Recognition: unknown

Probabilistic Forecasting for Day-ahead Electricity Prices, Battery Trading Strategies and the Economic Evaluation of Predictive Accuracy

Pith reviewed 2026-05-10 00:57 UTC · model grok-4.3

The pith

Quantile-based battery trading strategies fail to reward honest probabilistic forecasts and ignore price dependencies across hours.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Quantile-based trading strategies (QBTS) do not incentivize honest probabilistic forecasting and ignore the intertemporal dependence structure of electricity prices. Framing battery optimization as a stochastic program based on fully probabilistic forecasts provides a better link between statistical forecast quality and decision quality in both risk-neutral and risk-averse settings.

What carries the argument

A stochastic program for battery arbitrage that optimizes charge and discharge schedules over the full predictive distribution of day-ahead prices while respecting battery state constraints across consecutive hours.

If this is right

- Rankings of forecasting models by realized trading profits can differ from rankings by statistical scoring rules.

- Improvements in the full predictive distribution translate more directly into higher expected profits when decisions are made via stochastic optimization.

- Risk-averse battery operators need uncertainty models that properly capture tail risks to evaluate forecast value correctly.

- Simplified application studies using quantile rules can produce misleading assessments of which forecast models are economically best.

Where Pith is reading between the lines

- Forecast evaluation practice should incorporate the downstream optimization model rather than relying solely on statistical metrics or simple trading heuristics.

- The stochastic programming approach could be tested on other flexible assets such as demand response or pumped storage to check if the same advantages hold.

- Market operators might consider requiring full distributional forecasts from participants when assets involve multi-period decisions.

Load-bearing premise

The stochastic program and chosen risk models accurately reflect how real batteries trade without major unmodeled effects from transaction costs or market impact.

What would settle it

Empirical results on German market data in which the stochastic program yields lower profits than a quantile-based strategy despite higher forecast quality would falsify the claim of a superior link between forecast accuracy and decision quality.

Figures

read the original abstract

Electricity price forecasting supports decision-making in energy markets and asset operation. Probabilistic forecasts are increasingly adopted to explicitly quantify uncertainty, typically issued as quantile predictions or ensembles of the full predictive distribution. However, how improvements in statistical forecast quality translate into economic value remains unclear. Battery storage arbitrage in day-ahead markets is a popular application-based benchmark for this purpose. We analyze quantile-based trading strategies (QBTS) and identify two critical flaws: they do not incentivize honest probabilistic forecasting and they ignore the intertemporal dependence structure of electricity prices. We therefore frame battery optimization as a stochastic program based on fully probabilistic forecasts and examine decision quality measurement for risk-neutral and risk-averse settings under different uncertainty models. Our discussion touches both sides of the coin: How reliable is the economic evaluation of forecasting models though (simplified) application studies - and how do improvements in statistical forecast quality for stochastic programs relate to the decision-quality and economic performance? We provide theoretical justification and empirical evidence from a case study on the German electricity market. Our results highlight the pitfalls of ranking forecasting models through battery trading strategies. We conclude with implications for evaluation practice and directions for future research in application-based forecast assessment.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that quantile-based trading strategies (QBTS) for battery arbitrage in day-ahead electricity markets do not incentivize honest probabilistic forecasting and ignore the intertemporal dependence structure of electricity prices. It proposes framing battery optimization as a stochastic program based on fully probabilistic forecasts for better alignment between statistical forecast quality and decision quality, providing theoretical justification and empirical evidence from a German market case study while highlighting pitfalls of ranking forecasting models via simplified battery trading strategies.

Significance. If the results hold, this work is significant for probabilistic forecasting evaluation in energy markets. It challenges common application-based benchmarks like QBTS and advocates stochastic programming that incorporates full distributions and dependencies, potentially improving how economic value of forecasts is measured in risk-neutral and risk-averse settings. The dual focus on theoretical flaws and empirical pitfalls offers a useful framework for future application-based forecast assessment.

major comments (3)

- [§3] §3: The central claim that QBTS 'do not incentivize honest probabilistic forecasting' is illustrated via examples but lacks a general formal argument or counterexample demonstrating misalignment for arbitrary distributions; this is load-bearing for rejecting QBTS in favor of stochastic programs.

