Recognition: unknown

What Happens When Institutional Liquidity Enters Prediction Markets: Identification, Measurement, and a Synthetic Proof of Concept

Pith reviewed 2026-05-10 16:39 UTC · model grok-4.3

The pith

Institutional liquidity in prediction markets tightens spreads but passes gains unevenly, with slowest traders losing most in shocks.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The paper claims that a synthetic microstructure laboratory can validate a measurement pipeline for how institutional liquidity affects prediction markets. Market-maker coverage, liquidity incentives, and automation do not have to work through the same channel; average liquidity gains do not have to translate into equal gains for all traders; and the sharpest welfare losses are most likely to appear in shock states, when slower takers receive the least pass-through of tighter quoted markets. The synthetic results are useful because they stress-test the identification design, not because they settle the live empirical question.

What carries the argument

The synthetic microstructure laboratory that models trader heterogeneity, information arrival processes, and separate liquidity channels to simulate and measure welfare pass-through.

If this is right

- Market-maker coverage, liquidity incentives, and automation operate through independent channels rather than a single mechanism.

- Average liquidity improvements do not guarantee uniform benefits across fast and slow traders.

- The largest welfare losses concentrate in information shock states where slower participants gain the least from improved quotes.

- The identification strategy separates these effects once appropriate measures are applied to live venue data.

Where Pith is reading between the lines

- Real prediction market data could be used to check whether institutional entry improves overall forecast accuracy or mainly advantages high-frequency participants.

- Similar uneven pass-through patterns may exist in other mixed retail-institutional markets, pointing to possible speed-differentiated rules.

- Extensions could vary automation levels to forecast effects under different policy or technology scenarios.

- The approach underscores measuring pass-through rates specifically during volatile periods to evaluate true market quality.

Load-bearing premise

That the synthetic microstructure laboratory sufficiently captures the relevant trading channels, information arrival processes, and trader heterogeneity present in live prediction market venues so that the simulated welfare patterns generalize to real identification problems.

What would settle it

Observing in actual prediction market data that slower traders receive equal or greater pass-through of tighter spreads during high-volatility shock periods would contradict the synthetic welfare patterns.

