Decomposing Financial Market Dynamics via Mechanism Analysis in an Evolutionary Multi-Agent Simulation

Pith reviewed 2026-06-26 08:36 UTC · model grok-4.3

The pith

In an evolutionary agent-based market with pluggable mechanisms, selection controls diversity while price feedback controls realism and bias controls fragility.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

In single-mechanism sweeps the mechanisms behave as approximately distinct control knobs: Quality-Diversity selection raises strategy-mix entropy and sustains cycling, reflexive price feedback raises the 5-fact realism score, behavioral bias amplification raises the genomic fragility proxy, and consensus network topology produces no robust change, while selection leaves realism unchanged even when steered by a per-agent reward.

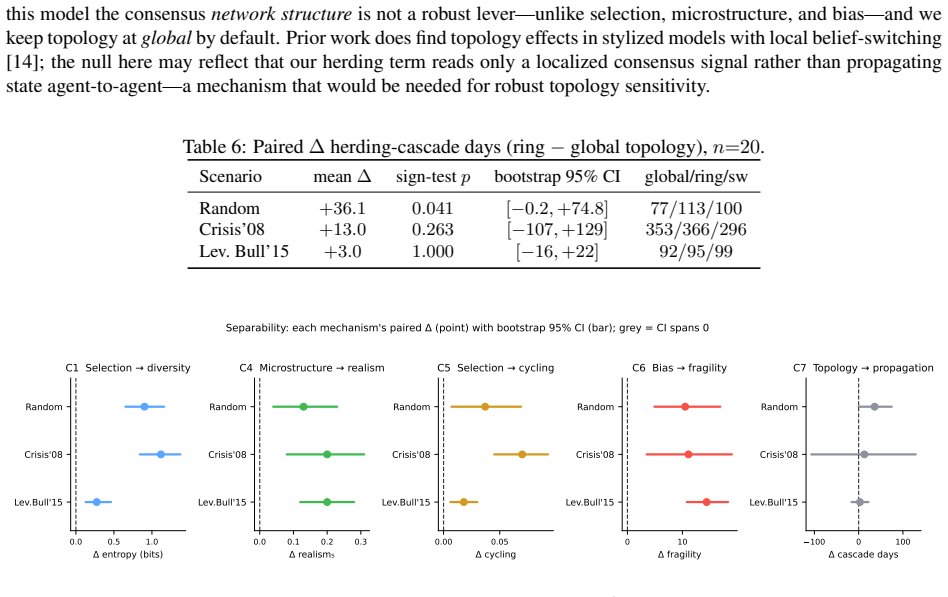

What carries the argument

The four pluggable mechanisms (selection operator, price formation via reflexive feedback, behavioral bias level, and consensus network topology) that are toggled independently while holding the rest of the 120-agent endogenous-price simulator fixed.

If this is right

- Quality-Diversity selection raises strategy-mix entropy by 0.27 to 1.12 bits and sustains more strategy cycling than truncation selection.

- Enabling reflexive price feedback raises the 5-fact realism score by 0.13 to 0.20, with effects visible in crisis and bull regimes.

- Amplifying behavioral bias raises the genomic fragility proxy by 10.5 to 14.4 while leaving the realism score flat.

- Consensus network topology produces no robust change in the measured properties across the tested conditions.

- Even a selection operator that includes an explicit per-agent realism reward does not raise the 5-fact realism score.

Where Pith is reading between the lines

- The separation suggests simulators could be designed with modular toggles so that increasing diversity does not automatically alter realism or fragility.

- The same decomposition approach could be applied to other agent-based models to check whether the control-knob pattern holds beyond this specific setup.

- If the pattern generalizes, builders of market models might first choose the mechanism that targets the property they most want to control rather than tuning all mechanisms at once.

Load-bearing premise

The five-fact realism metric and genomic fragility proxy are valid and sufficient measures of the target market properties.

What would settle it

A replication that applies the same single-mechanism interventions but finds that reflexive price feedback no longer raises the realism score outside the reported confidence intervals or that bias amplification no longer raises the fragility proxy.

