Recognition: no theorem link

Bayesian Dynamic Modeling of Realized Volatility in Financial Asset Price Forecasting

Pith reviewed 2026-05-13 03:53 UTC · model grok-4.3

The pith

A Bayesian model coupling realized volatility with price dynamics improves equity return forecasts by capturing leverage and feedback effects.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that integrating a novel dynamic gamma process model for realized volatility with Bayesian dynamic linear models for prices creates a reduced-form representation of leverage and feedback effects. This coupling of intraday volatility data with daily price series enables efficient conjugate Bayesian filtering, monitoring, and improved forecasting of equity returns, as shown in applications to multiple S&P sector ETFs.

What carries the argument

The dynamic gamma process for realized volatility proxies integrated into conditional Bayesian dynamic linear models for prices, which tracks volatility fluctuations and transmits leverage effects to the price forecasts.

If this is right

- Forecast accuracy for asset returns improves relative to models without the volatility component.

- The structure scales to multivariate price series for portfolio construction and risk management.

- Sequential analysis remains computationally straightforward with negligible added cost.

- Contextual understanding of volatility leverage and feedback effects becomes available from the fitted models.

Where Pith is reading between the lines

- The same reduced-form coupling could be tested on other asset classes such as currencies or commodities to check whether leverage patterns generalize.

- Real-time monitoring of the gamma process parameters might support adaptive trading rules that adjust exposure when volatility feedback strengthens.

- Adding macroeconomic covariates to the price models could be explored to isolate whether the volatility proxies retain explanatory power.

Load-bearing premise

The reduced-form coupling of realized volatility proxies into the price models accurately captures leverage and feedback without omitted-variable bias or misspecification in the gamma process dynamics.

What would settle it

Out-of-sample tests on the same S&P ETF data showing that forecast errors or log predictive scores from the new models are not materially better than those from standard dynamic linear models that ignore realized volatility.