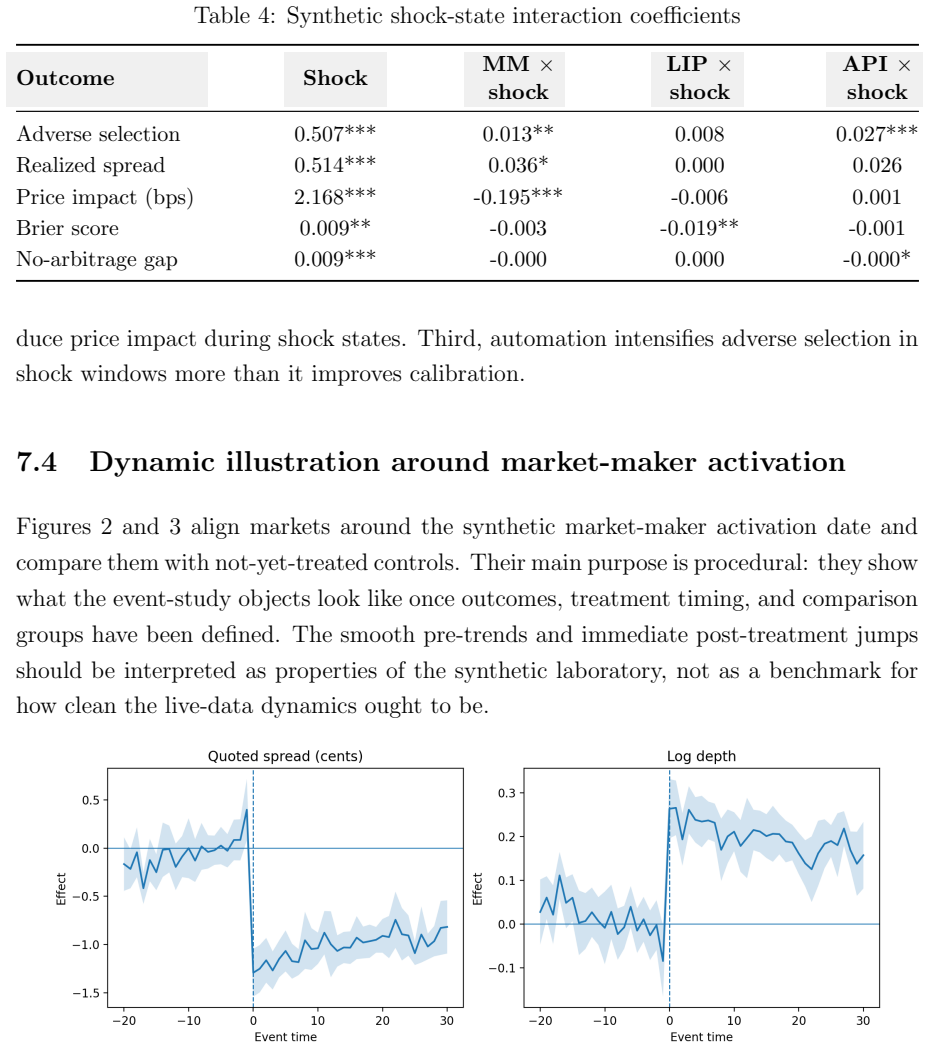

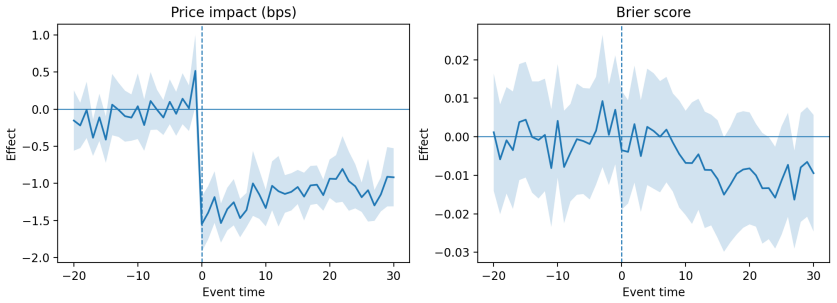

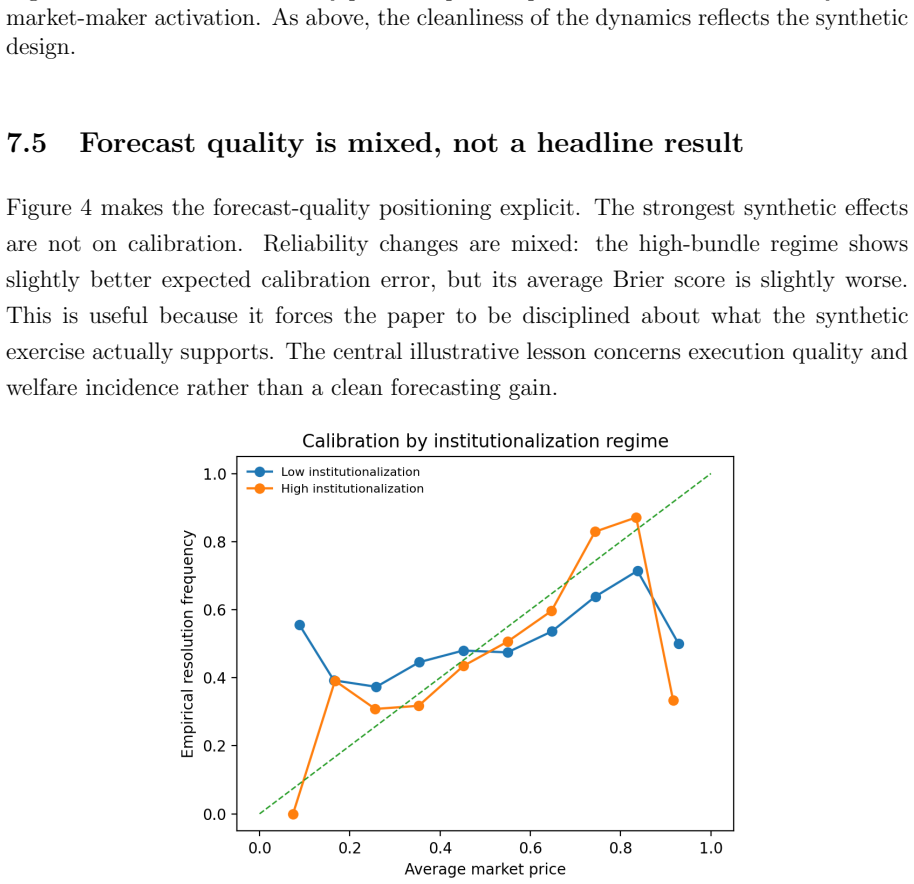

Figures

read the original abstract

Prediction markets are starting to look less like crowd polls and more like electronic markets. The central question is therefore no longer only whether these markets forecast well, but what happens when institutional liquidity enters: do spreads tighten, does price discovery improve, and do those gains actually reach the traders who are slowest to react when information arrives? This paper offers a research design for answering that question. It defines a broad market-quality lens, separates the main channels through which institutional liquidity enters, and maps the identification problems that arise in live venue data. It also uses a synthetic microstructure laboratory as a proof of concept for the measurement pipeline. The main lesson of the synthetic exercise is deliberately narrow. Market-maker coverage, liquidity incentives, and automation do not have to work through the same channel; average liquidity gains do not have to translate into equal gains for all traders; and the sharpest welfare losses are most likely to appear in shock states, when slower takers receive the least pass-through of tighter quoted markets. The synthetic results are useful because they stress-test the design, not because they settle the live empirical question.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript offers a research design for studying the effects of institutional liquidity entry on prediction markets. It defines a broad market-quality lens, separates the primary channels (market-maker coverage, liquidity incentives, and automation), maps identification challenges arising in live venue data, and deploys a synthetic microstructure laboratory as a narrow proof-of-concept stress-test of the measurement pipeline. The synthetic exercise illustrates three 'do not have to' possibilities: the channels need not operate through identical mechanisms, average liquidity improvements need not produce equal gains across trader types, and the sharpest welfare losses are likely to appear in shock states where slower takers receive the least pass-through from tighter quotes.

Significance. If the design and pipeline hold, the work supplies a structured framework for analyzing heterogeneous effects in prediction markets as they attract institutional participants. The deliberate narrow framing of the synthetic results as internal stress-tests rather than generalizable empirical claims is a strength, as is the explicit attention to channel separation and state-dependent welfare consequences. These elements could usefully inform subsequent empirical identification strategies and market-design discussions in the microstructure literature.

minor comments (3)

