Monte Carlo simulation shows that the lower boundary remains structurally relevant, whereas meaningful interior upper triggers survive mainly in the regimes with high carry and low costs. Third, the paper validates an execution-aware implementation with live routed execution and historical backtests. The execution layer shows that the realized wedges are significant, but become worse in the case of selling the basis. This justifies a minimum effective rebalancing size and a positive execution buffer. The historical validation shows that in the case of a fixed control rule the realized performance is predominantly explained by the funding environment.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper models permissionless spot-perpetual basis trading in DeFi as a collateral control problem. It solves a static optimization showing that a risk-constrained collateral allocation is more robust than the pure economic optimum, with collateral requirements rising monotonically under volatility stress (lowest for BTC, significantly higher for LINK and DOGE). It derives an asymmetric dynamic policy with a solvency-driven lower boundary and a carry-versus-rebalancing-cost upper boundary. Monte Carlo simulations indicate the lower boundary remains relevant across regimes while upper triggers appear mainly in high-carry, low-cost settings. The approach is validated via execution-aware live routing and historical backtests, which show significant realized wedges (worse when selling the basis), justify minimum rebalancing sizes and buffers, and attribute most performance variation to the funding environment.

Significance. If the results hold, this supplies a practical, robustness-focused framework for collateral management in decentralized basis trading that explicitly incorporates on-chain liquidity and execution frictions. The static benchmark, asymmetric dynamic rules, and execution-aware validation could directly inform live trading systems and risk controls in permissionless markets.

major comments (2)

- [Monte Carlo simulation] Monte Carlo simulation section: the claim that upper-boundary triggers survive 'mainly in the regimes with high carry and low costs' is central to the dynamic extension but lacks the specific carry rates, cost parameters, and volatility levels used. Without these values or a sensitivity table, it is difficult to assess whether the result is robust or parameter-specific.

- [Historical validation] Historical validation section: the statement that 'realized performance is predominantly explained by the funding environment' is load-bearing for the third result. A quantitative measure (e.g., R² from a regression of PnL on funding rates, or a variance-decomposition table) is needed to substantiate 'predominantly'.

minor comments (2)

- [Abstract] Abstract and introduction: several results are summarized without reference to the underlying equations or objective functions (e.g., the exact form of the risk constraint or the carry-loss term). Adding one or two key equations would improve traceability.

- [Execution-aware implementation] Execution layer description: the observation that 'realized wedges are significant, but become worse in the case of selling the basis' would benefit from a table of average wedge sizes by direction and asset.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback and the recommendation of minor revision. We address the major comments point by point below.

read point-by-point responses

-

Referee: [Monte Carlo simulation] Monte Carlo simulation section: the claim that upper-boundary triggers survive 'mainly in the regimes with high carry and low costs' is central to the dynamic extension but lacks the specific carry rates, cost parameters, and volatility levels used. Without these values or a sensitivity table, it is difficult to assess whether the result is robust or parameter-specific.

Authors: We appreciate the referee's observation. The Monte Carlo simulations were conducted using specific parameter sets for carry rates, rebalancing costs, and volatility levels, which we will now explicitly document in the revised manuscript. We will add a table listing the baseline parameters (e.g., carry rates ranging from 0.01% to 0.5% daily, cost parameters from 0.1% to 1%, volatility from 20% to 100% annualized) and include a sensitivity table demonstrating the frequency of upper-boundary triggers across these regimes. This will confirm that the result holds primarily in high-carry, low-cost settings while remaining robust. revision: yes

-

Referee: [Historical validation] Historical validation section: the statement that 'realized performance is predominantly explained by the funding environment' is load-bearing for the third result. A quantitative measure (e.g., R² from a regression of PnL on funding rates, or a variance-decomposition table) is needed to substantiate 'predominantly'.