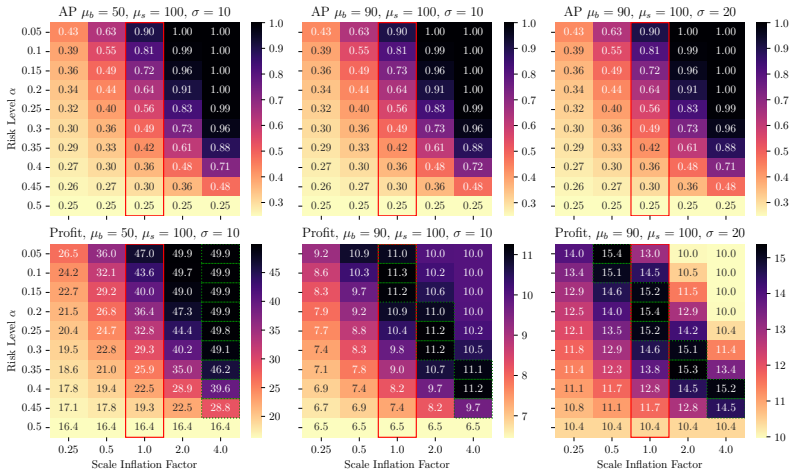

- [§5] §5 (German case study): The reported profit differentials and model rankings assume frictionless trading (no transaction costs, no market impact, perfect liquidity). These omitted frictions are load-bearing for the superiority claim, as even modest costs could reverse the economic advantage of stochastic programs over QBTS.

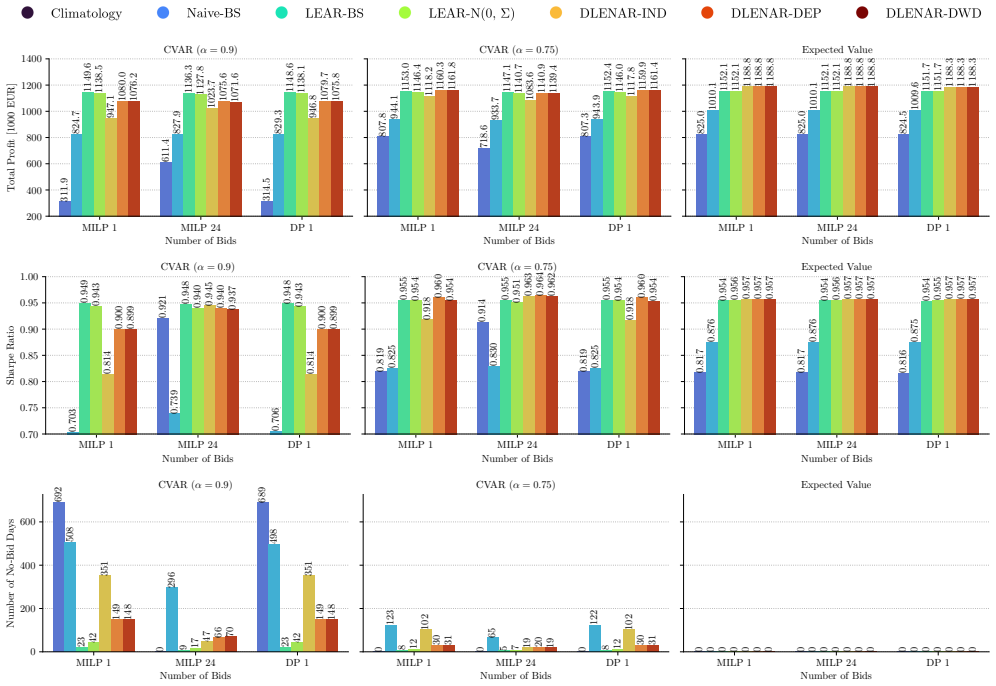

- [§4.2] §4.2, risk-averse formulation: The risk aversion parameter is free and its specific value affects the objective; the paper should show that stochastic program advantages persist across a range of values rather than selected cases, to support the general recommendation.

minor comments (3)

- [Abstract] Abstract: 'how reliable is the economic evaluation of forecasting models though (simplified) application studies' contains a typo ('though' should be 'through').

