An extendable, integrated, and dynamic approach to forecasting and stress-testing credit risk

Pith reviewed 2026-06-26 18:36 UTC · model grok-4.3

The pith

An extendable simulation integrates loan production with multistate cash flow modeling to enable dynamic credit risk stress testing.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

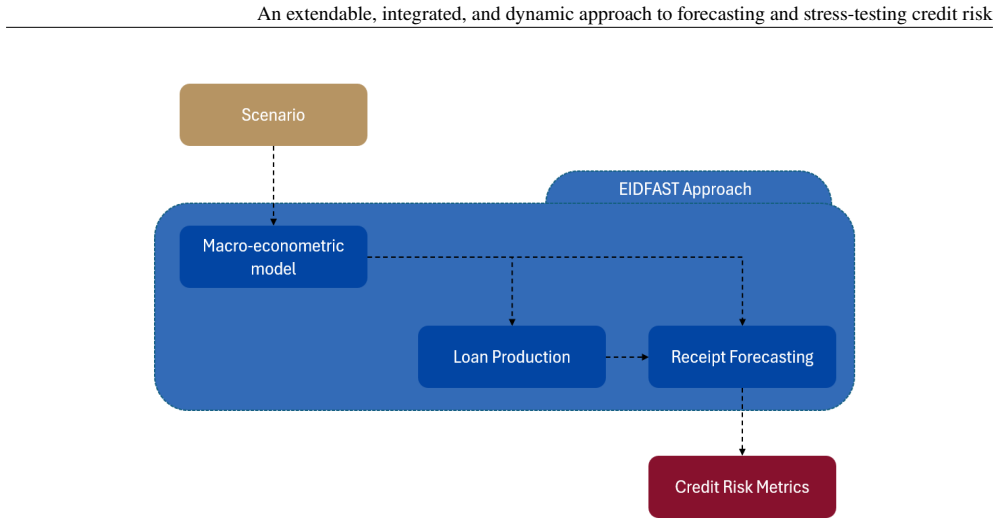

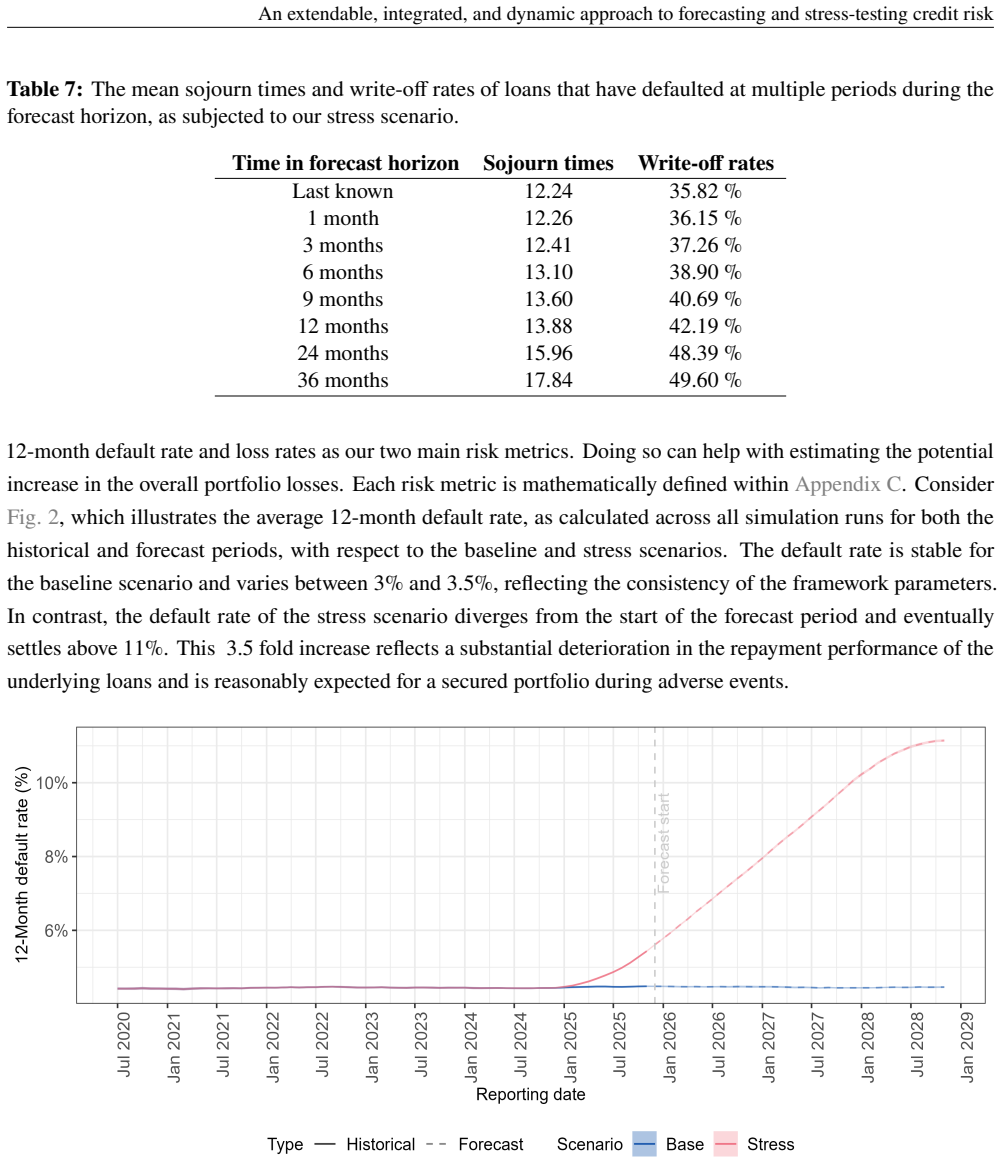

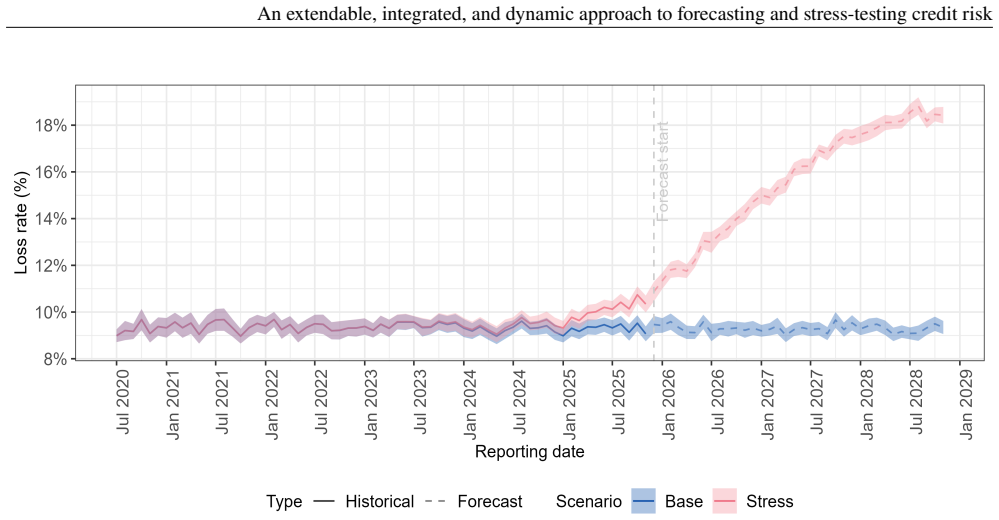

