CSTrader: A Testbed for Language-Grounded Trading in a Community-Driven Virtual Asset Market

Pith reviewed 2026-07-01 05:47 UTC · model grok-4.3

The pith

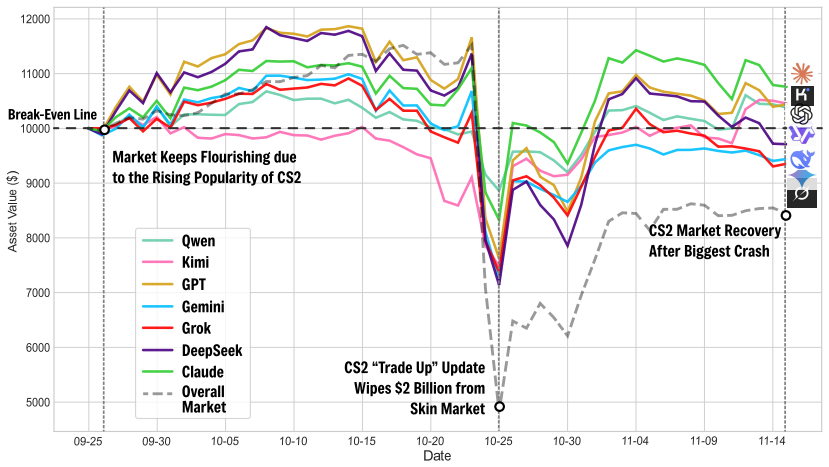

A multi-agent LLM system turns community discussions into CS2 skin trades that return 7.58 percent while the market index falls 15.62 percent.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

