Partial Information in a Mean-Variance Portfolio Selection Game

Pith reviewed 2026-05-24 05:44 UTC · model grok-4.3

The pith

Mean-variance investors with relative performance criteria achieve Nash equilibrium strategies that incorporate a filter for hidden expected returns under partial information.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

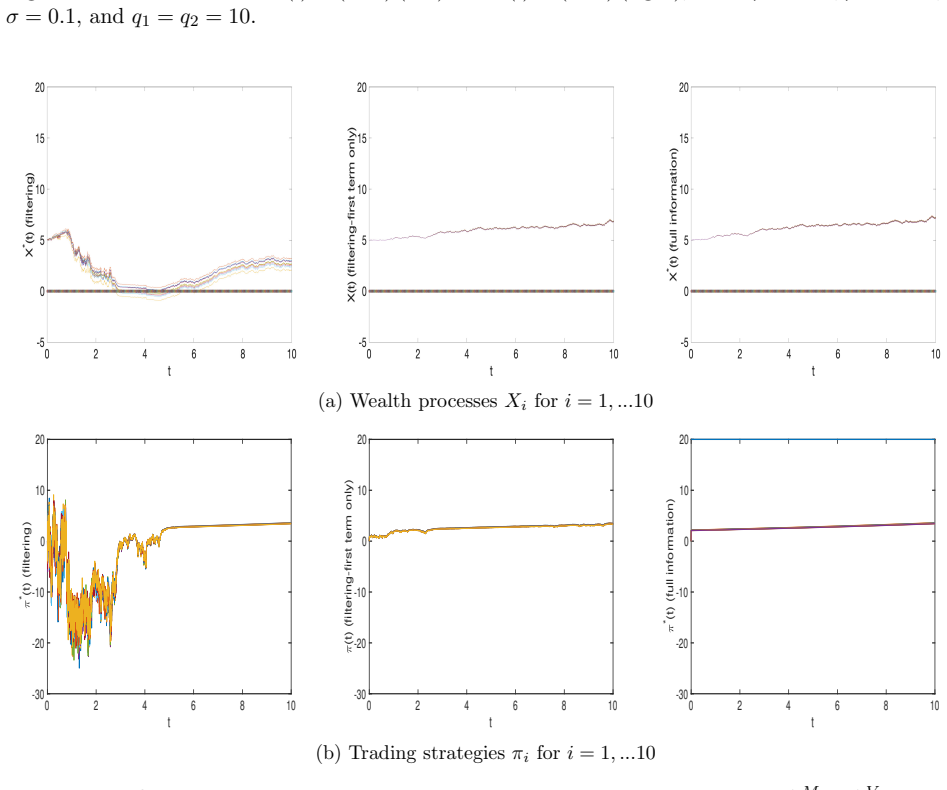

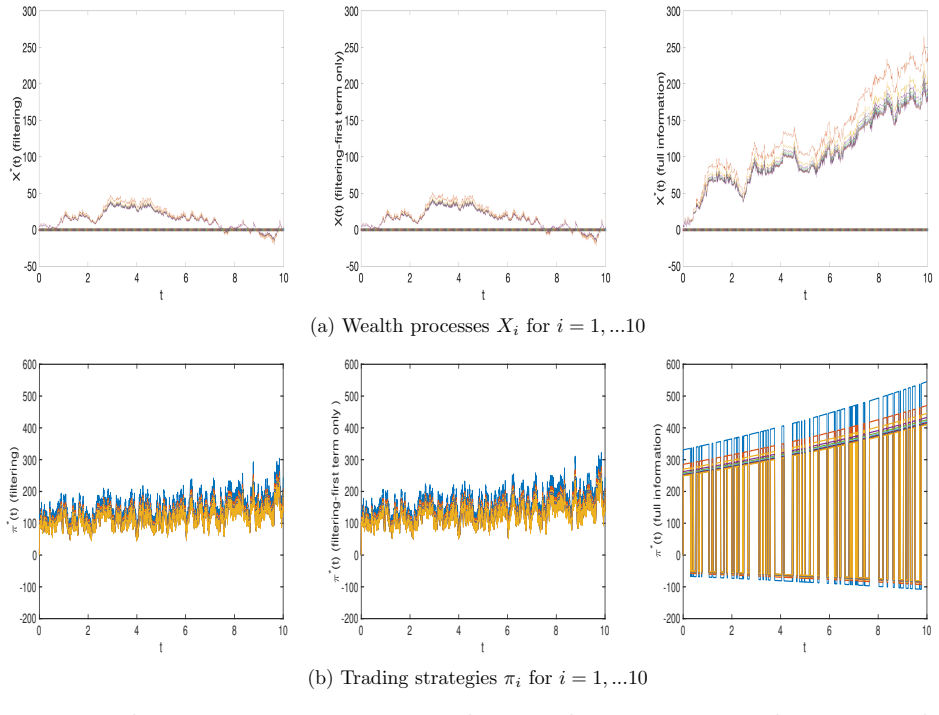

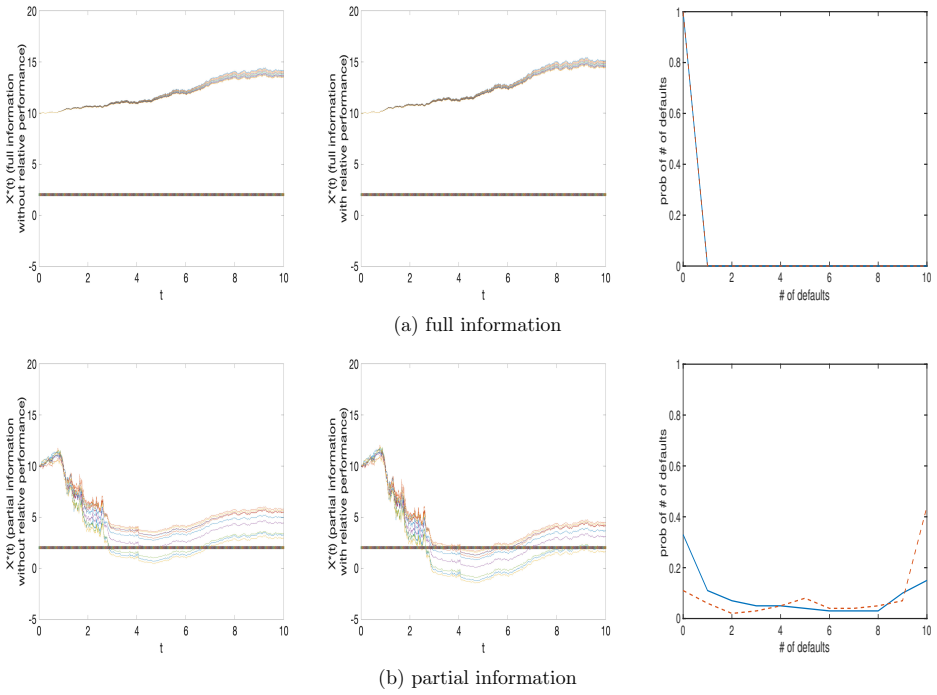

A Nash equilibrium exists for the mean-variance portfolio game with relative performance criteria. In the full-information case the equilibrium strategies are derived explicitly. In the partial-information case the equilibrium strategies consist of myopic trading and intertemporal hedging terms, both depending on an additional state process that filters the true expected return, with this dependence captured by a degenerate Cauchy problem. The analysis further shows that relative performance criteria induce downward self-reinforcement of investors' wealth, negligible under full information but pronounced under partial information.

What carries the argument

The additional state process that filters the true expected return from observed stock prices and enters both the myopic and hedging terms of the equilibrium strategies through a degenerate Cauchy problem.

If this is right

- The equilibrium strategies simultaneously satisfy inter-personal Nash conditions and intra-personal time consistency.

- Relative performance criteria induce downward self-reinforcement of wealth across investors.

- The self-reinforcement effect remains negligible when stock dynamics are fully known but becomes pronounced when the expected return must be filtered.

- Numerical examples confirm that the reinforcement is visible primarily under partial information.

Where Pith is reading between the lines

- In real markets with noisy return observations, relative-performance benchmarks may amplify collective wealth drops during downturns.

- The filtering construction could be applied to other time-inconsistent games that involve unobserved parameters.

- Allowing the hidden expected return to follow its own stochastic dynamics might change the strength of the observed self-reinforcement.

