Recognition: 2 theorem links

· Lean TheoremA deep learning approach for pricing convertible bonds with path-dependent reset and call provisions

Pith reviewed 2026-05-13 03:20 UTC · model grok-4.3

The pith

Deep learning prices path-dependent convertible bonds by solving high-dimensional PDEs with neural networks.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

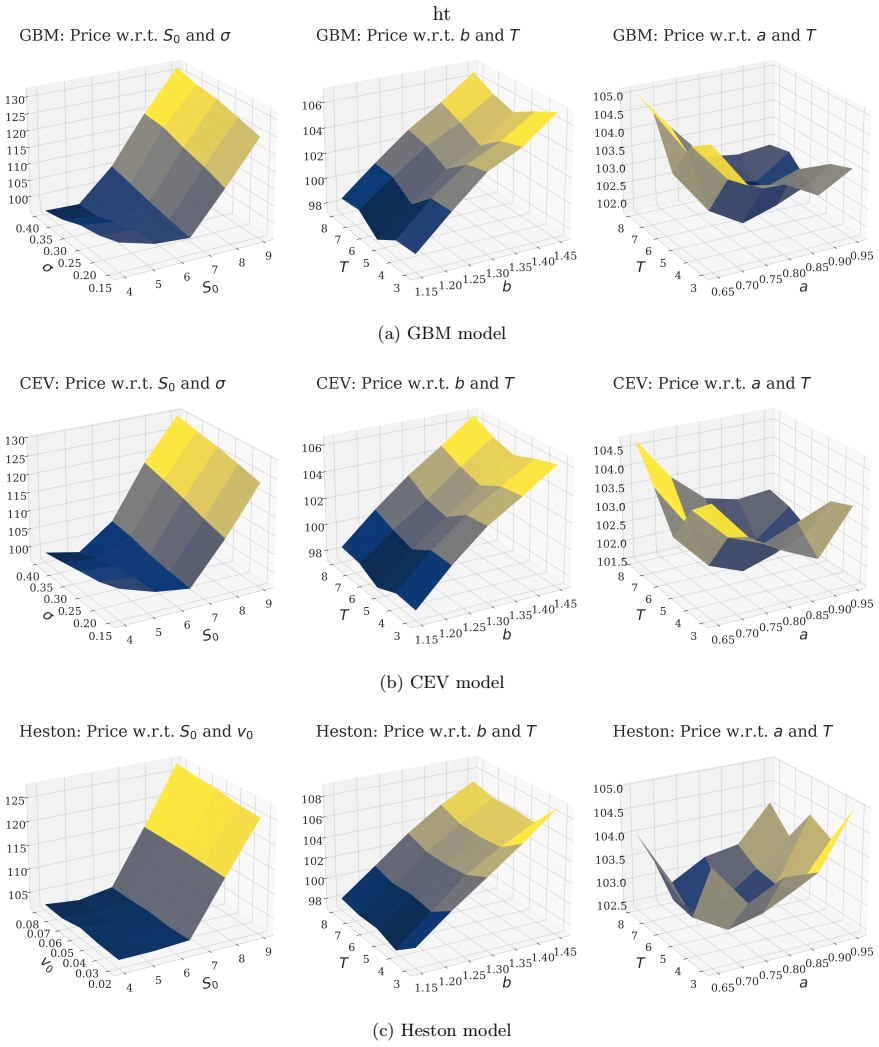

The valuation problem is cast as a path-dependent PDE for GBM, CEV, and Heston dynamics. A discrete-time dynamic programming scheme is constructed in which neural networks approximate the conditional expectations required to step the value backward from maturity. Application to the China CITIC Bank Convertible Bond produces stable prices and sensitivities across all three models, yielding the conclusions that contractual features dominate underlying dynamics, the call provision lowers price by truncating upside, and the downward reset lowers price by reducing the effective call threshold.