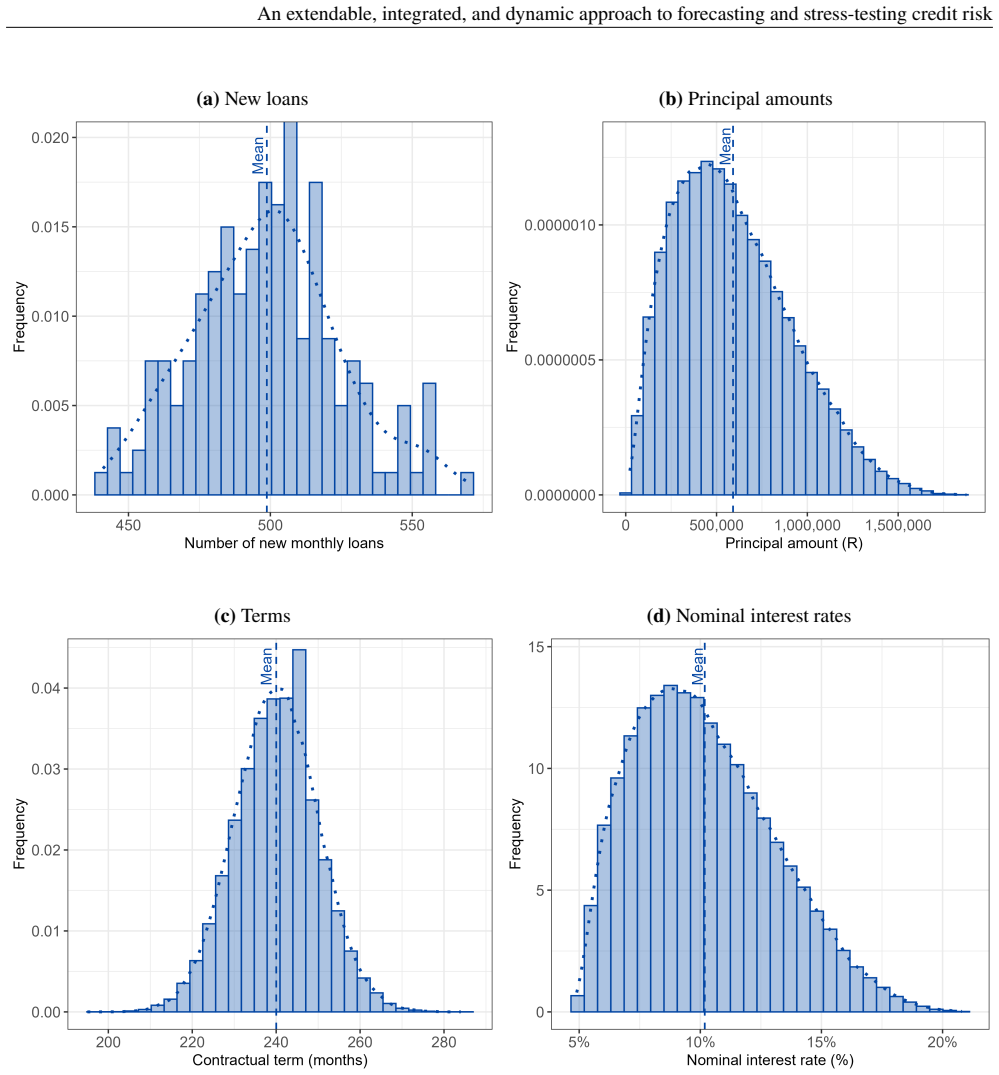

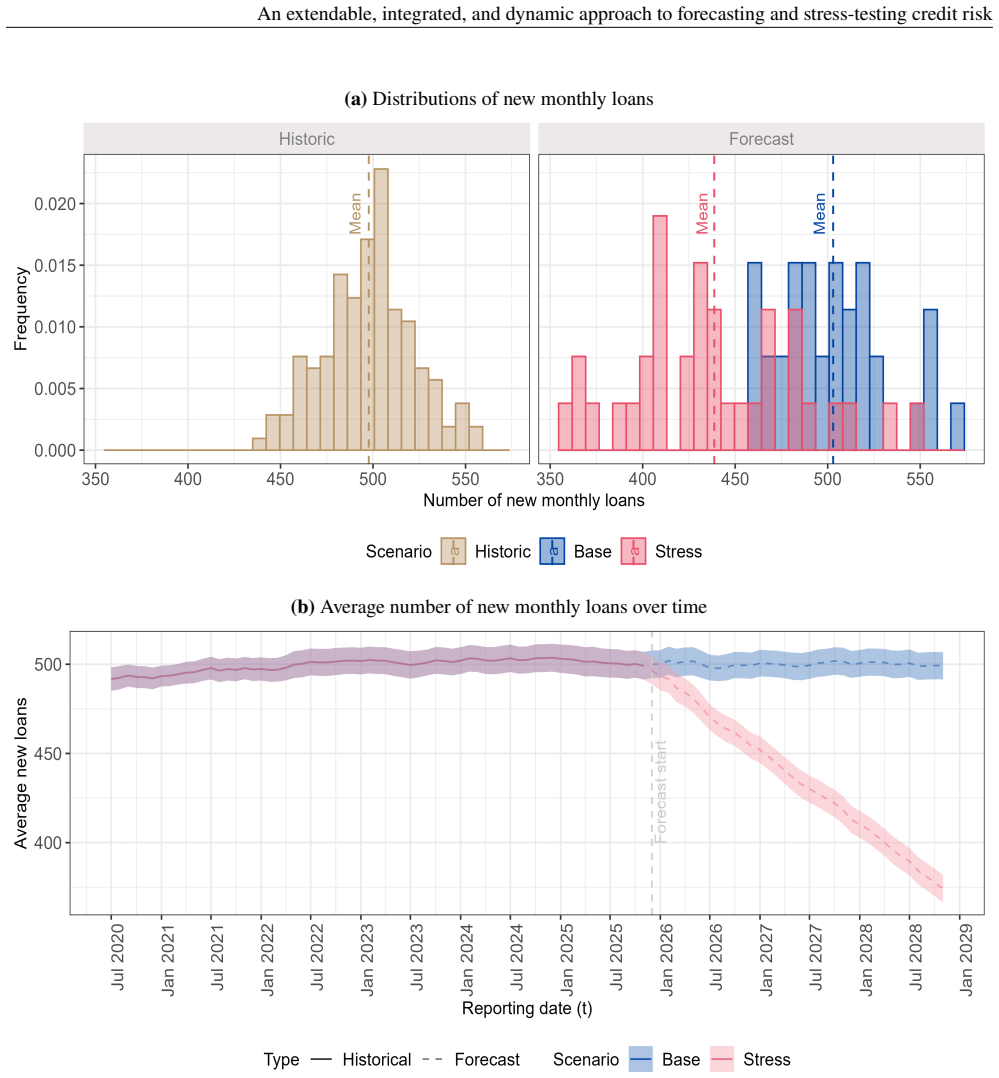

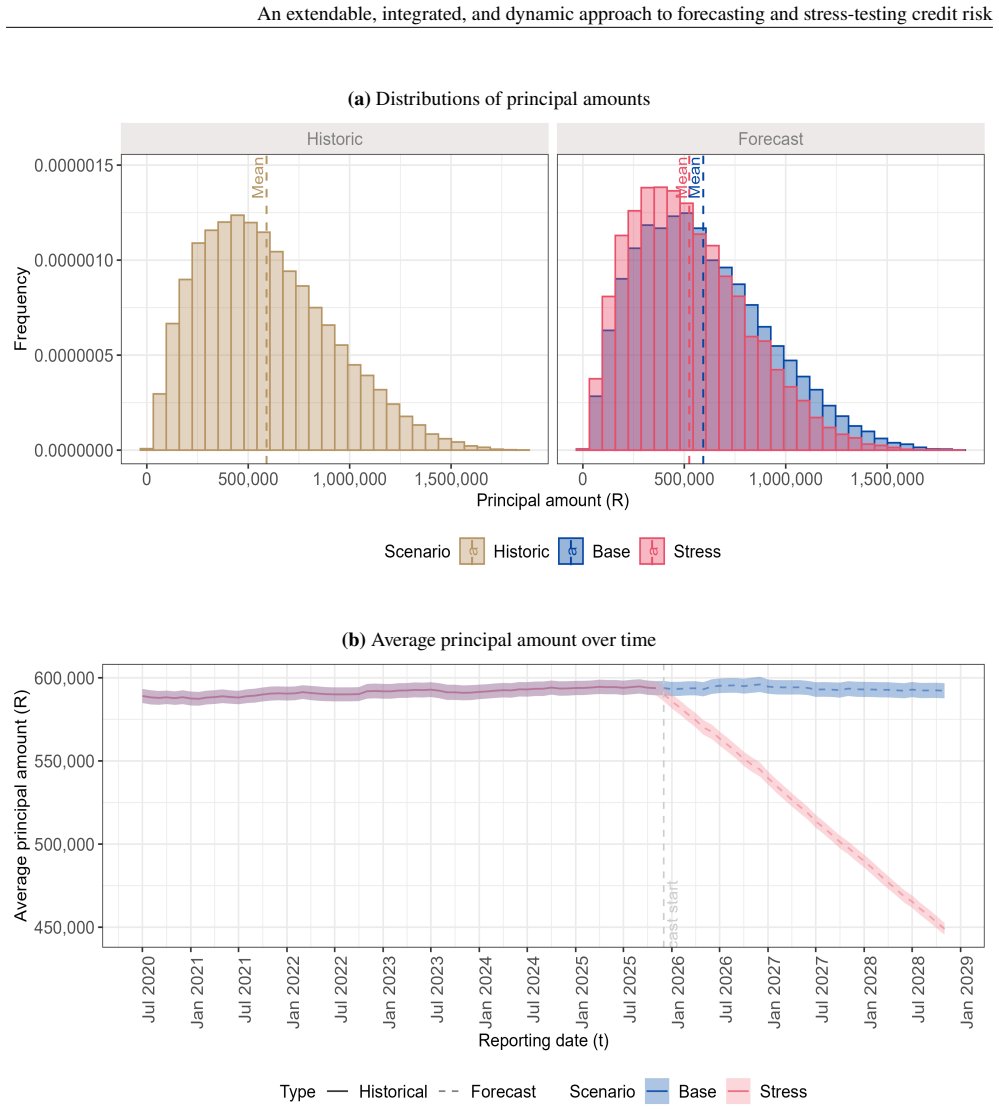

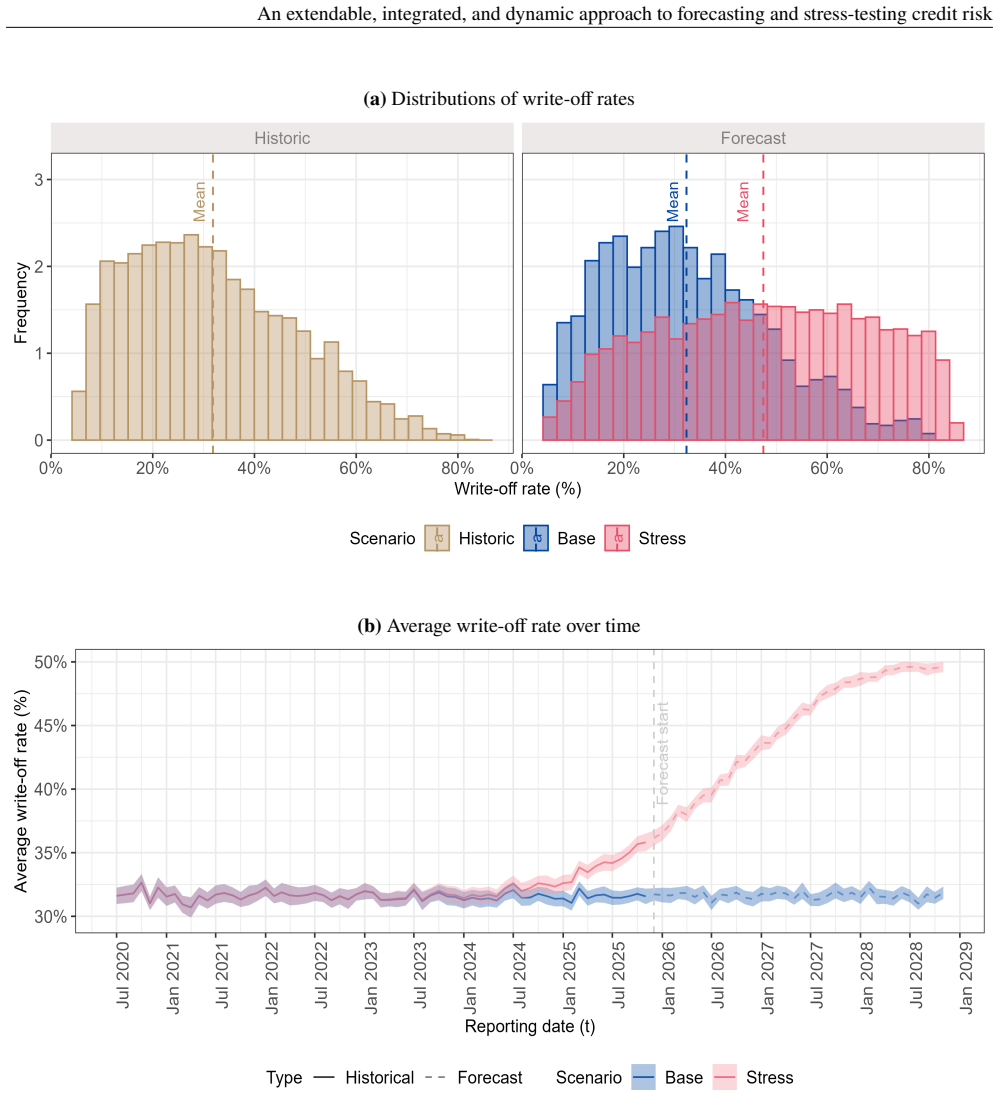

By simulating completed loan portfolios with realistic parameters, generating their cash flow histories in a multistate probabilistic framework, and introducing stress by varying parameters in a broader Monte Carlo setup, the approach computes credit risk metrics while integrating loan production forecasting with receipt generation, yielding more dynamic and flexibly tuned predictions.

What carries the argument

The multistate probabilistic framework for cash flow generation combined with Monte Carlo variation of loan parameters for stress scenarios.