Load-bearing premise

The expected return of the stock is a hidden constant or process that can be filtered from price observations to produce a solvable degenerate Cauchy problem whose solution supplies the Nash equilibrium strategies.

What would settle it

A numerical simulation or market dataset in which the derived partial-information strategies fail to satisfy the simultaneous Nash and time-consistency conditions or in which wealth declines do not exhibit the predicted self-reinforcement.

Figures

read the original abstract

This paper considers finitely many investors who perform mean-variance portfolio selection under relative performance criteria. That is, each investor is concerned about not only her terminal wealth, but how it compares to the average terminal wealth of all investors. At the inter-personal level, each investor selects a trading strategy in response to others' strategies. This selected strategy additionally needs to yield an equilibrium intra-personally, so as to resolve time inconsistency among the investor's current and future selves (triggered by the mean-variance objective). A Nash equilibrium we look for is thus a tuple of trading strategies under which every investor achieves her intra-personal equilibrium simultaneously. We derive such a Nash equilibrium explicitly in the idealized case of full information (i.e., the dynamics of the underlying stock is perfectly known) and semi-explicitly in the realistic case of partial information (i.e., the stock evolution is observed, but the expected return of the stock is not precisely known). The formula under partial information consists of the myopic trading and intertemporal hedging terms, both of which depend on an additional state process that serves to filter the true expected return and whose influence on trading is captured by a degenerate Cauchy problem. Our results identify that relative performance criteria can induce downward self-reinforcement of investors' wealth--if every investor suffers a wealth decline simultaneously, then everyone's wealth tends to decline further. This phenomenon, as numerical examples show, is negligible under full information but pronounced under partial information.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies a multi-investor mean-variance portfolio selection game under relative performance criteria, where each investor seeks a Nash equilibrium that is simultaneously an intra-personal equilibrium to resolve time inconsistency. Explicit equilibria are derived under full information; under partial information the equilibria are semi-explicit, consisting of myopic and intertemporal hedging demands that depend on a filter process for the unknown expected return and are obtained by solving a degenerate Cauchy problem. Numerical examples illustrate a downward self-reinforcement effect in wealth that is negligible under full information but pronounced under partial information.

Significance. If the central constructions hold, the work contributes to the literature on time-inconsistent multi-agent stochastic control by providing explicit and semi-explicit characterizations that incorporate filtering under incomplete information. The identification of the downward reinforcement phenomenon, supported by numerics, offers a concrete mechanism by which relative performance concerns can amplify coordinated wealth declines, with potential relevance for models of market stability and herding. The use of standard filtering combined with equilibrium analysis is a methodological strength.

major comments (1)

- [Abstract] Abstract (and the partial-information construction): the semi-explicit Nash equilibrium under partial information is obtained by expressing myopic and hedging demands via a filter process whose influence is captured by a degenerate Cauchy problem, yet no details are supplied on the precise degeneracy structure, existence/uniqueness of solutions, or regularity of the resulting value function and feedback controls. Because these objects are required to define the candidate equilibrium strategies, the absence of such analysis is load-bearing for the central claim in the partial-information case.

Simulated Author's Rebuttal

We thank the referee for the detailed reading and for highlighting the need for greater rigor in the partial-information analysis. We address the major comment below and will revise the manuscript accordingly.

read point-by-point responses

-

Referee: [Abstract] Abstract (and the partial-information construction): the semi-explicit Nash equilibrium under partial information is obtained by expressing myopic and hedging demands via a filter process whose influence is captured by a degenerate Cauchy problem, yet no details are supplied on the precise degeneracy structure, existence/uniqueness of solutions, or regularity of the resulting value function and feedback controls. Because these objects are required to define the candidate equilibrium strategies, the absence of such analysis is load-bearing for the central claim in the partial-information case.