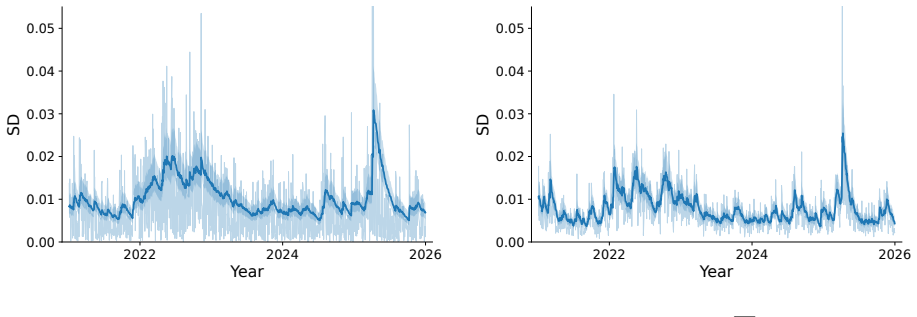

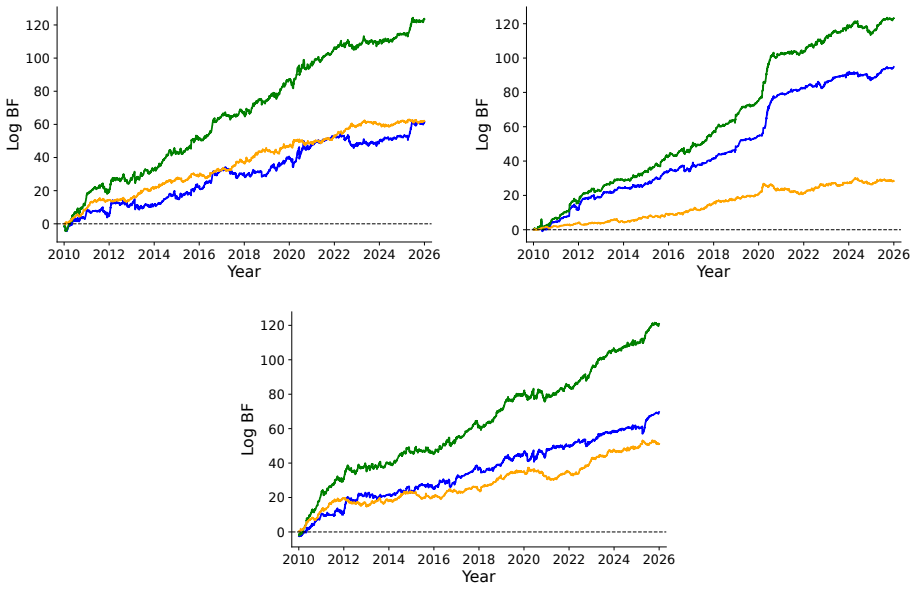

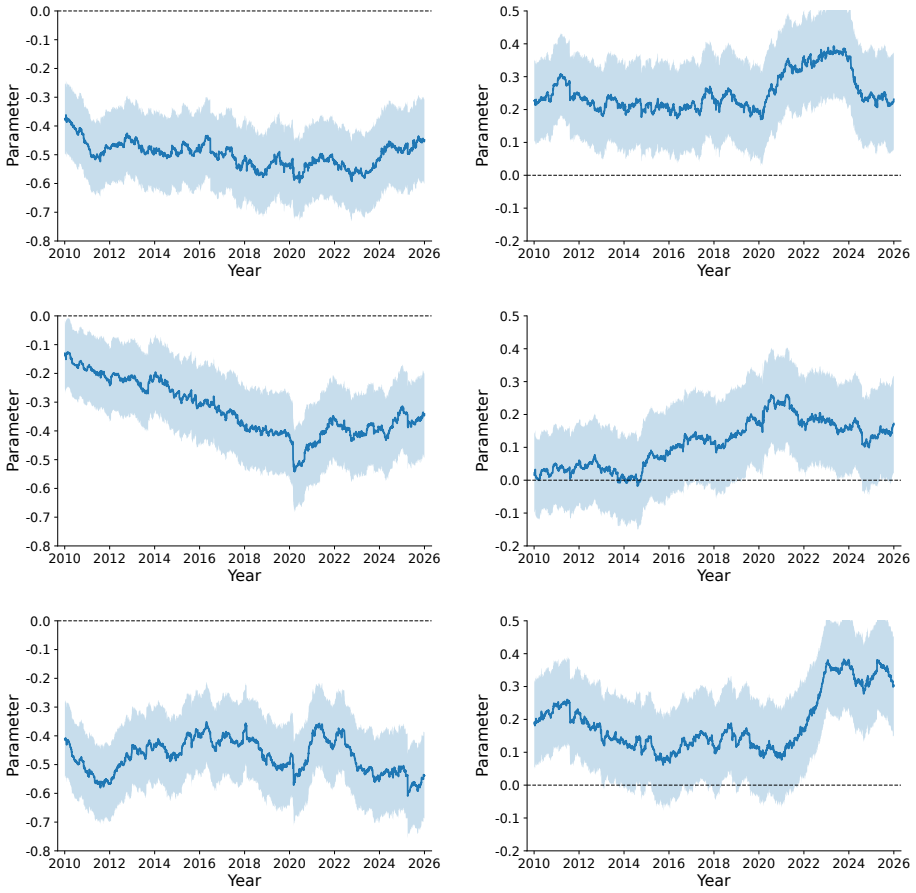

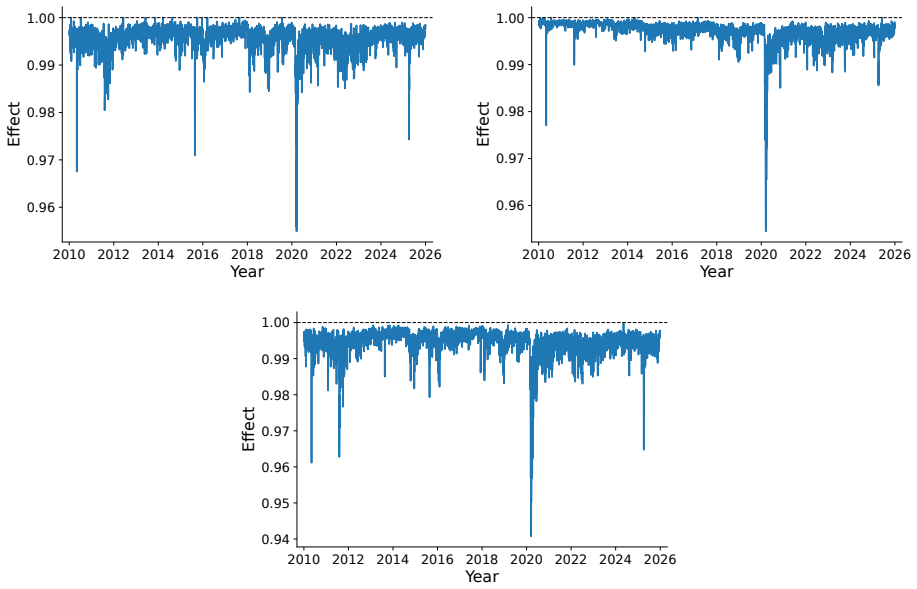

Figures

read the original abstract

We present a new class of Bayesian dynamic models for bivariate price-realized volatility time series in financial forecasting. A novel dynamic gamma process model adopted for realized volatility is integrated with traditional Bayesian dynamic linear models (DLMs) for asset price series. This represents reduced-form volatility leverage and feedback effects through use of realized volatility proxies in conditional DLMs for prices or returns, coupled with the synthesis of higher frequency data to track and anticipate volatility fluctuations. Analysis is computationally straightforward, extending conjugate-form Bayesian analyses for sequential filtering and model monitoring with simple and direct simulation for forecasting. A main applied setting is equity return forecasting with daily prices and realized volatility from high-frequency, intraday data. Detailed empirical studies of multiple S&P sector ETFs highlight the improvements achievable in asset price forecasting relative to standard models and deliver contextual insights on the nature and practical relevance of volatility leverage and feedback effects. The analytic structure and negligible extra computational cost will enable scaling to higher dimensions for multivariate price series forecasting for decouple/recouple portfolio construction and risk management applications.