Misspecified Estimate-then-Optimize Leads to Supra-Competitive Prices

Pith reviewed 2026-06-30 19:13 UTC · model grok-4.3

The pith

Misspecified estimate-then-optimize pricing leads to supra-competitive prices above the Nash equilibrium when firms explore similar price ranges.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

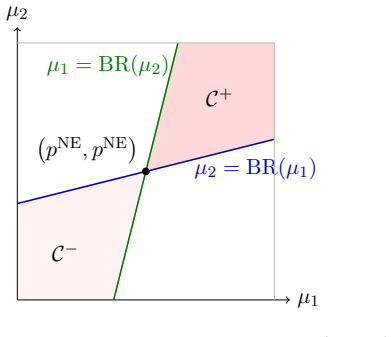

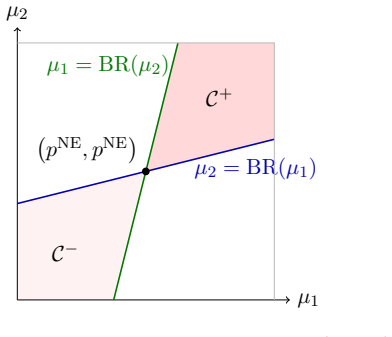

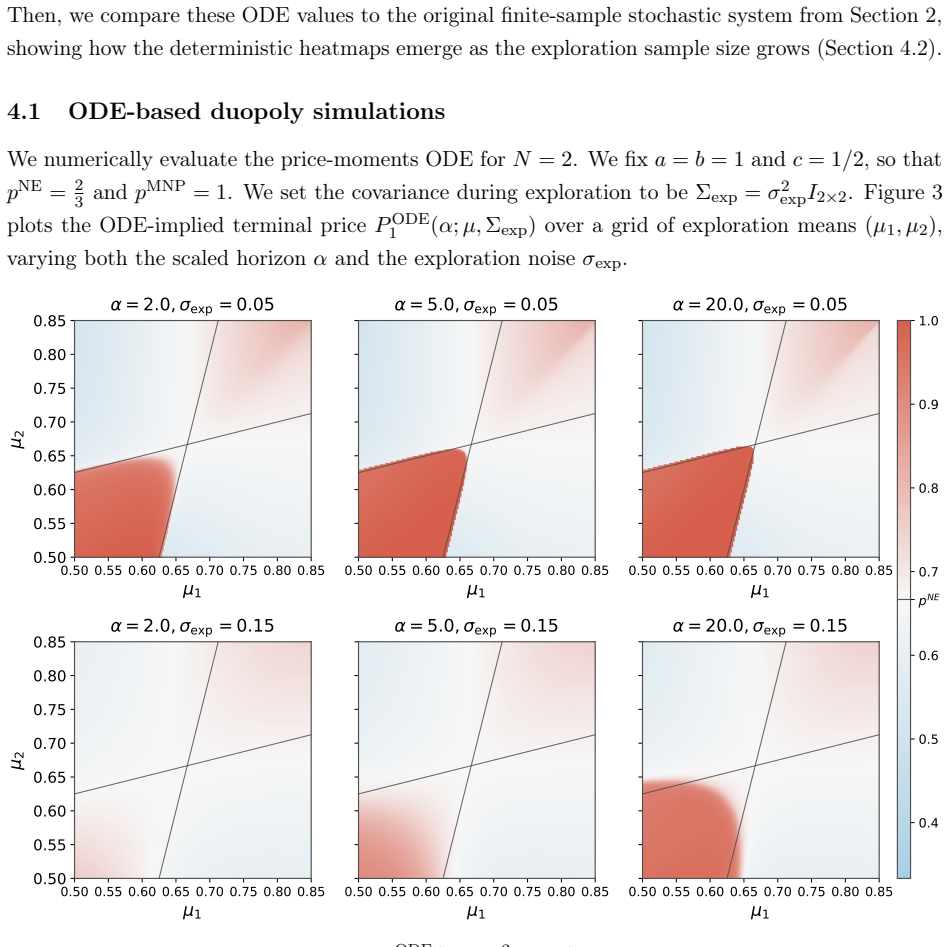

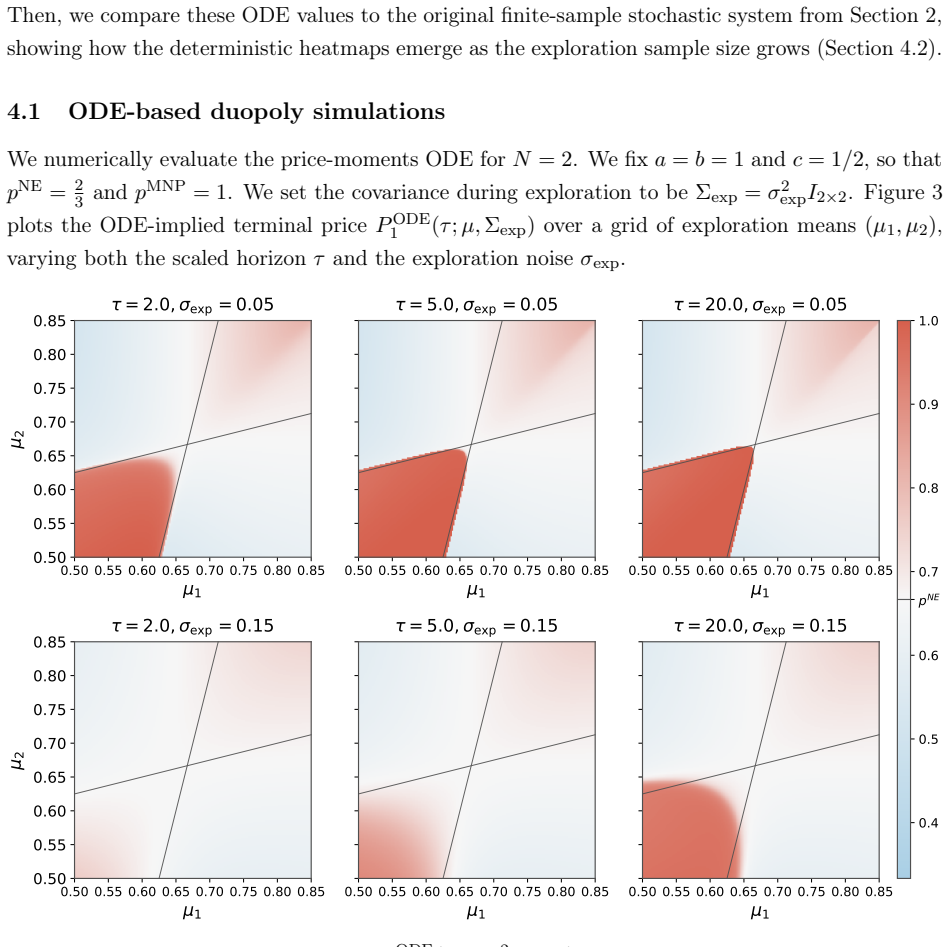

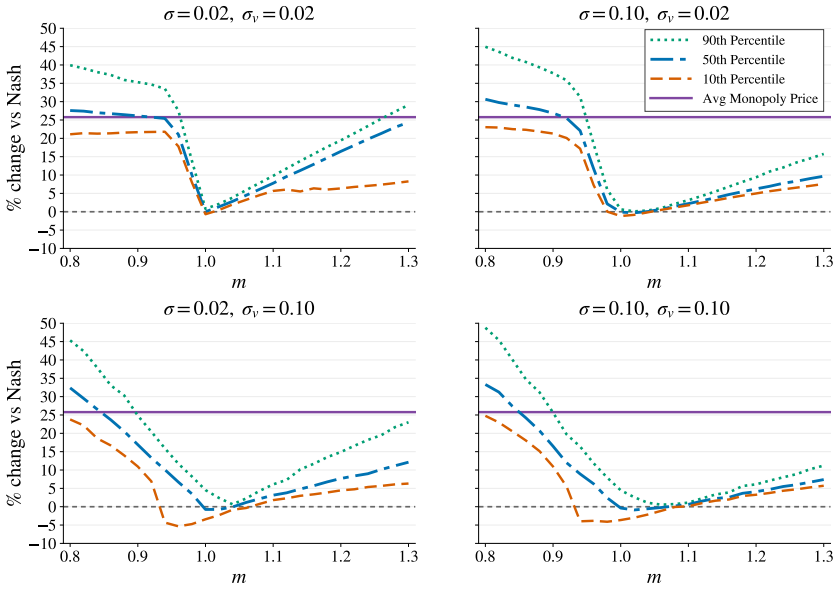

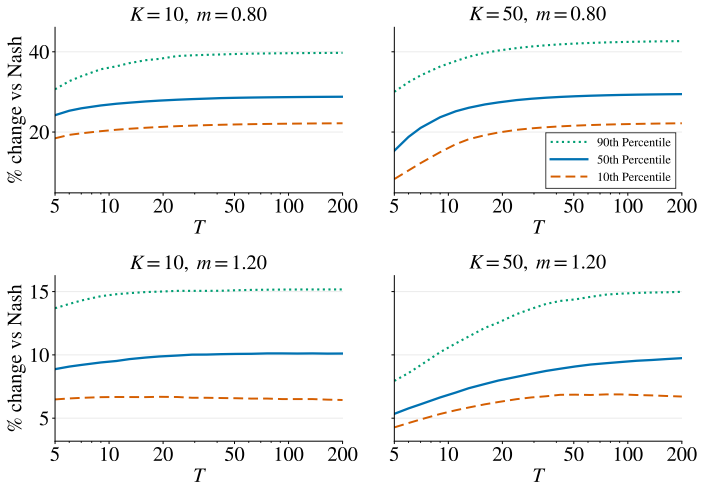

When firms apply a myopic estimate-then-optimize rule with a demand model that omits competitors' prices, and the system is initialized by independent random price explorations in similar ranges on the same side of the Nash price, the prices converge to levels above the Nash equilibrium, potentially reaching monopoly prices under symmetric exploration, as characterized by the fluid-limit ODE analysis.

What carries the argument

The fluid-limit ordinary differential equation that governs the price trajectory under repeated misspecified estimation and optimization.

If this is right

- Supra-competitive prices arise when firms initially explore within similar price ranges on the same side of the Nash price.

- Prices can reach monopoly levels under symmetric exploration.

