Recognition: unknown

Detecting Changes in Causal Dependence with Kernels and Copulas

Pith reviewed 2026-05-08 07:58 UTC · model grok-4.3

The pith

A quantity based on kernel mean embeddings of conditional copulas equals zero when causal dependence is unchanged and is positive otherwise.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We introduce a quantity based on the integrated difference between kernel mean embeddings of certain conditional copulas, which is provably equal to zero if the causal dependence does not change and strictly positive else. The framework treats both the causal mechanism and the distribution of the data as unknown, and supplies a consistent estimator that requires no additional parametric restrictions.

What carries the argument

The integrated difference between kernel mean embeddings of conditional copulas, which isolates shifts in the causal mechanism while remaining invariant to changes that leave the conditional dependence unchanged.

If this is right

- The statistic equals zero exactly when causal dependence remains unchanged and is strictly positive when it changes.

- A near-linear time estimator exists with explicit rates of convergence.

- The same statistic supports change-point detection when the time of change is unknown.

- No parametric assumptions on the data-generating process are required for the consistency result.

- Experiments confirm high detection accuracy on multiple synthetic and real-world data sets.

Where Pith is reading between the lines

- The approach could be used to monitor evolving causal effects in financial time series where market indicators affect asset returns at different strengths over time.

- Extensions to streaming or online settings would allow continuous detection of dependence shifts without re-estimating the entire history.

- The method might be combined with existing causal discovery algorithms to localize both when and in what direction a dependence change occurs.

Load-bearing premise

Kernel mean embeddings of the conditional copulas can be estimated consistently from finite samples without any parametric restrictions on the unknown causal mechanism or data distributions.

What would settle it

A controlled simulation in which the causal dependence of Y on X given Z changes yet the computed quantity remains zero, or fails to change yet the quantity becomes positive, would falsify the central claim.