Authors: We agree that the abstract is high-level and that the partial-information construction requires explicit justification of the degenerate Cauchy problem to support the candidate equilibria. In the body (Section 4), the filter is the Kalman-Bucy estimate of the unknown drift; the associated HJB equation is degenerate because the second-derivative matrix of the value function has a one-dimensional kernel induced by the linear dependence between wealth and the relative-performance term. Existence and uniqueness of a classical solution are established in Theorem 4.3 via a contraction-mapping argument on a suitably weighted Banach space, using the boundedness of the filter process and standard Schauder estimates away from the degeneracy locus. The resulting value function is C^{1,2} in the interior of the state space, which guarantees that the myopic and hedging feedback controls are Lipschitz and admissible. Nevertheless, these arguments currently appear only in outline form. In the revision we will (i) state the precise degeneracy structure (rank deficiency of the diffusion matrix) already in the abstract, (ii) move the key steps of the existence/uniqueness proof into the main text, and (iii) add a short paragraph on the regularity of the feedback map. These changes will make the central claim self-contained. revision: yes

Circularity Check

No circularity: derivations follow from primitives via standard filtering and PDE methods

full rationale

The paper constructs Nash equilibria explicitly under full information and semi-explicitly under partial information by applying standard stochastic filtering to the hidden expected return process and solving the resulting degenerate Cauchy problem for the value function, which yields the myopic and intertemporal hedging demands. These steps are obtained directly from the model dynamics, relative performance criteria, and time-inconsistency resolution without any self-definitional reductions, fitted inputs relabeled as predictions, or load-bearing self-citations that collapse the claimed result to its own inputs. The derivation chain remains self-contained against external benchmarks such as classical filtering theory and mean-variance control.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Asset prices follow dynamics allowing filtering of an unknown expected return via a state process governed by a degenerate Cauchy problem

- domain assumption A Nash equilibrium of intra-personally time-consistent strategies exists in both full and partial information cases

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The formula under partial information consists of the myopic trading and intertemporal hedging terms, both of which depend on an additional state process that serves to filter the true expected return and whose influence on trading is captured by a degenerate Cauchy problem.

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

A Nash equilibrium we look for is thus a tuple of trading strategies under which every investor achieves her intra-personal equilibrium simultaneously.

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

A. Arundel and I. Kabla , What percentage of innovations are patented? empirical estimates for european firms , Research Policy, 27 (1998), pp. 127--141

work page 1998

-

[2]

F. Biagini, A. Mazzon, and T. Meyer-Brandis , Financial asset bubbles in banking networks , SIAM Journal on Financial Mathematics, 10 (2019), pp. 430--465

work page 2019

-

[3]

Time Inconsistent Stochastic Control in Continuous Time: Theory and Examples

T. Bj\" o rk, K. Khapko, and A. Murgoci , On time-inconsistent stochastic control in continuous time: theory and examples , arXiv:1612.03650, (2016)

work page internal anchor Pith review Pith/arXiv arXiv 2016

- [4]

-

[5]

A. Capponi, X. Sun, and D. D. Yao , A dynamic network model of interbank lending , Mathematics of Operations Research, 45 (2020), pp. 1--26

work page 2020

-

[6]

R. Carmona, J. P. Fouque, M. Mousafa, and L.-H. Sun , Systemic risk and stochastic games with delay , Journal of Optimization Theory and Applications, 179 (2018), pp. 366--399

work page 2018

-

[7]

R. Carmona, J. P. Fouque, and L.-H. Sun , Mean field games and systemic risk , Communications in Mathematical Sciences, 13 (2015), pp. 911--933

work page 2015

-

[8]

X. Chen, Y.-J. Huang, Q. Song, and C. Zhu , The stochastic solution to a C auchy problem for degenerate parabolic equations , J. Math. Anal. Appl., 451 (2017), pp. 448--472

work page 2017

-

[9]

M. Dai, Q. Zhang, and Q. J. Zhu , Trend following trading under a regime switching model , SIAM Journal on Financial Mathematics, 1 (2010), pp. 780--810

work page 2010

-

[10]

G.-E. Espinosa and N. Touzi , Optimal investment under relative performance concerns , Mathematical Finance, 25 (2015), pp. 221--257

work page 2015

-

[11]

F. Fang, Y. Sun, and K. Spiliopoulous , On the effect of heterogeneity on flocking behavior and systemic risk , Statistics & Risk Modeling, 34 (2017), pp. 144--155

work page 2017

-

[12]

Z. Feinstein and A. Sojmark , A dynamic default contagion model: from E isenberg- N oe to the mean field , arXiv:1912.08695, (2019)

-

[13]