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims to introduce a new class of Bayesian dynamic models for bivariate price-realized volatility time series in financial forecasting. It integrates a novel dynamic gamma process model for realized volatility with traditional Bayesian dynamic linear models (DLMs) for asset prices or returns. This captures reduced-form volatility leverage and feedback effects via realized volatility proxies in conditional DLMs, with synthesis of higher-frequency data. The approach maintains conjugacy for straightforward sequential filtering, model monitoring, and simulation-based forecasting. Empirical studies on multiple S&P sector ETFs are said to show improved asset price forecasting relative to standard models and to deliver insights on the nature and practical relevance of leverage and feedback effects. The structure is presented as scalable to multivariate settings for portfolio and risk management.

Significance. If the empirical gains prove robust, the work provides a computationally efficient Bayesian framework for fusing intraday volatility information into daily price forecasts while preserving conjugacy and enabling direct simulation. The negligible extra cost and scalability to higher dimensions for decouple/recouple applications represent practical strengths. The reduced-form treatment of leverage/feedback could offer contextual insights useful for risk management if the modeling assumptions hold.

major comments (2)

- [§5] §5 (Empirical Studies): The central claim of improved forecasting performance on S&P sector ETFs and insights on leverage/feedback rests on comparisons to 'standard models,' but the manuscript provides insufficient detail on benchmark specifications (e.g., GARCH, HAR, or univariate DLMs), out-of-sample periods, loss functions, or statistical tests of differences. This directly affects evaluation of whether reported gains reflect genuine improvements or post-hoc choices, as highlighted by the stress-test concern.