- [Figures] Figure captions (e.g., profit comparison figures): Expand to explicitly list the uncertainty models and risk settings used in each stochastic program variant for clarity.

- [References] References: Add citations to recent work on stochastic optimization for battery arbitrage to better situate the contribution relative to existing literature.

Simulated Author's Rebuttal

We thank the referee for the constructive and insightful comments, which help clarify important aspects of our analysis. We address each major comment below, outlining our responses and planned revisions to strengthen the manuscript.

read point-by-point responses

-

Referee: The central claim that QBTS 'do not incentivize honest probabilistic forecasting' is illustrated via examples but lacks a general formal argument or counterexample demonstrating misalignment for arbitrary distributions; this is load-bearing for rejecting QBTS in favor of stochastic programs.

Authors: We acknowledge that the argument in §3 relies primarily on illustrative examples tailored to electricity price characteristics (asymmetry, multimodality) rather than a fully general formal proof for arbitrary distributions. These examples are intended to highlight the misalignment between quantile optimization and honest probabilistic forecasting. In the revision, we will expand §3 with a more rigorous theoretical section that specifies the conditions under which QBTS fail to incentivize honest forecasts and provide a counterexample framework applicable to a broad class of distributions relevant to energy markets. While a universal proof for literally all distributions may exceed the paper's scope and practical relevance, this will better support the central claim. revision: partial

-

Referee: §5 (German case study): The reported profit differentials and model rankings assume frictionless trading (no transaction costs, no market impact, perfect liquidity). These omitted frictions are load-bearing for the superiority claim, as even modest costs could reverse the economic advantage of stochastic programs over QBTS.

Authors: The referee correctly identifies that our empirical results in §5 assume frictionless trading, which is a common simplification to isolate forecast and optimization effects but limits generalizability. We agree that modest frictions could potentially alter rankings and differentials. In the revised manuscript, we will add a dedicated sensitivity analysis incorporating small transaction costs (e.g., 0.5–2 EUR/MWh) and discuss market impact qualitatively, demonstrating the robustness of the stochastic programming advantages where possible while acknowledging scenarios where they may diminish. revision: yes

-

Referee: §4.2, risk-averse formulation: The risk aversion parameter is free and its specific value affects the objective; the paper should show that stochastic program advantages persist across a range of values rather than selected cases, to support the general recommendation.

Authors: We thank the referee for highlighting the need for robustness in the risk-averse setting. Section 4.2 currently uses a representative risk aversion parameter to illustrate the formulation. In the revision, we will extend the empirical analysis to report results across a range of risk aversion values (e.g., λ = 0, 0.5, 1.0, 2.0) using the German market data, confirming that the performance advantages of stochastic programs over QBTS persist consistently and thereby supporting the broader recommendation. revision: yes

Circularity Check

No significant circularity; derivation is self-contained

full rationale

The paper critiques quantile-based trading strategies using external decision-theoretic arguments (incentives for honest forecasting and intertemporal dependence) and proposes stochastic programming formulations for battery optimization, supported by theoretical justification plus an empirical German market case study. No load-bearing steps reduce by construction to self-definitions, fitted parameters renamed as predictions, or self-citation chains; the central claims rely on independent concepts from stochastic optimization and forecast evaluation rather than internal equivalence to the paper's own inputs.

