Faster Monotone Implied Volatility Solver

Pith reviewed 2026-05-22 01:52 UTC · model grok-4.3

The pith

A monotone Euler-Chebyshev iteration starting from a lower-bound seed solves for Black-Scholes implied volatility with guaranteed convergence in exact arithmetic.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

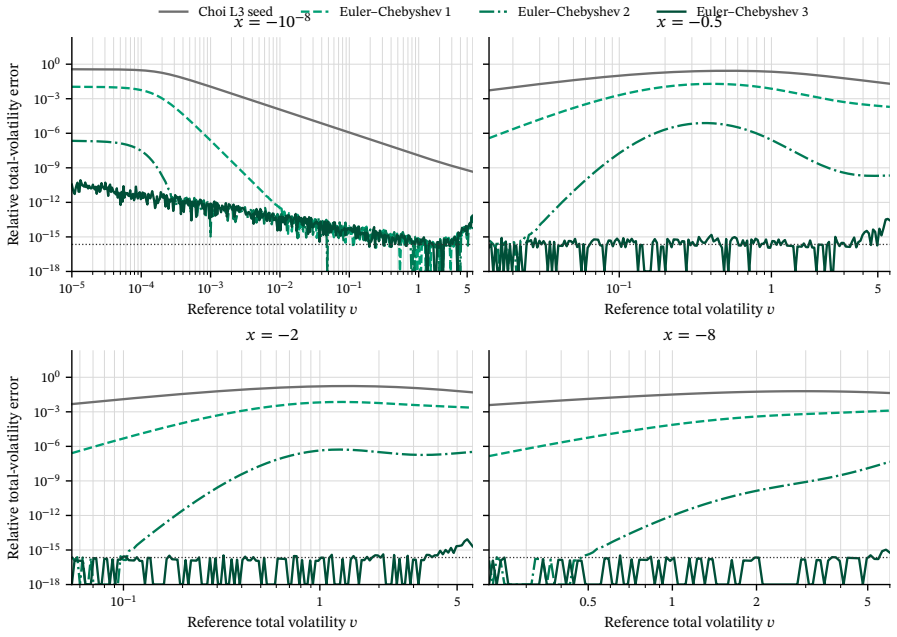

The central claim is that after normalising prices to Jäckel's out-of-the-money form and using a tail-stable logarithmic equation, the Choi-Huh-Su L3 lower-bound seed combined with three Euler-Chebyshev corrections yields a strictly increasing sequence that remains below the admissible root in exact arithmetic, as proven in the paper. The implementation incorporates parity normalisation, Bachelier-limit handling, saturated-price treatment, and other guards to make it robust for production, with an optional final Newton polish for higher accuracy.

What carries the argument

The Euler-Chebyshev correction map applied iteratively to the logarithmic price residual after out-of-the-money normalisation.

If this is right

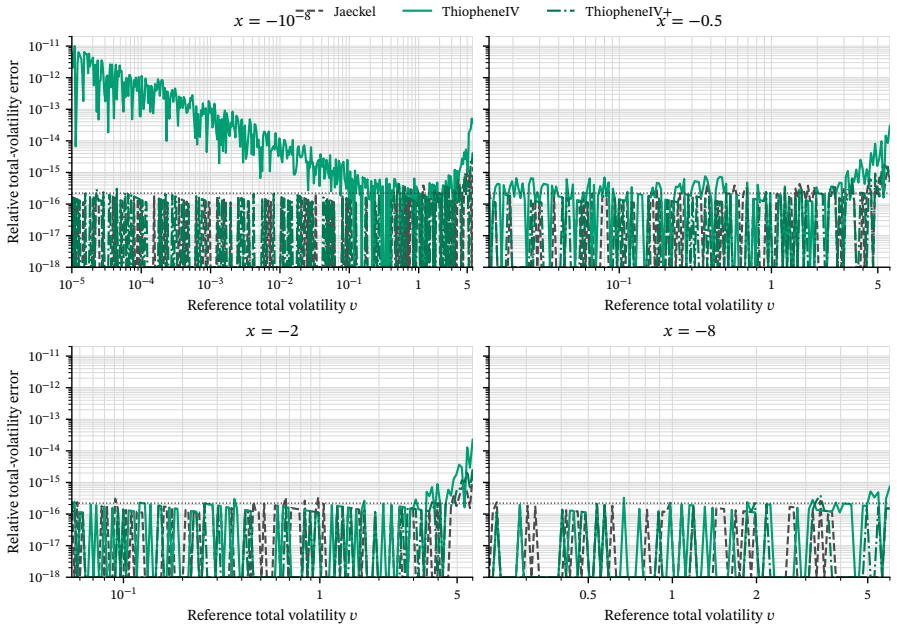

- The solver achieves higher speed than a Java port of Jäckel's Let's Be Rational while maintaining close agreement on regular-grid errors.

