Explicit Rational Formulae for Bachelier (Normal) Implied Volatility

Pith reviewed 2026-05-19 23:35 UTC · model grok-4.3

The pith

Two rational formulas calculate Bachelier implied volatility directly from option price, forward, strike and expiry without iteration.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The paper claims that the two formulas LFK-2026 and LFK-2026C recover the normal volatility parameter from the Bachelier price formula by means of rational functions alone, employing the absolute forward-strike difference over tail time value near the money and a direct rational fit to reciprocal absolute standardized moneyness in the tails, thereby eliminating any iterative root search.

What carries the argument

Branch-structured rational approximation that replaces the logarithm with the absolute forward-strike difference divided by tail time value near the money and approximates reciprocal absolute standardized moneyness directly in the far tail.

If this is right

- Pricing and risk systems can obtain normal implied volatility in constant time without convergence failures from iterative solvers.

- The formulas remain accurate for deep out-of-the-money options and very short expiries where iterative methods can struggle.

- LFK-2026C delivers faster scalar execution on typical hardware while preserving the same accuracy level as the accuracy-oriented version.

- Direct embedding into calibration loops becomes possible without added numerical overhead or safeguards.

Where Pith is reading between the lines

- The branch-rational approach may adapt to implied-volatility inversion for other one-dimensional diffusion models.

- Machine-precision accuracy supports repeated volatility extraction inside high-frequency risk engines without accumulation of round-off error.

- Elimination of special-function calls in the near-money region could reduce latency in embedded or low-precision financial hardware.

Load-bearing premise

The chosen rational branch structure and tail approximation for reciprocal absolute standardized moneyness remain accurate enough across all relevant moneyness and time-to-expiry regimes that the overall error stays near machine precision.

What would settle it

A numerical test in which the Bachelier pricing formula evaluated at the volatility returned by either rational formula produces an option price that differs from the input price by more than a few units in the last place for some strike, forward and expiry combination.