What carries the argument

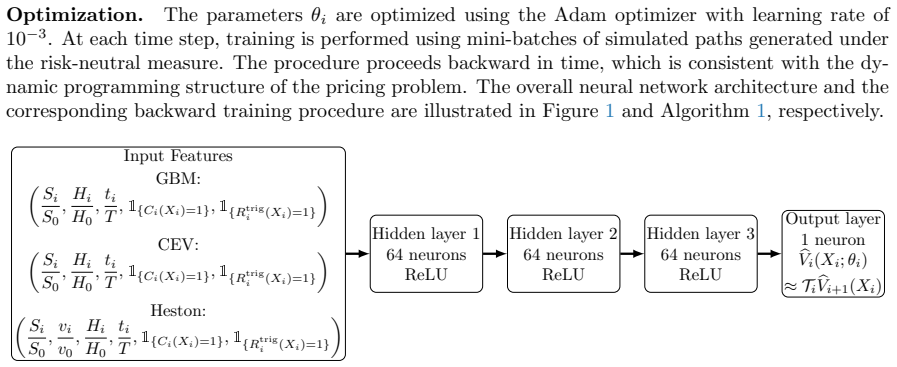

Path-dependent partial differential equation (PPDE) discretized via dynamic programming in which neural networks approximate the conditional expectations that depend on historical paths and the evolving conversion price.

If this is right

- Contractual features such as the call and reset provisions dominate the choice of underlying asset dynamics in determining convertible bond values.

- The issuer call provision decreases bond prices by truncating the holder's upside potential.

- The downward reset provision decreases bond prices by lowering the effective call threshold and increasing the likelihood of early redemption.

- The framework yields stable and accurate prices together with consistent sensitivity patterns across GBM, CEV, and Heston specifications.

Where Pith is reading between the lines

- The same neural-network dynamic programming structure could be applied to other path-dependent contracts such as barrier or lookback options to test computational scaling.

- The finding that contract terms outweigh model choice implies issuers may benefit from explicit valuation of reset-call interactions before issuing new bonds.

- Adding further state variables such as stochastic interest rates while retaining the neural network approximation provides a direct extension that can be checked numerically.

Load-bearing premise

The neural-network approximation of conditional expectations remains accurate and stable when the state space includes the full path history of the underlying and the dynamic conversion price.

What would settle it

Running the same pricing exercise on the China CITIC Bank Convertible Bond with a standard Monte Carlo simulation under identical path-dependent reset and call rules and comparing the resulting prices and sensitivities.

Figures

read the original abstract

This paper develops a deep learning-based framework for pricing convertible bonds with path-dependent contractual features, namely downward conversion price reset and issuer call clauses under rolling-window trigger rules, which are widespread in the convertible bond market. We formulate the valuation problem as a path-dependent partial differential equation (PPDE), which explicitly captures the dependence of the convertible bond value on the historical path of the underlying asset and the dynamic evolution of the conversion price. We derive consistent PPDE formulations for three canonical underlying dynamics: geometric Brownian motion (GBM), constant elasticity of variance (CEV) and Heston stochastic volatility. We then construct a discrete-time dynamic programming scheme in which conditional expectations are approximated by neural networks, which remains tractable in such high-dimensional path-dependent setting. Empirical tests on China CITIC Bank Convertible Bond show that our framework produces stable and accurate prices and sensitivity patterns across all model specifications. Three key economic insights emerge: 1. Contractual features dominate underlying dynamics in determining convertible bond values. 2. The call provision decreases convertible bonds prices by truncating upside gains. 3. Counterintuitively, despite improving conversion terms, the downward reset provision further decreases the price of convertible bonds by lowering the effective call threshold and making early redemption more likely. The proposed PPDE-deep learning approach provides an efficient, flexible tool for pricing convertible bonds with complex path-dependent structures.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a deep learning framework for pricing convertible bonds with path-dependent downward conversion price resets and issuer call provisions under rolling-window triggers. It formulates the valuation problem as a path-dependent PDE (PPDE) under GBM, CEV, and Heston dynamics, constructs a discrete-time dynamic programming scheme that approximates conditional expectations via neural networks, and reports empirical results on the China CITIC Bank Convertible Bond showing stable prices and sensitivities, along with three economic insights on the dominance of contractual features over underlying dynamics.