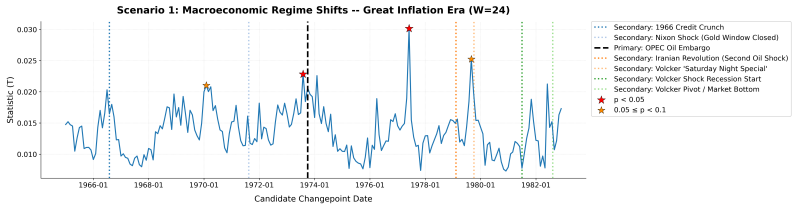

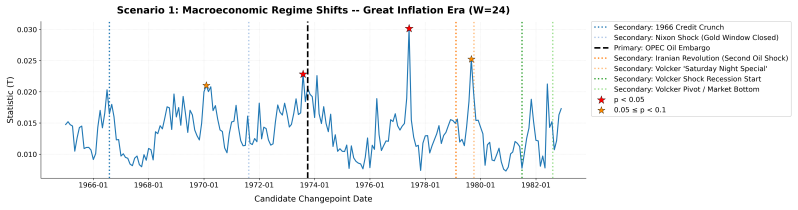

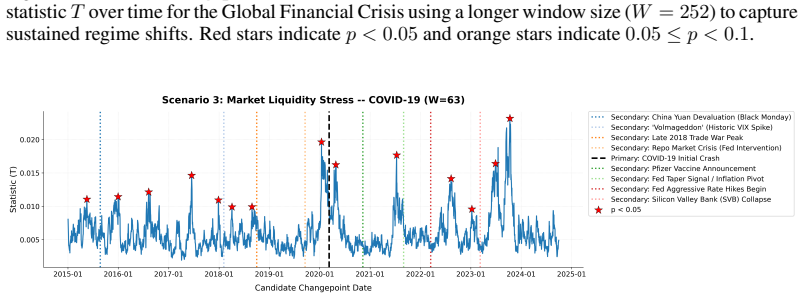

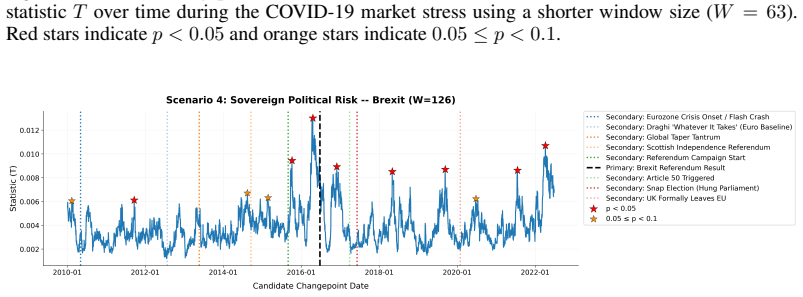

Figures

read the original abstract

We propose a framework for determining whether the causal dependence of an outcome $Y$ on a covariate $X$ changes at a given time point, given confounders $\boldsymbol{Z}$. For instance, in financial markets, the effect of a market indicator on asset returns may causally change over time. While many existing measures of association can be used to detect changes in joint and marginal distributions, in the absence of strong assumptions on the data generating process none are suitable for detecting changes in the causal mechanism or in the strength of causal relationship. In this work we approach the problem from a fully non-parametric perspective, and treat the causal mechanism as well as the distribution of the data as unknown. We introduce a quantity based on the integrated difference between kernel mean embeddings of certain conditionals copula, which is provably equal to zero if the causal dependence does not change and strictly positive else. A near-linear time estimator for the quantity is proposed, with rates of convergence explicitly spelled out. Extensive experiments demonstrate that the proposed statistic achieves high accuracy on multiple synthetic and real-world datasets. We additionally show how the proposed statistic can be used for change point detection when the goal is to detect changes in causal dependence occurring at an unknown times.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a non-parametric framework for detecting changes in the causal dependence of outcome Y on covariate X given confounders Z. It defines a population quantity as the integrated difference between kernel mean embeddings of conditional copulas, claimed to equal zero exactly when causal dependence is unchanged and to be strictly positive otherwise. A plug-in estimator with near-linear time complexity and explicit convergence rates is introduced, along with an extension to change-point detection at unknown times, supported by experiments on synthetic and real-world data.

Significance. If the central claims hold, the work provides a valuable non-parametric tool for isolating changes in causal mechanisms from mere distributional shifts, leveraging characteristic kernels and copulas without parametric restrictions on the DGP. The explicit rates, efficient estimator, and dual use for known and unknown change points enhance practicality for applications in finance and time-series analysis. The direct construction of the population quantity from embeddings (without reduction to fitted parameters) is a methodological strength.

major comments (1)

- The abstract and summary assert that the quantity is provably zero under no change with explicit convergence rates for the estimator, but the full derivations, explicit assumptions ensuring the kernel is characteristic on the space of conditional copula distributions, and verification that the finite-sample estimator matches the population quantity are not provided; this is load-bearing for the soundness of the zero/non-zero property and rates.

Simulated Author's Rebuttal

We thank the referee for their careful reading of the manuscript and for highlighting this important point regarding the rigor of our central claims. We address the major comment below.

read point-by-point responses

-

Referee: The abstract and summary assert that the quantity is provably zero under no change with explicit convergence rates for the estimator, but the full derivations, explicit assumptions ensuring the kernel is characteristic on the space of conditional copula distributions, and verification that the finite-sample estimator matches the population quantity are not provided; this is load-bearing for the soundness of the zero/non-zero property and rates.

Authors: We agree that the full derivations, assumptions, and verification steps are essential to substantiate the zero/non-zero property and the convergence rates. In the revised manuscript we will add a dedicated section (or substantially expanded appendix) that: (i) states the precise assumptions under which the chosen kernel is characteristic on the space of conditional copula distributions, (ii) supplies the complete proof that the integrated difference of the kernel mean embeddings equals zero if and only if the causal dependence is unchanged, and (iii) verifies that the finite-sample plug-in estimator is consistent for the population quantity together with the explicit convergence rates. These additions will be cross-referenced from the abstract and introduction so that the load-bearing claims are fully supported. revision: yes

Circularity Check

No significant circularity detected

full rationale

The central quantity is explicitly defined as the integrated difference between kernel mean embeddings of conditional copulas and is shown to equal zero exactly when the relevant conditional dependence is unchanged. This follows directly from the definition together with the characteristic property of the kernel; it is not a reduction of an independent target to a fitted parameter. The estimator is introduced separately as a plug-in with explicit convergence rates derived from standard kernel embedding theory. No self-citation is load-bearing for the zero/non-zero property, and no ansatz or uniqueness result is smuggled in. The derivation chain is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Kernel mean embeddings exist and are consistent estimators for the relevant conditional distributions under standard RKHS assumptions.

- domain assumption Conditional copulas correctly capture the dependence structure between X and Y given Z.