Figures

read the original abstract

Evolutionary agent-based markets (ABMs) couple several mechanisms -- who reproduces, how price forms, how biased the agents are, how consensus propagates -- yet these are usually fixed by convention, so it is unclear which mechanism controls which emergent property. In a coevolving, endogenous-price simulator with 120 heterogeneous behavioral agents, we make four mechanisms pluggable and run matched 3x20-seed interventions. We find the levers are largely separable. (1) Selection -> diversity: a Quality-Diversity (QD/MAP-Elites) operator robustly raises strategy-mix entropy over truncation top-k (paired Delta entropy +0.27 to +1.12 bits; sign-test p<0.001; CIs exclude 0) and sustains more strategy cycling (strongest in crisis: Delta=+0.070, p=0.0004). (2) Selection does not improve realism: even a per-agent realism reward that provably steers selection does not raise 5-fact realism (Delta_5=-0.11,-0.08,+0.03; not significant). (3) Microstructure -> realism: enabling reflexive price feedback does raise realism (Delta_5=+0.13,+0.20,+0.20; crisis/bull p<0.05, all CIs positive). (4) Behavior -> fragility: amplifying behavioral bias raises a genomic fragility proxy (Delta=+10.5,+11.1,+14.4; bull p<0.001, all CIs positive) while leaving realism flat. The remaining mechanism -- consensus network topology -- shows no robust effect (honest null). The contribution is a decomposition: in these single-mechanism sweeps the mechanisms behave as approximately distinct control knobs over diversity, realism, and fragility.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that in a coevolving endogenous-price ABM with 120 heterogeneous agents, four pluggable mechanisms (selection, microstructure/price feedback, behavioral bias, consensus topology) function as approximately separable control knobs. Matched 3x20-seed single-mechanism interventions show: (1) Quality-Diversity selection raises strategy entropy (+0.27 to +1.12 bits) and cycling; (2) selection does not raise 5-fact realism; (3) reflexive price feedback raises 5-fact realism (+0.13 to +0.20); (4) amplified bias raises genomic fragility (+10.5 to +14.4) while leaving realism unchanged; consensus yields a null. The contribution is this empirical decomposition of mechanism effects on diversity, realism, and fragility.

Significance. If the 5-fact realism metric and genomic fragility proxy are valid, the work would offer a useful systematic decomposition of how distinct mechanisms drive specific emergent properties in evolutionary market ABMs, aiding model construction and interpretation. The controlled single-mechanism sweeps with reported deltas, sign-test p-values, and CIs constitute a methodological strength over conventional fixed-mechanism simulations.

major comments (2)

- [Abstract, findings 2-4] Abstract, findings 2-4: The separability interpretation (microstructure controls realism; behavior controls fragility; selection does not control realism) is load-bearing on the assumption that the 5-fact realism aggregation and genomic fragility proxy track the intended market properties. No external validation, correlation with established market statistics, or sensitivity analysis for these proxies is reported, so the observed deltas cannot yet be read as evidence of control over the target constructs.

- [Abstract] Abstract: Multiple sign-test p-values and CIs are reported across metrics, market regimes (crisis/bull), and mechanisms without reference to pre-specification of the analysis or adjustment for multiple comparisons. This affects the strength of claims such as p<0.001 for behavioral bias on fragility and p=0.0004 for selection on crisis cycling.

minor comments (1)

- [Abstract] The phrase 'honest null' for the consensus topology result is nonstandard; replace with a clearer description of the statistical outcome.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed report. The two major comments identify important limitations in how the separability claims are supported. We respond point-by-point below and indicate where revisions will be made.

read point-by-point responses

-

Referee: [Abstract, findings 2-4] Abstract, findings 2-4: The separability interpretation (microstructure controls realism; behavior controls fragility; selection does not control realism) is load-bearing on the assumption that the 5-fact realism aggregation and genomic fragility proxy track the intended market properties. No external validation, correlation with established market statistics, or sensitivity analysis for these proxies is reported, so the observed deltas cannot yet be read as evidence of control over the target constructs.

Authors: We agree that the absence of external validation or sensitivity analysis for the 5-fact realism aggregation and genomic fragility proxy limits the strength of the separability interpretation. The metrics are defined in Section 3.3 from standard stylized-fact literature and a genomic-distance measure, but the manuscript does not report correlations with real-market statistics or weight-sensitivity checks. In revision we will add a dedicated Limitations subsection that (i) explicitly states the proxies are internal constructs without external anchoring, (ii) reports a post-hoc sensitivity analysis on the five-fact aggregation weights, and (iii) qualifies the separability language to “under the reported internal metrics.” This change will be reflected in the abstract and discussion as well. revision: yes

-

Referee: [Abstract] Abstract: Multiple sign-test p-values and CIs are reported across metrics, market regimes (crisis/bull), and mechanisms without reference to pre-specification of the analysis or adjustment for multiple comparisons. This affects the strength of claims such as p<0.001 for behavioral bias on fragility and p=0.0004 for selection on crisis cycling.

Authors: The reported sign-tests correspond to the four pre-planned single-mechanism interventions described in Section 4.1, each evaluated on the same fixed set of metrics and regimes. However, the manuscript does not declare an analysis plan, apply multiplicity corrections, or label the tests as exploratory. We will revise the abstract, Section 4, and the supplementary methods to (i) state that the p-values are uncorrected, (ii) report Bonferroni-adjusted thresholds for the 12 primary comparisons, and (iii) replace absolute claims (“p<0.001”) with “uncorrected p<0.001” where appropriate. These textual changes will be made without altering the underlying numerical results. revision: yes

Circularity Check

No significant circularity; empirical simulation results independent of inputs

full rationale

The paper reports results from direct single-mechanism interventions in an agent-based simulator, with statistical comparisons (e.g., paired deltas, sign-tests, CIs) on output metrics like entropy, 5-fact realism, and genomic fragility. No equations, fitted parameters, or self-citations are used to derive the separability claims; the findings are generated by running the interventions and measuring deltas. The central claim does not reduce to any input by construction, and the analysis is self-contained against external benchmarks via the simulation design.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The 5-fact realism metric and genomic fragility proxy validly capture the intended real-world market properties.