Significance. If the neural-network approximations prove reliable, the method would provide a practical tool for valuing complex path-dependent convertible bonds that are common in markets but intractable with standard PDE or Monte Carlo approaches. The reported dominance of contractual provisions and the counterintuitive price effects of resets could influence valuation practice and hedging strategies.

major comments (3)

- [Numerical scheme] Numerical scheme section: the discrete-time dynamic programming recursion replaces conditional expectations with neural-network approximations in a state space that includes the full rolling-window history of the underlying plus the evolving conversion price. No error bounds, convergence rates, or approximation guarantees specific to this high-dimensional path-dependent setting are supplied, even though the central claim of 'stable and accurate prices' rests on this step.

- [Empirical tests] Empirical tests section: the assertion that the framework produces 'stable and accurate prices and sensitivity patterns' across GBM/CEV/Heston is supported only by qualitative stability on one real bond; no quantitative error metrics, comparison to benchmark solvers (finite-difference, Monte Carlo with control variates, or closed-form GBM cases without reset/call), or analysis of NN approximation error are reported.

- [Model formulations and results] Model formulations and results: the three economic insights (contractual features dominate dynamics, call truncates upside, downward reset lowers effective call threshold) are derived from the NN-based prices. Without independent validation of the scheme on at least the GBM specification, these insights risk being artifacts of approximation bias rather than model behavior.

minor comments (1)

- [Abstract] Abstract: the phrase 'stable and accurate prices' is used without defining accuracy criteria or referencing any benchmark.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments. We agree that additional numerical validation and benchmark comparisons would strengthen the manuscript's claims regarding the reliability of the approximations and the robustness of the reported economic insights. We outline our responses and planned revisions below.

read point-by-point responses

-

Referee: Numerical scheme section: the discrete-time dynamic programming recursion replaces conditional expectations with neural-network approximations in a state space that includes the full rolling-window history of the underlying plus the evolving conversion price. No error bounds, convergence rates, or approximation guarantees specific to this high-dimensional path-dependent setting are supplied, even though the central claim of 'stable and accurate prices' rests on this step.

Authors: We acknowledge that the manuscript does not supply theoretical error bounds, convergence rates, or approximation guarantees for the neural-network approximations in this high-dimensional path-dependent setting. Deriving such guarantees is a significant theoretical undertaking that lies beyond the scope of the current applied work. In revision, we will add a dedicated discussion of the method's properties, citing relevant literature on neural-network approximations for dynamic programming and path-dependent PDEs, and include supplementary numerical experiments demonstrating empirical convergence with respect to network architecture and training parameters. revision: partial

-

Referee: Empirical tests section: the assertion that the framework produces 'stable and accurate prices and sensitivity patterns' across GBM/CEV/Heston is supported only by qualitative stability on one real bond; no quantitative error metrics, comparison to benchmark solvers (finite-difference, Monte Carlo with control variates, or closed-form GBM cases without reset/call), or analysis of NN approximation error are reported.

Authors: The referee is correct that the current empirical section provides only qualitative evidence from a single bond. We will revise the empirical tests to incorporate quantitative metrics, including the standard deviation of computed prices across repeated independent trainings and sensitivity analyses with respect to hyperparameters. For the GBM specification, we will add direct comparisons to Monte Carlo benchmarks (with and without control variates) and, for cases without reset or call features, to available closed-form or finite-difference solutions. revision: yes

-

Referee: Model formulations and results: the three economic insights (contractual features dominate dynamics, call truncates upside, downward reset lowers effective call threshold) are derived from the NN-based prices. Without independent validation of the scheme on at least the GBM specification, these insights risk being artifacts of approximation bias rather than model behavior.

