Recognition: no theorem link

The Phase Structure of Metallic Money: An MPTT Framework for the Spanish Price Revolution

Pith reviewed 2026-05-12 01:14 UTC · model grok-4.3

The pith

The Spanish Price Revolution featured a sharp weakening of money-to-price transmission after 1600.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

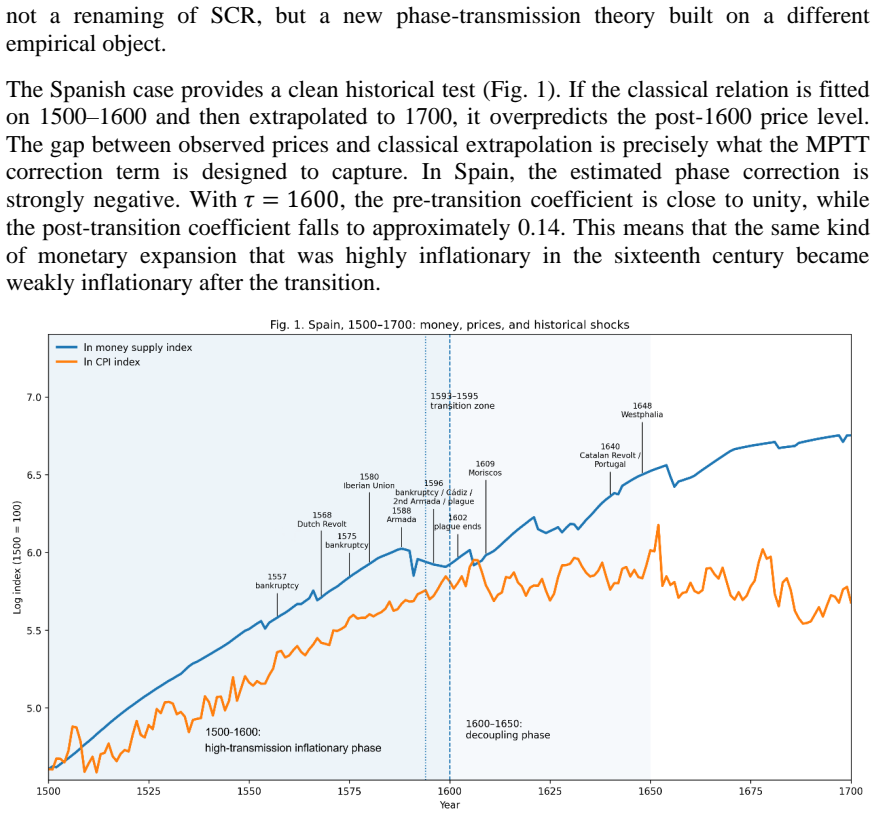

Using annual Spanish CPI and reconstructed money-supply data, the MPTT model with transition at 1600 recovers the classical relation before the break and applies a correction term after, estimating a drop in the money-price elasticity from 0.949 to 0.137.

What carries the argument

The MPTT two-phase model, which applies the standard monetary relation before a transition point tau and adds a gamma correction term after it to modify the transmission coefficient.