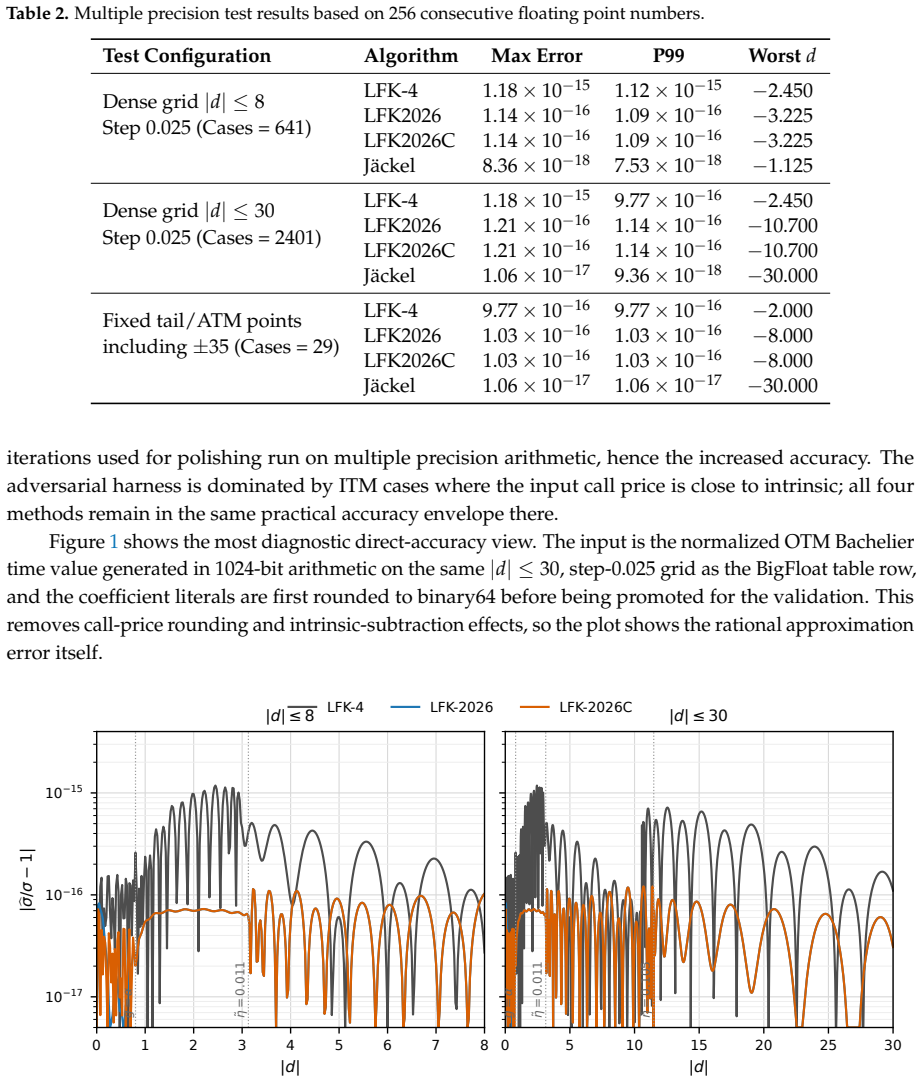

Figures

read the original abstract

We present two explicit rational formulae for Bachelier, or normal, implied volatility. The formulae take the option price, forward, strike, and expiry as inputs and return the implied normal volatility without iteration. They follow the branch structure of LFK-4, but use the simpler near-the-money variable given by the absolute forward-strike difference divided by the tail time value, avoiding a logarithm and a small-argument Taylor branch in that region. LFK-2026 is the accuracy-oriented formula and approximates reciprocal absolute standardized moneyness directly in the far tail. LFK-2026C keeps the same shifted out-of-the-money rational tail approximation, but splits the near-the-money branch into a very small low- \(u\) rational and a mid-range rational. In double precision tests both remain close to machine accuracy, while LFK-2026C is the faster scalar implementation on the current benchmark mix

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper presents two explicit rational formulae (LFK-2026 and LFK-2026C) for Bachelier/normal implied volatility. The inputs are option price, forward, strike and expiry; the output is the implied normal volatility without iteration. The constructions follow the LFK-4 branch structure but replace the near-the-money variable with the simpler |F-K| divided by tail time value, avoiding a logarithm and small-argument Taylor branch. LFK-2026 approximates reciprocal absolute standardized moneyness directly in the far tail; LFK-2026C retains the same tail form but splits the near-the-money region into a very-small-u rational and a mid-range rational. Double-precision tests are reported to reach near machine accuracy, with LFK-2026C faster on the benchmark mix.

Significance. If the accuracy claims are substantiated, the formulae would supply fast, non-iterative, rational-function implementations of normal implied volatility. Such explicit inversions are useful in computational finance for repeated pricing, calibration and risk calculations under the normal model, where iterative solvers are undesirable.

major comments (2)

- Abstract: the claim that 'in double precision tests both remain close to machine accuracy' is unsupported by any error tables, coefficient values, test-grid description, or exclusion rules. Without these the central accuracy claim cannot be verified and is load-bearing for the paper's contribution.

- Tail approximation section (implied by the description of LFK-2026): the rational fit to 1/|d| for reciprocal absolute standardized moneyness lacks an independent a-priori error bound or exhaustive regime coverage (T ≪ 1, |F-K|/(σ√T) ≫ 10, or exact branch-transition points). Because the underlying Bachelier map is transcendental, any untested corner can produce relative errors exceeding 1e-15 even if average-case results appear good.

minor comments (2)

- The abstract introduces 'tail time value' without an explicit definition or equation reference; a one-line definition would improve readability.

- The paper should state whether the rational coefficients were obtained by fitting on the same data later used for validation, to address potential circularity concerns.

Simulated Author's Rebuttal

We thank the referee for their thorough review and valuable comments on our manuscript. We address each of the major comments below and indicate the revisions we will make to strengthen the paper.

read point-by-point responses

-

Referee: Abstract: the claim that 'in double precision tests both remain close to machine accuracy' is unsupported by any error tables, coefficient values, test-grid description, or exclusion rules. Without these the central accuracy claim cannot be verified and is load-bearing for the paper's contribution.

Authors: We agree that the abstract's accuracy claim needs to be supported by explicit documentation to allow independent verification. In the revised manuscript, we will expand the numerical results section to include detailed error tables reporting the maximum, mean, and median relative errors for both formulae across the test cases. We will also list the rational coefficients explicitly, provide a full description of the test grid (including ranges for T from 10^{-8} to 100, standardized moneyness from 0 to 100, and other parameters), and clarify any exclusion criteria for degenerate cases such as zero time value. These additions will substantiate the near-machine-accuracy performance in double precision. revision: yes

-

Referee: Tail approximation section (implied by the description of LFK-2026): the rational fit to 1/|d| for reciprocal absolute standardized moneyness lacks an independent a-priori error bound or exhaustive regime coverage (T ≪ 1, |F-K|/(σ√T) ≫ 10, or exact branch-transition points). Because the underlying Bachelier map is transcendental, any untested corner can produce relative errors exceeding 1e-15 even if average-case results appear good.

