The Statistical Significance of the Inclusion of Graph Neural Networks in the Financial Time Series Forecasting Problem

Pith reviewed 2026-05-21 01:23 UTC · model grok-4.3

The pith

Including Graph Neural Networks to capture geometric patterns leads to statistically significant improvements in financial time series forecasting.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

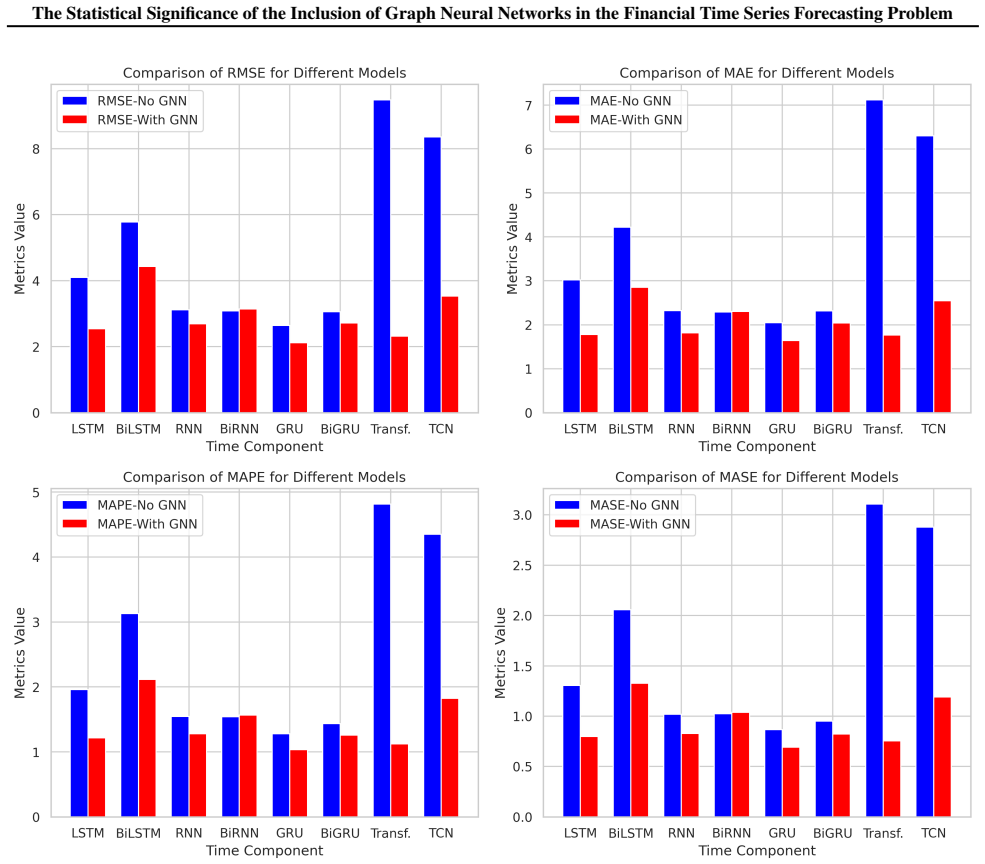

The authors introduce the Time-Geometric model as a combination of models that exploit both geometric and temporal patterns in univariate financial time series. Through empirical evaluations, they demonstrate that leveraging geometric patterns captured through Graph Neural Networks yields statistically significant improvements in forecasting accuracy over models relying solely on temporal patterns.

What carries the argument

The Time-Geometric model, which integrates Graph Neural Networks to extract geometric patterns in addition to standard temporal analysis.

If this is right

- Standard temporal models can be enhanced by incorporating geometric patterns from GNNs.

- The improvements in accuracy are statistically significant rather than due to chance.

- Geometric patterns provide complementary information to temporal patterns in financial data.

- Extensive empirical evaluations support the inclusion of such geometric components.

Where Pith is reading between the lines

- This could encourage exploring graph-based representations for other types of sequential data beyond finance.

