Hybrid News Sentiment Engine: Real-Time Market Analysis via Adaptive Ensemble Learning on News-Price Pairs

Pith reviewed 2026-06-28 07:32 UTC · model grok-4.3

The pith

Hybrid sentiment engine uses adaptive TF-IDF clusters to learn from news-price pairs without neural training or retraining

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The engine's statistical cluster learner organizes headlines into semantic neighborhoods via TF-IDF and tracks their average realized price reactions to adapt to changing market regimes without retraining, forming a novel part of the ensemble not found in existing sentiment systems.

What carries the argument

adaptive statistical TF-IDF cluster learner that organizes headlines into semantic neighborhoods and tracks average realized price reactions

If this is right

- The ensemble adjusts contributions based on each signal's historical correlation with price movements.

- The system achieves sub-second latency on CPU-only servers at effectively zero marginal cost.

- Comparisons indicate advantages over FinBERT, GPT scoring, VADER, and commercial APIs in cost, latency, accuracy, and adaptability.

- It processes 22 price-snapshot fields per news item across multiple asset classes on a continuous 3-hour cycle.

Where Pith is reading between the lines

- This could allow deployment in resource-constrained environments where neural retraining is impractical.

- If cluster stability holds, similar statistical approaches might replace parts of deep learning pipelines in dynamic prediction tasks.

- Extending the polling cycle or news sources could test the robustness of the adaptation mechanism.

Load-bearing premise

The assumption that TF-IDF clusters of headlines form semantic neighborhoods whose average realized price reactions remain stable enough to serve as a predictive signal when the weighting mechanism re-calibrates on historical correlations.

What would settle it

If the TF-IDF cluster signals lose their correlation with subsequent price movements after the weighting mechanism updates during a market regime change, the adaptation claim would be falsified.

Figures

read the original abstract

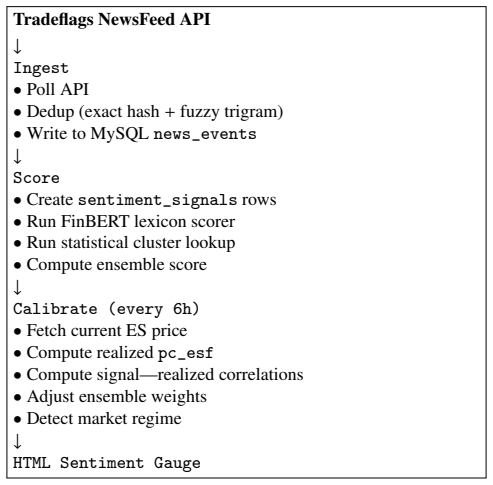

We present a hybrid news sentiment engine that continuously learns market sentiment from paired news headlines and concurrent asset-price snapshots without requiring any neural network training or GPU compute. The system uses a three-way ensemble combining (1) a financial-domain lexicon (FinBERT-style keyword scoring), (2) an adaptive statistical TF-IDF cluster learner that organizes headlines into semantic neighborhoods and tracks their average realized price reactions, and (3) an auto-calibrating weighting mechanism that adjusts ensemble contributions based on each signal's historical correlation with actual price movements. The engine runs on a 3-hour polling cycle from the Tradeflags NewsFeed API, which provides 22 price-snapshot fields per news item spanning equity indices (ES, NQ, SPY, DJIA, NDX, IWM), commodities (CL), and cryptocurrencies (BTC, ETH). All processing occurs at sub-second latency on a CPU-only server at effectively zero marginal cost per analytic cycle. We compare our approach against established methods -- FinBERT, GPT-based scoring, VADER, and commercial sentiment APIs -- across dimensions of cost, latency, accuracy, and adaptability. Our statistical cluster learner, which adapts to changing market regimes without retraining, represents a novel contribution not found in existing sentiment systems.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper presents a hybrid news sentiment engine for real-time market analysis that combines (1) a financial-domain lexicon, (2) an adaptive TF-IDF cluster learner that groups headlines into semantic neighborhoods and tracks their average realized price reactions, and (3) an auto-calibrating weighting mechanism based on historical correlations with price movements. It claims CPU-only sub-second latency operation on a 3-hour cycle using Tradeflags NewsFeed data across equities, commodities, and crypto, with comparisons to FinBERT, VADER, GPT scoring, and commercial APIs, and asserts novelty in the cluster learner's ability to adapt to market regimes without retraining.