Reference graph

Works this paper leans on

-

[1]

International Conference on Algorithmic Learning Theory , pages=

A Hilbert space embedding for distributions , author=. International Conference on Algorithmic Learning Theory , pages=. 2007 , organization=

2007

-

[2]

2017 , volume =

Foundations and Trends in Machine Learning , title =. 2017 , volume =

2017

-

[3]

Journal of Machine Learning Research , volume =

Kenji Fukumizu and Le Song and Arthur Gretton , title =. Journal of Machine Learning Research , volume =

-

[4]

Le Song and Kenji Fukumizu and Arthur Gretton , title =

-

[5]

Smola and Kenji Fukumizu , title =

Le Song and Jonathan Huang and Alexander J. Smola and Kenji Fukumizu , title =. International Conference on Machine Learning , volume =

-

[6]

Conditional mean embeddings as regressors , year =

Steffen Gr. Conditional mean embeddings as regressors , year =

-

[7]

Judea Pearl , title =

-

[8]

2011 , publisher=

Reproducing kernel Hilbert spaces in probability and statistics , author=. 2011 , publisher=

2011

-

[9]

2002 , publisher=

Learning with kernels: support vector machines, regularization, optimization, and beyond , author=. 2002 , publisher=

2002

-

[10]

Rossi and Murat Kocaoglu , title =

Shanyun Gao and Raghavendra Addanki and Tong Yu and Ryan A. Rossi and Murat Kocaoglu , title =. Proc. of

-

[11]

The Review of Financial Studies , volume=

Empirical asset pricing via machine learning , author=. The Review of Financial Studies , volume=

-

[12]

Learning to Optimize under Non-Stationarity , booktitle =

Wang Chi Cheung and David Simchi. Learning to Optimize under Non-Stationarity , booktitle =

-

[13]

and Nikiforov, I

Basseville, M. and Nikiforov, I. , file =

-

[14]

Kernel Change-point Analysis , booktitle =

Za. Kernel Change-point Analysis , booktitle =

-

[15]

Toby Hocking and Guillem Rigaill and Guillaume Bourque , title =. Proc. of ICML , volume =

-

[16]

Killick and P

R. Killick and P. Fearnhead and I. A. Eckley , journal =. Optimal Detection of Changepoints With a Linear Computational Cost , volume =

-

[17]

Emmanouil Angelis and Francesco Quinzan and Ashkan Soleymani and Patrick Jaillet and Stefan Bauer , title =. Trans. Mach. Learn. Res. , volume =

-

[18]

2024 , journal =

Causal Change Point Detection and Localization , author=. 2024 , journal =

2024

-

[20]

Journal of Machine Learning Research , volume=

Optimistic Search: Change Point Estimation for Large-scale Data via Adaptive Logarithmic Queries , author=. Journal of Machine Learning Research , volume=

-

[21]

Journal of Machine Learning Research , volume=

An efficient two step algorithm for high dimensional change point regression models without grid search , author=. Journal of Machine Learning Research , volume=

-

[22]

2014 , publisher=

Probabilistic reasoning in intelligent systems: networks of plausible inference , author=. 2014 , publisher=

2014

-

[23]

Acta mathematica hungarica , volume=

On measures of dependence , author=. Acta mathematica hungarica , volume=. 1959 , publisher=

1959

-

[24]

Econometric Theory , volume=

Least absolute deviation estimation of a shift , author=. Econometric Theory , volume=. 1995 , publisher=

1995

-

[25]

The Annals of Mathematical Statistics , pages=

Nonparametric tests for shift at an unknown time point , author=. The Annals of Mathematical Statistics , pages=. 1968 , publisher=

1968

-

[26]

The Annals of Statistics , pages=

The asymptotic behavior of some nonparametric change-point estimators , author=. The Annals of Statistics , pages=. 1991 , publisher=

1991

-

[27]

Biometrika , pages=

Nonparametric data segmentation in multivariate time series via joint characteristic functions , author=. Biometrika , pages=. 2025 , publisher=

2025

-

[28]

Electronic Journal of Statistics , pages=

Optimal nonparametric change point analysis , author=. Electronic Journal of Statistics , pages=

-

[29]

Journal of machine learning research , volume=

A kernel multiple change-point algorithm via model selection , author=. Journal of machine learning research , volume=

-

[30]

Advances in neural information processing systems , volume=

Kernel measures of conditional dependence , author=. Advances in neural information processing systems , volume=

-

[31]

Data Mining and Knowledge Discovery , volume=

Learning Bayesian networks by hill climbing: efficient methods based on progressive restriction of the neighborhood , author=. Data Mining and Knowledge Discovery , volume=. 2011 , publisher=

