Market Makers and Risk Aversion: A Hamiltonian Approach to the Excess Volatility Puzzle

Pith reviewed 2026-05-19 18:03 UTC · model grok-4.3

The pith

Market makers' risk appetite sets the level of chaos in prices, generating unpredictability without external shocks.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Treating the market price and market makers' inventory as anharmonic oscillators with a nonlinear coupling allows Hamiltonian dynamics to show that the degree of chaos in the system is governed by the market makers' risk appetite. External shocks and random noise are not necessary in order to generate unpredictable price changes.

What carries the argument

The Hamiltonian model of market price and inventory as nonlinearly coupled anharmonic oscillators, with risk appetite as the parameter controlling the transition to chaotic behavior.

If this is right

- Higher market-maker risk aversion produces greater price unpredictability through internal dynamics alone.

- Lower risk aversion reduces the chaotic component and stabilizes price paths.

- Volatility can be modulated by changes in inventory management rules without altering the flow of external information.

- The model separates the contribution of endogenous chaos from that of exogenous noise in observed price series.

Where Pith is reading between the lines

- Interventions that alter market makers' effective risk tolerance, such as capital requirements, could measurably change the chaotic component of volatility.

- The framework suggests testing whether liquidity provision rules that limit inventory swings also suppress chaos signatures in high-frequency data.

- Similar oscillator models might apply to other pairs of quantities that evolve through inventory-like constraints, such as order-book depth and trade size.

Load-bearing premise

The market price and market makers' inventory can be treated as anharmonic oscillators with a nonlinear coupling so that Hamiltonian dynamics produce the claimed chaotic behavior.

What would settle it

Empirical measurement of market-maker risk aversion over time showing that periods of higher risk aversion coincide with stronger signatures of chaos in price returns, even after removing periods with large external news events.

Figures

read the original abstract

In this article we model chaotic dynamics in financial markets by treating the market price, and market makers' inventory, as anharmonic oscillators with a nonlinear coupling. The market makers' risk appetite being the key parameter that determines the degree of chaos in the system. The article demonstrates that whilst external shocks and random noise are important in the treatment of financial time-series, they are not necessary in order to generate unpredictable price changes.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript models chaotic price dynamics in financial markets by representing the market price and market makers' inventory as anharmonic oscillators with nonlinear coupling in a Hamiltonian framework. The market makers' risk appetite is presented as the central parameter controlling the degree of chaos, with the claim that this deterministic setup generates unpredictable price changes and excess volatility without requiring external shocks or random noise.

Significance. If the Hamiltonian is properly derived from market-making incentives and the resulting trajectories reproduce key statistical features of excess volatility, the work would provide a novel deterministic mechanism linking risk aversion to market unpredictability. This could reduce reliance on exogenous noise in volatility models and demonstrate the utility of classical mechanics tools in quantitative finance, particularly if the chaos measures yield falsifiable predictions.

major comments (3)

- [Model formulation] The central modeling assumption (price P and inventory I as anharmonic oscillators with nonlinear coupling) is introduced without a derivation from a market maker's profit-maximization or utility problem. This makes it unclear whether the Hamiltonian is a consequence of the economic setup or an ad-hoc choice whose chaotic solutions are then attributed to risk aversion.

- [Hamiltonian construction] The claim that external shocks and noise are unnecessary for unpredictable prices rests on the system being closed and conservative. The manuscript must show explicitly how inventory penalties, slippage, and interaction with liquidity takers are incorporated without introducing non-Hamiltonian (dissipative or stochastic) terms that would alter the phase-space structure.