If this is right

- Portfolio-level credit risk metrics such as default and loss rates can be derived directly from the simulated completed loans.

- Stress scenarios produce a range of portfolios by adjusting loan parameters accordingly.

- The approach can be extended by dynamically modeling loan parameters as functions of input variables using any applicable technique when data is available.

- It embeds the correlation structure amongst risk metrics, unlike classical separate treatments.

Where Pith is reading between the lines

- Such an integration might uncover dependencies between how loans are originated and their subsequent risk behavior that separate models overlook.

- Banks could use this to test a wider variety of stress conditions, including those affecting both production and risk simultaneously.

- Applying real data to fit the parameters might reveal whether the multistate framework accurately captures actual loan behaviors under stress.

Load-bearing premise

The simulation uses realistic loan parameters and distributional assumptions that capture real-world loan behaviors, correlations, and cash flow dynamics under stress.

What would settle it

Running the simulation on historical loan data from a known stress period and finding that the computed default and loss rates do not match the observed rates, or that varying parameters does not produce meaningfully different outcomes from traditional methods.

Figures

read the original abstract

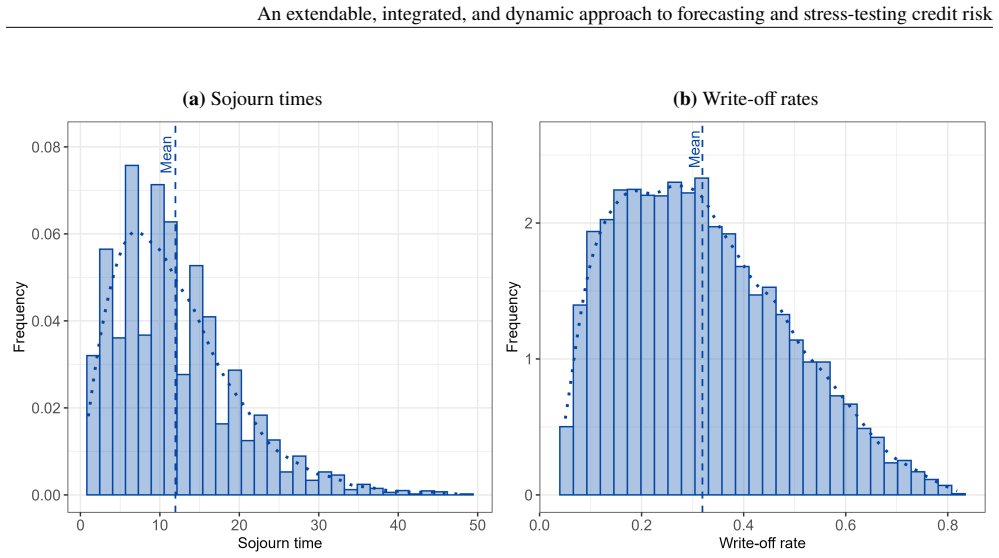

An integrated and extendable approach for stress-testing loan portfolios is presented, which includes both a loan production component and a credit risk component. In this approach, we simulate a completed portfolio using realistic loan parameters and distributional assumptions. Thereafter, we generate the uncertain cash flow history of these loans within a multistate probabilistic framework. We illustrate our approach using a simulation-based study, though the approach can be fit to real-world data. Such a simulation-based approach is ideal for stress-testing since it allows for evaluating a range of conditions. From these completed loans, we compute portfolio-level credit risk metrics, e.g., default and loss rates. Stress scenarios are introduced by varying the loan parameters accordingly within a broader Monte Carlo setup, thereby resulting in a range of portfolios. A classical approach to stress-testing does not typically integrate loan production or embed the correlation structure amongst risk metrics. In our approach, we integrate the forecasting of risk metrics with receipt-generation. Given data, the loan parameters within our extendable approach can be dynamically modelled as functions of input variables using any applicable technique. Overall, our approach can render predictions that are more dynamic and flexibly tuned, which can enhance stress-testing practices within any bank.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript presents an integrated, simulation-based framework for forecasting and stress-testing credit risk in loan portfolios. It combines a loan production component with a multistate probabilistic credit risk model, generates portfolios via Monte Carlo under stress scenarios by varying parameters, computes portfolio-level metrics such as default and loss rates, and claims the approach is extendable to real data for more dynamic and flexible predictions than classical non-integrated methods.