J. P. Fouque and T. Ichiba , Stability in a model of inter-bank lending , SIAM Journal on Financial Mathematics, 4 (2013), pp. 784--803

work page 2013

-

[14]

J.-P. Fouque and J. Langsam , Handbook on Systemic Risk , Cambridge University Press, 2013

work page 2013

-

[15]

J.-P. Fouque and L.-H. Sun , Systemic risk illustrated , Handbook on Systemic Risk, Eds J.-P. Fouque and J. Langsam, (2013), pp. 444--452

work page 2013

-

[16]

A. Friedman , Partial differential equations of parabolic type , Prentice-Hall, Inc., Englewood Cliffs, NJ, 1964

work page 1964

-

[17]

height 2pt depth -1.6pt width 23pt, Stochastic differential equations and applications. V ol. 1 , vol. Vol. 28 of Probability and Mathematical Statistics, Academic Press [Harcourt Brace Jovanovich, Publishers], New York-London, 1975

work page 1975

-

[18]

J. Garnier, G. Papanicolaou, and T.-W. Yang , Diversification in financial networks may increase systemic risk , Handbook on Systemic Risk, Eds J.-P. Fouque and J. Langsam, (2013), pp. 432--443

work page 2013

- [19]

-

[20]

height 2pt depth -1.6pt width 23pt, A risk analysis for a system stabilized by a central agent , Risk and Decision Analysis, 6 (2017), pp. 97--120

work page 2017

-

[21]

Y.-J. Huang and Z. Wang , Optimal equilibria for multidimensional time-inconsistent stopping problems , SIAM J. Control Optim., 59 (2021), pp. 1705--1729

work page 2021

-

[22]

Y.-J. Huang and Z. Zhou , The optimal equilibrium for time-inconsistent stopping problems--the discrete-time case , SIAM Journal on Control and Optimization, 57 (2019), pp. 590--609

work page 2019

-

[23]

height 2pt depth -1.6pt width 23pt, Optimal equilibria for time-inconsistent stopping problems in continuous time , Mathematical Finance, 30 (2020), pp. 1103--1134

work page 2020

- [24]

-

[25]

I. Karatzas and S. E. Shreve , Brownian Motion and Stochastic Calculus Second Edition , Springer-Verlag New York, Springer Science+Business Media New York, 1991

work page 1991

-

[26]

C. Kardaras and S. Robertson , Robust maximization of asymptotic growth , Ann. Appl. Probab., 22 (2012), pp. 1576--1610

work page 2012

- [27]

-

[28]

D. Lacker and T. Zariphopoulou , Mean field and n-agent games for optimal investment under relative performance criteria , Mathematical Finance, 29 (2019), pp. 1003--1038

work page 2019

-

[29]

G. M. Lieberman , Second order parabolic differential equations , World Scientific Publishing Co., Inc., River Edge, NJ, 1996

work page 1996

-

[30]

R. S. Liptser and A. N. Shiryaev , Statistics of random processes II: Applications, volume 6 , Springer-Verlag New York, Springer Science+Business Media New York, 2013

work page 2013

-

[31]

Pham , Optimal stopping of controlled jump diffusion processes: a viscosity solution approach , J

H. Pham , Optimal stopping of controlled jump diffusion processes: a viscosity solution approach , J. Math. Systems Estim. Control, 8 (1998), pp. 1--27

work page 1998

-

[32]

61 of Stochastic Modelling and Applied Probability, Springer-Verlag, Berlin, 2009

height 2pt depth -1.6pt width 23pt, Continuous-time stochastic control and optimization with financial applications , vol. 61 of Stochastic Modelling and Applied Probability, Springer-Verlag, Berlin, 2009

work page 2009

-

[33]

L.-H. Sun , Systemic risk and interbank lending , Journal of Optimization Theory and Applications, 179 (2018), pp. 400--424

work page 2018

- [34]

-

[35]

W. M. Wonham , Some applications of stochastic differential equations to optimal nonlinear filtering , SIAM Journal on Control and Optimization, 2 (1965), pp. 347--369

work page 1965

-

[36]

X. Y. Zhou and G. Yin , Markowitz's mean-variance portfolio selection with regime switching: a continuous-time model , SIAM Journal on Control and Optimization, 42 (2003), pp. 1466--1482

work page 2003

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.