Recognition: unknown

What Can Go Wrong During Caplet Stripping ?

Pith reviewed 2026-05-08 15:03 UTC · model grok-4.3

The pith

Interpolation choices and node placement are the main causes of oscillations and negative values when stripping caplets from market quotes.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Instability during exact caplet stripping arises primarily from the interpolation scheme and node placement, which can be worsened by isolated poor quotes. Continuous flat-linear and C1 flat-smooth kernels that preserve bootstrap equivalence, combined with midpoint node placement and a global solver, plus positivity enforcement via exponential reparametrization or Hyman non-negative C1 splines, deliver substantially reduced oscillations, robust positive caplet curves, and negligible repricing error.

What carries the argument

Continuous flat-linear and C1 flat-smooth interpolation kernels with midpoint node placement and global solver, plus exponential reparametrization or Hyman splines for positivity.

If this is right

- The workflow produces production-ready positive caplet curves without manual smoothing or quote filtering.

- Repricing error on the input caps remains negligible, preserving exact market consistency.

- Data quality checks become simpler because the method tolerates isolated bad quotes better.

- The same kernels and placement can be reused across different tenors without retuning.

Where Pith is reading between the lines

- Similar kernel and node choices might reduce instability in other single-curve bootstraps such as swaption volatilities.

- In live risk systems the positivity enforcement could be run continuously to flag when input data quality drops.

- The approach opens the door to fully automated daily caplet surface construction with minimal human oversight.

Load-bearing premise

Market cap quotes are sufficiently clean and the proposed kernels preserve exact bootstrap equivalence without adding material bias under typical conditions.

What would settle it

Applying the flat-linear kernel, midpoint placement, and exponential reparametrization to a standard set of market cap quotes and still obtaining negative or highly oscillatory caplet volatilities would falsify the stability claim.

Figures

read the original abstract

We study exact and near exact extraction of caplet volatilities from market cap quotes and identify why some common choices produce extreme oscillations or negative vols. Interpolation scheme and node placement are shown to be the primary drivers of instability, which can be amplified by isolated bad quotes. We propose practical, production ready remedies: continuous flat-linear and C1 flat-smooth kernels that preserve bootstrap equivalence, midpoint node placement with a global solver, positivity enforcement via an exponential reparametrization or Hyman non-negative C1 splines. We also introduce simple data quality checks. Numerical experiments demonstrate substantially reduced oscillations, robust positive caplet curves, and negligible repricing error, delivering a fast and stable caplet stripping workflow suitable for real-world use.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript studies exact and near-exact extraction of caplet volatilities from market cap quotes. It identifies interpolation scheme and node placement as the primary drivers of instability (oscillations or negative vols), which can be amplified by isolated bad quotes. Practical remedies are proposed: continuous flat-linear and C1 flat-smooth kernels that preserve bootstrap equivalence, midpoint node placement with a global solver, positivity enforcement via exponential reparametrization or Hyman non-negative C1 splines, and simple data quality checks. Numerical experiments are reported to demonstrate substantially reduced oscillations, robust positive caplet curves, and negligible repricing error.

Significance. If the numerical evidence holds, the work supplies directly usable, production-ready guidance for a common task in interest-rate volatility modeling. The emphasis on preserving bootstrap equivalence while enforcing positivity and stability addresses a practical pain point; the combination of targeted kernel choices, node placement, and reparametrization offers a concrete workflow that can be implemented without altering the economic meaning of the stripped curve.

major comments (2)

- [kernel section] Section describing the kernels (around the flat-linear and C1 flat-smooth proposals): the claim that these kernels 'preserve bootstrap equivalence' is central to the practical value of the remedies. The manuscript should supply either an explicit algebraic verification that the interpolated forward vols reproduce the input cap prices exactly, or a side-by-side numerical check (e.g., repricing error before and after the change) on the same market data set used for the oscillation experiments.