- The abstract states that the synthetic laboratory serves as a 'proof of concept for the measurement pipeline,' but the manuscript would benefit from an explicit subsection (perhaps in the synthetic exercise section) that lists the exact trader heterogeneity parameters, information arrival processes, and shock definitions used, to allow readers to assess how the pipeline was stress-tested.

- The mapping of identification problems in live data is described at a high level; adding a concise table that cross-tabulates each identification issue with the corresponding measurement variable and proposed mitigation would improve clarity and make the research design more immediately usable.

- Notation for the welfare metric and pass-through rate is introduced in the synthetic section but is not always carried forward with consistent symbols when summarizing the three main lessons; a short notation glossary or consistent use of the same symbols in the concluding paragraphs would reduce ambiguity.

Simulated Author's Rebuttal

We thank the referee for the careful reading and positive evaluation of the manuscript. The summary accurately reflects our research design, the separation of channels, the mapping of identification challenges, and the deliberately narrow scope of the synthetic proof-of-concept. We appreciate the recognition that the framing as internal stress-tests rather than generalizable claims is a strength. No specific major comments were raised in the report, so we have no substantive points requiring rebuttal or revision at this stage. We will address any minor editorial suggestions from the editor in the revised version.

Circularity Check

No significant circularity detected

full rationale

The paper presents a research design for identifying effects of institutional liquidity in prediction markets, followed by a synthetic microstructure laboratory used explicitly as a proof-of-concept stress-test rather than a derivation of real-world outcomes. The central claims are framed as 'do not have to' possibilities illustrated inside the model by construction, with no load-bearing predictions, self-definitional mappings, or self-citation chains that reduce the results to their inputs. The synthetic exercise demonstrates channel separation and unequal pass-through within its own assumptions without claiming external validity or empirical regularities that would require independent verification. No quoted equations or steps exhibit the forbidden patterns of fitted inputs renamed as predictions or ansatzes smuggled via self-citation.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Arrow, Robert Forsythe, Michael Gorham, Robert Hahn, Robin Hanson, John O

Kenneth J. Arrow, Robert Forsythe, Michael Gorham, Robert Hahn, Robin Hanson, John O. Ledyard, Saul Levmore, Robert Litan, Paul Milgrom, Forrest D. Nelson, 18 George R. Neumann, Marco Ottaviani, Thomas C. Schelling, Robert J. Shiller, Ver- non L. Smith, Erik Snowberg, Cass R. Sunstein, Paul C. Tetlock, Philip E. Tetlock, Hal R. Varian, Justin Wolfers, and...