If this is right

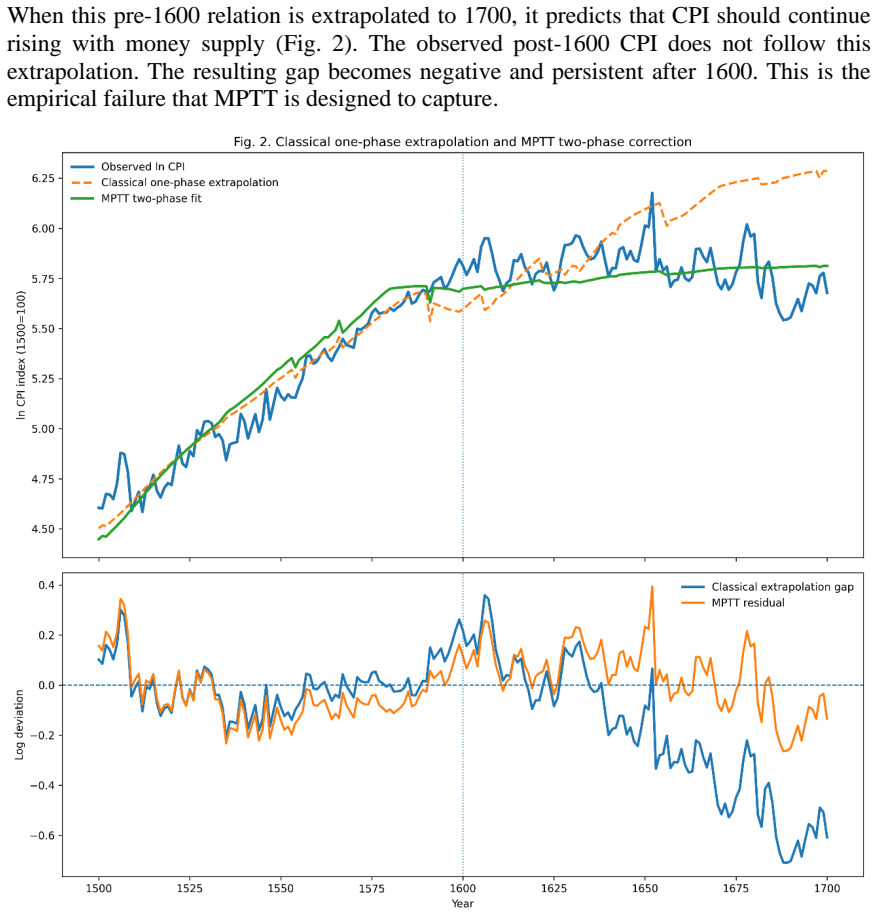

- A one-phase model fitted on pre-1600 data overpredicts prices after 1600.

- The episode reflects the rise and exhaustion of high-transmission metallic money inflation rather than a single monotonic process.

- An unrestricted break scan identifies a deeper BIC-minimizing break around 1636.

- Continued money supply growth after the transition had limited impact on CPI.

Where Pith is reading between the lines

- This framework could be applied to other historical periods with large monetary expansions to test for similar phase shifts.

- If the weakening reflects institutional or velocity changes, it raises questions about what causes transmission to decline over time.

Load-bearing premise

The reconstructed annual Spanish CPI and money-supply data accurately reflect the true historical values without significant measurement error or bias, and a discrete phase transition at 1600 is the appropriate structural model rather than a gradual change.

What would settle it

Observing that prices rose proportionally with money supply after 1600 in more accurate data, or finding that a continuous model fits better than the discrete break at 1600, would challenge the two-phase structure.

Figures

read the original abstract

The Spanish Price Revolution is usually treated as a classic case in which American bullion inflows expanded the money supply and generated inflation. This view captures the first phase of the episode but fails to explain why the same monetary expansion did not continue to produce proportional price growth after 1600. We develop a two-phase Money Phase Transition Theory (MPTT) model in which the classical monetary relation is recovered before a transition point, while a second-phase correction term modifies the money-price transmission coefficient after the transition. Using annual Spanish CPI and reconstructed money-supply data, we show that 1500-1600 was a high-transmission metallic inflationary phase: CPI increased approximately 3.35-fold while money supply increased approximately 3.73-fold. After 1600, money supply continued to rise, increasing approximately 1.82-fold during 1600-1650, while CPI rose only approximately 1.22-fold. A classical one-phase model fitted on 1500-1600, therefore, overpredicts post-1600 prices when extrapolated forward. The MPTT two-phase model with transition point tau=1600 estimates beta_1=0.949, gamma=-0.812, and beta_2=beta_1+gamma=0.137, indicating a sharp post-transition weakening of monetary transmission. An unrestricted break scan identifies a deeper BIC-minimizing break around 1636. These results suggest that the Spanish Price Revolution was not a single monotonic bullion-inflation process but the rise and exhaustion of high-transmission metallic money inflation.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that the Spanish Price Revolution was not a single monetary expansion process but exhibited a two-phase structure under the proposed Money Phase Transition Theory (MPTT). Using reconstructed annual Spanish CPI and money-supply data, it shows near-proportional growth from 1500-1600 (CPI 3.35-fold, money supply 3.73-fold) consistent with classical theory, followed by divergence after 1600 (money supply +1.82-fold but CPI only +1.22-fold). The MPTT model with fixed transition tau=1600 yields beta_1=0.949, gamma=-0.812, and beta_2=0.137, interpreted as a sharp post-transition weakening of monetary transmission; an unrestricted BIC scan prefers a 1636 break instead.

Significance. If the data reconstructions prove accurate and the discrete transition specification is robust, the MPTT framework supplies a concrete, falsifiable mechanism for why metallic money inflation can exhaust itself, with potential applicability to other historical episodes of bullion-driven price changes. The explicit parameter estimates and comparison to a one-phase extrapolation provide a clear benchmark for future work on structural breaks in monetary transmission.

major comments (2)

- [Abstract] Abstract: The headline parameter estimates (beta_1=0.949, gamma=-0.812, beta_2=0.137) and the two-phase interpretation are tied to the authors' choice of tau=1600, yet the text states that an unrestricted break scan identifies 1636 as BIC-minimizing. This choice is load-bearing; re-estimation at the preferred date is required to confirm whether the reported weakening of transmission (from 0.949 to 0.137) survives.