- Researchers might investigate how to best construct the graphs that GNNs operate on for time series.

- Similar combinations could be tested in non-financial domains like energy consumption or traffic flow prediction.

Load-bearing premise

The geometric patterns extracted by the GNN provide information that is independent from the temporal patterns used by standard models.

What would settle it

Running the same experiments on the datasets used and finding that the combined model does not show statistically significant improvement over the temporal-only baseline.

Figures

read the original abstract

Forecasting univariate time series in the financial market is a challenging endeavor. While numerous statistical and machine learning models have been introduced to address this challenge, they typically concentrate solely on analyzing temporal patterns within the time series data. In this research, we study the statistical significance of the inclusion of geometric patterns in enhancing forecasting accuracy within the context of time series analysis. We introduce the Time-Geometric model, a combination of models designed to exploit both geometric and temporal patterns. The contribution of this research lies in advancing the domain of univariate time series prediction,as demonstrated through extensive empirical evaluations. Our findings underscore that leveraging geometric patterns, captured through Graph Neural Networks, yields statistically significant improvements in forecasting accuracy.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript claims that a Time-Geometric model, which combines temporal patterns with geometric patterns captured via Graph Neural Networks, produces statistically significant improvements in accuracy for univariate financial time series forecasting, as shown by extensive empirical evaluations.

Significance. If the empirical results hold, the work would be significant for financial time series forecasting by indicating that GNN-derived geometric patterns supply predictive information beyond standard temporal models.

major comments (1)

- [Abstract] Abstract: The central claim that leveraging geometric patterns captured through Graph Neural Networks yields statistically significant improvements is unsupported by any experimental details. The abstract supplies no information on the temporal baseline models, datasets or assets, forecasting horizons, integration method for the GNN component, loss functions, evaluation metrics, or the statistical tests (including multiplicity corrections) used to establish significance. This prevents assessment of whether the geometric patterns add independent value or whether the reported significance is valid.

minor comments (1)

- [Abstract] Abstract: missing space after comma in 'prediction,as demonstrated'.

Simulated Author's Rebuttal

We thank the referee for their constructive feedback. We address the concern regarding the abstract below and agree that revisions are needed to strengthen the presentation of our claims.

read point-by-point responses

-

Referee: [Abstract] Abstract: The central claim that leveraging geometric patterns captured through Graph Neural Networks yields statistically significant improvements is unsupported by any experimental details. The abstract supplies no information on the temporal baseline models, datasets or assets, forecasting horizons, integration method for the GNN component, loss functions, evaluation metrics, or the statistical tests (including multiplicity corrections) used to establish significance. This prevents assessment of whether the geometric patterns add independent value or whether the reported significance is valid.

Authors: We agree that the abstract is currently too concise and omits key experimental details, which limits the ability to assess the contribution of the geometric patterns and the validity of the reported significance. In the revised manuscript we will expand the abstract to include brief but specific information on the temporal baseline models, the financial datasets and assets examined, the forecasting horizons, the method used to integrate the GNN component with the temporal models, the loss functions and evaluation metrics, and the statistical tests (including any multiplicity corrections). These additions will make the central claim more transparent and allow readers to better evaluate whether the GNN-derived geometric patterns supply independent predictive value. revision: yes

Circularity Check

No circularity: abstract states empirical claim with no derivation or equations

full rationale

The available text consists solely of the abstract, which presents the work as an empirical study introducing a Time-Geometric model that combines temporal and geometric patterns (via GNNs) and reports statistically significant forecasting improvements from extensive evaluations. No equations, first-principles derivations, fitted parameters renamed as predictions, self-citations, or ansatzes are present. The central claim is framed as a data-driven finding rather than a mathematical reduction, so no load-bearing step reduces to its own inputs by construction. The derivation chain is therefore self-contained and exhibits no circularity.