- [numerical experiments] Numerical experiments section: while reduced oscillations and positive curves are reported, the manuscript does not state the precise quantitative metrics employed (maximum oscillation amplitude, integrated negativity measure, or L2 deviation from a reference curve) nor the number and diversity of market regimes tested. Without these, it is difficult to judge whether the improvement is robust or specific to the chosen data snapshots.

minor comments (2)

- [figures] Figure captions should explicitly list the market data date, the tenor structure, and the solver tolerance used for the global optimization so that readers can reproduce the oscillation plots.

- [data quality] The data-quality checks are introduced as 'simple'; a short pseudocode or explicit threshold values (e.g., quote deviation in basis points) would make them immediately usable by practitioners.

Simulated Author's Rebuttal

We thank the referee for the positive evaluation and the helpful suggestions that will improve the clarity and rigor of the manuscript. We address each major comment below and will incorporate the requested additions in the revision.

read point-by-point responses

-

Referee: [kernel section] Section describing the kernels (around the flat-linear and C1 flat-smooth proposals): the claim that these kernels 'preserve bootstrap equivalence' is central to the practical value of the remedies. The manuscript should supply either an explicit algebraic verification that the interpolated forward vols reproduce the input cap prices exactly, or a side-by-side numerical check (e.g., repricing error before and after the change) on the same market data set used for the oscillation experiments.

Authors: We agree that an explicit demonstration of bootstrap equivalence is essential for the practical utility of the proposed kernels. In the revised manuscript we will add a short algebraic verification in the kernel section proving that the continuous flat-linear and C1 flat-smooth kernels, when used within the standard bootstrap, exactly recover the input cap prices at the node dates. We will also include a side-by-side numerical table of repricing errors (before versus after the kernel change) computed on the identical market data snapshots employed in the oscillation experiments, confirming that the errors remain negligible. revision: yes

-

Referee: [numerical experiments] Numerical experiments section: while reduced oscillations and positive curves are reported, the manuscript does not state the precise quantitative metrics employed (maximum oscillation amplitude, integrated negativity measure, or L2 deviation from a reference curve) nor the number and diversity of market regimes tested. Without these, it is difficult to judge whether the improvement is robust or specific to the chosen data snapshots.

Authors: We accept that greater specificity on metrics and test coverage will strengthen the numerical section. The revised version will explicitly define the quantitative measures used (maximum oscillation amplitude, integrated negativity, and L2 deviation from a reference curve) and will report the exact number and diversity of market regimes examined. This will make the robustness of the improvements transparent to readers. revision: yes

Circularity Check

No significant circularity in derivation or claims

full rationale

The paper presents an empirical study of caplet volatility extraction procedures, diagnosing instability sources through numerical experiments on interpolation schemes, node placement, and data quality, then proposing practical adjustments such as flat-linear kernels, midpoint nodes, global solvers, and positivity reparametrizations. No load-bearing mathematical derivation, prediction, or first-principles result is shown to reduce by construction to its own inputs or to a self-citation chain; the central claims rest on observable numerical behavior and bootstrap equivalence preservation rather than self-referential fitting or renamed ansatzes. The work is self-contained against external market data benchmarks with no internal reduction of outputs to fitted parameters.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Market cap quotes represent exact prices of the corresponding cap instruments under the chosen pricing model

Reference graph

Works this paper leans on

-

[1]

What Can Go Wrong During Caplet Stripping ?

Introduction Interest rate caps and floors are widely used financial instruments that provide protection against interestratefluctuations. AcapisaseriesofEuropeancalloptionsoninterestrates,whileafloorisaseries ofEuropeanputoptions. Capletstrippingistheprocessofextractingtheimpliedvolatilitiesofindividual capletsfromthemarketpricesofcapsandfloors. Thisproc...