- Supra-competitive outcomes arise robustly in simulations beyond theoretical assumptions, including under finite horizons, heterogeneous products, and nonlinear logit demand.

Where Pith is reading between the lines

- If the exploration phase covers ranges on opposite sides of the Nash price, prices may instead converge to the Nash level.

- Markets where firms rely on own-history data without competitor variables could sustain elevated prices even without explicit coordination.

- Adding competitor prices to the fitted demand model would likely eliminate the supra-competitive convergence path shown in the fluid limit.

Load-bearing premise

The demand model fitted by each firm omits competitors' prices, and the outcome depends on the specific ranges of the initial independent random price explorations.

What would settle it

Running the pricing dynamics with initial explorations on opposite sides of the Nash price and checking whether prices converge to the Nash equilibrium rather than above it.

Figures

read the original abstract

We study whether simple algorithmic pricing systems can systematically produce collusive-like prices in multi-firm markets. We consider firms that price using a myopic estimate-then-optimize rule: each repeatedly fits a demand model to its own price and sales history and sets the price that maximizes estimated profit. This demand model is misspecified, omitting competitors' prices. We analyze the dynamics of this rule when it is initialized by an exploration phase of independent random prices. We characterize when this pipeline converges to supra-competitive prices above the Nash equilibrium, via a fluid-limit ordinary differential equation analysis. We show that supra-competitive prices arise when firms initially explore within similar price ranges on the same side of the Nash price. Moreover, prices can be substantially above the Nash price; we show that prices can reach monopoly levels under symmetric exploration. Simulations calibrated to a real multifamily rental market confirm that supra-competitive outcomes arise robustly beyond our theoretical assumptions, including under finite horizons, heterogeneous products, and nonlinear logit demand.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies firms that repeatedly fit a misspecified demand model (omitting competitors' prices) to their own price-sales history and myopically optimize estimated profit. Initialized by an independent random-price exploration phase, the dynamics are analyzed via a fluid-limit ODE whose attractors determine long-run prices. The central claim is that supra-competitive prices (including monopoly levels under symmetric exploration) arise when firms explore in similar ranges on the same side of the Nash price; calibrated simulations are said to confirm robustness beyond the ODE assumptions.