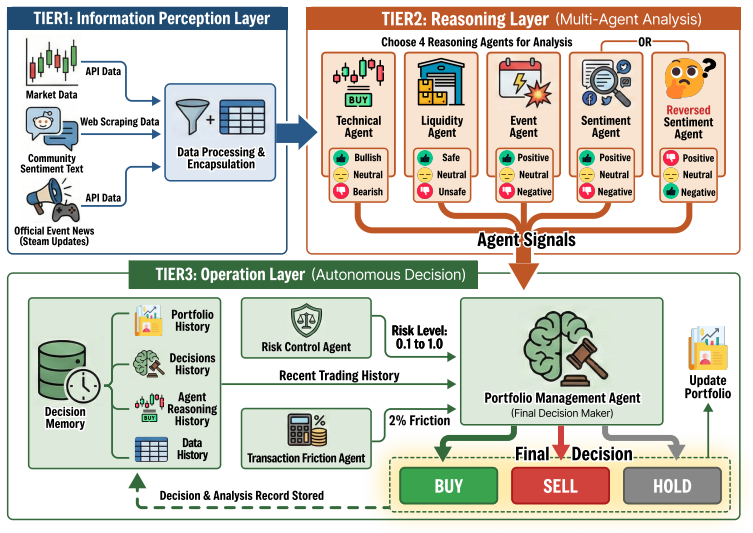

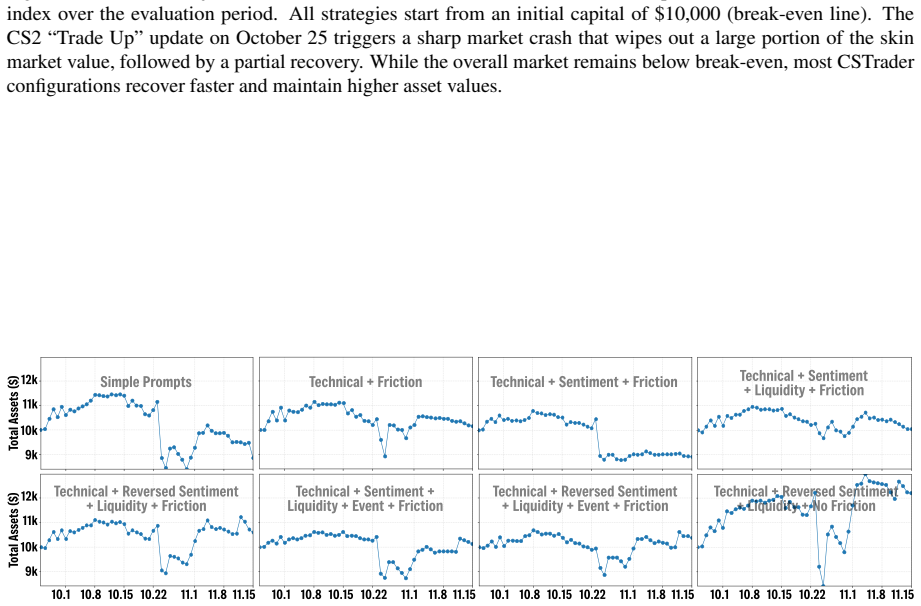

CSTrader first integrates heterogeneous signals from multiple sources, then routes them through specialized agents for technical analysis, liquidity assessment, event detection, and reversed sentiment analysis, and finally applies risk control, transaction friction, and portfolio management agents to produce decisions. In a live-like environment built on real CS2 weapon skin data from a highly volatile period, the system achieves up to 7.58 percent cumulative return against a market index decline of 15.62 percent across several LLM backbones, with ablation studies confirming that liquidity, reversed sentiment, and transaction friction components are essential for converting noisy language si

What carries the argument

The multi-agent decomposition that assigns distinct LLM agents to technical analysis, liquidity, events, reversed sentiment, risk control, and transaction friction before producing buy-sell-hold outputs.

If this is right

- Niche, language-driven asset markets can function as repeatable benchmarks for language-to-action systems.

- Liquidity detection and reversed-sentiment processing become necessary steps when converting community text into trading actions.

- Explicit modeling of transaction friction and risk limits is required to keep cumulative returns positive under realistic conditions.

- Different LLM backbones can be compared directly on the same trading task and data set.

- The framework supplies a concrete way to measure how well language models handle portfolio decisions rather than isolated predictions.

Where Pith is reading between the lines

- The same agent structure could be tested on other community-driven markets such as NFTs or meme stocks to check whether the performance pattern repeats.

- Reversing community sentiment may be a general tactic worth examining in any market where public discussion tends to lag or overreact to price moves.

- The testbed could be extended to include real-time streaming of new community posts to measure latency between text arrival and trade execution.

- Removing the virtual-asset restriction and applying the agents to conventional equities would test whether the language-to-profit conversion depends on the small-market setting.

Load-bearing premise

The chosen live-like evaluation with real CS2 data from one volatile period accurately reflects real trading frictions and that the listed set of specialized agents is both necessary and sufficient to turn language signals into profits.

What would settle it

Running the same agents on a later CS2 data period in which community sentiment shows no reliable price correlation, or finding that a single-prompt baseline matches the multi-agent returns, would falsify the performance and necessity claims.

Figures

read the original abstract

Niche asset markets, such as Counter-Strike 2 (CS2) weapon skins, are small, volatile, and heavily driven by community discussions and platform rules. These properties make them hard for traditional quantitative models, but provide an ideal testbed for studying how large language models (LLMs) turn unstructured text into trading actions. We present CSTrader, a multi-agent framework for language-grounded trading in the CS2 skin market. The system first integrates heterogeneous signals from various sources, then uses specialized agents for technical analysis, liquidity, events, and (reversed) sentiment, and finally applies risk control, transaction friction, and portfolio management agents to produce buy, sell, or hold decisions under realistic trading frictions. We build a live-like evaluation environment with real CS2 data from a highly volatile period and evaluate several recent LLM backbones. Across models, CSTrader consistently outperforms both a falling market index (-15.62%) and simple single-prompt LLM baselines, achieving up to a 7.58% cumulative return with controlled risk. Ablation studies show that liquidity, reversed sentiment, and transaction friction agents are crucial for turning noisy language signals into stable profits, suggesting that niche, language-driven markets are a useful benchmark for future language-to-action research. Code is available at: https://github.com/IatomicreactorI/CSGOTrading?tab=readme-ov-file#quick-start

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript presents CSTrader, a multi-agent framework that integrates heterogeneous signals from community sources and deploys specialized LLM agents for technical analysis, liquidity assessment, events, reversed sentiment, risk control, transaction friction, and portfolio management to generate buy/sell/hold decisions in the CS2 weapon skin market. Using a live-like evaluation environment with real data from a highly volatile period, the system is shown to achieve up to 7.58% cumulative return across several LLM backbones, outperforming both the market index (-15.62%) and single-prompt baselines, with ablation studies identifying liquidity, reversed sentiment, and transaction friction agents as critical. Code is released at the provided GitHub link.