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[2]

Bootstrapping Wehave𝑁capvolquotes( ̂𝜎1,…,̂𝜎𝑁)atmaturities𝑇1 <⋯<𝑇𝑁,eachdefiningatargetcapprice 𝑃mkt 𝑞 = 𝑀𝑞∑ 𝑖=1 Caplet𝑖(̂𝜎𝑞), 𝑀 𝑞=𝑇𝑞∕∆, where∆is the caplet frequency (e.g

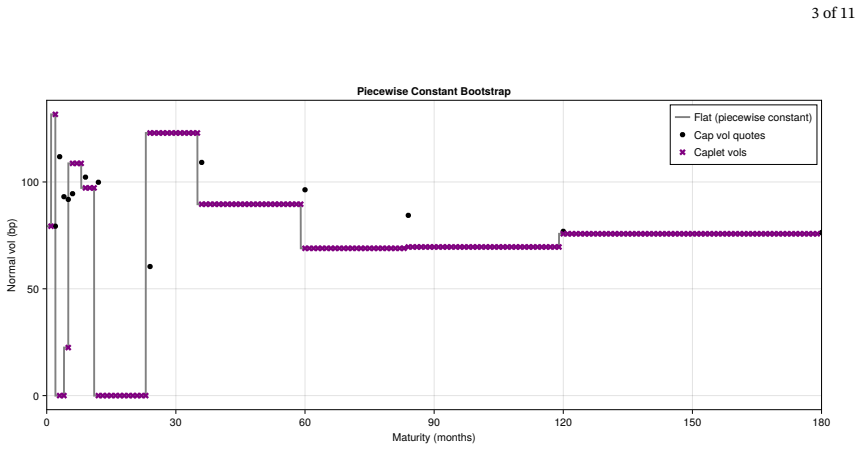

StrippingMethodology 2.1. Bootstrapping Wehave𝑁capvolquotes( ̂𝜎1,…,̂𝜎𝑁)atmaturities𝑇1 <⋯<𝑇𝑁,eachdefiningatargetcapprice 𝑃mkt 𝑞 = 𝑀𝑞∑ 𝑖=1 Caplet𝑖(̂𝜎𝑞), 𝑀 𝑞=𝑇𝑞∕∆, where∆is the caplet frequency (e.g. 1 month). We parameterise the caplet vol curve by𝑁node values (𝑣1,…,𝑣𝑁)atnodetimes (𝜏1,…,𝜏𝑁),withaninterpolation 𝜎(𝑡)=𝐼(𝑡;𝜏,𝑣). Thestrippingproblemis: find 𝑣suc...

2022

-

[3]

Aflatregionat𝑣𝑘−1from𝜏𝑘−1to𝑎𝑘

-

[4]

Arampfrom𝑎𝑘to𝑏𝑘,centredat𝑐𝑘=𝜏𝑘−1+∆∕2,duringwhichthevoltransitionsfrom𝑣𝑘−1to𝑣𝑘

-

[5]