Significance. If the simulation framework can be calibrated to real data and shown to outperform baselines, the integration of loan origination dynamics with credit risk correlations could strengthen stress-testing practices by enabling more comprehensive scenario analysis. The emphasis on simulation for exploring stress conditions is a methodological strength suited to the domain.

major comments (1)

- [Abstract and simulation study] Abstract and simulation study section: the central claim that the approach 'can render predictions that are more dynamic and flexibly tuned, which can enhance stress-testing practices' requires evidence that parameters can be fit to data and that outputs differ meaningfully from classical methods; the manuscript provides neither a calibration example nor a quantitative comparison of portfolio default/loss rates against a baseline omitting the loan-production or correlation components, relying instead on assumed 'realistic' parameters.

minor comments (2)

- [Abstract] The multistate probabilistic framework is described at a high level without specifying the states, transition probabilities, or how cash-flow histories are generated; adding these details would clarify the implementation.

- [Abstract] The manuscript states the approach 'can be fit to real-world data' and 'dynamically modelled' but does not illustrate any fitting technique or input variables; an example would strengthen the extendability claim.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback on our manuscript. We respond to the major comment below.

read point-by-point responses

-

Referee: [Abstract and simulation study] Abstract and simulation study section: the central claim that the approach 'can render predictions that are more dynamic and flexibly tuned, which can enhance stress-testing practices' requires evidence that parameters can be fit to data and that outputs differ meaningfully from classical methods; the manuscript provides neither a calibration example nor a quantitative comparison of portfolio default/loss rates against a baseline omitting the loan-production or correlation components, relying instead on assumed 'realistic' parameters.

Authors: We agree that the manuscript does not include an empirical calibration to real data or a quantitative comparison against a baseline that omits the loan-production or correlation components. The simulation study relies on assumed realistic parameters to illustrate the integrated Monte Carlo framework under stress scenarios. The central claim uses 'can' to refer to the extendability of the approach, where loan parameters are described as dynamically modelable from covariates. However, this does not substitute for demonstrated fitting or numerical differences from classical methods. We will revise the abstract and simulation study section to clarify the illustrative purpose of the simulation, moderate the language on enhanced stress-testing practices, and note that empirical calibration and baseline comparisons remain important directions for future work. revision: yes

Circularity Check

No circularity; methodological simulation framework with no self-referential derivations

full rationale

The manuscript describes an integrated simulation approach for stress-testing that incorporates loan production and multistate credit risk components, illustrated with chosen realistic parameters and distributional assumptions. It states the framework 'can be fit to real-world data' and 'can be dynamically modelled' but exhibits no equations, fitted parameters, or predictions that reduce by construction to those inputs. No self-citations, uniqueness theorems, or ansatzes are invoked in a load-bearing way. The central claim of greater dynamism remains an unverified assertion about future applicability rather than a derivation that collapses into its own assumptions.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

W., & Goodman, L

Anderson, T. W., & Goodman, L. A. (1957). Statistical inference about Markov chains.Tha Annals of Mathematical Statistics,28(1)

1957

-

[2]

(2019).The Basel framework

BCBS. (2019).The Basel framework. Bank of International Settlements: Basel Committee on Banking Supervision (BCBS). Switzerland.https://www.bis.org/basel_framework/

2019

-

[3]

Bellotti, T., & Crook, J. (2013). Forecasting and stress testing credit card default using dynamic models. International Journal of Forecasting,29

2013

-

[4]

Bocchio, C., Crook, J., & Andreeva, G. (2023). The impact of macroeconomic scenarios on recurrent delinquency: A stress testing framework of multi-state models for mortgages.International Journal of Forecasting,39, 1655–1677

2023

-

[5]

Botha, A. (2021).A procedure for loss-optimising the timing of loan recovery under uncertainty[Doctoral dissertation, University of Pretoria].https://doi.org/10.13140/RG.2.2.12015.30888/1

-

[6]

Botha, A., Beyers, C., & de Villiers, P. (2021). Simulation-based optimisation of the timing of loan recovery across different portfolios.Expert Systems with Applications

2021

-

[7]

Botha, A., Verster, T., & Breedt, R. (2026). Modelling the term-structure of default risk under IFRS 9 within a multistate regression framework.Journal of Applied Statistics.https://doi.org/10.1080/02664763. 2026.2660955

-

[8]

Breuer, T., Jandacka, M., Mencia, J., & Summer, M. (2012). A systematic approach to multi-period stress testing of portfolio credit risk.Journal of Banking & Finance,36

2012

-

[9]