- [Abstract] Abstract: The central claim that post-1600 divergence reflects a genuine drop in the transmission coefficient rather than reconstruction artifacts rests on 'reconstructed' CPI and money-supply series, but no reconstruction methodology, interpolation details, bullion-inflow sources, or robustness checks to alternative series or error bounds are supplied. Systematic bias in either series around 1600 could mechanically generate the observed 1.82-fold vs. 1.22-fold contrast without any phase transition.

minor comments (2)

- [Abstract] The abstract should state the precise functional form of the MPTT two-phase regression (e.g., how the gamma correction term enters the money-price relation) so readers can replicate the beta_2 calculation.

- Report standard errors, t-statistics, or confidence intervals for beta_1, gamma, and the implied beta_2; also state the estimation method (OLS, etc.) and sample sizes for each phase.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive report. We agree that the choice of transition date and the documentation of the reconstructed series require further attention to strengthen the paper. We respond to each major comment below and will incorporate the necessary revisions.

read point-by-point responses

-

Referee: [Abstract] Abstract: The headline parameter estimates (beta_1=0.949, gamma=-0.812, beta_2=0.137) and the two-phase interpretation are tied to the authors' choice of tau=1600, yet the text states that an unrestricted break scan identifies 1636 as BIC-minimizing. This choice is load-bearing; re-estimation at the preferred date is required to confirm whether the reported weakening of transmission (from 0.949 to 0.137) survives.

Authors: We chose tau=1600 on historical grounds as the conventional endpoint of the main phase of the Price Revolution, while noting in the text that the unrestricted BIC scan selects 1636. To address the concern, we will re-estimate the MPTT model at the BIC-preferred date of 1636, report the resulting beta_1, gamma, and beta_2 values, and update the abstract and results to show whether the weakening of transmission (from near 1 to a low positive value) persists at this alternative break point. revision: yes

-

Referee: [Abstract] Abstract: The central claim that post-1600 divergence reflects a genuine drop in the transmission coefficient rather than reconstruction artifacts rests on 'reconstructed' CPI and money-supply series, but no reconstruction methodology, interpolation details, bullion-inflow sources, or robustness checks to alternative series or error bounds are supplied. Systematic bias in either series around 1600 could mechanically generate the observed 1.82-fold vs. 1.22-fold contrast without any phase transition.

Authors: We agree that explicit documentation of the data construction is essential to substantiate the claim. In the revision we will add a dedicated data appendix that details the bullion-inflow sources, the interpolation and aggregation procedures used to obtain annual series, and robustness checks against alternative reconstructions together with plausible error bounds. This will allow direct evaluation of whether systematic bias around 1600 could account for the observed divergence. revision: yes

Circularity Check

No significant circularity in the MPTT model derivation or application.

full rationale

The paper proposes an MPTT two-phase framework as a descriptive model for the Spanish Price Revolution, fits its parameters (beta_1, gamma, beta_2) to reconstructed annual CPI and money-supply series, and reports that a one-phase extrapolation from 1500-1600 overpredicts later prices. This is standard econometric model selection and parameter estimation on observed growth-rate differences; the estimates directly reflect the input data patterns rather than deriving an independent result that reduces to itself by construction. No self-citations, uniqueness theorems, or ansatzes are invoked as load-bearing steps. The choice of tau=1600 is presented alongside a BIC scan noting 1636, but the central claim remains an empirical description of the series, not a tautological loop. The derivation chain is self-contained against the data without circular reduction.

Axiom & Free-Parameter Ledger

free parameters (3)

- beta_1 =

0.949

- gamma =

-0.812

- tau =

1600

axioms (1)

- domain assumption Within each identified phase, the relationship between log money supply and log CPI is linear with constant coefficients.

invented entities (1)

-

Money Phase Transition

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Álvarez-Nogal, C., & Prados de la Escosura, L. (2013). The rise and fall of Spain (1270 – 1850). Economic History Review, 66(1), 1–37. Bai, J., & Perron, P. (1998). Estimating and testing linear models with multiple structural changes. Econometrica, 66(1), 47–78. Chen, Y., Palma, N., & Ward, F. (2021). Reconstruction of the Spanish money supply, 1492–1810...

work page 2013

-

[2]

Princeton University Press. Hamilton, E. J. (1934). American Treasure and the Price Revolution in Spain, 1501–1650. Harvard University Press. Huang, R. (2018). A physical review on currency. arXiv preprint arXiv:1805.12102. Huang, R. (2026a). A phase transition in monetary function explains expansion without inflation. arXiv preprint arXiv:2604.24035. Hua...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.