Axiom & Free-Parameter Ledger

free parameters (1)

- Risk aversion parameter

axioms (2)

- domain assumption Battery decisions can be accurately modeled as a stochastic program with known constraints and objective.

- domain assumption Intertemporal dependence in prices is captured by the full predictive distribution.

Reference graph

Works this paper leans on

-

[1]

Journal of Applied Meteorology (1962-1982) , volume=

A scoring system for probability forecasts of ranked categories , author=. Journal of Applied Meteorology (1962-1982) , volume=. 1969 , publisher=

1962

-

[2]

Forecasting , volume=

Event-based evaluation of electricity price ensemble forecasts , author=. Forecasting , volume=. 2021 , publisher=

2021

-

[3]

Journal of Quantitative Analysis in Sports , volume=

Solving the problem of inadequate scoring rules for assessing probabilistic football forecast models , author=. Journal of Quantitative Analysis in Sports , volume=

-

[4]

Journal of Quantitative Analysis in Sports , volume=

Evaluating probabilistic forecasts of football matches: the case against the ranked probability score , author=. Journal of Quantitative Analysis in Sports , volume=. 2021 , publisher=

2021

-

[5]

Weather and forecasting , volume=

Beyond strictly proper scoring rules: The importance of being local , author=. Weather and forecasting , volume=

-

[6]

ACM computing surveys (CSUR) , volume=

K-nearest neighbour classifiers-a tutorial , author=. ACM computing surveys (CSUR) , volume=. 2021 , publisher=

2021

-

[7]

Asymmetric penalties underlie proper loss functions in probabilistic forecasting , author=. arXiv preprint arXiv:2505.00937 , year=

-

[8]

2013 , publisher=

Discrimination ability of the energy score , author=. 2013 , publisher=

2013

-

[9]

Renewable and Sustainable Energy Reviews , volume=

Recent advances in electricity price forecasting: A review of probabilistic forecasting , author=. Renewable and Sustainable Energy Reviews , volume=. 2018 , publisher=

2018

-

[10]

International Conference on Machine Learning , pages=

The Kendall and Mallows kernels for permutations , author=. International Conference on Machine Learning , pages=. 2015 , organization=

2015

-

[11]

Biometrika , volume=

A new measure of rank correlation , author=. Biometrika , volume=. 1938 , publisher=

1938

-

[12]

Computational and mathematical methods in medicine , volume=

Correlation kernels for support vector machines classification with applications in cancer data , author=. Computational and mathematical methods in medicine , volume=. 2012 , publisher=

2012

-

[13]

Computational Statistics & Data Analysis , volume=

Conditional copulas, association measures and their applications , author=. Computational Statistics & Data Analysis , volume=. 2011 , publisher=

2011

-

[14]

arXiv preprint arXiv:1910.07325 , year=

Multivariate forecasting evaluation: On sensitive and strictly proper scoring rules , author=. arXiv preprint arXiv:1910.07325 , year=

-

[15]

Energy Economics , volume=

Regularized quantile regression averaging for probabilistic electricity price forecasting , author=. Energy Economics , volume=. 2021 , publisher=

2021

-

[16]

Operations research , volume=

The value of coordination in multimarket bidding of grid energy storage , author=. Operations research , volume=. 2023 , publisher=

2023

-

[17]

Energy Economics , volume=

Postprocessing of point predictions for probabilistic forecasting of day-ahead electricity prices: The benefits of using isotonic distributional regression , author=. Energy Economics , volume=. 2024 , publisher=

2024

-

[18]

The Energy Journal , volume=

The profitability of energy storage in European electricity markets , author=. The Energy Journal , volume=. 2021 , publisher=

2021

-

[19]

European Journal of Operational Research , volume=

Stochastic optimization of trading strategies in sequential electricity markets , author=. European Journal of Operational Research , volume=. 2023 , publisher=

2023

-

[20]

Journal of Energy Storage , volume=

Maximising the value of electricity storage , author=. Journal of Energy Storage , volume=. 2016 , publisher=