Authors: We agree that the economic insights require independent validation on the GBM case to rule out approximation artifacts. In the revised manuscript, we will insert a new validation subsection that applies the scheme to the GBM dynamics in simplified settings (standard convertible bonds without path-dependent reset or call provisions) and compares the results against Monte Carlo benchmarks. The three insights will then be presented only after this validation step, with explicit caveats regarding the scope of the supporting evidence. revision: yes

Circularity Check

No circularity: numerical PPDE-DP scheme with NN approximation is independent of its outputs

full rationale

The derivation proceeds from PPDE formulation of the path-dependent convertible bond value (under GBM/CEV/Heston) to a discrete dynamic programming recursion whose conditional expectations are replaced by neural networks. No equation equates the final price to a fitted parameter, no prediction is a renaming of an input, and no load-bearing step reduces to a self-citation or ansatz smuggled from prior work by the same authors. The reported prices and sensitivities are computed outputs of the scheme rather than algebraically forced by its inputs. The absence of error bounds is a correctness concern, not a circularity one.

Axiom & Free-Parameter Ledger

free parameters (1)

- neural-network weights and biases

axioms (2)

- domain assumption The value function satisfies the path-dependent PDE derived from the chosen diffusion and the contractual rules.

- ad hoc to paper Neural networks can accurately approximate the conditional expectations arising in the dynamic-programming recursion.

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclearWe formulate the valuation problem as a path-dependent partial differential equation (PPDE)... discrete-time dynamic programming scheme in which conditional expectations are approximated by neural networks

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclearTheorem 2... V^h → V as h→0... neural network class is dense in L^2

Reference graph

Works this paper leans on

-

[1]

Ammann, M., Kind, A., and Wilde, C

doi: 10.1016/S0378-4266(01)00256-4. Ammann, M., Kind, A., and Wilde, C. Simulation-based pricing of convertible bonds.Journal of Empirical Finance, 15(2):310–331,

-

[2]

Arandjelovi´ c, A., Shevchenko, P

doi: 10.1016/j.jempfin.2006.06.008. Arandjelovi´ c, A., Shevchenko, P. V., Matsui, T., Murakami, D., and Myrvoll, T. Solving stochastic climate-economy models: a deep least-squares Monte Carlo approach.Mathematical Finance,

-

[3]

Bachouch, A., Hur´ e, C., Langren´ e, N., and Pham, H

doi: 10.3905/jod.2003.319208. Bachouch, A., Hur´ e, C., Langren´ e, N., and Pham, H. Deep neural networks algorithms for stochastic control problems on finite horizon: numerical applications.Methodology and Computing in Applied Probability, 24(1):143–178,

-

[4]

doi: 10.1007/s11009-019-09767-9. Barles, G. and Souganidis, P. E. Convergence of approximation schemes for fully nonlinear second order equations.Asymptotic Analysis, 4(3):271–283,

-

[5]

19 Barone-Adesi, G., Bermudez, A., and Hatgioannides, J

doi: 10.3233/ASY-1991-4305. 19 Barone-Adesi, G., Bermudez, A., and Hatgioannides, J. Two-factor convertible bonds valuation using the method of characteristics/finite elements.Journal of Economic Dynamics and Control, 27(10): 1801–1831,

-

[6]

doi: 10.1016/S0165-1889(02)00083-0. Batten, J. A., Khaw, K. L.-H., and Young, M. R. Pricing convertible bonds.Journal of Banking and Finance, 92:216–236,

-

[7]

doi: 10.1016/j.jbankfin.2018.05.006. Brennan, M. J. and Schwartz, E. S. Convertible bonds: valuation and optimal strategies for call and conversion.Journal of Finance, 32:1699–1715,