- [§3.2] §3.2 (Reduced-form coupling): The bivariate DLM-gamma construction represents leverage and feedback solely through realized volatility proxies in the conditional DLMs. No explicit checks for omitted-variable bias (e.g., macro or order-flow factors) or sensitivity analyses on the dynamic gamma process specification are described; if these are absent, the forecast gains and interpretive conclusions on leverage/feedback may not be isolated from model artifact.

minor comments (2)

- [Abstract and §6] The abstract states 'negligible extra computational cost' but the main text lacks any timing benchmarks or scaling experiments to support this for multivariate extensions.

- [§3.1] Notation for the dynamic gamma process parameters (shape, rate, evolution) would benefit from a consolidated table or explicit listing to aid reproducibility.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments on our manuscript. We address each major comment point by point below, indicating where we will revise the paper to improve clarity, transparency, and robustness while preserving the core contributions of the Bayesian dynamic modeling framework.

read point-by-point responses

-

Referee: [§5] §5 (Empirical Studies): The central claim of improved forecasting performance on S&P sector ETFs and insights on leverage/feedback rests on comparisons to 'standard models,' but the manuscript provides insufficient detail on benchmark specifications (e.g., GARCH, HAR, or univariate DLMs), out-of-sample periods, loss functions, or statistical tests of differences. This directly affects evaluation of whether reported gains reflect genuine improvements or post-hoc choices, as highlighted by the stress-test concern.

Authors: We agree that greater specificity on the empirical setup is needed to allow readers to fully evaluate the reported forecast improvements. In the revised manuscript, we will expand Section 5 with explicit descriptions of all benchmark models (including exact GARCH and HAR specifications, as well as the univariate DLM baselines), the precise out-of-sample periods and rolling-window evaluation scheme, the loss functions employed (MSE, QLIKE, and others), and formal statistical tests such as Diebold-Mariano tests for pairwise forecast accuracy differences. We will also add the requested stress-test robustness checks using alternative market regimes and volatility proxies. These additions will be presented in new tables and text to demonstrate that the gains are not artifacts of post-hoc choices. revision: yes

-

Referee: [§3.2] §3.2 (Reduced-form coupling): The bivariate DLM-gamma construction represents leverage and feedback solely through realized volatility proxies in the conditional DLMs. No explicit checks for omitted-variable bias (e.g., macro or order-flow factors) or sensitivity analyses on the dynamic gamma process specification are described; if these are absent, the forecast gains and interpretive conclusions on leverage/feedback may not be isolated from model artifact.

Authors: The reduced-form coupling is intentional, as the paper focuses on a computationally conjugate and scalable framework that directly incorporates realized-volatility proxies to capture leverage and feedback effects without requiring a full structural model. However, we acknowledge the value of additional checks. In revision, we will add sensitivity analyses that vary key hyperparameters of the dynamic gamma process (e.g., evolution variance and shape parameters) and report the resulting impact on forecast performance and leverage-effect estimates. We will also include a brief discussion of potential omitted variables such as macro factors, noting that their explicit inclusion lies outside the reduced-form scope but that the current specification remains robust within the class of models that rely on volatility proxies. These additions will help readers assess whether the reported insights are sensitive to modeling choices. revision: partial

Circularity Check

No significant circularity; empirical claims rest on external data validation

full rationale

The paper introduces a modeling framework that couples DLMs for prices with a dynamic gamma process for realized volatility to capture leverage/feedback in reduced form. Forecasting proceeds via conjugate sequential updates and direct simulation, with performance evaluated on external S&P sector ETF data. No step equates a prediction to its own fitted inputs by construction, renames a known result, or relies on a self-citation chain for the core result. The derivation is self-contained against standard benchmarks and external time series.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

