Growth rate of liquidity provider's wealth in G3Ms

Pith reviewed 2026-05-24 03:54 UTC · model grok-4.3

The pith

The long-term logarithmic growth rate of liquidity provider wealth in G3Ms is derived from stochastic reflected diffusion models of arbitrage and fees.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

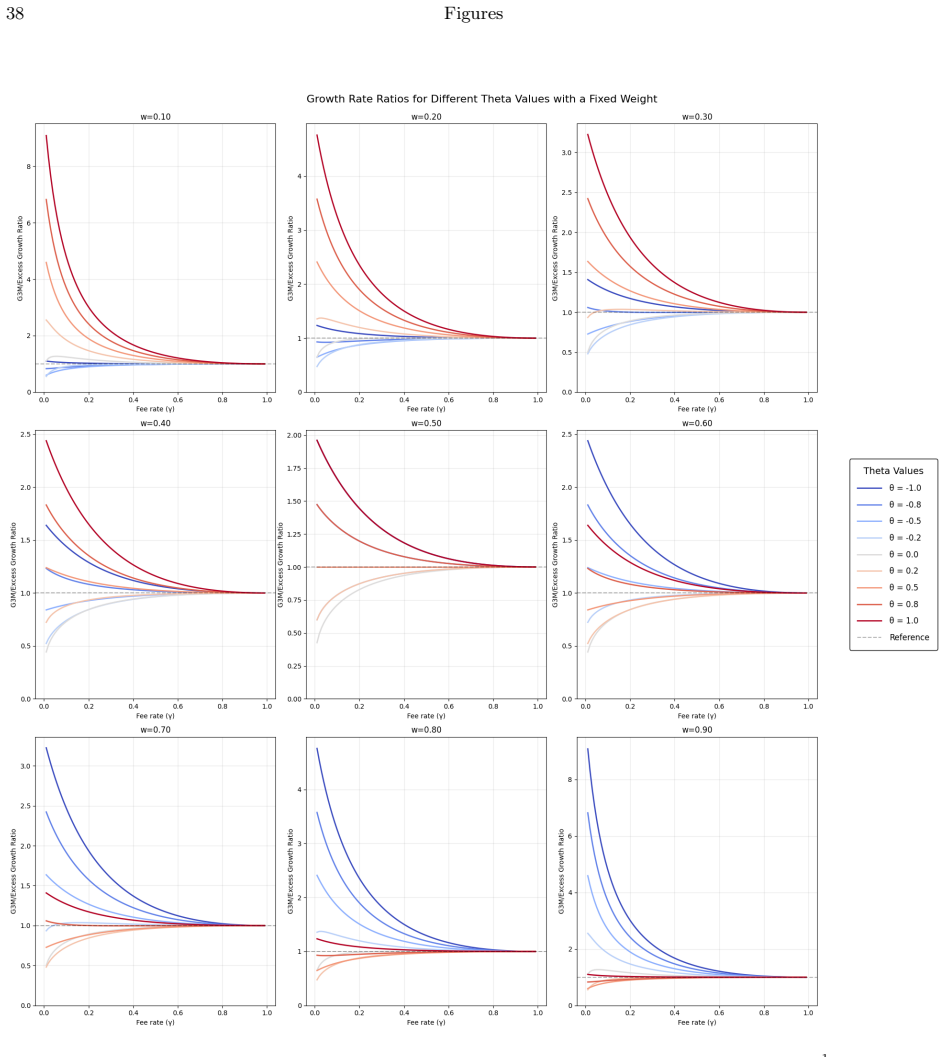

Under an arbitrage-driven market, the reserve vector of a G3M evolves as a stochastic reflected diffusion whose long-term expected logarithmic growth for the liquidity provider equals a closed-form expression linear in the fee rate and determined by the weight vector of the geometric mean.

What carries the argument

Stochastic reflected diffusion process for the reserve vector, with reflection at the no-arbitrage hyperplane and a fee-adjusted drift.