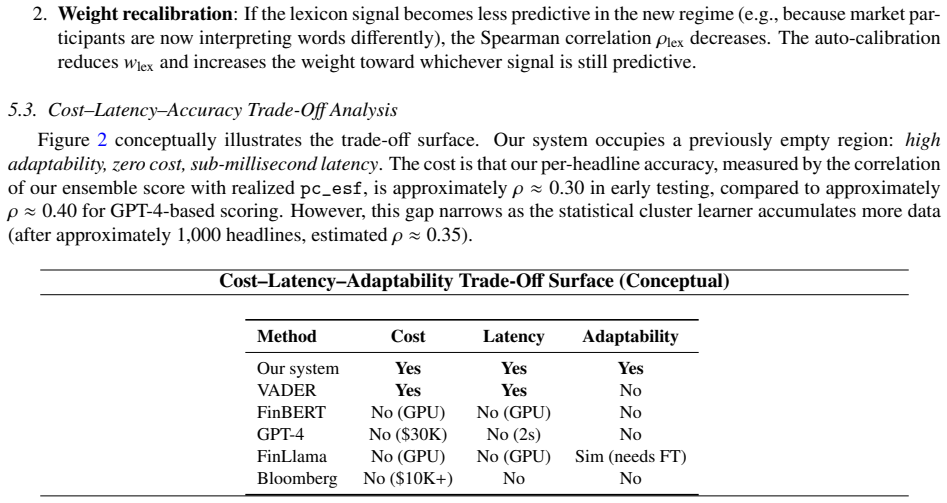

Significance. If the performance and stability claims were empirically validated, the approach could offer a low-cost, low-latency alternative to neural sentiment models for financial applications where GPU resources are unavailable. The adaptive clustering idea, if shown to maintain stable price-reaction signals across regimes, would address a recognized limitation of static lexicons. However, the manuscript contains no quantitative results, so these potential contributions cannot be assessed.

major comments (3)

- [Abstract] Abstract: The manuscript asserts performance advantages in accuracy and adaptability over FinBERT, VADER, and GPT-based methods, yet supplies no error metrics, baseline comparisons, experimental setup, or results tables to support any of these claims. All assertions rest on description alone.

- [Description of the statistical cluster learner] Description of the statistical cluster learner: No details are provided on cluster formation (value of k, distance metric, update rule), validation of semantic coherence of the TF-IDF neighborhoods, or any test of temporal stability of the average realized price reactions. This assumption is load-bearing for the novelty claim that the learner adapts to regime shifts without retraining.

- [Auto-calibrating weighting mechanism] Auto-calibrating weighting mechanism: The weighting adjusts ensemble contributions according to each signal's historical correlation with price movements; by the paper's own description this calibration uses the same past data that defines the clusters, creating a circularity that is not addressed with any out-of-sample protocol or robustness check.

Simulated Author's Rebuttal

We thank the referee for their detailed review and constructive comments. We address each major comment below and outline the revisions we will make to strengthen the manuscript.

read point-by-point responses

-

Referee: [Abstract] Abstract: The manuscript asserts performance advantages in accuracy and adaptability over FinBERT, VADER, and GPT-based methods, yet supplies no error metrics, baseline comparisons, experimental setup, or results tables to support any of these claims. All assertions rest on description alone.