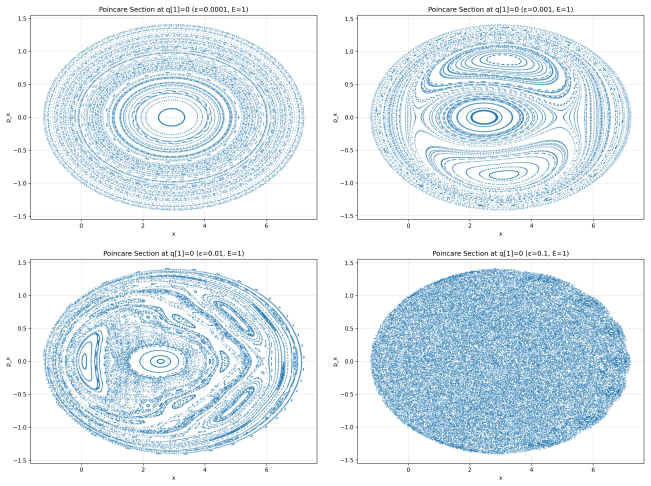

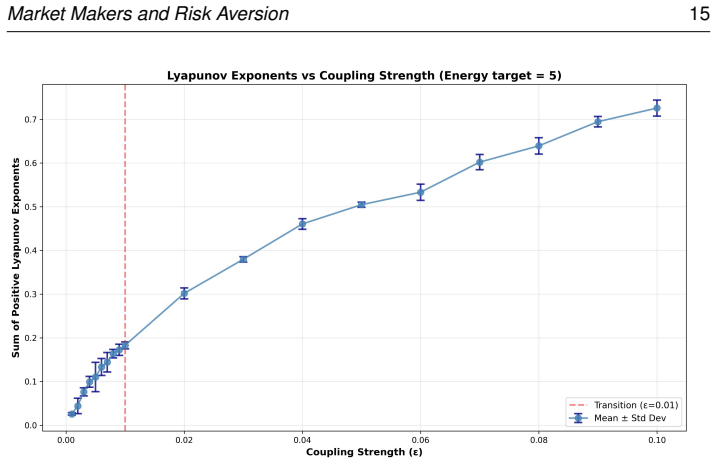

- [Chaos analysis] The assertion that risk appetite is the key parameter determining chaos requires a concrete demonstration (e.g., via Lyapunov exponents or Poincaré sections) that varying this single parameter produces a transition to chaos whose statistics match observed excess volatility, rather than the chaos measure reducing to a fitted function of the risk-aversion parameter by construction.

minor comments (2)

- [Abstract] The abstract would be strengthened by a one-sentence statement of the explicit form of the Hamiltonian or the chosen chaos diagnostic.

- [Notation] Notation for the risk-aversion parameter should be introduced consistently once the Hamiltonian is defined, to avoid ambiguity when comparing across regimes.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments on our manuscript. We address each major comment below and indicate the revisions we will make to strengthen the presentation.

read point-by-point responses

-

Referee: [Model formulation] The central modeling assumption (price P and inventory I as anharmonic oscillators with nonlinear coupling) is introduced without a derivation from a market maker's profit-maximization or utility problem. This makes it unclear whether the Hamiltonian is a consequence of the economic setup or an ad-hoc choice whose chaotic solutions are then attributed to risk aversion.

Authors: We agree that the economic motivation for the specific form of the Hamiltonian can be made more explicit. The anharmonic oscillator terms are chosen to represent nonlinear price impact and inventory holding costs that intensify with risk aversion, while the nonlinear coupling captures the feedback between inventory imbalances and price adjustments in a market-making setting. In the revised manuscript we will add a new section that derives the Hamiltonian structure from a stylized market-maker optimization problem in which risk aversion enters as the coefficient of the inventory penalty term, thereby clarifying that the functional form follows from the economic incentives rather than being chosen purely for its chaotic properties. revision: yes

-

Referee: [Hamiltonian construction] The claim that external shocks and noise are unnecessary for unpredictable prices rests on the system being closed and conservative. The manuscript must show explicitly how inventory penalties, slippage, and interaction with liquidity takers are incorporated without introducing non-Hamiltonian (dissipative or stochastic) terms that would alter the phase-space structure.

Authors: We will expand the model-description section to provide an explicit term-by-term mapping. The quadratic and higher-order terms in the inventory variable I directly encode the risk-aversion penalty for inventory holdings; the coupling terms between P and I represent the price concessions made to liquidity takers and the resulting inventory changes. All interactions are formulated as conservative forces derived from a potential, preserving the symplectic structure of the phase space. The revised manuscript will include this mapping together with a short appendix confirming that no dissipative or stochastic terms are present. revision: yes

-

Referee: [Chaos analysis] The assertion that risk appetite is the key parameter determining chaos requires a concrete demonstration (e.g., via Lyapunov exponents or Poincaré sections) that varying this single parameter produces a transition to chaos whose statistics match observed excess volatility, rather than the chaos measure reducing to a fitted function of the risk-aversion parameter by construction.

Authors: The current manuscript reports numerical trajectories that become increasingly irregular as the risk-aversion parameter is raised, but we accept that a more quantitative characterization is required. In the revision we will compute and plot the largest Lyapunov exponent as a function of the risk-aversion parameter, include representative Poincaré sections, and compare the resulting price-return statistics (kurtosis, volatility clustering measures) against empirical benchmarks for excess volatility. These additions will demonstrate that the transition to chaos and the associated volatility statistics emerge from the deterministic dynamics rather than from direct fitting of the chaos indicator to the parameter. revision: yes

Circularity Check

No circularity: Hamiltonian model is an explicit ansatz whose chaotic regime is derived from the posited equations rather than fitted inputs

full rationale

The paper constructs a closed Hamiltonian system with price and inventory as anharmonic oscillators under nonlinear coupling, treating risk aversion as a free parameter that modulates the degree of chaos. The claim that external noise is unnecessary follows directly from integrating the deterministic equations of motion; no step reduces a prediction to a fitted value by construction, nor does any load-bearing premise rest on a self-citation chain. The modeling choice is stated as such and does not smuggle an ansatz via prior work or rename an empirical pattern. The derivation therefore remains self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

free parameters (1)

- risk appetite parameter

axioms (1)

- domain assumption Market price and market makers' inventory behave as anharmonic oscillators with nonlinear coupling.

