Recognition: unknown

Early Detection of Latent Microstructure Regimes in Limit Order Books

Pith reviewed 2026-05-10 00:07 UTC · model grok-4.3

The pith

A latent build-up regime in limit order books can be identified before stress emerges under mild assumptions.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

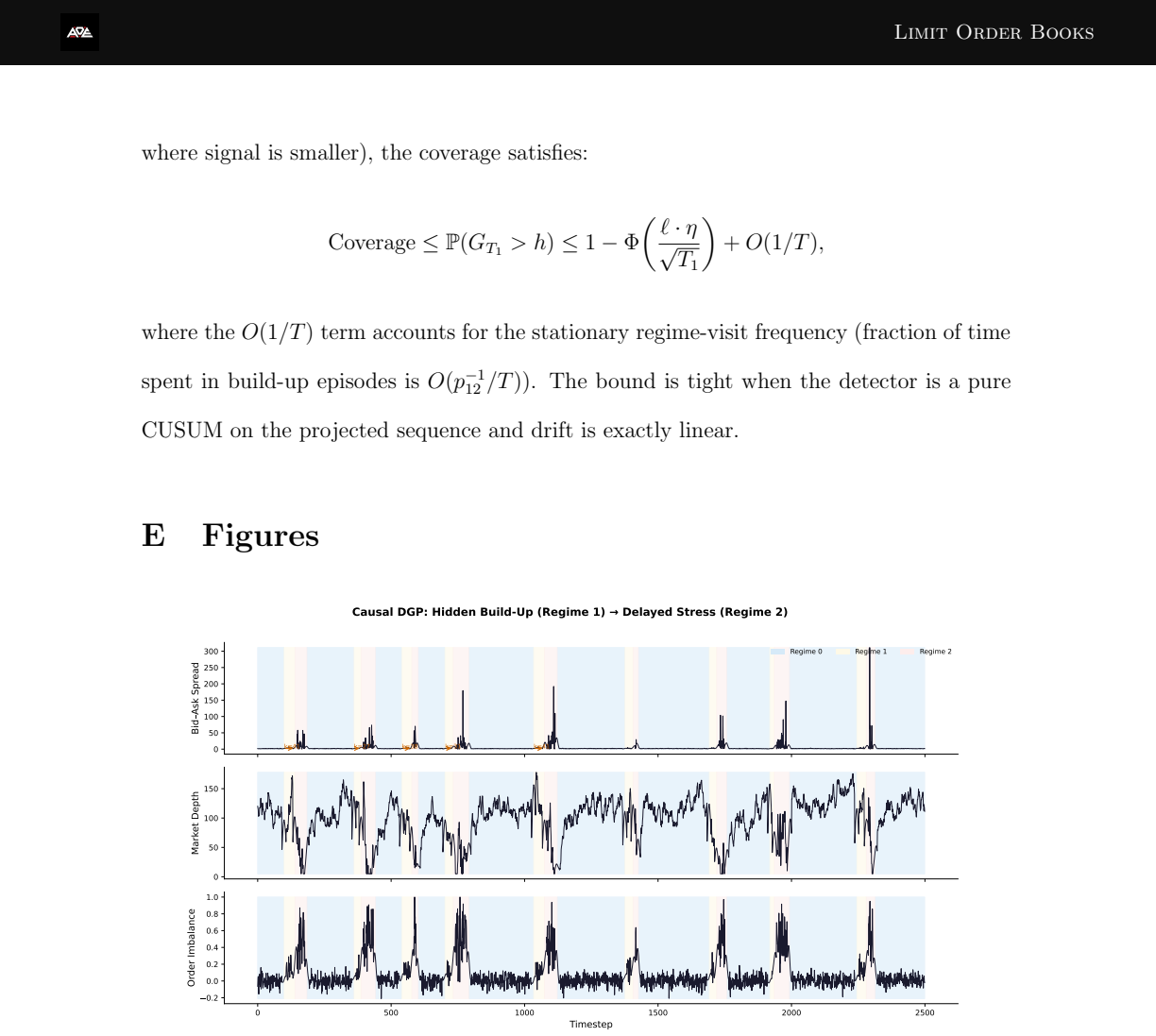

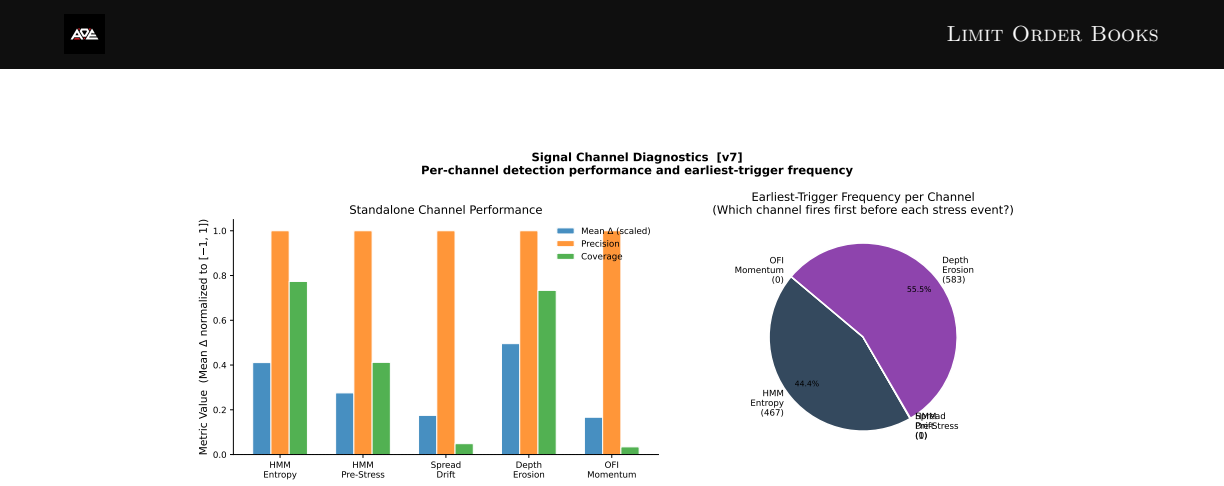

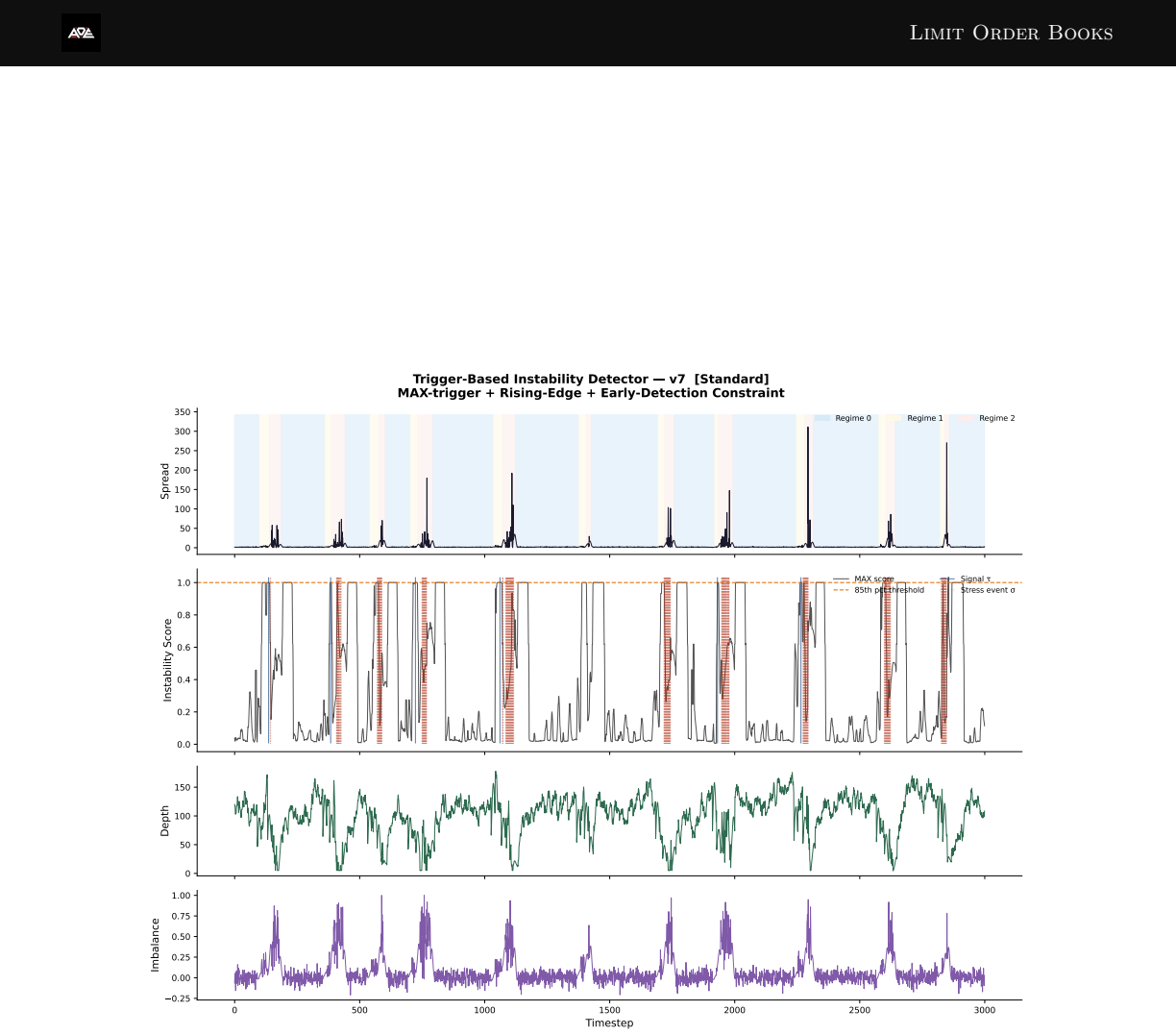

We formalise this limitation via a three-regime causal data-generating process (stable → latent build-up → stress) in which a latent deterioration phase creates a prediction window prior to observable stress. Under mild assumptions on temporal drift and regime persistence, we establish identifiability of the latent build-up regime and derive guarantees for strictly positive expected lead-time and non-trivial probability of early detection. We propose a trigger-based detector combining MAX aggregation of complementary signal channels, a rising-edge condition, and adaptive thresholding.

What carries the argument

Three-regime causal data-generating process containing a latent build-up phase, together with a trigger-based detector that uses MAX aggregation of signal channels, rising-edge detection, and adaptive thresholding.

If this is right

- The detector delivers mean lead time of +18.6 timesteps with perfect precision and moderate coverage in 200 simulations.

- It outperforms classical change-point and microstructure baselines in both simulated and real order-book data.

- Application to one week of BTC/USDT data yields consistent positive lead times while baselines stay reactive.

- Detection performance degrades in low signal-to-noise conditions and short build-up regimes, as predicted by the theory.

Where Pith is reading between the lines

- The same three-regime structure could be tested on equity or futures order books to check whether similar latent phases appear across asset classes.

- The identifiability result suggests that other high-frequency financial series with abrupt regime shifts might admit analogous early-detection windows.