2011

-

[32]

arXiv preprint arXiv:2111.14969 , year=

A fast non-parametric approach for local causal structure learning , author=. arXiv preprint arXiv:2111.14969 , year=

-

[33]

The Annals of Statistics , volume=

A simple measure of conditional dependence , author=. The Annals of Statistics , volume=. 2021 , publisher=

2021

-

[34]

Computational Statistics & Data Analysis , volume=

Conditional copulas, association measures and their applications , author=. Computational Statistics & Data Analysis , volume=. 2011 , publisher=

2011

-

[35]

Scandinavian Journal of Statistics , volume=

Estimation of a conditional copula and association measures , author=. Scandinavian Journal of Statistics , volume=. 2011 , publisher=

2011

-

[36]

Fonctions de r

Sklar, M , booktitle=. Fonctions de r

-

[37]

Applied Mathematics Letters , volume=

A topological proof of Sklar’s theorem , author=. Applied Mathematics Letters , volume=. 2013 , publisher=

2013

-

[38]

Journal of the Royal Statistical Society Series B: Statistical Methodology , volume=

Narrowest-over-threshold detection of multiple change points and change-point-like features , author=. Journal of the Royal Statistical Society Series B: Statistical Methodology , volume=. 2019 , publisher=

2019

-

[39]

The Journal of Machine Learning Research , volume=

Algorithms for discovery of multiple Markov boundaries , author=. The Journal of Machine Learning Research , volume=. 2013 , publisher=

2013

-

[40]

arXiv preprint arXiv:2504.02233 , year=

Testing independence and conditional independence in high dimensions via coordinatewise Gaussianization , author=. arXiv preprint arXiv:2504.02233 , year=

-

[41]

Huang, Zhen and Deb, Nabarun and Sen, Bodhisattva , TITLE =. J. Mach. Learn. Res. , FJOURNAL =. 2022 , PAGES =

2022

-

[42]

arXiv preprint arXiv:2010.01768 , year=

Measuring association on topological spaces using kernels and geometric graphs , author=. arXiv preprint arXiv:2010.01768 , year=

-

[43]

, TITLE =

Bhattacharya, Bhaswar B. , TITLE =. J. R. Stat. Soc. Ser. B. Stat. Methodol. , FJOURNAL =. 2019 , NUMBER =

2019

-

[44]

Advances in neural information processing systems , volume=

A measure-theoretic approach to kernel conditional mean embeddings , author=. Advances in neural information processing systems , volume=

-

[45]

arXiv preprint arXiv:2506.07760 , year=

Quickest Causal Change Point Detection by Adaptive Intervention , author=. arXiv preprint arXiv:2506.07760 , year=

-

[46]

Econometrica , volume =

Tests of Equality Between Sets of Coefficients in Two Linear Regressions , author =. Econometrica , volume =

-

[47]

Giornale dell'Istituto Italiano degli Attuari , volume =

Sulla determinazione empirica di una legge di distribuzione , author =. Giornale dell'Istituto Italiano degli Attuari , volume =

-

[48]

Bulletin of Moscow University , volume =

On the estimation of the discrepancy between empirical curves of distribution for two independent samples , author =. Bulletin of Moscow University , volume =

-

[49]

Advances in Neural Information Processing Systems , volume =

A Kernel Statistical Test of Independence , author =. Advances in Neural Information Processing Systems , volume =

-

[50]

Journal of the American Statistical Association , volume =

A New Coefficient of Correlation , author =. Journal of the American Statistical Association , volume =

-

[51]

Technometrics , volume =

The Use of the Rank Transform in Regression , author =. Technometrics , volume =

-

[52]

The Annals of Statistics , volume =

Measuring and Testing Dependence by Correlation of Distances , author =. The Annals of Statistics , volume =

-

[53]

The Annals of Statistics , volume =

Partial Distance Correlation with Methods for Dissimilarities , author =. The Annals of Statistics , volume =. 2014 , doi =

2014

-

[54]

Journal of Machine Learning Research , volume =

A Kernel Two-Sample Test , author =. Journal of Machine Learning Research , volume =

-

[55]

Advances in Neural Information Processing Systems , volume =

Random Features for Large-Scale Kernel Machines , author =. Advances in Neural Information Processing Systems , volume =

-

[56]

arXiv preprint arXiv:2403.12677 , year =

Causal Change Point Detection and Localization , author =. arXiv preprint arXiv:2403.12677 , year =