2016

-

[21]

European Journal of Operational Research , volume=

Stochastic search for a parametric cost function approximation: Energy storage with rolling forecasts , author=. European Journal of Operational Research , volume=. 2024 , publisher=

2024

-

[22]

European Journal of Operational Research , year=

Value-oriented forecast reconciliation for renewables in electricity markets , author=. European Journal of Operational Research , year=

-

[23]

Electric Power Systems Research , volume=

Probabilistic forecasting with a hybrid Factor-QRA approach: Application to electricity trading , author=. Electric Power Systems Research , volume=. 2024 , publisher=

2024

-

[24]

Journal of Forecasting , volume=

Economic and statistical measures of forecast accuracy , author=. Journal of Forecasting , volume=. 2000 , publisher=

2000

-

[25]

The Annals of Statistics , volume=

Higher order elicitability and Osband’s principle , author=. The Annals of Statistics , volume=. 2016 , publisher=

2016

-

[26]

Electronic Journal of Statistics , volume=

Order-sensitivity and equivariance of scoring functions , author=. Electronic Journal of Statistics , volume=

-

[27]

Annals of Operations Research , volume=

Evaluating the discrimination ability of proper multi-variate scoring rules , author=. Annals of Operations Research , volume=. 2024 , publisher=

2024

-

[28]

European Journal of Operational Research , volume=

An empirical analysis of scenario generation methods for stochastic optimization , author=. European Journal of Operational Research , volume=. 2016 , publisher=

2016

-

[29]

International Conference on Machine Learning , pages=

Regions of reliability in the evaluation of multivariate probabilistic forecasts , author=. International Conference on Machine Learning , pages=. 2023 , organization=

2023

-

[30]

arXiv preprint arXiv:1507.00244 , year=

Expected shortfall is jointly elicitable with value at risk-implications for backtesting , author=. arXiv preprint arXiv:1507.00244 , year=

-

[31]

Journal of Financial Econometrics , volume=

Robust forecast evaluation of expected shortfall , author=. Journal of Financial Econometrics , volume=. 2020 , publisher=

2020

-

[32]

Energy Economics , volume=

Loss functions in regression models: Impact on profits and risk in day-ahead electricity trading , author=. Energy Economics , volume=. 2025 , publisher=

2025

-

[33]

Energy and AI , volume=

Optimising quantile-based trading strategies in electricity arbitrage , author=. Energy and AI , volume=. 2025 , publisher=

2025

-

[34]

Energy and AI , volume=

Conformal prediction for electricity price forecasting in the day-ahead and real-time balancing market , author=. Energy and AI , volume=. 2025 , publisher=

2025

-

[35]

International Workshop on Advanced Analytics and Learning on Temporal Data , pages=

Conformal Prediction Techniques for Electricity Price Forecasting , author=. International Workshop on Advanced Analytics and Learning on Temporal Data , pages=. 2024 , organization=

2024

-

[36]

arXiv preprint arXiv:2308.15443 , year=

Combining predictive distributions of electricity prices: Does minimizing the CRPS lead to optimal decisions in day-ahead bidding? , author=. arXiv preprint arXiv:2308.15443 , year=

-

[37]

Journal of Risk and Financial Management , volume=

Optimizing Energy Storage Profits: A New Metric for Evaluating Price Forecasting Models , author=. Journal of Risk and Financial Management , volume=. 2024 , publisher=

2024

-

[38]

2025 21st International Conference on the European Energy Market (EEM) , pages=

Forecasting Electricity Prices With Decision-Focused Learning for Storage Optimization , author=. 2025 21st International Conference on the European Energy Market (EEM) , pages=. 2025 , organization=

2025

-

[39]

IEEE Transactions on Smart Grid , volume=

Electricity price prediction for energy storage system arbitrage: A decision-focused approach , author=. IEEE Transactions on Smart Grid , volume=. 2022 , publisher=