Axiom & Free-Parameter Ledger

invented entities (1)

-

Time-Geometric model

no independent evidence

Lean theorems connected to this paper

-

IndisputableMonolith/Foundation/AlexanderDuality.leanalexander_duality_circle_linking unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

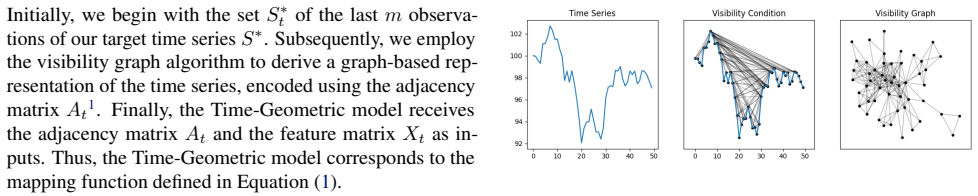

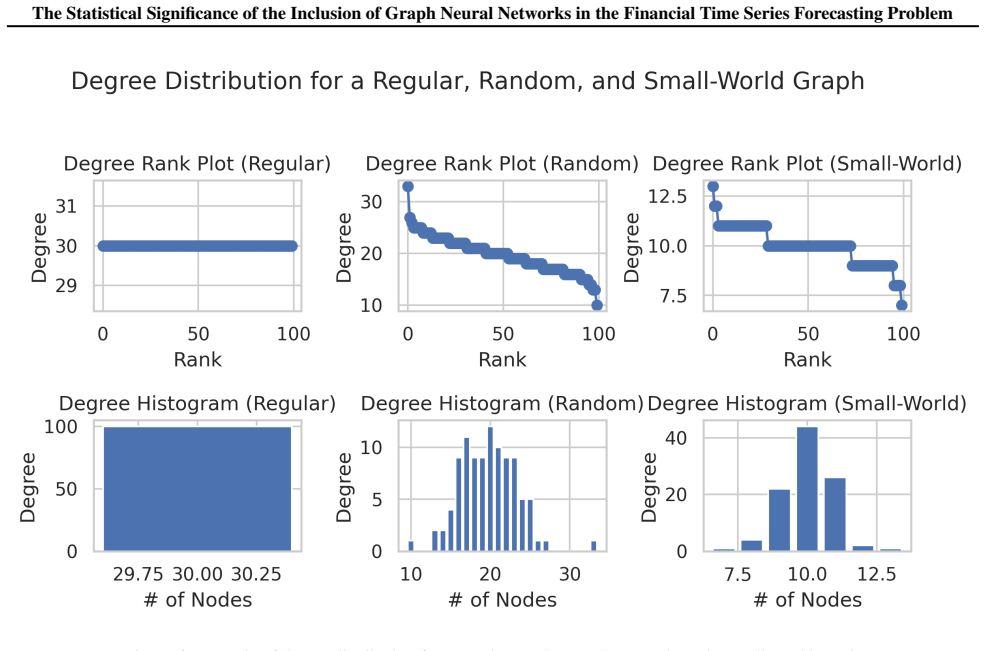

We opt for the visibility graph algorithm (Lacasa et al., 2008) to construct the graph-based representation... periodic time series transforms into a regular graph, a random time series manifests as a random graph, and a fractal time series results in a small-world graph.

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The Time-Geometric model... combines baseline time series neural network models with dynamic GNNs... H(l)_t = GNN(l)(H(l-1)_t) via message-passing

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Proceedings of the National Academy of Sciences , volume=

From time series to complex networks: The visibility graph , author=. Proceedings of the National Academy of Sciences , volume=. 2008 , publisher=

work page 2008

-

[2]

Ts2vg: Time series to visibility graphs

Carlos Bergillos , howpublished = ". Ts2vg: Time series to visibility graphs

-

[3]

Visibility Graph Based Time Series Analysis , author=. PloS One , volume=. 2015 , publisher=

work page 2015

- [4]

- [5]

-

[6]

Introduction to Stochastic Calculus Applied to Finance , author=. 2011 , publisher=

work page 2011

-

[7]