-

[57]

Journal of the American statistical Association , volume=

The Kolmogorov-Smirnov test for goodness of fit , author=. Journal of the American statistical Association , volume=. 1951 , publisher=

1951

-

[58]

Biometrika , volume=

Partial rank correlation , author=. Biometrika , volume=. 1942 , publisher=

1942

-

[59]

Metron , volume=

The distribution of the partial correlation coefficient , author=. Metron , volume=

-

[60]

2006 , publisher=

An introduction to copulas , author=. 2006 , publisher=

2006

-

[61]

CAM: Causal additive models, high-dimensional order search and penalized regression , journal=

B. CAM: Causal additive models, high-dimensional order search and penalized regression , journal=

-

[62]

Biocomputing 2002 , pages=

Estimation of genetic networks and functional structures between genes by using Bayesian networks and nonparametric regression , author=. Biocomputing 2002 , pages=. 2001 , publisher=

2002

-

[63]

Social science computer review , volume=

An algorithm for fast recovery of sparse causal graphs , author=. Social science computer review , volume=. 1991 , publisher=

1991

-

[64]

Studies in Logic and the Foundations of Mathematics , volume=

A theory of inferred causation , author=. Studies in Logic and the Foundations of Mathematics , volume=. 1995 , publisher=

1995

-

[65]

Partial distance correlation with methods for dissimilarities , journal=

Sz. Partial distance correlation with methods for dissimilarities , journal=

-

[66]

Advances in Neural Information Processing Systems , volume=

iscan: Identifying causal mechanism shifts among nonlinear additive noise models , author=. Advances in Neural Information Processing Systems , volume=

-

[67]

Journal of the American Statistical Association , volume=

A nonparametric approach for multiple change point analysis of multivariate data , author=. Journal of the American Statistical Association , volume=. 2014 , publisher=

2014

-

[68]

Rojas and Stefan Bauer , title =

Francesco Quinzan and Ashkan Soleymani and Patrick Jaillet and Cristian R. Rojas and Stefan Bauer , title =. Proc. of

-

[69]

Advances in Neural Information Processing Systems , volume=

Identifying general mechanism shifts in linear causal representations , author=. Advances in Neural Information Processing Systems , volume=

-

[70]

Advances in neural information processing systems , volume=

Direct estimation of differences in causal graphs , author=. Advances in neural information processing systems , volume=

-

[71]

arXiv preprint arXiv:1906.12024 , year=

Direct learning with guarantees of the difference dag between structural equation models , author=. arXiv preprint arXiv:1906.12024 , year=

-

[72]

Journal of the American Statistical Association , volume=

Kernel-based partial permutation test for detecting heterogeneous functional relationship , author=. Journal of the American Statistical Association , volume=. 2023 , publisher=

2023

-

[73]

International conference on machine learning , pages=

Causal structure discovery from distributions arising from mixtures of dags , author=. International conference on machine learning , pages=. 2020 , organization=

2020

-

[74]

SIAM Journal on Mathematics of Data Science , volume=

A rigorous theory of conditional mean embeddings , author=. SIAM Journal on Mathematics of Data Science , volume=. 2020 , publisher=

2020

-

[75]

ACM Transactions on Mathematical Software (TOMS) , volume=

An algorithm for finding best matches in logarithmic expected time , author=. ACM Transactions on Mathematical Software (TOMS) , volume=. 1977 , publisher=

1977

-

[76]

Scandinavian Journal of Statistics , pages=

Permutation and bootstrap Kolmogorov-Smirnov tests for the equality of two distributions , author=. Scandinavian Journal of Statistics , pages=. 1995 , publisher=

1995

-

[77]

2018 , publisher=

High-dimensional probability: An introduction with applications in data science , author=. 2018 , publisher=

2018

-

[78]

Journal of Machine Learning Research , volume =

Peter Spirtes , title =. Journal of Machine Learning Research , volume =

-

[79]

The Journal of Machine Learning Research , volume=

Hilbert space embeddings and metrics on probability measures , author=. The Journal of Machine Learning Research , volume=. 2010 , publisher=

2010

-

[80]

Econometrica , volume =

Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation , author =. Econometrica , volume =. 1982 , publisher =

1982

-

[81]

Journal of Political Economy , volume =

Oil and the Macroeconomy since World War II , author =. Journal of Political Economy , volume =. 1983 , publisher =

1983

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.