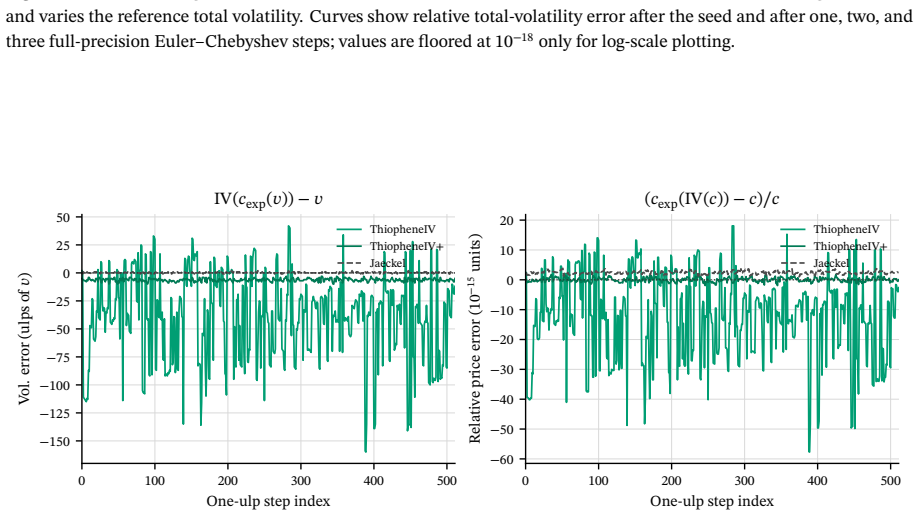

- ThiopheneIV+ with the extra Jäckel-Newton correction provides closer match to the expanded Jäckel reference price.

- The separation of the provable monotone core from boundary-handling guards allows clean extension to other inversion problems.

- Robust production use requires careful treatment of microscopic prices, parity, and saturation cases to preserve the theoretical properties.

Where Pith is reading between the lines

- Similar monotone iteration proofs could be developed for implied volatility in more complex models such as stochastic volatility.

- The emphasis on explicit guards highlights the gap between exact-arithmetic theory and floating-point implementation that affects many numerical finance tools.

- Adopting this approach might reduce the need for ad-hoc adjustments in real-time pricing engines.

Load-bearing premise

The floating-point guards for parity, limits, saturation, and updates preserve the monotonicity and performance benefits when the solver processes actual market data on standard hardware.

What would settle it

A direct computation in arbitrary-precision arithmetic showing whether the three Euler-Chebyshev steps ever overshoot the root or decrease for some valid input price and parameters.

Figures

read the original abstract

We present ThiopheneIV, a Black-Scholes implied-volatility solver with a monotone core and explicit production guards. The solver starts from the simple Choi-Huh-Su L3 lower-bound seed and applies three Euler-Chebyshev steps on a lower branch and three Halley steps on the remaining upper branch. We prove that, in exact arithmetic, the seed lies below the root and both maps increase monotonically without overshooting. We also detail the practical challenges encountered for a double-precision implementation: parity normalisation, microscopic Bachelier-limit handling, saturated price treatment, and an optional J\"ackel-Newton polish. Across standard grids, market-like data, high-volatility cases, and adversarial corners, ThiopheneIV agrees closely with multiprecision Black reference prices at low latency. We provide detailed comparisons with recent solvers, including J\"ackel's Let's Be Rational. The broader lesson is that a convergence proof gives a clean core, but robust production inversion still depends on boundary handling and on the pricing objective one chooses to match.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript presents ThiopheneIV, a Black-Scholes implied-volatility solver that first reduces prices to Jäckel's out-of-the-money normalisation and inverts a tail-stable logarithmic price equation. The core algorithm starts from the non-iterative Choi-Huh-Su L3 lower-bound seed and applies three Euler-Chebyshev corrections. A proof is supplied that, in exact arithmetic, the seed lies below the admissible root and the Euler-Chebyshev map increases monotonically without overshooting. The implementation augments this core with floating-point guards (parity normalisation, microscopic Bachelier-limit handling, saturated-price treatment, finite-update checks, fallback seeds) and offers an optional Jäckel-Newton polish. Against an expanded Jäckel reference price, the guarded solver is reported faster than a Java port of Jäckel's Let's Be Rational while keeping regular-grid errors close.