- Incorporating the detector into real-time risk systems would allow position adjustments during the build-up window rather than after stress is already priced in.

Load-bearing premise

Mild assumptions on temporal drift and regime persistence are required to prove identifiability of the latent build-up regime and the existence of positive expected lead time.

What would settle it

A simulation drawn from the three-regime process under the stated assumptions in which the detector produces zero or negative expected lead time would falsify the guarantees.

Figures

read the original abstract

Limit order books can transition rapidly from stable to stressed conditions, yet standard early-warning signals such as order flow imbalance and short-term volatility are inherently reactive. We formalise this limitation via a three-regime causal data-generating process (stable $\to$ latent build-up $\to$ stress) in which a latent deterioration phase creates a prediction window prior to observable stress. Under mild assumptions on temporal drift and regime persistence, we establish identifiability of the latent build-up regime and derive guarantees for strictly positive expected lead-time and non-trivial probability of early detection. We propose a trigger-based detector combining MAX aggregation of complementary signal channels, a rising-edge condition, and adaptive thresholding. Across 200 simulations, the method achieves mean lead-time $+18.6 \pm 3.2$ timesteps with perfect precision and moderate coverage, outperforming classical change-point and microstructure baselines. A preliminary application to one week of BTC/USDT order book data shows consistent positive lead-times while baselines remain reactive. Results degrade in low signal-to-noise and short build-up regimes, consistent with theory.