Authors: The referee is correct that the current manuscript version does not include quantitative results or experimental details to support the claims made in the abstract. We will revise the manuscript to include a comprehensive results section with error metrics, baseline comparisons, experimental setup, and results tables comparing our approach to FinBERT, VADER, GPT scoring, and commercial APIs. revision: yes

-

Referee: [Description of the statistical cluster learner] Description of the statistical cluster learner: No details are provided on cluster formation (value of k, distance metric, update rule), validation of semantic coherence of the TF-IDF neighborhoods, or any test of temporal stability of the average realized price reactions. This assumption is load-bearing for the novelty claim that the learner adapts to regime shifts without retraining.

Authors: We acknowledge that the manuscript provides only a high-level description of the cluster learner without the requested technical details. In the revision, we will expand the methods section to specify the value of k, the distance metric used, the update rule for clusters, and include validation metrics for semantic coherence and tests for temporal stability of the price-reaction signals. revision: yes

-

Referee: [Auto-calibrating weighting mechanism] Auto-calibrating weighting mechanism: The weighting adjusts ensemble contributions according to each signal's historical correlation with price movements; by the paper's own description this calibration uses the same past data that defines the clusters, creating a circularity that is not addressed with any out-of-sample protocol or robustness check.

Authors: The referee correctly points out the potential issue of circularity in the weighting mechanism. We will revise the description to explicitly detail the out-of-sample protocol used for calibration, including how historical correlations are computed separately from cluster formation, and add robustness checks to address this concern. revision: yes

Circularity Check

No circularity: adaptive weighting is standard engineering, not a derivation

full rationale

The paper presents an engineering description of a hybrid sentiment system rather than a mathematical derivation chain. The auto-calibrating weights based on historical correlations are a conventional online adaptation step and do not reduce any claimed first-principles result or prediction to its own inputs by construction. No equations, uniqueness theorems, self-citations, or ansatzes are supplied that could trigger the enumerated circularity patterns. The novelty assertion concerns the practical combination of lexicon, TF-IDF clustering, and weighting; this remains an empirical claim open to external validation and does not collapse definitionally.

Axiom & Free-Parameter Ledger

free parameters (1)

- ensemble weighting coefficients

Reference graph

Works this paper leans on

-

[1]

E. F. Fama, Efficient capital markets: A review of theory and empirical work, Journal of Finance 25 (2) (1970) 383–417

1970

-

[2]

G. Iacovides, T. Konstantinidis, M. Xu, D. Mandic, Finllama: Llm-based financial sentiment analysis for al- gorithmic trading, in: International Conference on AI in Finance (ICAIF), 2024.doi:10.1145/3677052. 3698696

-

[3]

K. Kirtac, G. Germano, Large language models in finance: What is financial sentiment?, in: SSRN Working Paper, 2025.doi:10.2139/ssrn.5166656

-

[4]

Loughran, B

T. Loughran, B. McDonald, When is a liability not a liability? textual analysis, dictionaries, and 10-ks, Journal of Finance 66 (1) (2011) 35–65

2011

-

[5]

R. Catelli, S. Pelosi, M. Esposito, Lexicon-based vs. bert-based sentiment analysis: A comparative study in italian, Electronics 11 (3) (2022) 374.doi:10.3390/electronics11030374

-

[6]

A. Kotelnikova, D. Paschenko, K. O. Bochenina, E. Kotelnikov, Lexicon-based methods vs. bert for text senti- ment analysis, in: International Joint Conference on the Analysis of Images, Social Networks and Texts (AIST), 2021.doi:10.1007/978-3-031-16500-9_7

-

[7]

BERT: Pre-training of Deep Bidirectional Transformers for Language Understanding

J. Devlin, M.-W. Chang, K. Lee, K. Toutanova, Bert: Pre-training of deep bidirectional transformers for language understanding, arXiv preprintArXiv:1810.04805v2 (2019).doi:10.48550/arXiv.1810.04805

work page internal anchor Pith review Pith/arXiv arXiv doi:10.48550/arxiv.1810.04805 2019

-

[8]

D. Araci, Finbert: Financial sentiment analysis with pre-trained language models, arXiv preprint- ArXiv:1908.10063 (2019)

Pith/arXiv arXiv 1908

-

[9]