Authors: We appreciate the referee's point regarding the need for more rigorous validation of the tail approximation. While our current tests include regimes with small T and large |F-K|/(σ√T), we acknowledge that a more exhaustive coverage and explicit branch points would improve the manuscript. In the revision, we will add a new subsection detailing the maximum observed relative errors in the far-tail regime for T ≪ 1 and |F-K|/(σ√T) ≫ 10, specify the exact transition points between the near-the-money and tail branches, and include plots or tables demonstrating coverage. An independent a-priori error bound is challenging to derive for this transcendental inversion without additional analysis; however, we will provide a conservative empirical bound based on the tested regimes and the properties of the rational approximant. revision: partial

Circularity Check

Minor self-citation to prior branch structure; central explicit formulae remain independent

specific steps

-

self citation load bearing

[Abstract]

"They follow the branch structure of LFK-4, but use the simpler near-the-money variable given by the absolute forward-strike difference divided by the tail time value, avoiding a logarithm and a small-argument Taylor branch in that region."

The foundational branch structure is imported from LFK-4 (prior work sharing the LFK author prefix), so the organizational skeleton of the derivation is self-referential even though the concrete variable choice and rational coefficients are novel.

full rationale

The paper constructs and presents two new explicit rational approximations (LFK-2026 and LFK-2026C) for Bachelier implied volatility using a chosen near-the-money variable and tail rational fit. It references LFK-4 only for the overall branch structure while introducing a simpler variable and specific rational forms. This self-citation is not load-bearing for the central result, which consists of the new formulae and their reported numerical accuracy. No step reduces the output formulae to a tautological fit or self-definition by construction; the approximations are offered as practical explicit alternatives with independent validation tests.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

LFK-2026 uses the no-log ITM variable u = z/(1-z) = m/cotm. For g>alpha it uses a P10/Q9 rational: sigma = (m + cotm)/sqrt(T) * R10,9(u; a26I, b26I). In the OTM branch it approximates 1/|d| directly.

-

IndisputableMonolith/Foundation/BranchSelection.leanbranch_selection unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The formulae follow the branch structure of LFK-4 but use the simpler near-the-money variable given by the absolute forward-strike difference divided by the tail time value.

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Théorie de la spéculation.Annales Scientifiques de l’École Normale Supérieure1900,17, 21–86

Bachelier, L. Théorie de la spéculation.Annales Scientifiques de l’École Normale Supérieure1900,17, 21–86

-

[2]

Fast and Accurate Analytic Basis Point Volatility

Le Floc’h, F. Fast and Accurate Analytic Basis Point Volatility. Available online: https://ssrn.com/abstract=2420 757 (accessed on 17 May 2026)

work page 2026

-

[3]

Patel, J.; Russo, V .; Fabozzi, F.J. Using the Right Implied Volatility Quotes in Times of Low Interest Rates: An Empirical Analysis across Different Currencies.Finance Research Letters2018,25, 196–201. https://doi.org/10.1016/j.frl.2017.10.013

-

[4]

Switch to Bachelier Options Pricing Model—Effective April 22, 2020

CME Clearing. Switch to Bachelier Options Pricing Model—Effective April 22, 2020. CME Clearing Advisory 20-171, 21 April 2020. Available online: https://www.cmegroup.com/notices/clearing/2020/04/Chadv20-171. html (accessed on 18 May 2026)

work page 2020

-

[5]

A Black–Scholes User’s Guide to the Bachelier Model.Journal of Futures Markets2022,42, 959–980

Choi, J.; Kwak, M.; Tee, C.W.; Wang, Y. A Black–Scholes User’s Guide to the Bachelier Model.Journal of Futures Markets2022,42, 959–980. https://doi.org/10.1002/fut.22315

-

[6]

Choi, J.; Kim, K.; Kwak, M. Numerical Approximation of the Implied Volatility under Arithmetic Brownian Motion.Applied Mathematical Finance2009,16, 261–268

-

[7]

https://doi.org/10.1002/wilm.10395

Jäckel, P . Let’s Be Rational.Wilmott2017,2015, 40–53. https://doi.org/10.1002/wilm.10395

-

[8]

QuantLib: A Free/Open-Source Library for Quantitative Finance

QuantLib Project. QuantLib: A Free/Open-Source Library for Quantitative Finance. Available online: https: //www.quantlib.org/ (accessed on 18 May 2026). 7

work page 2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.