Significance. If the reported outperformance holds under rigorous verification, the work supplies a reproducible testbed for language-to-action research in small, text-driven, volatile markets where conventional quant models are ill-suited. Explicit credit is due for the open-source code release and the targeted ablation experiments that isolate which agent components convert noisy signals into stable profits; these elements directly support future benchmarking and component-level analysis.

major comments (1)

- [Abstract] Abstract: performance numbers (7.58% cumulative return, outperformance vs. -15.62% index) are reported without any description of data splits, statistical significance tests, position-sizing rules, or the procedure used to select the volatile evaluation period. These omissions are load-bearing for the central empirical claim of consistent, controlled-risk superiority.

minor comments (1)

- The term 'reversed sentiment' is used in the abstract and agent list but is not defined or operationalized in the provided text, leaving unclear how reversal is implemented relative to standard sentiment signals.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback highlighting the need for greater methodological transparency in the abstract. We address this point below and will revise the manuscript accordingly.

read point-by-point responses

-

Referee: [Abstract] Abstract: performance numbers (7.58% cumulative return, outperformance vs. -15.62% index) are reported without any description of data splits, statistical significance tests, position-sizing rules, or the procedure used to select the volatile evaluation period. These omissions are load-bearing for the central empirical claim of consistent, controlled-risk superiority.

Authors: We agree that the abstract would be strengthened by briefly noting these elements to make the central claims more self-contained. The full manuscript describes the live-like evaluation environment using real CS2 market data from a volatile period selected based on observed large drawdowns in the skin index, chronological train/test splits to prevent leakage, position sizing and exposure limits enforced by the portfolio management agent, and risk-control mechanisms. Performance is compared across multiple LLM backbones and ablations rather than formal p-value tests. We will revise the abstract to concisely reference the volatile-period selection criterion and the presence of these controls, while directing readers to the methods section for full details. This change directly addresses the concern. revision: yes

Circularity Check

No significant circularity

full rationale

The paper presents an empirical multi-agent LLM trading system evaluated on real CS2 market data. No equations, fitted parameters renamed as predictions, self-definitional constructs, or load-bearing self-citations appear in the derivation chain. Reported returns and ablation results are direct empirical outcomes from the described agents and environment, with no reduction of claims to inputs by construction. This is the standard case of a self-contained empirical benchmark paper.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

DeepSeek-V3.2: Pushing the Frontier of Open Large Language Models

Deepseek-v3. 2: Pushing the frontier of open large language models , author=. arXiv preprint arXiv:2512.02556 , year=

work page internal anchor Pith review Pith/arXiv arXiv

-

[2]

Qwen3 technical report , author=. arXiv preprint arXiv:2505.09388 , year=

work page internal anchor Pith review Pith/arXiv arXiv

-

[3]

How to use Moonshot v1 , howpublished =

-

[4]

Gemini 3 Flash Best for frontier intelligence at speed , howpublished =

-

[5]

2025 , howpublished =

Introducing GPT-5 for Developers , author =. 2025 , howpublished =

2025

-

[6]

2024 , howpublished =

Claude 4: Technical Report , author =. 2024 , howpublished =

2024

-

[7]

2024 , howpublished =

Grok-4 Technical Overview , author =. 2024 , howpublished =

2024

-

[8]

arXiv preprint arXiv:2406.10811 , year=

LLMFactor: Extracting profitable factors through prompts for explainable stock movement prediction , author=. arXiv preprint arXiv:2406.10811 , year=

-

[9]

arXiv preprint arXiv:2307.10485 , year=

Fingpt: Democratizing internet-scale data for financial large language models , author=. arXiv preprint arXiv:2307.10485 , year=

-

[10]

FinRobot: an open-source AI agent platform for financial applications using large language models , author=. arXiv preprint arXiv:2405.14767 , year=

-

[11]