If this is right

- LP profitability increases linearly with the trading fee rate for any fixed weight vector.

- Different weight vectors in a G3M produce different growth rates even under identical external volatility and fee schedules.

- In the zero-fee limit the expected growth rate is non-positive, recovering the constant-product result that LPs lose to arbitrage on average.

- The growth-rate formula supplies a ranking of G3M parameter choices by expected LP return.

Where Pith is reading between the lines

- The same diffusion framework could be used to compare G3M performance against other AMM families once their invariant surfaces are expressed as reflecting boundaries.

- If real markets exhibit discrete block times or latency, the continuous-reflection assumption would need a discrete-time correction term added to the growth formula.

- The model implies that LPs should prefer higher-fee pools when external volatility is fixed, which could be tested by comparing pools with identical assets but different fee tiers.

Load-bearing premise

Arbitrage occurs continuously and instantaneously, so that prices stay exactly aligned with the external market at all times and no discrete jumps or additional trading frictions appear.

What would settle it

A long-horizon empirical time series from a live Balancer pool in which the realized logarithmic wealth growth of LPs deviates systematically from the closed-form expression once fees and observed volatility are plugged in.

Figures

read the original abstract

We study how trading fees and continuous-time arbitrage affect the profitability of liquidity providers (LPs) in Geometric Mean Market Makers (G3Ms). We use stochastic reflected diffusion processes to analyze the dynamics of a G3M model under the arbitrage-driven market. Our research focuses on calculating LP wealth and extends the findings of Tassy and White related to the constant product market maker (Uniswap v2) to a wider range of G3Ms, including Balancer. This allows us to calculate the long-term expected logarithmic growth of LP wealth, offering new insights into the complex dynamics of AMMs and their implications for LPs in decentralized finance.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper models liquidity provider (LP) wealth dynamics in Geometric Mean Market Makers (G3Ms), including Balancer, under continuous arbitrage and trading fees. It extends the constant-product analysis of Tassy and White by representing reserve ratios as stochastic reflected diffusions whose drift is fixed by instantaneous no-arbitrage conditions, then derives a closed-form expression for the long-term expected logarithmic growth rate of LP wealth.

Significance. If the derivation is correct, the result supplies an explicit growth-rate formula that generalizes the Uniswap v2 case to arbitrary weights, which is useful for quantitative assessment of LP returns in weighted AMMs. The modeling choice of reflected diffusions is standard for arbitrage-driven markets, but the paper does not appear to supply machine-checked proofs or reproducible code.

major comments (2)

- [§4] §4, Eq. (15)–(18): the claim that the multi-dimensional reflection at the no-arbitrage boundary contributes no extra local-time term to the log-wealth process is not verified. The extension from the one-dimensional constant-product case requires an explicit Itô–Tanaka expansion or quadratic-variation calculation for the reflected process; without it the growth-rate formula may miss a correction proportional to the local time at the boundary.

- [§3.2] §3.2, definition of the reflection barrier and fee parameters: these quantities are defined via the same instantaneous-arbitrage condition that supplies the drift of the diffusion. The manuscript should show that the resulting growth rate is invariant under small perturbations of the barrier or provide an external benchmark (e.g., discrete-time simulation) to confirm the formula is not an artifact of this modeling choice.

minor comments (2)

- [§2] Notation for the weight vector w and the geometric-mean price process is introduced without a clear reference to the earlier Tassy–White paper; adding a short comparison table would improve readability.

- [§1] The abstract states the target quantity but the introduction does not list the precise assumptions (continuous trading, zero latency, perfect arbitrage) that are later used; a dedicated assumptions paragraph would help.