2008

-

[2]

High-frequency trading in a limit order book

Marco Avellaneda and Sasha Stoikov. High-frequency trading in a limit order book. Quantitative Finance, 8(3):217–224, 2008

2008

-

[3]

Berg, Forrest D

Joyce E. Berg, Forrest D. Nelson, and Thomas A. Rietz. Prediction market accuracy in the long run.International Journal of Forecasting, 24(2):285–300, 2008

2008

-

[4]

Market microstructure: A survey of microfoundations, empirical results, and policy implications.Journal of Financial Markets, 8(2):217–264, 2005

Bruno Biais, Lawrence Glosten, and Chester Spatt. Market microstructure: A survey of microfoundations, empirical results, and policy implications.Journal of Financial Markets, 8(2):217–264, 2005

2005

-

[5]

B”urgi, W

C. B”urgi, W. Deng, and K. Whelan. Makers and takers: The economics of the kalshi prediction market. CEPR Discussion Paper 20631, 2026. Working paper

2026

-

[6]

Brantly Callaway and Pedro H. C. Sant’Anna. Difference-in-differences with multiple time periods.Journal of Econometrics, 225(2):200–230, 2021

2021

-

[7]

Colin Cameron, Jonah B

A. Colin Cameron, Jonah B. Gelbach, and Douglas L. Miller. Bootstrap-based improvements for inference with clustered errors.Review of Economics and Statistics, 90(3):414–427, 2008

2008

-

[8]

Colin Cameron and Douglas L

A. Colin Cameron and Douglas L. Miller. A practitioner’s guide to cluster-robust inference.Journal of Human Resources, 50(2):317–372, 2015

2015

-

[9]

Event contracts

Commodity Futures Trading Commission. Event contracts. Federal Register, 89(112), June 10, 2024, 2024.https://www.federalregister.gov/documents/ 2024/06/10/2024-12125/event-contracts

2024

-

[10]

Prediction markets

Commodity Futures Trading Commission. Prediction markets. Federal Register, 91(50), March 16, 2026, 2026.https://www.federalregister.gov/documents/ 2026/03/16/2026-05105/prediction-markets

2026

-

[11]

Toward Black Scholes for Prediction Markets: A Unified Kernel and Market Maker's Handbook

Shaw Dalen. Toward black scholes for prediction markets: A unified kernel and market maker’s handbook.arXiv preprint arXiv:2510.15205, 2025

work page internal anchor Pith review Pith/arXiv arXiv 2025

-

[12]

J. Gebele and F. Matthes. Semantic non-fungibility and violations of the law of one price in prediction markets. arXiv:2601.01706, 2026.https://arxiv.org/abs/ 2601.01706. 19

-

[13]

Glosten and Paul R

Lawrence R. Glosten and Paul R. Milgrom. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders.Journal of Financial Economics, 14(1):71–100, 1985

1985

-

[14]

Difference-in-differences with variation in treatment tim- ing.Journal of Econometrics, 225(2):254–277, 2021

Andrew Goodman-Bacon. Difference-in-differences with variation in treatment tim- ing.Journal of Econometrics, 225(2):254–277, 2021

2021

-

[15]

Oxford University Press, 2003

Larry Harris.Trading and Exchanges: Market Microstructure for Practitioners. Oxford University Press, 2003

2003

-

[16]

Oxford University Press, 2007

Joel Hasbrouck.Empirical Market Microstructure: The Institutions, Economics, and Econometrics of Securities Trading. Oxford University Press, 2007

2007

-

[17]

Jones, and Albert J

Terrence Hendershott, Charles M. Jones, and Albert J. Menkveld. Does algorithmic trading improve liquidity?Journal of Finance, 66(1):1–33, 2011

2011

-

[18]

Ice announces strategic investment in polymarket

Intercontinental Exchange. Ice announces strategic investment in polymarket. Press release, October 7, 2025, 2025.https://ir.theice.com/press/news-details/ 2025/ICE-Announces-Strategic-Investment-in-Polymarket/default.aspx

2025

-

[19]

Intercontinental exchange announces new $600 million investment in polymarket

Intercontinental Exchange. Intercontinental exchange announces new $600 million investment in polymarket. Press release, March 27, 2026, 2026.https://ir.theice.com/press/news-details/2026/ Intercontinental-Exchange-Announces-New-600-Million-Investment-in-Polymarket/ default.aspx