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript formalizes early detection of latent microstructure regimes in limit order books using a three-regime causal data-generating process (stable → latent build-up → stress). Under explicitly stated mild assumptions on temporal drift and regime persistence, it proves identifiability of the latent build-up regime and derives guarantees for strictly positive expected lead-time together with non-trivial early-detection probability. A detector is constructed via MAX aggregation of complementary signals, a rising-edge condition, and adaptive thresholding. Simulations (200 runs) report mean lead-time of +18.6 ± 3.2 timesteps with perfect precision and moderate coverage, outperforming change-point and microstructure baselines; a preliminary one-week BTC/USDT backtest shows consistent positive lead-times while baselines remain reactive, with noted degradation in low-SNR and short-build-up regimes.

Significance. If the stated assumptions hold in practice, the work supplies a principled, non-reactive early-warning framework grounded in identifiability results rather than post-hoc fitting. The explicit derivation of positive expected lead-time and the simulation results with reported error bars constitute clear strengths; the detector construction follows directly from the model without circularity. This could meaningfully advance microstructure-based risk monitoring, provided the mild-assumption regime is shown to be representative of real-market conditions beyond the single-week preliminary test.

major comments (1)

- [Real-data experiment section] Real-data evaluation (one week of BTC/USDT): while positive lead-times are reported, the degradation in low-SNR and short-build-up regimes is described only qualitatively; quantitative lead-time, coverage, and precision figures with confidence intervals for these regimes are needed to assess whether the empirical results remain consistent with the theoretical guarantees.

minor comments (2)

- [Abstract] Abstract: the reported simulation lead-time includes ±3.2 error bars, but the real-data claim of 'consistent positive lead-times' lacks corresponding quantitative detail or error bars; adding a brief numerical summary would improve clarity.