Significance. If the ODE characterization and its simulation validation hold, the work identifies a concrete, non-collusive mechanism by which simple algorithmic pricing can produce supra-competitive outcomes in oligopoly. The fluid-limit approach ties outcomes to initial exploration distributions in a falsifiable way, and the use of real-market calibration strengthens applicability. This is relevant to algorithmic collusion debates and market-design questions.

major comments (2)

- [Fluid-limit ODE analysis] Fluid-limit ODE section: the claim that the ODE attractors characterize the discrete stochastic process rests on the approximation that estimation noise vanishes and new observations track the continuous trajectory. Because prices are chosen endogenously from the current estimate, the data-generating process is not exogenous; it is unclear whether finite-sample variance or path dependence can cause escape from the predicted basins. The abstract invokes simulations for robustness, but this does not substitute for a direct argument or numerical check that the discrete algorithm converges to the ODE equilibria rather than other limits.

- [Simulation section] Simulation calibration and validation: the abstract states that simulations confirm supra-competitive outcomes under finite horizons, heterogeneous products, and logit demand, yet no information is given on the number of Monte Carlo replications, how initial exploration ranges are sampled in finite samples, or whether the realized long-run prices match the specific ODE attractors (as opposed to merely exceeding Nash). Without these details the simulations cannot be assessed as confirming the ODE characterization.

minor comments (1)

- [Introduction] The introduction could more explicitly contrast the misspecification (omission of rivals' prices) with standard Bertrand-Nash assumptions to clarify the source of the bias.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive comments. We address each major comment below and describe the revisions that will be made to strengthen the manuscript.

read point-by-point responses

-

Referee: [Fluid-limit ODE analysis] Fluid-limit ODE section: the claim that the ODE attractors characterize the discrete stochastic process rests on the approximation that estimation noise vanishes and new observations track the continuous trajectory. Because prices are chosen endogenously from the current estimate, the data-generating process is not exogenous; it is unclear whether finite-sample variance or path dependence can cause escape from the predicted basins. The abstract invokes simulations for robustness, but this does not substitute for a direct argument or numerical check that the discrete algorithm converges to the ODE equilibria rather than other limits.

Authors: We agree that the link between the fluid-limit ODE and the discrete process merits a more explicit justification, especially given the endogenous data generation. In the revision we will add a dedicated subsection that invokes standard results from stochastic approximation theory to delineate the conditions under which the ODE attractors govern the long-run behavior. We will also include new numerical experiments that run the exact discrete algorithm alongside the ODE trajectory and report the frequency with which the discrete process reaches the predicted basins rather than escaping. revision: yes

-

Referee: [Simulation section] Simulation calibration and validation: the abstract states that simulations confirm supra-competitive outcomes under finite horizons, heterogeneous products, and logit demand, yet no information is given on the number of Monte Carlo replications, how initial exploration ranges are sampled in finite samples, or whether the realized long-run prices match the specific ODE attractors (as opposed to merely exceeding Nash). Without these details the simulations cannot be assessed as confirming the ODE characterization.

Authors: We accept that the simulation section lacks the necessary methodological detail. The revised manuscript will report the exact number of Monte Carlo replications, describe the precise sampling distribution used for initial exploration ranges, and add quantitative comparisons (e.g., tables or histograms) showing that the empirical terminal prices align with the specific ODE equilibria rather than merely lying above the Nash price. revision: yes

Circularity Check

No circularity: fluid-limit ODE derives from stated misspecified dynamics

full rationale

The paper's central result characterizes convergence of the estimate-then-optimize process to supra-competitive prices via a fluid-limit ODE whose trajectories and attractors are obtained directly from the myopic pricing rule applied to the misspecified demand model and the initial exploration distribution. This is a standard mean-field approximation of the discrete stochastic updates and does not reduce any claimed prediction to a fitted parameter or self-citation by construction. The ODE is not obtained by renaming a known result or smuggling an ansatz; the attractors emerge from solving the derived differential equation under the given misspecification. No load-bearing step relies on prior self-citations whose content is unverified or tautological. The derivation remains self-contained against the paper's own model equations.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Demand model omits competitors' prices

Forward citations

Cited by 1 Pith paper

-

Should Demand Models Incorporate Competitor Prices? Oblivious Learning and Algorithmic Collusion

In stylized competitive markets with noisy demand and iterated least squares learning, oblivious demand models yield transient collusive patterns that dissipate under sufficient exploration, informed sellers strictly ...