2022

-

[40]

2025 , journal=

Smoothing quantile regression averaging: A new approach to probabilistic forecasting of electricity prices , author=. 2025 , journal=

2025

-

[41]

arXiv preprint arXiv:2509.19417 , year=

Analyzing Uncertainty Quantification in Statistical and Deep Learning Models for Probabilistic Electricity Price Forecasting , author=. arXiv preprint arXiv:2509.19417 , year=

-

[42]

arXiv preprint arXiv:2411.17743 , year=

Ranking probabilistic forecasting models with different loss functions , author=. arXiv preprint arXiv:2411.17743 , year=

-

[43]

Journal of Commodity Markets , volume=

Extrapolating the long-term seasonal component of electricity prices for forecasting in the day-ahead market , author=. Journal of Commodity Markets , volume=. 2025 , publisher=

2025

-

[44]

Neurocomputing , volume=

Stock portfolio selection using learning-to-rank algorithms with news sentiment , author=. Neurocomputing , volume=. 2017 , publisher=

2017

-

[45]

Quantitative Finance , volume=

Constructing long-short stock portfolio with a new listwise learn-to-rank algorithm , author=. Quantitative Finance , volume=. 2022 , publisher=

2022

-

[46]

Energy Economics , volume=

Distributional neural networks for electricity price forecasting , author=. Energy Economics , volume=. 2023 , publisher=

2023

-

[47]

Probabilistic multivariate electricity price forecasting using implicit generative ensemble post-processing , year =

Janke, Tim and Steinke, Florian , booktitle =. Probabilistic multivariate electricity price forecasting using implicit generative ensemble post-processing , year =

-

[48]

Energy Economics , title =

Agakishiev, Ilyas and H. Energy Economics , title =. 2025 , pages =

2025

-

[49]

arXiv preprint arXiv:2407.07795 , year=

Multiple split approach--multidimensional probabilistic forecasting of electricity markets , author=. arXiv preprint arXiv:2407.07795 , year=

-

[50]

Online Multivariate Regularized Distributional Regression for High-dimensional Probabilistic Electricity Price Forecasting , author=. arXiv preprint arXiv:2504.02518 , year=

work page internal anchor Pith review Pith/arXiv arXiv

-

[51]

Annual Review of Statistics and Its Application , volume=

Risk measures: robustness, elicitability, and backtesting , author=. Annual Review of Statistics and Its Application , volume=. 2022 , publisher=

2022

-

[52]

Journal of risk , volume=

Optimization of conditional value-at-risk , author=. Journal of risk , volume=

-

[53]

Stochastic optimization: algorithms and applications , pages=

Conditional value-at-risk: optimization approach , author=. Stochastic optimization: algorithms and applications , pages=. 2001 , publisher=

2001

-

[54]

arXiv:2511.13616 URL:https://arxiv.org/abs/ 2511.13616

Statistical and economic evaluation of forecasts in electricity markets: beyond RMSE and MAE , author=. arXiv preprint arXiv:2511.13616 , year=

-

[55]

Journal of political Economy , volume=

The utility of wealth , author=. Journal of political Economy , volume=. 1952 , publisher=

1952

-

[56]

The Journal of Finance , volume=

Portfolio Selection , author=. The Journal of Finance , volume=

-

[57]

Journal of Business & Economic Statistics , volume=

Comparing predictive accuracy, twenty years later: A personal perspective on the use and abuse of Diebold--Mariano tests , author=. Journal of Business & Economic Statistics , volume=. 2015 , publisher=

2015

-

[58]

multivariate modeling frameworks , author=

Day-ahead electricity price forecasting with high-dimensional structures: Univariate vs. multivariate modeling frameworks , author=. Energy Economics , volume=. 2018 , publisher=

2018

-

[59]

Journal of Business & economic statistics , volume=

Comparing predictive accuracy , author=. Journal of Business & economic statistics , volume=. 2002 , publisher=