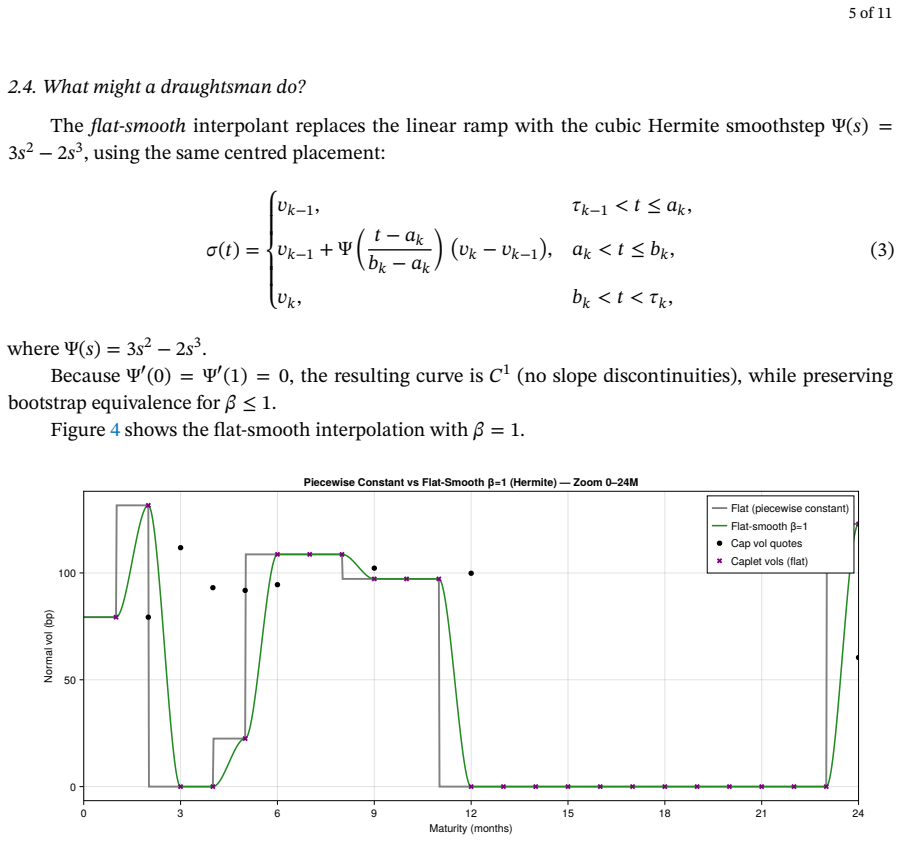

When𝛽=1,theramprunsfrom𝜏 𝑘−1to𝜏𝑘−1+∆,leavinganyremainingintervalflatat𝑣 𝑘

Aflatregionat𝑣𝑘from𝑏𝑘to𝜏𝑘. When𝛽=1,theramprunsfrom𝜏 𝑘−1to𝜏𝑘−1+∆,leavinganyremainingintervalflatat𝑣 𝑘. Figure3showstheimpactoftherampwidth𝛽onthecapletvolatilities. Maturity (months) 0 3 6 9 12 15 18 21 24 Normal vol (bp) 0 50 100 Piecewise Constant vs Flat-Linear — Zoom 0–24M Flat (piecewise constant) Flat-linear β=0.25 Flat-linear β=0.5 Flat-linear β=0.8 ...

-

[6]

NodePlacementandInterpolation Being overly enthusiastic about joining the dots, one may consider to directly interpolate linearly betweenthenodes,placedatthecapmaturities

SmootherInterpolations 3.1. NodePlacementandInterpolation Being overly enthusiastic about joining the dots, one may consider to directly interpolate linearly betweenthenodes,placedatthecapmaturities. Thereisnodependencytowardsthenextcaplet(thematrix islowertriangular)andthusbootstrappingisstillapplicable. However,thisapproachcanleadtostrong oscillations i...

-

[7]

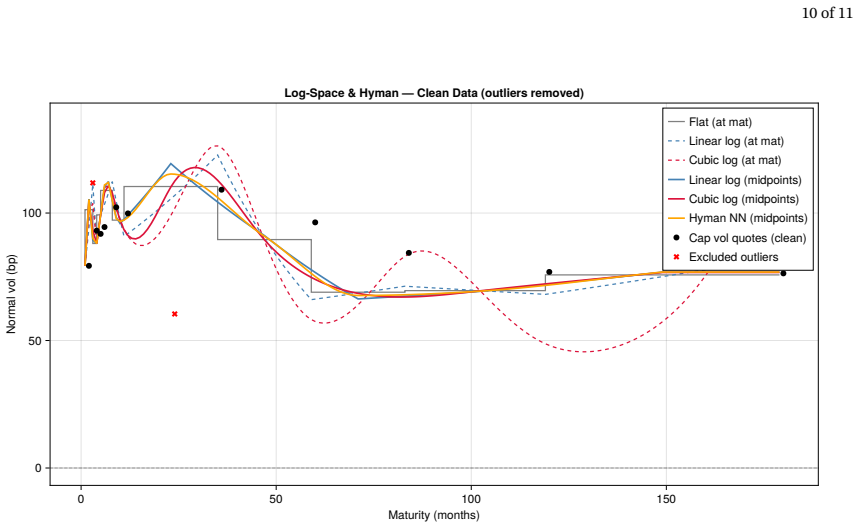

With midpoint nodes, the oscillations are muchreduced,andthenodenear18monthssettlesat −14bpinsteadof −159bp(Figure6)

OscillationsandBlow-ups Theresultingcapletvolatilitiesobtainedwithlinearinterpolationandat-maturitynodesshowstrong oscillations, with a node near 18 months settling at−159bp. With midpoint nodes, the oscillations are muchreduced,andthenodenear18monthssettlesat −14bpinsteadof −159bp(Figure6). Theoscillations growstrongerforlongermaturities. Thecubicsplinei...