P. Malo, A. Sinha, P. Korhonen, J. Wallenius, P. Takala, Good debt or bad debt: Detecting semantic orientations in economic texts, Journal of the Association for Information Science and Technology 65 (4) (2014) 782–796

2014

-

[10]

Huang, et al., Finbert-tone: Fine-tuned bert for financial tone analysis, GitHub repositoryhttps://github

Y . Huang, et al., Finbert-tone: Fine-tuned bert for financial tone analysis, GitHub repositoryhttps://github. com/yiyanghkust/finbert-tone(2021)

2021

-

[11]

M. P. Cristescu, C. Brânda¸ s, D. A. Mara, P. Ioana, Fine-tuning and explaining finbert for sector-specific financial news: A reproducible workflow, Electronics 14 (23) (2025) 4680.doi:10.3390/electronics14234680

-

[12]

S. Chandra, D. G. Balakrishna, Enhancing finrl trading agents with advance llm-processed financial news: An improved approach using deepseek-v3, in: International Conference on Intelligent Data Science (IDS), 2025. doi:10.1109/IDS66066.2025.00016

-

[13]

D. Dai, D. Ma, D. Liu, K. Geng, Y . Wang, Beyond polarity: Multi-dimensional llm sentiment signals for wti crude oil futures return predictionS2 paper ID 286489493 (2026)

2026

-

[14]

U. Mishra, P. R. Chandre, N. Saxena, S. Saxena, Hybrid dl models for stock market analysis: A compara- tive survey of feature engineering, ensemble strategies, and risk metrics, in: IEEE International Conference on Blockchain and Distributed Systems Security (ICBDS), 2025.doi:10.1109/ICBDS67396.2025.11376636. 13

-

[15]

H. Liu, Z. Lin, R. R. Rojas, Enhancing trading performance through sentiment analysis with large language models: Evidence from the s&p 500S2 paper ID 280233126 (2025)

2025

-

[16]

N. Passalis, S. Seficha, A. Tsantekidis, A. Tefas, Learning sentiment-aware trading strategies for bitcoin leverag- ing deep learning-based financial news analysis, in: Artificial Intelligence Applications and Innovations (AIAI), 2021.doi:10.1007/978-3-030-79150-6_59

-

[17]

Z. Song, R. Huang, A. Li, A. Shen, H. Chen, Adapter-regularised continual learning for dynamic financial sentiment encoding in multi-modal market fusion, Expert Systems (2025).doi:10.1111/exsy.70178

-

[18]

Tsaknaki, F

I.-Y . Tsaknaki, F. Lillo, P. Mazzarisi, Online learning of order flow and market impact with bayesian change- point detection methodsS2 paper ID 274683885 (2023)

2023

-

[19]

J. P. Moyano, D. Partida, M. Gessl, Your sentiment matters: A machine learning approach for predicting regime changes in the cryptocurrency market, in: Hawaii International Conference on System Sciences (HICSS), 2023. doi:10.24251/hicss.2023.115

-

[20]

Kahneman, A

D. Kahneman, A. Tversky, Prospect theory: An analysis of decision under risk, Econometrica 47 (2) (1979) 263–291

1979

-

[21]

Salton, C

G. Salton, C. Buckley, Term-weighting approaches in automatic text retrieval, Information Processing and Man- agement 24 (5) (1988) 513–523

1988

-

[22]

DSPy: Compiling Declarative Language Model Calls into Self-Improving Pipelines

O. Khattab, A. Singhvi, P. Maheshwari, et al., Dspy: Compiling declarative language model calls into self- improving pipelines, arXiv preprintArXiv:2310.03714 (2024).doi:10.48550/arXiv.2310.03714. 14 Table 2: Comprehensive comparison of our system against existing sentiment approaches. Dimension Ours FinBERT GPT-4 FinLlama V ADER Bloomberg Alpha Vant. Cos...

work page internal anchor Pith review Pith/arXiv arXiv doi:10.48550/arxiv.2310.03714 2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.