Simulated Author's Rebuttal

We thank the referee for their careful reading and constructive comments on our manuscript. We address each major comment below and will revise the paper to strengthen the mathematical justification and validation of the results.

read point-by-point responses

-

Referee: [§4] §4, Eq. (15)–(18): the claim that the multi-dimensional reflection at the no-arbitrage boundary contributes no extra local-time term to the log-wealth process is not verified. The extension from the one-dimensional constant-product case requires an explicit Itô–Tanaka expansion or quadratic-variation calculation for the reflected process; without it the growth-rate formula may miss a correction proportional to the local time at the boundary.

Authors: We agree that the multi-dimensional extension requires explicit verification. In the revised manuscript we will add a detailed Itô–Tanaka expansion (or equivalent quadratic-variation calculation) for the reflected diffusion to confirm that the local-time contribution to the log-wealth process remains zero, thereby rigorously supporting the growth-rate formula. revision: yes

-

Referee: [§3.2] §3.2, definition of the reflection barrier and fee parameters: these quantities are defined via the same instantaneous-arbitrage condition that supplies the drift of the diffusion. The manuscript should show that the resulting growth rate is invariant under small perturbations of the barrier or provide an external benchmark (e.g., discrete-time simulation) to confirm the formula is not an artifact of this modeling choice.

Authors: The barrier and fee parameters are defined directly from the instantaneous no-arbitrage condition, which is the core modeling assumption. To address the concern we will include, in the revision, either a first-order perturbation analysis showing invariance of the long-term growth rate or discrete-time Monte Carlo simulations as an external benchmark. revision: yes

Circularity Check

No significant circularity; derivation extends external model without reducing to self-input by construction

full rationale

The paper models G3M dynamics via stochastic reflected diffusions under an arbitrage-driven market assumption and derives the long-term log-growth rate of LP wealth as a mathematical consequence of that process. This extends the Tassy-White constant-product analysis to weighted G3Ms without any quoted step that redefines the target growth rate in terms of itself, renames a fitted parameter as a prediction, or relies on a load-bearing self-citation whose content is unverified. The modeling choice (reflection at no-arbitrage boundaries) is an explicit assumption rather than a tautology that forces the final formula; external benchmarks or independent verification of the SDE solution would falsify the result. No load-bearing step collapses to an input by definition.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Market dynamics under continuous arbitrage are captured by stochastic reflected diffusion processes

Reference graph

Works this paper leans on

-

[1]

Improved price oracles: Constant function market makers

Guillermo Angeris and Tarun Chitra. Improved price oracles: Constant function market makers. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies (AFT '20) , AFT '20, pages 80--91, New York, NY, USA, 2020. Association for Computing Machinery

work page 2020

-

[2]

An analysis of uniswap markets

Guillermo Angeris, Hsien-Tang Kao, Rei Chiang, Charlie Noyes, and Tarun Chitra. An analysis of uniswap markets. arXiv e-prints , 2019

work page 2019

-

[3]

Hayden Adams, Noah Zinsmeister, and Dan Robinson. Uniswap v2 core, 2020

work page 2020

-

[4]

W. Br\" o nnimann, P. Egloff, and T. Krabichler. Automated market makers and their implications for liquidity providers. Digital Finance , 6:573--604, 2024

work page 2024

-

[5]

\' A lvaro Cartea, Fayçal Drissi, and Marcello Monga. Predictable losses of liquidity provision in constant function markets and concentrated liquidity markets. Applied Mathematical Finance , 30(2):69--93, 2023

work page 2023

-

[6]

Decentralized finance and automated market making: Predictable loss and optimal liquidity provision

\' A lvaro Cartea, Fayçal Drissi, and Marcello Monga. Decentralized finance and automated market making: Predictable loss and optimal liquidity provision. SIAM Journal on Financial Mathematics , 15(3):931--959, 2024

work page 2024

-

[7]

The adoption of blockchain-based decentralized exchanges

Agostino Capponi and Ruizhe Jia. The adoption of blockchain-based decentralized exchanges. arXiv e-prints , 2021

work page 2021

-

[8]