-

[8]

doi: 10.1111/j.1540-6261.1977.tb03364.x. Brennan, M. J. and Schwartz, E. S. Analyzing convertible bonds.Journal of Financial and Quantitative Analysis, 15(4):907–929,

-

[9]

doi: 10.2307/2330567. Carriere, J. Valuation of the early-exercise price for options using simulations and nonparametric regression.Insurance: Mathematics and Economics, 19(1):19–30,

-

[10]

doi: 10.1016/j.rinam. 2023.100423. Costabile, M. and Viviano, F. Combining lattice and regression methods for the evaluation of convert- ible bonds with soft call/put provisions.Journal of Computational and Applied Mathematics, 477: 117208,

-

[11]

doi: 10.1016/j.cam.2025.117208. Cox, J. C., Ross, S. A., and Rubinstein, M. Option pricing: a simplified approach.Journal of Financial Economics, 7(3):229–263,

-

[12]

Ekren, I., Touzi, N., and Zhang, J

doi: 10.1016/0304-405X(79)90015-1. Ekren, I., Touzi, N., and Zhang, J. Viscosity solutions of fully nonlinear parabolic path dependent PDEs: Part I.Annals of Probability, 44(2):1212–1253, 2016a. doi: 10.1214/14-AOP999. Ekren, I., Touzi, N., and Zhang, J. Viscosity solutions of fully nonlinear parabolic path dependent PDEs: Part II.Annals of Probability, 4...

-

[13]

Feng, Y., Huang, B.-H., and Huang, Y

doi: 10.21314/JCF.2021.006. Feng, Y., Huang, B.-H., and Huang, Y. Valuing resettable convertible bonds: based on path decom- posing.Finance Research Letters, 19:279–290,

-

[14]

doi: 10.1016/j.frl.2016.09.002. Franco, C. d., Nicolle, J., and Pham, H.Discrete-time portfolio optimization under maximum drawdown constraint with partial information and deep learning resolution, pages 101–136. Springer,

-

[15]

doi: 10.1007/978-3-030-98519-6

-

[16]

Hur´ e, C., Pham, H., Bachouch, A., and Langren´ e, N

doi: 10.3905/jod.1994.407908. Hur´ e, C., Pham, H., Bachouch, A., and Langren´ e, N. Deep neural networks algorithms for stochastic control problems on finite horizon: convergence analysis.SIAM Journal on Numerical Analysis, 59 (1):525–557,

-

[17]

doi: 10.1137/20M1316640. Ingersoll, J. E. A contingent-claims valuation of convertible securities.Journal of Financial Economics, 4(3):289–321,

-

[18]

doi: 10.1016/0304-405X(77)90004-6. Kimura, T. and Shinohara, T. Monte Carlo analysis of convertible bonds with reset clauses.European Journal of Operational Research, 168(2):301–310,

-

[19]

doi: 10.1016/j.ejor.2004.07.008. Lau, K. W. and Kwok, Y. K. Anatomy of option features in convertible bonds.Journal of Futures Markets, 24(6):513–532,

-

[20]

doi: 10.1002/fut.10127. Lewis, C. M. Convertible debt: valuation and conversion in complex capital structures.Journal of Banking and Finance, 15(3):665–682,

-

[21]

Li, L., Hu, Z., Guo, H., Wang, L., Zhang, Z., and Xu, Y

doi: 10.1016/0378-4266(91)90091-Y. Li, L., Hu, Z., Guo, H., Wang, L., Zhang, Z., and Xu, Y. Pricing convertible bonds based on GAN and transformer.Computational Economics, 2025a. doi: 10.1007/s10614-025-11021-z. 20 Li, Z., Wang, Y., Qiao, F., and Yu, M. Convertible bond return predictability with machine learning. Journal of Financial Markets, page 101010...