High-frequency realized stochastic volatility model , year =

Toshiaki Watanabe and Jouchi Nakajima , journal =. High-frequency realized stochastic volatility model , year =

-

[2]

Journal of Financial Econometrics , year =

Bollerslev, Tim and Litvinova, Julia and Tauchen, George , title =. Journal of Financial Econometrics , year =

-

[3]

Makoto Takahashi and Toshiaki Watanabe and Yasuhiro Omori , journal =. Forecasting Daily Volatility of Stock Price Index Using Daily Returns and Realized Volatility , year =

-

[4]

K. Irie and M. West , journal =. Bayesian emulation for multi-step optimization in decision problems , year =. doi:10.1214/18-BA1105 , url =

- [5]

- [6]

-

[7]

Jacquier, Eric and Polson, Nicholas G. and Rossi, Peter E. , journal =. Bayesian Analysis of Stochastic Volatility Models , year =

-

[8]

Statistical Aspects of ARCH and Stochastic Volatility , year =

Shephard, Neil , booktitle =. Statistical Aspects of ARCH and Stochastic Volatility , year =

-

[9]

Barndorff-Nielsen, Ole E. and Hansen, Peter R. and Lunde, Asger and Shephard, Neil , journal =. Designing Realized Kernels to Measure the Ex-Post Variation of Equity Prices in the Presence of Noise , year =

-

[10]

and Bollerslev, Tim and Mikkelsen, Hans Ole , journal =

Baillie, Richard T. and Bollerslev, Tim and Mikkelsen, Hans Ole , journal =. Fractionally Integrated Generalized Autoregressive Conditional Heteroskedasticity , year =

-

[11]

The Analysis of Stochastic Volatility in the Presence of Daily Realized Measures , year =

Koopman, Siem Jan and Scharth, Marcel , journal =. The Analysis of Stochastic Volatility in the Presence of Daily Realized Measures , year =

- [12]

-

[13]

Engle, Robert F. and Gallo, Giampiero M. , journal =. A Multiple Indicators Model for Volatility Using Intra-Daily Data , year =

-

[14]

and Kotz, Samuel and Balakrishnan, N

Johnson, Norman L. and Kotz, Samuel and Balakrishnan, N. , publisher =. Continuous Univariate Distributions, Volume 2 , year =

-

[15]

Realising the Future: Forecasting with High-Frequency-Based Volatility (

Shephard, Neil and Sheppard, Kevin , journal =. Realising the Future: Forecasting with High-Frequency-Based Volatility (. 2010 , number =

work page 2010

-

[16]

and Shephard, Neil , journal =

Pitt, Michael K. and Shephard, Neil , journal =. Filtering via Simulation: Auxiliary Particle Filters , year =

-

[17]

Pole, Andy and West, Mike and Harrison, Jeff , publisher =. Applied. 1994 , address =

work page 1994

-

[18]

Prado, Raquel and Ferreira, Marco A. R. and West, Mike , publisher =. Time Series: Modeling, Computation, and Inference , year =

- [19]

-

[20]

Mulder, Joris and Pericchi, Luis R. , journal =. The Matrix-. 2018 , number =

work page 2018

-

[21]

J. R. M. Hosking , journal =. Fractional Differencing , year =

-

[22]

Granger, C. W. J. and Joyeux, Roselyne , journal =. AN INTRODUCTION TO LONG-MEMORY TIME SERIES MODELS AND FRACTIONAL DIFFERENCING , year =. doi:https://doi.org/10.1111/j.1467-9892.1980.tb00297.x , eprint =

-

[23]

Long memory stochastic volatility : A bayesian approach , year =

Ngai Hang Chan and Giovanni Petris , journal =. Long memory stochastic volatility : A bayesian approach , year =. doi:10.1080/03610920008832549 , eprint =

-

[24]