Reference graph

Works this paper leans on

-

[1]

I. Abada and X. Lambin. Artificial intelligence: Can seemingly collusive outcomes be avoided? Management Science, 69 0 (9): 0 5042--5065, 2023. doi:10.1287/mnsc.2022.4623

-

[2]

I. Abada, X. Lambin, and N. Tchakarov. Collusion by mistake: Does algorithmic sophistication drive supra-competitive profits? European Journal of Operational Research, 318 0 (3): 0 927--953, 2024. doi:10.1016/j.ejor.2024.06.006

-

[3]

A. Aouad and A. V. den Boer. Algorithmic collusion in assortment games. Available at SSRN 3930364 , 2021. doi:10.2139/ssrn.3930364. URL https://ssrn.com/abstract=3930364

-

[4]

E. R. Arunachaleswaran, N. Collina, S. Kannan, A. Roth, and J. Ziani. Algorithmic collusion without threats. In R. Meka, editor, 16th Innovations in Theoretical Computer Science Conference ( ITCS 2025) , volume 325 of Leibniz International Proceedings in Informatics ( LIPIcs ) , pages 10:1--10:21, Dagstuhl, Germany, 2025. Schloss Dagstuhl -- Leibniz-Zentr...

-

[5]

J. Asker, C. Fershtman, and A. Pakes. Artificial intelligence, algorithm design, and pricing. AEA Papers and Proceedings , 112: 0 452--456, 2022. doi:10.1257/pandp.20221059

-

[6]

S. Assad, R. Clark, D. Ershov, and L. Xu. Algorithmic pricing and competition: Empirical evidence from the German retail gasoline market. Journal of Political Economy, 132 0 (3): 0 723--771, 2024. doi:10.1086/726906

-

[7]

Aviv and A

Y. Aviv and A. Pazgal. Pricing of short life-cycle products through active learning. Working paper, Olin School of Business, Washington University in St. Louis, 2002

2002

-

[8]

arXiv preprint arXiv:2202.05946 , year=

M. Banchio and G. Mantegazza. Artificial intelligence and spontaneous collusion. arXiv preprint arXiv :2202.05946 , 2022. URL https://arxiv.org/abs/2202.05946

-

[9]

M. Bichler, J. Durmann, and M. Oberlechner. Online optimization algorithms in repeated price competition: Equilibrium learning and algorithmic collusion, 2024. URL https://arxiv.org/abs/2412.15707

-

[10]

Z. Y. Brown and A. MacKay. Competition in pricing algorithms. American Economic Journal: Microeconomics, 15 0 (2): 0 109--156, 2023. doi:10.1257/mic.20210158

-

[11]

S. Calder-Wang and G. H. Kim. Algorithmic pricing in multifamily rentals: Efficiency gains or price coordination? Available at SSRN 4403058 , 2024. doi:10.2139/ssrn.4403058. URL https://ssrn.com/abstract=4403058

-

[12]

E. Calvano, G. Calzolari, V. Denicol \`o , and S. Pastorello. Artificial intelligence, algorithmic pricing, and collusion. American Economic Review, 110 0 (10): 0 3267--3297, 2020. doi:10.1257/aer.20190623

-

[13]

L. Chen, A. Mislove, and C. Wilson. An empirical analysis of algorithmic pricing on Amazon Marketplace . In Proceedings of the 25th International Conference on World Wide Web , pages 1339--1349, 2016. doi:10.1145/2872427.2883089

-

[14]

W. L. Cooper, T. Homem-de-Mello , and A. J. Kleywegt. Learning and pricing with models that do not explicitly incorporate competition. Operations Research, 63 0 (1): 0 86--103, 2015. doi:10.1287/opre.2014.1341

-

[15]

A. V. den Boer, J. M. Meylahn, and M. P. Schinkel. Artificial collusion: Examining supracompetitive pricing by Q -learning algorithms. Amsterdam Law School Research Paper No. 2022-25; Amsterdam Center for Law & Economics Working Paper No. 2022-06; available at SSRN 4213600, 2024. URL https://ssrn.com/abstract=4213600

2022

-

[16]

C. Douglas, F. Provost, and A. Sundararajan. The illusion of collusion. arXiv preprint arXiv :2411.16574 , 2024. URL https://arxiv.org/abs/2411.16574

-

[17]

V. F. Farias and B. Van Roy. Dynamic pricing with a prior on market response. Operations Research, 58 0 (1): 0 16--29, 2010. doi:10.1287/opre.1090.0729