Box, George EP and Jenkins, Gwilym M and Reinsel, Gregory C and Ljung, Greta M , title=. 2015 , publisher=

work page 2015

-

[8]

Journal of Political Economy , volume=

The pricing of options and corporate liabilities , author=. Journal of Political Economy , volume=. 1973 , publisher=

work page 1973

-

[9]

Financial Modelling with Jump Processes , author=. 2003 , publisher=

work page 2003

-

[10]

Finding structure in time , author=. Cognitive Science , volume=. 1990 , publisher=

work page 1990

-

[11]

IEEE Communications Magazine , volume=

Deep learning with long short-term memory for time series prediction , author=. IEEE Communications Magazine , volume=. 2019 , publisher=

work page 2019

-

[12]

Deep Learning , author=

-

[13]

Advances in Neural Information Processing Systems , volume=

Attention is all you need , author=. Advances in Neural Information Processing Systems , volume=

-

[14]

Temporal Convolutional Networks: A Unified Approach to Action Segmentation , author=. 2016 , eprint=

work page 2016

-

[15]

Fractals and Scaling in Finance: Discontinuity, Concentration, Risk. Selecta volume E , author=. 2013 , publisher=

work page 2013

-

[16]

Fractal Market Analysis: Applying Chaos Theory to Investment and Economics , author=. 1994 , publisher=

work page 1994

-

[17]

Fractal Geometry of Financial Time Series , author=. Fractals , volume=. 1995 , publisher=

work page 1995

-

[18]

IEEE Transactions on Neural Networks , volume=

The graph neural network model , author=. IEEE Transactions on Neural Networks , volume=. 2008 , publisher=

work page 2008

-

[19]

Advances in Neural Information Processing Systems , volume=

Inductive representation learning on large graphs , author=. Advances in Neural Information Processing Systems , volume=

-

[20]

Long short-term memory , author=. Neural Computation , volume=. 1997 , publisher=

work page 1997

-

[21]

Wu, Zonghan and Pan, Shirui and Chen, Fengwen and Long, Guodong and Zhang, Chengqi and Yu, Philip S. , year=. A Comprehensive Survey on Graph Neural Networks , volume=. IEEE Transactions on Neural Networks and Learning Systems , publisher=. doi:10.1109/tnnls.2020.2978386 , number=

-

[22]

Yu, Bing and Yin, Haoteng and Zhu, Zhanxing , year=. Spatio-Temporal Graph Convolutional Networks: A Deep Learning Framework for Traffic Forecasting , url=. doi:10.24963/ijcai.2018/505 , booktitle=

-

[23]

Advances in Neural Information Processing Systems , volume=

Spectral temporal graph neural network for multivariate time-series forecasting , author=. Advances in Neural Information Processing Systems , volume=

-

[24]

IEEE TRANSACTIONS ON INTELLIGENT TRANSPORTATION SYSTEMS 21, 3848–3858

Zhao, Ling and Song, Yujiao and Zhang, Chao and Liu, Yu and Wang, Pu and Lin, Tao and Deng, Min and Li, Haifeng , year=. IEEE Transactions on Intelligent Transportation Systems , publisher=. doi:10.1109/tits.2019.2935152 , number=

-

[25]

International Conference on Learning Representations , year=

Graph Wavelet Neural Network , author=. International Conference on Learning Representations , year=

-

[26]

IEEE Transactions on Signal Processing , volume=

Gated graph recurrent neural networks , author=. IEEE Transactions on Signal Processing , volume=. 2020 , publisher=

work page 2020

-

[27]

Financial time series forecasting with multi-modality graph neural network , journal =. 2022 , issn =. doi:https://doi.org/10.1016/j.patcog.2021.108218 , url =

-

[28]

A new hybrid model for multi-step. Resources Policy , volume =. 2023 , issn =. doi:https://doi.org/10.1016/j.resourpol.2023.103956 , url =

-

[29]