Makoto Takahashi and Toshiaki Watanabe and Yasuhiro Omori , journal =. Forecasting Daily Volatility of Stock Price Index Using Daily Returns and Realized Volatility , year =. doi:https://doi.org/10.1016/j.ecosta.2021.08.002 , keywords =

-

[25]

Makoto Takahashi and Toshiaki Watanabe and Yasuhiro Omori , journal =. Volatility and quantile forecasts by realized stochastic volatility models with generalized hyperbolic distribution , year =. doi:https://doi.org/10.1016/j.ijforecast.2015.07.005 , keywords =

-

[26]

Studies of Stock Price Volatility Changes , year =

Black, Fischer , booktitle =. Studies of Stock Price Volatility Changes , year =

-

[27]

Localized Realized Volatility Modelling , year =

Chen, Ying and Härdle, Wolfgang Karl and Pigorsch, Uta , journal =. Localized Realized Volatility Modelling , year =

-

[28]

Stochastic volatility model with leverage and asymmetrically heavy-tailed error using

Jouchi Nakajima and Yasuhiro Omori , journal =. Stochastic volatility model with leverage and asymmetrically heavy-tailed error using. 2012 , issn =. doi:https://doi.org/10.1016/j.csda.2010.07.012 , keywords =

-

[29]

Leverage, heavy-tails and correlated jumps in stochastic volatility models , year =

Jouchi Nakajima and Yasuhiro Omori , journal =. Leverage, heavy-tails and correlated jumps in stochastic volatility models , year =. doi:https://doi.org/10.1016/j.csda.2008.03.015 , url =

-

[30]

Stochastic volatility with leverage: Fast and efficient likelihood inference , year =

Yasuhiro Omori and Siddhartha Chib and Neil Shephard and Jouchi Nakajima , journal =. Stochastic volatility with leverage: Fast and efficient likelihood inference , year =. doi:https://doi.org/10.1016/j.jeconom.2006.07.008 , keywords =

-

[31]

Measuring and Modeling Risk Using High-Frequency Data , year =

H. Measuring and Modeling Risk Using High-Frequency Data , year =. Applied Quantitative Finance , doi =

-

[32]

Barndorff‐Nielsen, Ole E. and Hansen, Peter R. and Lunde, Asger and Shephard, Neil , journal =. Realized Kernels in Practice: Trades and Quotes , year =

-

[33]

Combined Parameter and State Estimation in Simulation-Based Filtering , year =

Liu, Jane and West, Mike , editor =. Combined Parameter and State Estimation in Simulation-Based Filtering , year =. Sequential Monte Carlo Methods in Practice , doi =

-

[34]

N.J. Gordon and D.J. Salmond and A.F.M. Smith , journal =. Novel approach to nonlinear/non-Gaussian Bayesian state estimation , year =. doi:10.1049/ip-f-2.1993.0015 , eprint =

-

[35]

Christie, Andrew A. , journal =. The Stochastic Behavior of Common Stock Variances , year =

-

[36]

Engle, Robert F. and Ng, Victor K. , journal =. Measuring and Testing the Impact of News on Volatility , year =

-

[37]

Ameen, J. R. M. and Harrison, P. J. , booktitle =. Normal Discount. 1985 , address =

work page 1985

-

[38]

Dobrislav Dobrev and Pawel J. Szerszen , institution =. The Information Content of High-Frequency Data for Estimating Equity Return Models and Forecasting Risk , year =

-

[39]

Peter Christoffersen and Bruno Feunou and Kris Jacobs and Nour Meddahi , journal =. The Economic Value of Realized Volatility: Using High-Frequency Returns for Option Valuation , year =

-

[40]

Leverage Effects in Stochastic Volatility with Time‐Varying Persistence , year =

Nakajima, Jouchi and Omori, Yasuhiro , journal =. Leverage Effects in Stochastic Volatility with Time‐Varying Persistence , year =