Proceedings of the 5th ACM International Conference on AI in Finance , pages=

Xbrl agent: Leveraging large language models for financial report analysis , author=. Proceedings of the 5th ACM International Conference on AI in Finance , pages=

-

[12]

arXiv preprint arXiv:2504.13522 , year=

Cross-Modal Temporal Fusion for Financial Market Forecasting , author=. arXiv preprint arXiv:2504.13522 , year=

-

[13]

arXiv preprint arXiv:2501.12399 , year=

FinSphere: A Conversational Stock Analysis Agent Equipped with Quantitative Tools based on Real-Time Database , author=. arXiv preprint arXiv:2501.12399 , year=

-

[14]

Proceedings of the AAAI Symposium Series , volume=

FinMem: A performance-enhanced LLM trading agent with layered memory and character design , author=. Proceedings of the AAAI Symposium Series , volume=

-

[15]

arXiv preprint arXiv:2310.10436 , year=

Econagent: large language model-empowered agents for simulating macroeconomic activities , author=. arXiv preprint arXiv:2310.10436 , year=

-

[16]

arXiv preprint arXiv:2502.11433 , year=

FLAG-Trader: Fusion LLM-Agent with Gradient-based Reinforcement Learning for Financial Trading , author=. arXiv preprint arXiv:2502.11433 , year=

-

[17]

arXiv preprint arXiv:2402.03755 , year=

Quantagent: Seeking holy grail in trading by self-improving large language model , author=. arXiv preprint arXiv:2402.03755 , year=

-

[18]

Proceedings of the 30th ACM SIGKDD Conference on Knowledge Discovery and Data Mining , pages=

A multimodal foundation agent for financial trading: Tool-augmented, diversified, and generalist , author=. Proceedings of the 30th ACM SIGKDD Conference on Knowledge Discovery and Data Mining , pages=

-

[19]

C rypto T rade: A Reflective LLM -based Agent to Guide Zero-shot Cryptocurrency Trading

Li, Yuan and Luo, Bingqiao and Wang, Qian and Chen, Nuo and Liu, Xu and He, Bingsheng. C rypto T rade: A Reflective LLM -based Agent to Guide Zero-shot Cryptocurrency Trading. Proceedings of the 2024 Conference on Empirical Methods in Natural Language Processing. 2024. doi:10.18653/v1/2024.emnlp-main.63

-

[20]

Advances in Neural Information Processing Systems , volume=

Fincon: A synthesized llm multi-agent system with conceptual verbal reinforcement for enhanced financial decision making , author=. Advances in Neural Information Processing Systems , volume=

-

[21]

TradingAgents: Multi-agents LLM financial trading framework,

TradingAgents: Multi-Agents LLM Financial Trading Framework , author=. arXiv preprint arXiv:2412.20138 , year=

-

[22]

Changlun Li and Yao Shi and Yuyu Luo and Nan Tang , title =. CoRR , volume =. 2025 , url =. doi:10.48550/ARXIV.2503.18313 , eprinttype =. 2503.18313 , timestamp =

-

[23]

SSRN Electronic Journal , year =

Investor Attention and Cryptocurrency Volatility: A Machine Learning and Econometric Analysis , author =. SSRN Electronic Journal , year =

-

[24]

arXiv preprint arXiv:2508.15825 , year =

Enhancing Cryptocurrency Sentiment Analysis with Multimodal Features , author =. arXiv preprint arXiv:2508.15825 , year =

-

[25]

and Tselikas, Nikolaos D

Roumeliotis, Konstantinos I. and Tselikas, Nikolaos D. and Nasiopoulos, Dimitrios K. , journal =. 2024 , doi =

2024

-

[26]

2025 , url =

Luo, Yichen and Feng, Yebo and Xu, Jiahua and Tasca, Paolo and Liu, Yang , journal =. 2025 , url =

2025

-

[27]

SSRN Electronic Journal , year =

Can Large Language Models Forecast Carbon Price Movements? Evidence from Chinese Carbon Markets , author =. SSRN Electronic Journal , year =

-

[28]

SSRN Electronic Journal , year =

Time is Money: An Investment in Luxury Watches , author =. SSRN Electronic Journal , year =. doi:10.2139/ssrn.5119075 , url =