Xiang, Sheng and Cheng, Dawei and Shang, Chencheng and Zhang, Ying and Liang, Yuqi , title =. 2022 , isbn =. doi:10.1145/3511808.3557089 , booktitle =

-

[30]

A Combined Model Based on Recurrent Neural Networks and Graph Convolutional Networks for Financial Time Series Forecasting , author=. Mathematics , volume=. 2023 , publisher=

work page 2023

-

[31]

Machine Learning with Applications , volume=

Rainfall prediction: A comparative analysis of modern machine learning algorithms for time-series forecasting , author=. Machine Learning with Applications , volume=. 2022 , publisher=

work page 2022

-

[32]

Journal of Healthcare Engineering , year=

Comparison of Time Series Methods and Machine Learning Algorithms for Forecasting Taiwan Blood Services Foundation's Blood Supply , author=. Journal of Healthcare Engineering , year=

-

[33]

Evaluation of statistical and machine learning models for time series prediction: Identifying the state-of-the-art and the best conditions for the use of each model , journal =. 2019 , issn =. doi:https://doi.org/10.1016/j.ins.2019.01.076 , url =

-

[34]

The Journal of Machine Learning Research , volume=

Statistical comparisons of classifiers over multiple data sets , author=. The Journal of Machine Learning Research , volume=. 2006 , publisher=

work page 2006

-

[35]

Empirical Evaluation of Gated Recurrent Neural Networks on Sequence Modeling

Empirical evaluation of gated recurrent neural networks on sequence modeling , author=. arXiv preprint arXiv:1412.3555 , year=

work page internal anchor Pith review Pith/arXiv arXiv

-

[36]

IEEE Transactions on Signal Processing , volume=

Bidirectional recurrent neural networks , author=. IEEE Transactions on Signal Processing , volume=. 1997 , publisher=

work page 1997

-

[37]

Graves, Alex and Fern. Bidirectional. International Conference on Artificial Neural Networks , pages=. 2005 , organization=

work page 2005

-

[38]

International Conference on Machine Learning , pages=

Dynamic memory networks for visual and textual question answering , author=. International Conference on Machine Learning , pages=. 2016 , organization=

work page 2016

-

[39]

Semi-Supervised Classification with Graph Convolutional Networks

Semi-supervised classification with graph convolutional networks , author=. arXiv preprint arXiv:1609.02907 , year=

work page internal anchor Pith review Pith/arXiv arXiv

-

[40]

Optuna: A next-generation hyperparameter optimization framework , author=. Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining , pages=

-

[41]

International Journal of Forecasting , volume=

Another look at measures of forecast accuracy , author=. International Journal of Forecasting , volume=. 2006 , publisher=

work page 2006

-

[42]

Adam: A Method for Stochastic Optimization

Adam: A method for stochastic optimization , author=. arXiv preprint arXiv:1412.6980 , year=

work page internal anchor Pith review Pith/arXiv arXiv

-

[43]

Journal of the American Statistical Association , volume=

The use of ranks to avoid the assumption of normality implicit in the analysis of variance , author=. Journal of the American Statistical Association , volume=. 1937 , publisher=

work page 1937

-

[44]

The Annals of Mathematical Statistics , volume=

A comparison of alternative tests of significance for the problem of m rankings , author=. The Annals of Mathematical Statistics , volume=. 1940 , publisher=

work page 1940

-

[45]

Distribution-Free Multiple Comparisons , author=. 1963 , publisher=

work page 1963

-

[46]

Data Mining and Knowledge Discovery , volume=

On comparing classifiers: Pitfalls to avoid and a recommended approach , author=. Data Mining and Knowledge Discovery , volume=. 1997 , publisher=

work page 1997

-

[47]

Handbook of Parametric and Nonparametric Statistical Procedures , author=. 2003 , publisher=

work page 2003

-

[48]

Breakthroughs in Statistics: Methodology and Distribution , pages=

Individual comparisons by ranking methods , author=. Breakthroughs in Statistics: Methodology and Distribution , pages=. 1992 , publisher=

work page 1992

-

[49]