-

[8]

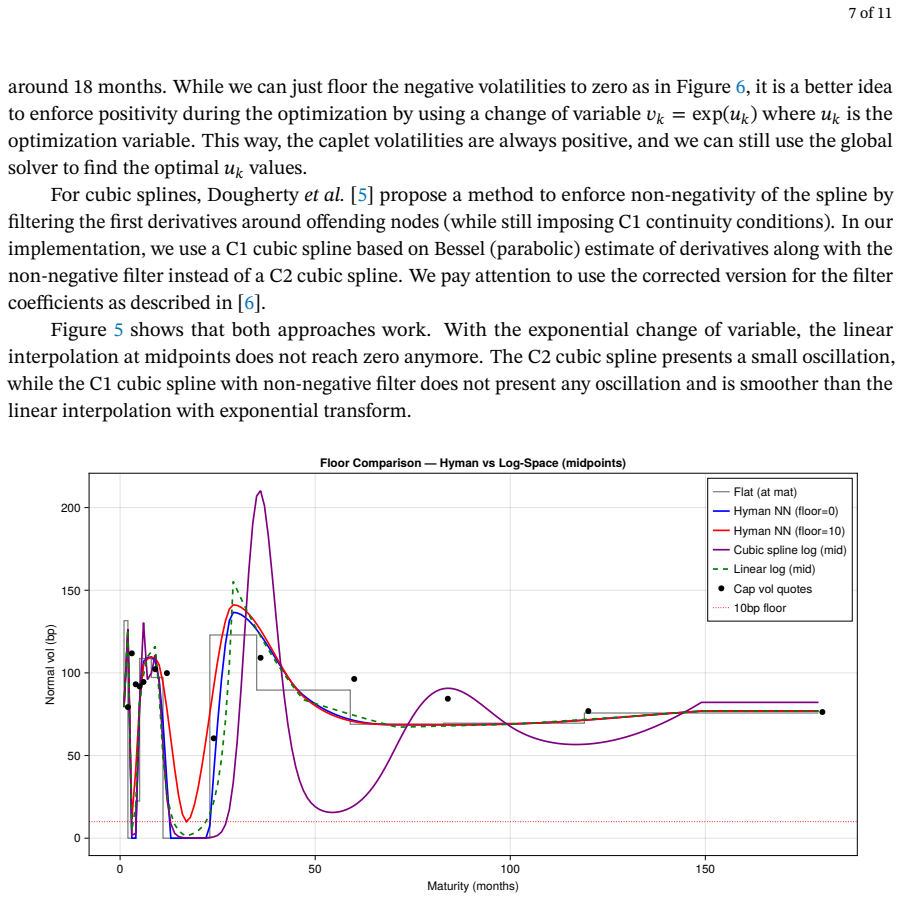

The2Ycapisverycheapcomparedtothe1Yand3Y caps,whichcreatesadipinthecapletvolatilitiesaround18months

TheRealIssueWithOurExample: The2YDip Thequalityofourcapquotesisinfactnotgreat. The2Ycapisverycheapcomparedtothe1Yand3Y caps,whichcreatesadipinthecapletvolatilitiesaround18months. Itisunlikelytobereal,butmaystem fromastalequote. 5.1. ModifiedZ-Score Givenaseriesofobservations𝑥 1,…,𝑥𝑛,themedianabsolutedeviation(MAD)is MAD=median (|𝑥𝑖−̃𝑥|), ̃𝑥=median(𝑥𝑖). Un...