-

[41]

and Hautsch, Nikolaus and Mihoci, Andrija , journal =

Härdle, Wolfgang K. and Hautsch, Nikolaus and Mihoci, Andrija , journal =. Local Adaptive Multiplicative Error Models for High-Frequency Forecasts , year =. doi:https://doi.org/10.1002/jae.2376 , eprint =

-

[42]

GENERALIZED AUTOREGRESSIVE SCORE MODELS WITH APPLICATIONS , year =

Creal, Drew and Koopman, Siem Jan and Lucas, André , journal =. GENERALIZED AUTOREGRESSIVE SCORE MODELS WITH APPLICATIONS , year =. doi:https://doi.org/10.1002/jae.1279 , eprint =

-

[43]

Robert F. Engle and Giampiero M. Gallo , journal =. A multiple indicators model for volatility using intra-daily data , year =. doi:https://doi.org/10.1016/j.jeconom.2005.01.018 , keywords =

-

[44]

Polson, Nicholas G. and Scott, James G. , journal =. On the Half-Cauchy Prior for a Global Scale Parameter , year =

-

[45]

Gelman, Andrew , journal =. Prior distributions for variance parameters in hierarchical models (Comment on article by Browne and Draper) , year =

-

[46]

and Bollerslev, TIM , journal =

Andersen, TORBEN G. and Bollerslev, TIM , journal =. Heterogeneous Information Arrivals and Return Volatility Dynamics: Uncovering the Long-Run in High Frequency Returns , year =. doi:https://doi.org/10.1111/j.1540-6261.1997.tb02722.x , eprint =

-

[47]

A Gamma Filter for Positive Parameter Estimation , year =

Govaers, Felix and Alqaderi, Hosam , booktitle =. A Gamma Filter for Positive Parameter Estimation , year =. doi:10.1109/MFI49285.2020.9235265 , keywords =

-

[48]

Eric Jacquier and Nicholas G. Polson and Peter E. Rossi , journal =. Bayesian Analysis of Stochastic Volatility Models , year =

-

[49]

Statistics for Long-Memory Processes , year =

Beran, Jan , publisher =. Statistics for Long-Memory Processes , year =. doi:10.1201/9780203738481 , url =

-

[50]

Local scale models: State space alternative to integrated GARCH processes , year =

Neil Shephard , journal =. Local scale models: State space alternative to integrated GARCH processes , year =. doi:https://doi.org/10.1016/0304-4076(94)90043-4 , keywords =

-

[51]

Hansen, Peter Reinhard and Huang, Zhuo and Shek, Howard Howan Stephen , month = oct, note =. Realized GARCH:. 2010 , day =. doi:10.2139/ssrn.1533475 , url =

-

[52]

Realising the future: forecasting with high-frequency-based volatility (HEAVY) models , year =

Shephard, Neil and Sheppard, Kevin , journal =. Realising the future: forecasting with high-frequency-based volatility (HEAVY) models , year =. doi:https://doi.org/10.1002/jae.1158 , eprint =

-

[53]

Andrew Gelman , journal =. 2006 , number =. doi:10.1214/06-BA117A , keywords =

-

[54]

M. West , journal =. Bayesian forecasting of multivariate time series:. 2020 , pages =

work page 2020

-

[55]

Amir Bashir and Carlos M. Carvalho and P. Richard Hahn and M. Beatrix Jones , journal =. Post-processing posteriors over precision matrices to produce sparse graph estimates , year =

-

[56]

Henrique Bolfarine and Carlos M. Carvalho and Hedibert F. Lopes and Jared S. Murray , journal =. Decoupling shrinkage and selection in. 2024 , pages =. doi:10.1214/22-BA1349 , keywords =

-

[57]

Comparative politics and the synthetic control method , year =

Abadie, Alberto and Diamond, Alexis and Hainmueller, Jens , journal =. Comparative politics and the synthetic control method , year =