- [Model section] Notation: the three-regime DGP is introduced with symbols for stable, build-up, and stress states; ensure all subsequent equations reuse the same symbols without redefinition to avoid reader confusion.

Simulated Author's Rebuttal

We thank the referee for the positive assessment and the recommendation for minor revision. We address the single major comment below and will incorporate the requested quantitative analysis into the revised manuscript.

read point-by-point responses

-

Referee: [Real-data experiment section] Real-data evaluation (one week of BTC/USDT): while positive lead-times are reported, the degradation in low-SNR and short-build-up regimes is described only qualitatively; quantitative lead-time, coverage, and precision figures with confidence intervals for these regimes are needed to assess whether the empirical results remain consistent with the theoretical guarantees.

Authors: We agree that a quantitative stratification of the real-data results is needed to allow direct comparison with the theoretical guarantees and simulation outcomes. In the revised manuscript we will add a table (or supplementary figure) reporting mean lead-time, coverage, and precision together with 95% confidence intervals, computed separately for the low-SNR and short-build-up subsets of the one-week BTC/USDT dataset. Events will be partitioned using the same SNR and build-up-duration thresholds defined in the simulation section, ensuring the empirical figures can be assessed against the identifiability and lead-time results. revision: yes

Circularity Check

No significant circularity identified

full rationale

The paper derives identifiability of the latent build-up regime and guarantees of strictly positive expected lead-time directly from its explicitly stated mild assumptions on temporal drift and regime persistence in the three-regime causal DGP. The proposed detector (MAX aggregation of signal channels, rising-edge condition, adaptive thresholding) is constructed as a direct consequence of the model rather than fitted to target performance metrics. Simulation outcomes are reported as consistent with the derived theory, and the real-data application serves as preliminary validation without circular reduction. No self-citation chain, self-definitional step, or fitted-input-renamed-as-prediction is present in the load-bearing argument, rendering the derivation self-contained.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption mild assumptions on temporal drift and regime persistence

invented entities (1)

-

latent build-up regime

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Adams, R. P. and D. J. C. MacKay (2007). Bayesian online changepoint detection. arXiv preprint\/ , arXiv:0710.3742

work page Pith review arXiv 2007

-

[2]

Bouchaud, J.-P., J. D. Farmer, and F. Lillo (2009). How markets slowly digest changes in supply and demand. In Handbook of Financial Markets: Dynamics and Evolution , 57--160. Elsevier

2009

-

[3]

Jaimungal, and J

Cartea, \'A., S. Jaimungal, and J. Penalva (2015). Algorithmic and High-Frequency Trading . Cambridge University Press

2015

-

[4]

Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance\/ 1\/ (2), 223--236

2001

-

[5]

Kukanov, and S

Cont, R., A. Kukanov, and S. Stoikov (2014). The price impact of order book events. Journal of Financial Econometrics\/ 12\/ (1), 47--88

2014

-

[6]

L\'opez de Prado, and M

Easley, D., M. L\'opez de Prado, and M. O'Hara (2012). Flow toxicity and liquidity in a high-frequency world. Review of Financial Studies\/ 25\/ (5), 1457--1493

2012

-

[7]

Glosten, L. R. and P. R. Milgrom (1985). Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of Financial Economics\/ 14\/ (1), 71--100

1985

-

[8]

Gould, M. D., M. A. Porter, S. Williams, M. McDonald, D. J. Fenn, and S. D. Howison (2013). Limit order books. Quantitative Finance\/ 13\/ (11), 1709--1742

2013

-

[9]

Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica\/ 57\/ (2), 357--384

1989

-

[10]

Hasbrouck, J. (1991). Measuring the information content of stock trades. Journal of Finance\/ 46\/ (1), 179--207

1991

-

[11]

Huang, R. and T. Polak (2011). LOBSTER: Limit order book system - the efficient reconstructor. SSRN Working Paper\/ , https://ssrn.com/abstract=1977207

2011

-

[12]

Kyle, A. S. (1985). Continuous auctions and insider trading. Econometrica\/ 53\/ (6), 1315--1335

1985

-

[13]

Moustakides, G. V. (1986). Optimal stopping times for detecting changes in distributions. Annals of Statistics\/ 14\/ (4), 1379--1387

1986

-

[14]

Page, E. S. (1954). Continuous inspection schemes. Biometrika\/ 41\/ (1/2), 100--115

1954

-

[15]

Rabiner, L. R. (1989). A tutorial on hidden Markov models and selected applications in speech recognition. Proceedings of the IEEE\/ 77\/ (2), 257--286

1989

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.