Reference graph

Works this paper leans on

-

[1]

V . Alfi, M. Cristelli, L. Pietronero, and A. Zaccaria. Minimal agent based model for financial markets I: Origin and self- organization of stylized facts.The European Physical Journal B, 67(3):385–397, 2009. doi: 10.1140/epjb/e2009-00028-4

-

[2]

Asset pricing under endogenous ex- pectations in an artificial stock market

W Brian Arthur, John H Holland, Blake LeBaron, Richard Palmer, and Paul Tayler. Asset pricing under endogenous ex- pectations in an artificial stock market. InThe Economy as an Evolving Complex System II, pages 15–44. Addison-Wesley, 1997

1997

-

[3]

Heterogeneous beliefs and routes to chaos in a simple asset pricing model.Journal of Economic Dynamics and Control, 22(8-9):1235–1274, 1998

William A Brock and Cars H Hommes. Heterogeneous beliefs and routes to chaos in a simple asset pricing model.Journal of Economic Dynamics and Control, 22(8-9):1235–1274, 1998

1998

-

[4]

Empirical properties of asset returns: stylized facts and statistical issues.Quantitative Finance, 1(2):223–236, 2001

Rama Cont. Empirical properties of asset returns: stylized facts and statistical issues.Quantitative Finance, 1(2):223–236, 2001

2001

-

[5]

A fast and elitist multiobjective genetic algorithm: NSGA-II.IEEE Transactions on Evolutionary Computation, 6(2):182–197, 2002

Kalyanmoy Deb, Amrit Pratap, Sameer Agarwal, and T Meyarivan. A fast and elitist multiobjective genetic algorithm: NSGA-II.IEEE Transactions on Evolutionary Computation, 6(2):182–197, 2002

2002

-

[6]

Tibshirani.An Introduction to the Bootstrap

Bradley Efron and Robert J. Tibshirani.An Introduction to the Bootstrap. Chapman & Hall, New York, 1993. ISBN 0-412- 04231-2

1993

-

[7]

J. Doyne Farmer and Duncan Foley. The economy needs agent-based modelling.Nature, 460(7256):685–686, 2009. doi: 10.1038/460685a

-

[8]

Structural stochastic volatility in asset pricing dynamics: Estimation and model contest

Reiner Franke and Frank Westerhoff. Structural stochastic volatility in asset pricing dynamics: Estimation and model contest. Journal of Economic Dynamics and Control, 36(8):1193–1211, 2012. doi: 10.1016/j.jedc.2011.10.004

-

[9]

Ryuji Hashimoto and Kiyoshi Izumi. Towards realistic and interpretable market simulations: Factorizing financial power law using optimal transport.arXiv preprint arXiv:2507.09863, 2025. doi: 10.48550/arXiv.2507.09863

-

[10]

Cars H. Hommes. Heterogeneous agent models in economics and finance. In Leigh Tesfatsion and Kenneth L. Judd, ed- itors,Handbook of Computational Economics, volume 2, chapter 23, pages 1109–1186. Elsevier, 2006. doi: 10.1016/ S1574-0021(05)02023-X

2006

-

[11]

Agent-based computational finance

Blake LeBaron. Agent-based computational finance. In Leigh Tesfatsion and Kenneth L. Judd, editors,Handbook of Compu- tational Economics, volume 2, chapter 24, pages 1187–1233. Elsevier, 2006. doi: 10.1016/S1574-0021(05)02024-1

-

[12]

Abandoning objectives: Evolution through the search for novelty alone.Evolutionary Computation, 19(2):189–223, 2011

Joel Lehman and Kenneth O Stanley. Abandoning objectives: Evolution through the search for novelty alone.Evolutionary Computation, 19(2):189–223, 2011

2011

-

[13]

Illuminating search spaces by mapping elites.arXiv preprint arXiv:1504.04909, 2015

Jean-Baptiste Mouret and Jeff Clune. Illuminating search spaces by mapping elites.arXiv preprint arXiv:1504.04909, 2015

Pith/arXiv arXiv 2015

-

[14]

Valentyn Panchenko, Sergiy Gerasymchuk, and Oleg V . Pavlov. Asset price dynamics with heterogeneous beliefs and local network interactions.Journal of Economic Dynamics and Control, 37(12):2623–2642, 2013. doi: 10.1016/j.jedc.2013.06.015. 6

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.