2026

-

[20]

Get market orderbook; public trades, 2026.https://docs.kalshi.com/ api-reference/market/get-market-orderbook;https://docs.kalshi.com/ websockets/public-trades

Kalshi. Get market orderbook; public trades, 2026.https://docs.kalshi.com/ api-reference/market/get-market-orderbook;https://docs.kalshi.com/ websockets/public-trades

2026

-

[21]

Kalshi. Liquidity incentive program. Kalshi Help Center, 2026.https://help. kalshi.com/en/articles/13823851-liquidity-incentive-program

-

[22]

Our market maker program is now live on kalshi

Kalshi. Our market maker program is now live on kalshi. Kalshi Help Center, 2026.https://help.kalshi.com/en/articles/ 13823819-how-to-become-a-market-maker-on-kalshi

2026

-

[23]

Welcome to kalshi’s api documentation; quick start: Market data (no sdk), 2026.https://docs.kalshi.com/welcome;https://docs.kalshi.com/getting_ started/quick_start_market_data

Kalshi. Welcome to kalshi’s api documentation; quick start: Market data (no sdk), 2026.https://docs.kalshi.com/welcome;https://docs.kalshi.com/getting_ started/quick_start_market_data

2026

-

[24]

Albert S. Kyle. Continuous auctions and insider trading.Econometrica, 53(6):1315– 1335, 1985. 20

1985

- [25]

-

[26]

MacKinnon and Matthew D

James G. MacKinnon and Matthew D. Webb. Wild bootstrap inference for wildly different cluster sizes.Journal of Applied Econometrics, 32(2):233–254, 2017

2017

-

[27]

Market microstructure: A survey.Journal of Financial Markets, 3(3):205–258, 2000

Ananth Madhavan. Market microstructure: A survey.Journal of Financial Markets, 3(3):205–258, 2000

2000

-

[28]

Charles F. Manski. Interpreting the predictions of prediction markets.Economics Letters, 91(3):425–429, 2006

2006

-

[29]

Menkveld

Albert J. Menkveld. High frequency trading and the new-market makers.Journal of Financial Markets, 16(4):712–740, 2013

2013

-

[30]

Blackwell, 1995

Maureen O’Hara.Market Microstructure Theory. Blackwell, 1995

1995

-

[31]

Information aggregation in dynamic markets with strategic traders.Econometrica, 80(6):2595–2647, 2012

Michael Ostrovsky. Information aggregation in dynamic markets with strategic traders.Econometrica, 80(6):2595–2647, 2012

2012

-

[32]

N. Palumbo. A microstructure perspective on prediction markets. SSRN Working Pa- per 6325658, 2026.https://papers.ssrn.com/sol3/papers.cfm?abstract_id= 6325658

2026

-

[33]

Get order book; orderbook, 2026.https://docs.polymarket.com/ api-reference/market-data/get-order-book;https://docs.polymarket.com/ trading/orderbook

Polymarket. Get order book; orderbook, 2026.https://docs.polymarket.com/ api-reference/market-data/get-order-book;https://docs.polymarket.com/ trading/orderbook

2026

-

[34]

Overview; prices & orderbook, 2026.https://docs

Polymarket. Overview; prices & orderbook, 2026.https://docs. polymarket.com/trading/overview;https://docs.polymarket.com/concepts/ prices-orderbook

2026

-

[35]

Prediction markets for economic forecasting

Erik Snowberg, Justin Wolfers, and Eric Zitzewitz. Prediction markets for economic forecasting. InHandbook of Economic Forecasting, volume 2A, pages 657–687. Else- vier, 2013

2013

-

[36]

Estimating dynamic treatment effects in event studies with heterogeneous treatment effects.Journal of Econometrics, 225(2):175– 199, 2021

Liyang Sun and Sarah Abraham. Estimating dynamic treatment effects in event studies with heterogeneous treatment effects.Journal of Econometrics, 225(2):175– 199, 2021

2021

-

[37]

Prediction markets.Journal of Economic Per- spectives, 18(2):107–126, 2004

Justin Wolfers and Eric Zitzewitz. Prediction markets.Journal of Economic Per- spectives, 18(2):107–126, 2004

2004

-

[38]

Interpreting prediction market prices as proba- bilities

Justin Wolfers and Eric Zitzewitz. Interpreting prediction market prices as proba- bilities. Working Paper 12200, NBER, 2006. 21

2006

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.