2002

-

[60]

arXiv preprint arXiv:2508.18251 , year=

Aligning the Evaluation of Probabilistic Predictions with Downstream Value , author=. arXiv preprint arXiv:2508.18251 , year=

-

[61]

International conference on machine learning , pages=

Addressing the loss-metric mismatch with adaptive loss alignment , author=. International conference on machine learning , pages=. 2019 , organization=

2019

-

[62]

International Conference on Learning Representations , year=

Automatic loss function search for predict-then-optimize problems with strong ranking property , author=. International Conference on Learning Representations , year=

-

[63]

predict, then optimize

Smart “predict, then optimize” , author=. Management Science , volume=. 2022 , publisher=

2022

-

[64]

Advances in neural information processing systems , volume=

Task-based end-to-end model learning in stochastic optimization , author=. Advances in neural information processing systems , volume=

-

[65]

Journal of the American statistical Association , volume=

Strictly proper scoring rules, prediction, and estimation , author=. Journal of the American statistical Association , volume=. 2007 , publisher=

2007

-

[66]

Modeling public holidays in load forecasting: a German case study , year =

Ziel, Florian , journal =. Modeling public holidays in load forecasting: a German case study , year =

-

[67]

Journal of Statistical Software , volume=

Weighted scoringrules: Emphasizing particular outcomes when evaluating probabilistic forecasts , author=. Journal of Statistical Software , volume=

-

[68]

SIAM/ASA Journal on Uncertainty Quantification , volume=

Evaluating forecasts for high-impact events using transformed kernel scores , author=. SIAM/ASA Journal on Uncertainty Quantification , volume=. 2023 , publisher=

2023

-

[69]

Weather and Forecasting , volume=

Weighted verification tools to evaluate univariate and multivariate probabilistic forecasts for high-impact weather events , author=. Weather and Forecasting , volume=

-

[70]

Journal of Business & Economic Statistics , volume=

Generic conditions for forecast dominance , author=. Journal of Business & Economic Statistics , volume=. 2021 , publisher=

2021

-

[71]

arXiv preprint arXiv:2410.04165 , year=

How to Compare Copula Forecasts? , author=. arXiv preprint arXiv:2410.04165 , year=

-

[72]

Mathematical Geosciences , volume=

Estimation of the continuous ranked probability score with limited information and applications to ensemble weather forecasts , author=. Mathematical Geosciences , volume=. 2018 , publisher=

2018

-

[73]

Monthly Weather Review , volume=

Variogram-based proper scoring rules for probabilistic forecasts of multivariate quantities , author=. Monthly Weather Review , volume=

-

[74]

Annals of Statistics , pages=

Coherent dispersion criteria for optimal experimental design , author=. Annals of Statistics , pages=. 1999 , publisher=

1999

-

[75]

Mathematical Programming Computation , volume=

Pyomo: modeling and solving mathematical programs in Python , author=. Mathematical Programming Computation , volume=. 2011 , publisher=

2011

-

[76]

Mathematical Programming Computation , volume=

Parallelizing the dual revised simplex method , author=. Mathematical Programming Computation , volume=. 2018 , publisher=

2018

-

[77]

The Journal of business , volume=

Mutual fund performance , author=. The Journal of business , volume=. 1966 , publisher=

1966

-

[78]

Journal of portfolio Management , volume=

Downside risk , author=. Journal of portfolio Management , volume=. 1991 , publisher=

1991

-

[79]

arXiv preprint arXiv:2501.02963 , year=

A data-driven merit order: Learning a fundamental electricity price model , author=. arXiv preprint arXiv:2501.02963 , year=

-

[80]

Hierarchical forecasting for aggregated curves with an application to day-ahead electricity price auctions , year =

Ghelasi, Paul and Ziel, Florian , journal =. Hierarchical forecasting for aggregated curves with an application to day-ahead electricity price auctions , year =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.