Significance. If the monotonicity property and accuracy claims survive the floating-point guards, the work supplies a rigorously grounded, production-ready implied-volatility solver whose exact-arithmetic proof constitutes a clear methodological advance over purely heuristic or iterative methods. The reported speed advantage over Let's Be Rational would be practically relevant for high-volume pricing engines. The explicit separation of the provable core from the necessary boundary machinery is a useful architectural lesson for numerical finance software.

major comments (2)

- [Implementation description and floating-point guards] The central guarantee is the exact-arithmetic monotonicity proof for the Choi-Huh-Su L3 seed plus three Euler-Chebyshev steps. The manuscript states that the production solver inserts parity normalisation, microscopic Bachelier-limit handling, saturated-price treatment, finite-update checks and fallback seeds, yet provides no analysis or numerical test demonstrating that these guards preserve monotonicity or prevent overshoot when the price is near machine epsilon, exactly at the Bachelier limit, or when the log-price equation underflows. Because the headline speed/accuracy comparisons are performed on the guarded code, this gap is load-bearing for the claim of a 'monotone' production solver.

- [Results and benchmark comparisons] The abstract and results summary assert that regular-grid errors remain 'close' to the expanded Jäckel reference, but no quantitative error tables, maximum absolute or relative errors, or full benchmark data (including timing distributions across volatility and moneyness ranges) are supplied. Without these data it is difficult to judge whether the observed speed gain is achieved at an acceptable accuracy cost for the intended use cases.

minor comments (2)

- [Core algorithm] The notation used for the tail-stable logarithmic price equation is introduced at a high level; an explicit formula with all variables defined would improve readability.

- [Proof section] A short table summarising the exact-arithmetic proof steps (seed bound, monotonicity of each Euler-Chebyshev update, non-overshoot) would make the mathematical contribution easier to verify at a glance.

Simulated Author's Rebuttal

We thank the referee for the thoughtful review and valuable suggestions. We address the major comments point by point below and outline the changes we will make to the manuscript.

read point-by-point responses

-

Referee: [Implementation description and floating-point guards] The central guarantee is the exact-arithmetic monotonicity proof for the Choi-Huh-Su L3 seed plus three Euler-Chebyshev steps. The manuscript states that the production solver inserts parity normalisation, microscopic Bachelier-limit handling, saturated-price treatment, finite-update checks and fallback seeds, yet provides no analysis or numerical test demonstrating that these guards preserve monotonicity or prevent overshoot when the price is near machine epsilon, exactly at the Bachelier limit, or when the log-price equation underflows. Because the headline speed/accuracy comparisons are performed on the guarded code, this gap is load-bearing for the claim of a 'monotone' production solver.

Authors: We agree that the monotonicity proof applies strictly to exact arithmetic and that the production guards require explicit justification to support the claim for the guarded solver. The guards are constructed to intervene only in regimes where the core map would otherwise produce NaN, negative updates, or invalid results, and they are designed to return values that remain below the admissible root (e.g., via safe clamping or fallback seeds that inherit the lower-bound property). Nevertheless, we acknowledge that the manuscript currently lacks a dedicated analysis or targeted numerical verification for these edge cases. In the revision we will add a subsection that examines each guard's effect on monotonicity together with numerical experiments confirming absence of overshoot near machine epsilon, at the Bachelier limit, and under log-price underflow. This will directly address the load-bearing nature of the claim. revision: yes

-

Referee: [Results and benchmark comparisons] The abstract and results summary assert that regular-grid errors remain 'close' to the expanded Jäckel reference, but no quantitative error tables, maximum absolute or relative errors, or full benchmark data (including timing distributions across volatility and moneyness ranges) are supplied. Without these data it is difficult to judge whether the observed speed gain is achieved at an acceptable accuracy cost for the intended use cases.

Authors: We agree that quantitative error metrics and comprehensive benchmark statistics are necessary for readers to evaluate the speed-accuracy trade-off. The current manuscript reports only that errors remain 'close' on regular grids. In the revised version we will expand the results section with tables of maximum absolute and relative errors stratified by volatility and moneyness, together with timing distributions (means, medians, and tails) across the tested ranges. These additions will make the accuracy cost explicit and allow direct comparison with the expanded Jäckel reference. revision: yes

Circularity Check

No significant circularity; core monotonicity claim rests on supplied independent proof

full rationale

The paper's central derivation chain consists of a non-iterative seed (Choi-Huh-Su L3) followed by three Euler-Chebyshev iterations whose monotonicity and non-overshooting property in exact arithmetic is asserted via an included mathematical proof. This proof is presented as external to the implementation and does not reduce to a fitted parameter, a self-referential definition, or a load-bearing self-citation. The floating-point guards (parity normalisation, Bachelier handling, etc.) are described as practical additions whose interaction with the exact-arithmetic guarantee is not claimed to be proven; however, this is a robustness question rather than a circularity in the derivation itself. Performance claims are benchmarked against an external expanded Jäckel reference, keeping the core argument self-contained.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math The Black-Scholes price function is strictly monotone in volatility for fixed strike and maturity.

- domain assumption Floating-point arithmetic with the listed guards preserves the ordering and convergence properties established in exact arithmetic.

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.