- [18]

-

[19]

E. J. Green and R. H. Porter. Noncooperative collusion under imperfect price information. Econometrica, 52 0 (1): 0 87--100, 1984. doi:10.2307/1911462

-

[20]

K. T. Hansen, K. Misra, and M. M. Pai. Frontiers: Algorithmic collusion: Supra-competitive prices via independent algorithms. Marketing Science, 40 0 (1): 0 1--12, 2021. doi:10.1287/mksc.2020.1276

-

[21]

M. Hettich. Algorithmic collusion: Insights from deep learning. Available at SSRN 3785966 , 2021. doi:10.2139/ssrn.3785966. URL https://ssrn.com/abstract=3785966

-

[22]

J. Keppo, Y. Li, G. Tsoukalas, and N. Yuan. AI pricing, agent heterogeneity, and collusion. Available at SSRN 5386338 , 2025. doi:10.2139/ssrn.5386338. URL https://ssrn.com/abstract=5386338

-

[23]

A. P. Kirman. Learning by firms about demand conditions. In R. H. Day and T. Groves, editors, Adaptive Economic Models, pages 137--156. Academic Press, New York, 1975

1975

-

[24]

A. P. Kirman. On mistaken beliefs and resultant equilibria. In R. Frydman and E. S. Phelps, editors, Individual Forecasting and Aggregate Outcomes: ``Rational Expectations'' Examined, pages 147--168. Cambridge University Press, Cambridge, 1986

1986

-

[25]

A. P. Kirman. Learning in oligopoly: Theory, simulation, and experimental evidence. In A. P. Kirman and M. Salmon, editors, Learning and Rationality in Economics, pages 127--178. B. Blackwell, Oxford, UK and Cambridge, MA, 1995

1995

-

[26]

T. Klein. Autonomous algorithmic collusion: Q -learning under sequential pricing. The RAND Journal of Economics , 52 0 (3): 0 538--558, 2021. doi:10.1111/1756-2171.12383

-

[27]

M. A. Lariviere and E. L. Porteus. Stalking information: Bayesian inventory management with unobserved lost sales. Management Science, 45 0 (3): 0 346--363, 1999. doi:10.1287/mnsc.45.3.346

-

[28]

B. Light and W. Wang. Conjectural variations in competitive dynamic pricing: A learning foundation via experimentation design and feedback structure, 2026. URL https://arxiv.org/abs/2602.12888

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[29]

Lin and \"O

M. Lin and \"O . Sar ta c . Competition in pricing algorithms: Stability, exploration, and supracompetitive outcomes. Available at SSRN 5958355, December 2025. URL https://ssrn.com/abstract=5958355

2025

-

[30]

T. Loots and A. V. den Boer. Data-driven collusion and competition in a pricing duopoly with multinomial logit demand. Production and Operations Management, 32 0 (4): 0 1169--1186, 2023. doi:10.1111/poms.13919

-

[31]

E. Maskin and J. Tirole. A theory of dynamic oligopoly, II : Price competition, kinked demand curves, and edgeworth cycles. Econometrica, 56 0 (3): 0 571--599, 1988. doi:10.2307/1911701

-

[32]

J. M. Meylahn and A. V. den Boer. Learning to collude in a pricing duopoly. Manufacturing & Service Operations Management, 24 0 (5): 0 2577--2594, 2022. doi:10.1287/msom.2021.1074

-

[33]

Robinson

J. Robinson. An iterative method of solving a game. Annals of Mathematics, 54 0 (2): 0 296--301, 1951

1951

-

[34]

H. A. Simon. Dynamic programming under uncertainty with a quadratic criterion function. Econometrica, 24 0 (1): 0 74--81, 1956

1956

-

[35]

R. S. Sutton and A. G. Barto. Reinforcement Learning: An Introduction. MIT Press, Cambridge, MA, 1998

1998

-

[36]

Z. Yang, X. Lei, and P. Gao. Regulating discriminatory pricing in the presence of tacit collusion. Available at SSRN 4633784 , 2023. doi:10.2139/ssrn.4633784. URL https://ssrn.com/abstract=4633784

-

[37]

Z. Yang, P. Gao, and Z. Wang. Driven to collusion: Competitive pricing under independent demand model and price imitation, 2026. URL https://ssrn.com/abstract=6197578. Available at SSRN 6197578

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.