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

We start with the concept of a linear restoring force pulling the traded price x back to the equilibrium price x0: H(x,Px)=Px²/2Mx + Kx(x−x0)²/2 ... + ε(xv)²/2 + f(v)

-

IndisputableMonolith/Foundation/BranchSelection.leanbranch_selection unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

For a sufficiently small perturbation ε, the Hamiltonian can be written ... + ε IxIv / 2KxKv + O(ε²) ... breakdown of periodic motion and the onset of chaos

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Vasicek, O: An Equilibrium characterization of the term structure.Journal of Financial Economics, 5:177-178, 1977

work page 1977

-

[2]

Cambridge University Press, 2018, ISBN:978-1- 107-15605-0

Donier, J,; Bouchaud, J-P,; Bonart, J,; Gould, M:Trades Quotes and Financial Markets Under The Microscope. Cambridge University Press, 2018, ISBN:978-1- 107-15605-0

work page 2018

-

[3]

Cutler D.M, Poterba J.M, Summers L.H:“What Moves Stock Prices?”, The Journal of Portfolio Management, 15(3)pp 4-12

-

[4]

What Moves Stock Prices? Another Look

Cornell B: “What Moves Stock Prices? Another Look”, The Journal of Portfolio Management, 39(3)pp 32-38, 2013

work page 2013

-

[5]

Arnold:Mathematical Methods of Classical Mechanics, Springer Graduate Texts in Mathematics, 1988 17

V .I. Arnold:Mathematical Methods of Classical Mechanics, Springer Graduate Texts in Mathematics, 1988 17

work page 1988

-

[6]

G. Matinyan, G. K. Sawidi, and N. G. Ter-Arutyunyan-Sawid: Classical Yang-Mills Mechanics: Nonlinear Color Oscillations,Journal of Experimental and Theoretical Physics, V ol. 53, Issue 3, p.421S

-

[7]

Matinyan, Berndt M ¨uller: Adventures of the Coupled Yang-Mills Oscillators: I

Sergei G. Matinyan, Berndt M ¨uller: Adventures of the Coupled Yang-Mills Oscillators: I. Semiclassical Expansion,Journal of Physics A, 2006

work page 2006

-

[8]

Matinyan, Berndt M ¨uller: Adventures of the coupled Yang–Mills oscillators

Sergei G. Matinyan, Berndt M ¨uller: Adventures of the coupled Yang–Mills oscillators. II: YM–Higgs quantum mechanics,Journal of Physics A, 2006

work page 2006

- [9]

-

[10]

J. M. Sanz-Serna: Symplectic Integrators for Hamiltonian Problems: An Overview, Acta Numerica, 1991 pp 243-286

work page 1991

-

[11]

Information Entropy of the Financial Market: Modelling Random Processes Using Open Quantum Systems

Hicks, W: “Information Entropy of the Financial Market: Modelling Random Processes Using Open Quantum Systems”.Quantum Economics and Finance (2024) https://doi.org/10.1177/29767032241279990

-

[12]

Available at: https://arxiv.org/abs/2505.01284

Hicks, W: Modelling Financial Markets using Open Quantum Systems. Available at: https://arxiv.org/abs/2505.01284

-

[13]

Louis N. Hand and Janet D. Finch:Analytical Mechanics, Cambridge University Press, 1998

work page 1998

- [14]

-

[15]

Beyer:CRC Standard Mathematical Tables, 28th ed, CRC Press, 1987

W.H. Beyer:CRC Standard Mathematical Tables, 28th ed, CRC Press, 1987

work page 1987

-

[16]

Ornstein D.S, Shields P.C: The Classification of Bernoulli Flows of Infinite Entropy, Advances in Mathematics, 10(1), pp143-146, 1973

work page 1973

-

[17]

Pesin Y ,B: Characteristic Lyapunov Exponents and Smooth Ergodic Theory, Russian Mathematical Surveys, 32(4), pp 55-114, 1977

work page 1977

-

[18]

Chandre C: pyHamSys, Python Hamiltonian Systems (Version 0.9). Github. https://github.com/cchandre/pyhamsys

-

[19]

Mauger F, Chandre C: Extended phase-space symplectic integration for election dynamics,Phys. Rev. E, 113, DOI: https://doi.org/10.1103/7ghc-htf8, 2026 18

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.