Authors: We agree that providing a quantitative measure will strengthen the validation. In the revised version, we will include a regression of the realized PnL on the funding rates, reporting the R² value to quantify the explanatory power of the funding environment. We will also consider adding a variance decomposition if space permits, to show the proportion of performance variation attributable to funding versus other factors. revision: yes

Circularity Check

No significant circularity; derivation self-contained

full rationale

The paper formulates a static collateral control problem, solves it to compare risk-constrained vs. economic optimum benchmarks, derives an asymmetric dynamic extension with boundaries, and validates via Monte Carlo plus historical backtests. No quoted equations or steps reduce a claimed prediction or result to a fitted parameter by construction, nor rely on load-bearing self-citations for uniqueness or ansatz. Monotonicity under volatility stress and robustness claims follow from the solved control problem and simulation inputs rather than re-labeling fitted values. Execution-aware validation uses independent live and historical data. This is the common honest non-finding for model-based control papers.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Perpetual futures pricing.Mathematical Finance, 2025

Damien Ackerer, Julien Hugonnier, and Urban Jermann. Perpetual futures pricing.Mathematical Finance, 2025. doi: 10.1111/mafi.70018

-

[2]

Fundamentals of perpetual futures.arXiv preprint arXiv:2212.06888, 2022

Songrun He, Asaf Manela, Omri Ross, and Victor von Wachter. Fundamentals of perpetual futures. 2024. Working paper version available as arXiv:2212.06888

-

[3]

Uniswap v3 core

Hayden Adams, Noah Zinsmeister, Moody Salem, River Keefer, and Dan Robinson. Uniswap v3 core. White paper, 2021

2021

-

[4]

The dominance of uniswap v3 liquidity

Gordon Liao and Dan Robinson. The dominance of uniswap v3 liquidity. Research paper, 2022

2022

-

[5]

Erdong Chen, Mengzhong Ma, and Zixin Nie. Perpetual future contracts in centralized and decentralized exchanges: Mechanism and traders’ behavior.Electronic Markets, 2024. doi: 10.1007/s12525-024-00715-1

-

[6]

Liquidations

Hyperliquid. Liquidations. Documentation, 2025a. URL https://hyperliquid.gitbook.io/hyperliquid-docs/trading/ liquidations

-

[7]

Margining

Hyperliquid. Margining. Documentation, 2026a. URL https:// hyperliquid.gitbook.io/hyperliquid-docs/trading/margining

-

[8]

A next-generation smart contract and decentralized application platform

Vitalik Buterin. A next-generation smart contract and decentralized application platform. Ethereum White Paper, 2014

2014

-

[9]

Ethereum: A secure decentralised generalised transaction ledger

Gavin Wood. Ethereum: A secure decentralised generalised transaction ledger. Ethereum Yellow Paper, 2014

2014

-

[10]

Optimal execution of portfolio transactions.Journal of Risk, 3(2):5–39, 2001

Robert Almgren and Neil Chriss. Optimal execution of portfolio transactions.Journal of Risk, 3(2):5–39, 2001

2001

-

[11]

Nicolae Gârleanu and Lasse Heje Pedersen. Dynamic trading with predictable returns and transaction costs.Journal of Finance, 68(6):2309–2340, 2013. doi: 10.1111/jofi.12080

-

[12]

Anna A. Obizhaeva and Jiang Wang. Optimal trading strategy and supply/demand dynamics.Journal of Financial Markets, 16(1):1–32, 2013. doi: 10.1016/j.finmar.2012.09. 001

-

[13]

Jay Kahn

Daniel Barth and R. Jay Kahn. Hedge funds and the treasury cash–futures disconnect.Office of Financial Research Working Paper, (21-01), 2021

2021

-

[14]

Mathias S. Kruttli, Phillip J. Monin, Lubomir Petrasek, and Sumudu W. Watugala. Hedge fund treasury trading and funding fragility: Evidence from the covid-19 crisis.Finance and Economics Discussion Series, (2021-038), 2021. doi: 10.17016/FEDS.2021.038

-

[15]

Trading and arbitrage in cryptocurrency markets.Journal of Financial Economics, 135(2):293–319, 2020

Igor Makarov and Antoinette Schoar. Trading and arbitrage in cryptocurrency markets.Journal of Financial Economics, 135(2):293–319, 2020. doi: 10.1016/j.jfineco.2019.07.001

-

[16]

Andrea Barbon and Angelo Ranaldo. On the quality of cryptocurrency markets: Centralized versus decentralized exchanges.Management Science, 2026. doi: 10.1287/mnsc. 2024.07703

-

[17]

Execu- tion welfare across solver-based dexes.arXiv preprint arXiv:2503.00738, 2025

Yuki Yuminaga, Dex Chen, and Danning Sui. Execu- tion welfare across solver-based dexes.arXiv preprint arXiv:2503.00738, 2025. doi: 10.48550/arXiv.2503.00738

-

[18]