ACM Computing Surveys , volume=

Deep learning for time series forecasting: Tutorial and literature survey , author=. ACM Computing Surveys , volume=. 2022 , publisher=

work page 2022

-

[50]

Machine Learning and Big Data Analytics Paradigms: Analysis, Applications and Challenges , pages=

A survey on deep learning for time-series forecasting , author=. Machine Learning and Big Data Analytics Paradigms: Analysis, Applications and Challenges , pages=. 2021 , publisher=

work page 2021

-

[51]

A survey on forecasting of time series data , author=. 2016 International Conference on Computing Technologies and Intelligent Data Engineering (ICCTIDE'16) , pages=. 2016 , organization=

work page 2016

- [52]

-

[53]

Investigation of market efficiency and financial stability between

Rounaghi, Mohammad Mahdi and Zadeh, Farzaneh Nassir , journal=. Investigation of market efficiency and financial stability between. 2016 , publisher=

work page 2016

- [54]

-

[55]

Stock price prediction using the

Ariyo, Adebiyi A and Adewumi, Adewumi O and Ayo, Charles K , booktitle=. Stock price prediction using the. 2014 , organization=

work page 2014

-

[56]

Econometrica: Journal of the Econometric Society , pages=

Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation , author=. Econometrica: Journal of the Econometric Society , pages=. 1982 , publisher=

work page 1982

-

[57]

Comparative study of volatility forecasting models: The case of

Lee, San K and Nguyen, LT and Sy, Malick O , journal=. Comparative study of volatility forecasting models: The case of

-

[58]

Bollerslev, Tim and Engle, Robert F and Nelson, Daniel B , journal=. 1994 , publisher=

work page 1994

-

[59]

Francq, Christian and Zakoian, Jean-Michel , year=

-

[60]

2016 IEEE International Conference on Data Science and Advanced Analytics (DSAA) , pages=

Robust online time series prediction with recurrent neural networks , author=. 2016 IEEE International Conference on Data Science and Advanced Analytics (DSAA) , pages=. 2016 , organization=

work page 2016

-

[61]

Ghosh, Achyut and Bose, Soumik and Maji, Giridhar and Debnath, Narayan and Sen, Soumya , booktitle=. Stock price prediction using

-

[62]

Chen, Chi and Xue, Lei and Xing, Wanqi , journal=. Research on Improved. 2023 , publisher=

work page 2023

-

[63]

Selvin, Sreelekshmy and Vinayakumar, R and Gopalakrishnan, EA and Menon, Vijay Krishna and Soman, KP , booktitle=. Stock price prediction using. 2017 , organization=

work page 2017

-

[64]

Roondiwala, Murtaza and Patel, Harshal and Varma, Shraddha , journal=. Predicting stock prices using

-

[65]

Stock price prediction via discovering multi-frequency trading patterns , author=. Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining , pages=

-

[66]

Ding, Qianggang and Wu, Sifan and Sun, Hao and Guo, Jiadong and Guo, Jian , booktitle =. Hierarchical Multi-Scale. 2020 , month =. doi:10.24963/ijcai.2020/640 , url =

-

[67]

Lu, Wenjie and Li, Jiazheng and Wang, Jingyang and Qin, Lele , journal=. A. 2021 , publisher=

work page 2021

-

[68]

Lin, Yuyang and Huang, Qi and Zhong, Qiyin and Li, Muyang and Li, Yan and Ma, Fei , journal=. A new attention-based. 2022 , publisher=

work page 2022

-

[69]

Network science , author=. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences , volume=. 2013 , publisher=

work page 2013

-

[70]

Proceedings of the 28th ACM SIGKDD Conference on Knowledge Discovery and Data Mining , pages=

ROLAND: graph learning framework for dynamic graphs , author=. Proceedings of the 28th ACM SIGKDD Conference on Knowledge Discovery and Data Mining , pages=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.