Liquidity provider returns in geometric mean markets

Alex Evans. Liquidity provider returns in geometric mean markets. Cryptoeconomic Systems , 1(2), October 2021

work page 2021

-

[9]

E. Robert Fernholz. Stochastic Portfolio Theory , volume 48 of Applications of Mathematics (New York) . Springer-Verlag, New York, 2002

work page 2002

-

[10]

Model-free hedging of impermanent loss in geometric mean market makers

Masaaki Fukasawa, Basile Maire, and Marcus Wunsch. Model-free hedging of impermanent loss in geometric mean market makers. arXiv e-prints , 2023

work page 2023

-

[11]

Weighted variance swaps hedge against impermanent loss

Masaaki Fukasawa, Basile Maire, and Marcus Wunsch. Weighted variance swaps hedge against impermanent loss. Quantitative Finance , 23(6):901--911, 2023

work page 2023

-

[12]

Decentralized finance & blockchain technology

Emmanuel Gobet and Anastasia Melachrinos. Decentralized finance & blockchain technology. In SIAM Financial Mathematics and Engineering 2023 , Philadelphia, United States, 2023

work page 2023

-

[13]

Peter Glynn and Rob Wang. Central limit theorems and large deviations for additive functionals of reflecting diffusion processes. Fields Institute Communications , 76, 2013

work page 2013

-

[14]

J. Michael Harrison. Brownian Models of Performance and Control . Cambridge University Press, Cambridge, 2013

work page 2013

-

[15]

Charles S. Kahane. On the asymptotic behavior of solutions of parabolic equations. Czechoslovak Mathematical Journal , 33(2):262--285, 1983

work page 1983

-

[16]

Stochastic portfolio theory: an overview

Ioannis Karatzas and Robert Fernholz. Stochastic portfolio theory: an overview. In Alain Bensoussan and Qiang Zhang, editors, Special Volume: Mathematical Modeling and Numerical Methods in Finance , volume 15 of Handbook of Numerical Analysis , pages 89--167. Elsevier, 2009

work page 2009

-

[17]

Balancer: A non-custodial portfolio manager, liquidity provider, and price sensor, 2019

Fernando Martinelli and Nikolai Mushegian. Balancer: A non-custodial portfolio manager, liquidity provider, and price sensor, 2019

work page 2019

-

[18]

Jason Milionis, Ciamac C. Moallemi, and Tim Roughgarden. Automated market making and arbitrage profits in the presence of fees. arXiv e-prints , 2023

work page 2023

-

[19]

Moallemi, Tim Roughgarden, and Anthony Lee Zhang

Jason Milionis, Ciamac C. Moallemi, Tim Roughgarden, and Anthony Lee Zhang. Automated market making and loss-versus-rebalancing. arXiv e-prints , 2022

work page 2022

-

[20]

Moallemi, Tim Roughgarden, and Anthony Lee Zhang

Jason Milionis, Ciamac C. Moallemi, Tim Roughgarden, and Anthony Lee Zhang. Quantifying loss in automated market makers. In Proceedings of the 2022 ACM CCS Workshop on Decentralized Finance and Security (DeFi'22) , pages 71--74, New York, NY, USA, 2022. Association for Computing Machinery

work page 2022

-

[21]

V. Mohan. Automated market makers and decentralized exchanges: a defi primer. Financial Innovation , 8(20), 2022

work page 2022

-

[22]

An arbitrage driven price dynamics of automated market makers in the presence of fees

Joseph Najnudel, Shen-Ning Tung, Kazutoshi Yamazaki, and Ju-Yi Yen. An arbitrage driven price dynamics of automated market makers in the presence of fees. Frontiers of Mathematical Finance , 3(4):560--571, 2024

work page 2024

-

[23]

Growth rate of a liquidity provider's wealth in xy=c automated market makers, 2020

Martin Tassy and David White. Growth rate of a liquidity provider's wealth in xy=c automated market makers, 2020

work page 2020

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.