-

[58]

Synthetic control methods for comparative case studies:

Abadie, Alberto and Diamond, Alexis and Hainmueller, Jens , journal =. Synthetic control methods for comparative case studies:. 2010 , pages =

work page 2010

-

[59]

K. Li and G. Tierney and C. Hellmayr and M. West , journal =. Compositional dynamic modelling for counterfactual prediction in multivariate time series , year =. doi:10.1002/asmb.2908 , url =

-

[60]

M. West and P. J. Harrison , journal =. Subjective intervention in formal models , year =

-

[61]

L. F. Gruber and M. West , journal =. 2016 , pages =. doi:10.1214/15-BA946 , url =

-

[62]

L. F. Gruber and M. West , journal =. Bayesian forecasting and scalable multivariate volatility analysis using simultaneous graphical dynamic linear models , year =. doi:10.1016/j.ecosta.2017.03.003 , owner =

-

[63]

Bayesian forecasting of stock Returns on the

Nelson Kyakutwika and Bruce Bartlett , journal =. Bayesian forecasting of stock Returns on the. 2024 , pages =

work page 2024

-

[64]

Quantitative Finance , title =

Griveau-Billion, Th. Quantitative Finance , title =. 2021 , pages =

work page 2021

-

[65]

G. C. Tiao and R. S. Tsay , journal =. Model specification in multivariate time series , year =

-

[66]

R. Yoshida and M. West , journal =. Bayesian learning in sparse graphical factor models via annealed entropy , year =

-

[67]

A. J. Cron and M. West , booktitle =. Models of random sparse eigenmatrices and. 2016 , editor =

work page 2016

-

[68]

Lopes, H. F. and C. M. Carvalho , journal =. Factor stochastic volatility with time varying loadings and. 2007 , pages =

work page 2007

-

[69]

Hedibert F. Lopes and Robert E. McCulloch and Ruey S. Tsay , journal =. Parsimony inducing priors for large scale state–space models , year =

-

[70]

Primiceri, G. E. , journal =. Time varying structural vector autoregressions and monetary policy , year =

- [71]

-

[72]

Gary Koop and Dimitris Korobilis , journal =. Large time-varying parameter. 2013 , pages =. doi:https://doi.org/10.1016/j.jeconom.2013.04.007 , url =

-

[73]

Bayesian Multivariate Time Series Methods for Empirical Macroeconomics , year =

Gary Koop and Dimitris Korobilis , journal =. Bayesian Multivariate Time Series Methods for Empirical Macroeconomics , year =

-

[74]

Journal of Applied Econometrics , title =

Marta Ba. Journal of Applied Econometrics , title =. 2010 , pages =

work page 2010

-

[75]

J. Nakajima and M. West , journal =. Bayesian dynamic factor models:. 2013 , pages =. doi:10.1093/jjfinec/nbs013 , url =

-

[76]

J. Nakajima and M. West , journal =. Dynamics and sparsity in latent threshold factor models:. 2017 , pages =. doi:10.1214/17-BJPS364 , url =

-

[77]

J. Nakajima and M. West , journal =. Bayesian analysis of latent threshold dynamic models , year =. doi:10.1080/07350015.2012.747847 , url =

-

[78]

J. Nakajima and M. West , journal =. Dynamic network signal processing using latent threshold models , year =. doi:10.1016/j.dsp.2015.04.008 , url =

-

[79]

C. M. Carvalho and J. E. Lucas and Q. Wang and J. Chang and J. R. Nevins and M. West , journal =. High-dimensional sparse factor modelling--. 2008 , pages =

work page 2008

-

[80]

Comparative politics and the synthetic control method revisited:

Klößner, Stefan and Kaul, Ashok and Pfeifer, Gregor and Schieler, Manuel , journal =. Comparative politics and the synthetic control method revisited:. 2018 , pages =

work page 2018

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.