-

[22]

doi: 10.1080/14697688.2026.2616345. Lin, S. and Zhu, S.-P. Numerically pricing convertible bonds under stochastic volatility or stochastic interest rate with an ADI-based predictor–corrector scheme.Computers and Mathematics with Applications, 79(5):1393–1419,

-

[23]

doi: 10.1016/j.camwa.2019.09.003. Liu, Q. and Guo, S. An excellent approximation for themout ofnday provision.North American Journal of Economics and Finance, 54:101222,

-

[24]

doi: 10.1016/j.najef.2020.101222. Longstaff, F. A. and Schwartz, E. S. Valuing American options by simulation: a simple least-squares approach.Review of Financial Studies, 14(1):113–147,

-

[25]

doi: 10.1093/rfs/14.1.113. Ma, C. and Xu, W. Valuation model for Chinese convertible bonds with soft call/put provision under the hybrid willow tree.Quantitative Finance, 20(12):1999–2014,

-

[26]

doi: 10.1080/14697688.2020. 1814022. McGuinness, P. B. and Keasey, K. The listing of Chinese state-owned banks and their path to banking and ownership reform.China Quarterly, 201:125–155,

-

[27]

doi: 10.1017/S030574100999110X. Nyborg, K. G. The use and pricing of convertible bonds.Applied Mathematical Finance, 3(3):167–190,

-

[28]

doi: 10.1080/13504869600000009. Roch, A. Optimal liquidation through a limit order book: a neural network and simulation ap- proach.Methodology and Computing in Applied Probability, 25(3):1–29,

-

[29]

doi: 10.3905/jfi.1998.408243. Warin, X. Reservoir optimization and machine learning methods.EURO Journal on Computational Optimization, 11:100068,

-

[30]

Xu, W., Yu, B., Yao, L., and Zhou, Y

doi: 10.1016/j.ejco.2023.100068. Xu, W., Yu, B., Yao, L., and Zhou, Y. A tree model for pricing convertible bonds with equity, market and default risk.Computational Economics, 34(2):169–194,

-

[31]

Monte Carlo analysis of convertible bonds with reset clause

doi: 10.1007/s10614-009-9170-8. Yang, J., Choi, Y., Li, S., and Yu, J. A note on “Monte Carlo analysis of convertible bonds with reset clause”.European Journal of Operational Research, 200(3):924–925,

-

[32]

doi: 10.1016/j.ejor.2009. 02.012. Yarotsky, D. Error bounds for approximations with deep ReLU networks.Neural Networks, 94: 103–114,

-

[33]

doi: 10.1016/j.neunet.2017.07.002. Zabolotnyuk, Y., Jones, R. J., and Fan, H. An empirical comparison of convertible bond valuation models.Financial Management, 39(2):675–705,

-

[34]

doi: 10.1111/j.1755-053X.2010.01088.x. Zhang, S. and Zhu, X. Financing structure and risk response in overseas investment and M&A by Chinese enterprises. InThe Challenge of “Going Out” Chinese Experiences in Outbound Investment, pages 71–87. Springer,

-

[35]

doi: 10.1007/978-981-99-3326-6

-

[36]

doi: 10.3390/axioms13040218. Zhu, S.-P. A closed-form analytical solution for the valuation of convertible bonds with constant dividend yield.ANZIAM Journal, 47(4):477–494,

-

[37]

Zhu, S.-P., Lin, S., and Lu, X

doi: 10.1017/S1446181100010087. Zhu, S.-P., Lin, S., and Lu, X. Pricing puttable convertible bonds with integral equation approaches. Computers and Mathematics with Applications, 75(8):2757–2781,

-

[38]

doi: 10.1016/j.camwa.2018. 01.007. 21 A Proofs in Section 2 A.1 Proof of Theorem 1 Proof.We derive the PPDE satisfied by the convertible bond value functionalV(t, ω t, Ht) on the continuation regionC. By definition ofC, on the continuation region, neither the reset clause nor the call clause is active, so the conversion priceH t remains locally constant a...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.