-

[9]

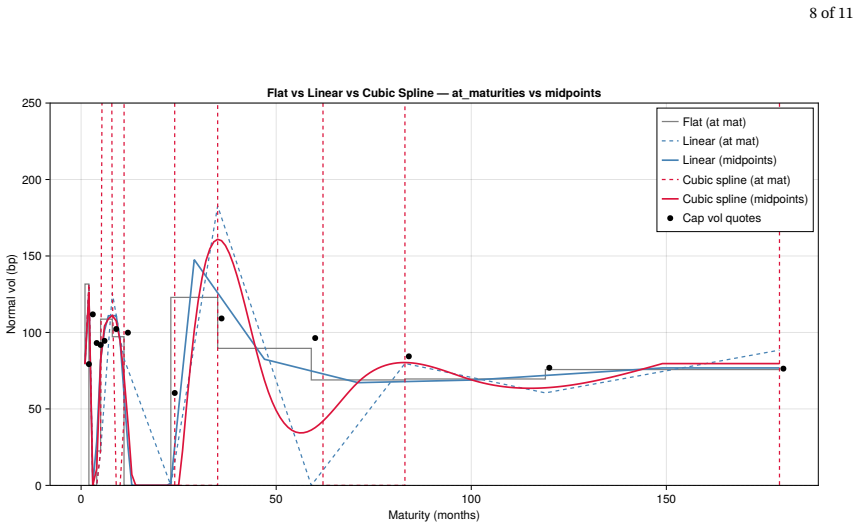

A flat-linear interpolation is always preferable as it produces a continuousvolcurve

Conclusion Whenusingasimplebootstrapalgorithmtostripthecapletvolatilities,thereisnogoodreasontouse a pure piecewise-constant interpolation. A flat-linear interpolation is always preferable as it produces a continuousvolcurve. Forsmootherinterpolations,theuseofmidpointnodesinsteadofat-maturitynodes helptoreduceoscillationssignificantly. Inparticular,wefoun...

-

[10]

Interestratesbenchmarkreformandoptionsmarkets.AvailableatSSRN35379252020

Piterbarg,V. Interestratesbenchmarkreformandoptionsmarkets.AvailableatSSRN35379252020

-

[11]

Benchmarkreformgoesnon-linear.Risk

Piterbarg,V. Benchmarkreformgoesnon-linear.Risk. net2020,pp. 1–5

-

[12]

Eight ways to strip your caplets: An introduction to caplet stripping.OpenGamma QuantitativeResearch2014

White, R.; Iwashita, Y. Eight ways to strip your caplets: An introduction to caplet stripping.OpenGamma QuantitativeResearch2014

-

[13]

Nocedal,J.;Wright,S.J.Numericaloptimization;Springer,2006

2006

-

[14]

Nonnegativity-,monotonicity-,orconvexity-preservingcubicand quinticHermiteinterpolation.mathematicsofcomputation1989,52,471–494

Dougherty,R.L.;Edelman,A.S.;Hyman,J.M. Nonnegativity-,monotonicity-,orconvexity-preservingcubicand quinticHermiteinterpolation.mathematicsofcomputation1989,52,471–494

-

[15]

TypoinHymannon-negativeconstraint-28yearslater

LeFloc’h,F. TypoinHymannon-negativeconstraint-28yearslater. https://chasethedevil.github.io/post/typo- in-hyman-non-negative-constraint/,2017. Accessed: 2026-05-05

2017

-

[16]

Theinfluencecurveanditsroleinrobustestimation.Journaloftheamericanstatisticalassociation 1974,69,383–393

Hampel,F.R. Theinfluencecurveanditsroleinrobustestimation.Journaloftheamericanstatisticalassociation 1974,69,383–393

1974

-

[17]

\nTotal-variance arbitrage violations at indices:

Iglewicz,B.;Hoaglin,D. Volume16: howtodetectandhandleoutliers,TheASQCbasicreferencesinquality control: statisticaltechniques,EdwardF.Mykytka.Ph. D.dissertation,Ph. D.,Editor1993. 11of11 AppendixA MarketData TableA1.capvolatilities(inbasispoints)onLibor-1MasofFebruary2022forastrike𝐾=0%. Maturity(months) 2 3 4 5 6 9 12 24 36 60 84 120 180 CapVol(bp) 79.30 1...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.