-

[29]

Predicting Liquidity-Aware Bond Yields using Causal GANs and Deep Reinforcement Learning with LLM Evaluation , author =. arXiv preprint arXiv:2502.17011 , year =

work page internal anchor Pith review Pith/arXiv arXiv

-

[30]

Proceedings of the 18th International Conference on Agents and Artificial Intelligence (ICAART) , year =

BondBERT: What we learn when assigning sentiment in the bond market , author =. Proceedings of the 18th International Conference on Agents and Artificial Intelligence (ICAART) , year =

-

[31]

Frontiers in Artificial Intelligence , volume =

Artificial Intelligence for Algorithmic Trading Digital Assets: Evidence from the Counter-Strike 2 Skin Market , author =. Frontiers in Artificial Intelligence , volume =. 2025 , url =. doi:10.3389/frai.2025.1702924 , issn =

-

[32]

Calculation Formula of Market Index , year =

-

[33]

arXiv preprint arXiv:2105.07447 , year=

Non-fungible token (NFT): Overview, evaluation, opportunities and challenges , author=. arXiv preprint arXiv:2105.07447 , year=

-

[34]

Available at SSRN 4891841 , year=

Beyond the hype: A meme coin reality check for retail investors , author=. Available at SSRN 4891841 , year=

-

[35]

Applied Sciences , volume=

Crypto collectibles, museum funding and OpenGLAM: challenges, opportunities and the potential of Non-Fungible Tokens (NFTs) , author=. Applied Sciences , volume=. 2021 , publisher=

2021

-

[36]

UNLV Gaming LJ , volume=

" Skins" in the Game: Counter-Strike, Esports, and the Shady World of Online Gambling , author=. UNLV Gaming LJ , volume=. 2017 , publisher=

2017

-

[37]

, author=

Esports betting and skin gambling: A brief history. , author=. Journal of Gambling Issues , volume=

-

[38]

arXiv preprint arXiv:2412.10906 , year=

SusGen-GPT: A Data-Centric LLM for Financial NLP and Sustainability Report Generation , author=. arXiv preprint arXiv:2412.10906 , year=

-

[39]

Finance Research Letters , volume=

Can ChatGPT improve investment decisions? From a portfolio management perspective , author=. Finance Research Letters , volume=. 2024 , publisher=

2024

-

[40]

Gaming Law Review , volume=

Skin gambling: Have we found the millennial goldmine or imminent trouble? , author=. Gaming Law Review , volume=. 2017 , publisher=

2017

-

[41]

arXiv preprint arXiv:2502.07071 , year=

TRADES: Generating Realistic Market Simulations with Diffusion Models , author=. arXiv preprint arXiv:2502.07071 , year=

-

[42]

Companion Proceedings of the ACM on Web Conference 2025 , pages=

Hedgeagents: A balanced-aware multi-agent financial trading system , author=. Companion Proceedings of the ACM on Web Conference 2025 , pages=

2025

-

[43]

arXiv preprint arXiv:2407.17866 , year=

Financial statement analysis with large language models , author=. arXiv preprint arXiv:2407.17866 , year=

-

[44]

Proceedings of the 2024 joint international conference on computational linguistics, language resources and evaluation (LREC-COLING 2024) , pages=

Alphafin: Benchmarking financial analysis with retrieval-augmented stock-chain framework , author=. Proceedings of the 2024 joint international conference on computational linguistics, language resources and evaluation (LREC-COLING 2024) , pages=

2024

-

[45]

2012 , publisher=

Risk management and financial institutions,+ Web Site , author=. 2012 , publisher=

2012

-

[46]

Stanfold University, Fall , year=

The sharpe ratio, the journal of portfolio management , author=. Stanfold University, Fall , year=

-

[47]

1991 , institution=

Volatility tests and efficient markets: A review essay , author=. 1991 , institution=

1991

-

[48]

The review of financial studies , volume=

Downside risk , author=. The review of financial studies , volume=. 2006 , publisher=

2006

-

[49]

The Journal of Finance , volume=

The performance of mutual funds in the period 1945–1964 , author=. The Journal of Finance , volume=. 1968 , publisher=

1945

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.