Borodin and Paavo Salminen.Handbook of Brownian Motion: Facts and Formulae

Andrei N. Borodin and Paavo Salminen.Handbook of Brownian Motion: Facts and Formulae. Birkh"auser, 2 edition, 2015

2015

-

[19]

Contract specifications

Hyperliquid. Contract specifications. Documentation, 2025b. URL https://hyperliquid.gitbook.io/hyperliquid-docs/trading/ contract-specifications

-

[20]

Introduction to binance futures funding rates

Binance. Introduction to binance futures funding rates. Support documentation, 2019. URL https://www.binance. com/en/support/faq/detail/360033525031

-

[21]

The two-tiered structure of cryptocur- rency funding rate markets.Mathematics, 14(2):346, 2026

Petar Zhivkov. The two-tiered structure of cryptocur- rency funding rate markets.Mathematics, 14(2):346, 2026. doi: 10.3390/math14020346. URL https://www.mdpi.com/ 2227-7390/14/2/346

-

[22]

Hyperliquid. Bridge. Developer documentation, 2025c. URL https://hyperliquid.gitbook.io/hyperliquid-docs/ hypercore/bridge

-

[23]

Bridge2 api

Hyperliquid. Bridge2 api. Developer documentation, 2025d. URL https://hyperliquid.gitbook.io/hyperliquid-docs/ for-developers/api/bridge2

-

[24]

Arbitrum one outage report

Offchain Labs. Arbitrum one outage report. Official incident report, 2021. URL https://medium.com/offchainlabs/ arbitrum-one-outage-report-d365b24d49c

2021

-

[25]

Sequencer and feed issues (arbitrum one)

Arbitrum Status. Sequencer and feed issues (arbitrum one). Official status page incident report, 2023. URL https://status. arbitrum.io/clq6te1l142387b8n5bmllk9es

2023

-

[26]

Fractal: A python research library for DeFi strategies, 2026

Anatoly Krestenko and the Fractal contributors. Fractal: A python research library for DeFi strategies, 2026. URL https://doi.org/10.5281/zenodo.20049904

-

[27]

Basisos: A managed basis trading strategy for yield optimization in exotic mar- kets

Boring Wozniak and Numa Pumpilius. Basisos: A managed basis trading strategy for yield optimization in exotic mar- kets. https://github.com/Logarithm-Labs/basisos-whitepaper/ blob/main/basisos_whitepaper.pdf, February 2025. BasisOS whitepaper, accessed 2026-03-31

2025

-

[28]

Eip-4626: Tokenized vaults

Ethereum Improvement Proposals. Eip-4626: Tokenized vaults. Ethereum Improvement Proposal, 2021. URL https: //eips.ethereum.org/EIPS/eip-4626

2021

-

[29]

1inch classic swap api documentation

1inch. 1inch classic swap api documentation. Devel- oper documentation, 2026a. URL https://portal.1inch.dev/ documentation/apis/swap/classic-swap/introduction

-

[30]

1inch orderbook api documentation

1inch. 1inch orderbook api documentation. Devel- oper documentation, 2026b. URL https://portal.1inch.dev/ documentation/apis/orderbook/introduction

-

[31]

Order book

Hyperliquid. Order book. Developer documentation, 2025e. URL https://hyperliquid.gitbook.io/hyperliquid-docs/ hypercore/order-book

-

[32]

Info endpoint

Hyperliquid. Info endpoint. Developer documentation, 2026b. URL https://hyperliquid.gitbook.io/hyperliquid-docs/ for-developers/api/info-endpoint

-

[33]

Albert S. Kyle. Continuous auctions and insider trading. Econometrica, 53(6):1315–1335, 1985

1985

-

[34]

Oxford University Press, 2007

Joel Hasbrouck.Empirical Market Microstructure. Oxford University Press, 2007

2007

-

[35]

Bernt Øksendal and Agnès Sulem.Applied Stochastic Control of Jump Diffusions. Universitext. Springer, 2007. doi: 10.1007/978-3-540-69826-1

-

[36]

Optimal basis github reposi- tory

Anatoly Krestenko. Optimal basis github reposi- tory. https://github.com/0xBoringWozniak/optimal-basis- trade-control, 2026. APPENDIXA EXTENDEDSTATICTABLES Tables XV–XVIII report the extended static simulation grid by asset. TABLE XV: BTC: static grid. Panel A reports the economic formulation with LGD= 0.1 ; Panel B reports the risk-constrained formulatio...

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.