Crook, J., & Bellotti, T. (2010). Time varying and dynamic models for default risk in consumer loans. Journal of the Royal Statistical Society Series A,173(2), 283–305.https://doi.org/10.1111/j.1467- 985X.2009.00617.x 22 An extendable, integrated, and dynamic approach to forecasting and stress-testing credit risk

-

[10]

Djeundje,V.B.,Crook,J.,&Andreeva,G.(2025).Thedevilinthedetails:Dynamicpredictionofloanportfolio profitability with macroeconomic drivers through multi-state modelling.European Journal of Operational Research,327(2), 703–715.https://doi.org/https://doi.org/10.1016/j.ejor.2025.07.008

-

[11]

Ferrari, S., Van Roy, P., & Vespro, C. (2011). Stress testing credit risk: Modelling issues.Financial Stability Review,9, 105–120

2011

-

[12]

Foglia, A. (2008). Stress testing credit risk: Survey of authorities’ approached.Unkown

2008

-

[13]

(2000a).Collateral damage: A source of systematic credit risk(Working Paper)

Frye, J. (2000a).Collateral damage: A source of systematic credit risk(Working Paper). Federal Reserve Bank of Chicago

-

[14]

Frye, J. (2000b). Collateral damage: A source of systematic credit risk.Risk Magazine

-

[15]

(2014).A transitions-based framework for estimating expected credit losses(Research Technical Papers No

Gaffney, E., Kelly, R., & McCann, F. (2014).A transitions-based framework for estimating expected credit losses(Research Technical Papers No. 16/RT/14). Central Bank of Ireland.https://ideas.repec.org/ p/cbi/wpaper/16-rt-14.html

2014

-

[16]

Grimshaw, S. D., & Alexander, W. P. (2011). Markov chain models for delinquency: Transition matrix estimation and forecasting.Applied Stochastic Models in Business and Industry,27(3), 267–279.https: //doi.org/10.1002/asmb.827

-

[17]

(2014).International financial reporting standard (IFRS) 9: Financial instruments

IASB. (2014).International financial reporting standard (IFRS) 9: Financial instruments. IFRS Foundation: International Accounting Standards Board (IASB). London.https://www.ifrs.org/issued-standard s/list-of-standards/ifrs-9-financial-instruments/

2014

-

[18]

Jimenez, G., & Mencia, J. (2009). Modelling the distribution of credit losses with observable and latent factors.Journal of Empirical Finance,16(2)

2009

-

[19]

Jokivuolle, E., & Peura, S. (2003). Incorporating collateral value uncertainty in loss given default estimates and loan-to-value ratios.Capital Markets: Asset Pricing & Valuation.https://api.semanticscholar. org/CorpusID:154268934

2003

-

[20]

Jokivuolle, E., & Viren, M. (2013). Cyclical default and recovery in stress testing loan losses.Journal of Financial Stability,9, 139–149

2013

-

[21]

T., Hilbers, P., & Slack, G

Jones, M. T., Hilbers, P., & Slack, G. (2004). Stress testing financial systems: What to do when the governor calls.International Monetary Fund (IMF)

2004

-

[22]

Kelly,R.,&O’Malley,T.(2016).Thegood,thebadandtheimpaired:Acreditriskmodeloftheirishmortgage market.Journal of Financial Stability,22, 1–9.https://doi.org/10.1016/j.jfs.2015.09.005

-

[23]

Muller, M., & Botha, A. (2026). An extendable, integrated, and dynamic approach to forecasting and stress-testing credit risk [source code]

2026

-

[24]

NCA. (2015). National Credit Act (NCA): Regulations: Review of limitations of fees and interest rates [Pretoria: Government Printer].https://www.gov.za/sites/default/files/gcis_document/ 201511/39379gon1080.pdf

2015

-

[25]

Norris, J. R. (1997).Markov chains. Cambridge University Press. https : / / doi . org / 10 . 1017 / CBO9780511810633

1997

-

[26]

Rosch, D., & Scheule, H. (2007). Stress-testing credit risk parameters: An application to retail loan portfolios. Journal of Risk Model Validation,1, 55–75

2007

-

[27]

Smith, L. D., & Lawrence, E. C. (1995). Forecasting losses on a liquidating long-term loan portfolio.Journal of Banking & Finance,19(6), 959–985.https://doi.org/10.1016/0378-4266(94)00065-B

-

[28]

Sorge, M., & Virolainen, K. (2006). A comparative analysis of macro stress-testing methodologies with application to finland.Journal of Financial Stability,2, 113–151. 23

2006

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.