Recognition: unknown

An Explicit Solution to Black-Scholes Implied Volatility

Pith reviewed 2026-05-07 16:54 UTC · model grok-4.3

The pith

The Black-Scholes call price equals the survival probability of an inverse Gaussian random variable, so implied volatility equals the corresponding quantile function applied to observable inputs.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The Black-Scholes call price equals the survival probability of an inverse Gaussian distribution. Inverting this representation produces an analytically explicit formula for implied volatility expressed via the inverse Gaussian quantile function, with volatility isolated on the left-hand side and only observable option inputs on the right-hand side.

What carries the argument

The identity that equates the Black-Scholes call price to the survival probability of an inverse Gaussian random variable, allowing direct inversion through its quantile function.

Load-bearing premise

The Black-Scholes call price must be exactly equal to the survival probability of an inverse Gaussian distribution.

What would settle it

Take a known volatility, compute the corresponding Black-Scholes call price, insert that price into the proposed explicit formula, and check whether the original volatility is recovered to machine precision.

Figures

read the original abstract

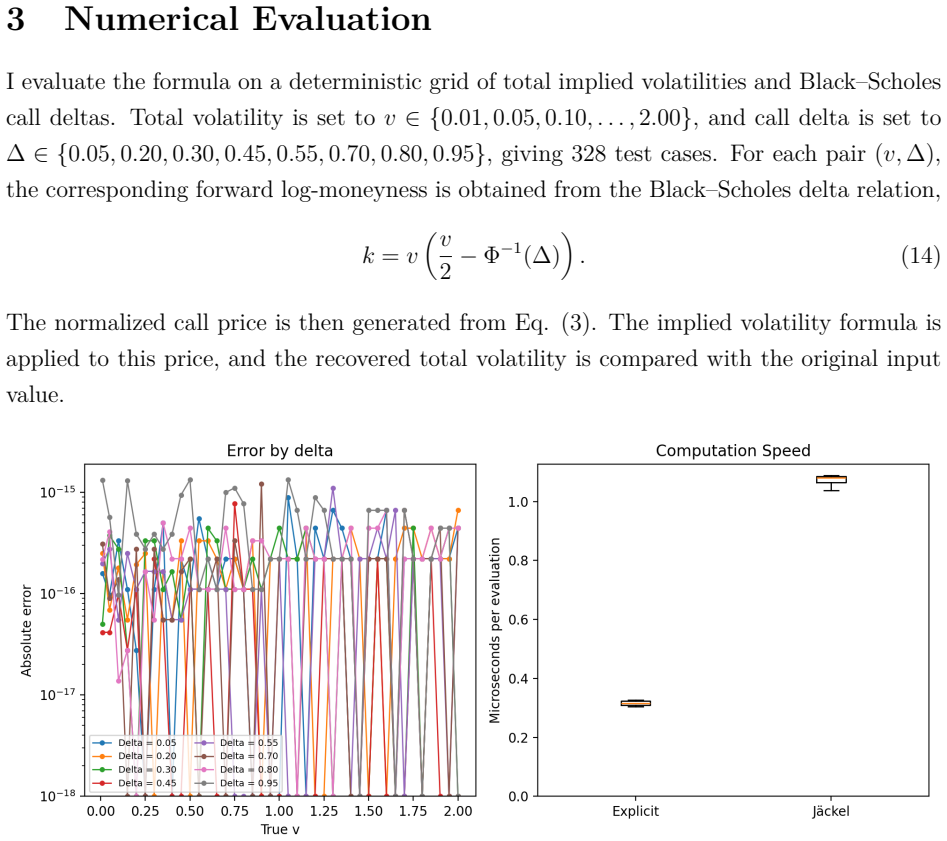

This paper observes that the Black--Scholes call price can be written as the survival probability of an inverse Gaussian distribution, equivalently as a probability in variance space. Inverting this representation yields an analytically explicit formula for implied volatility in terms of the corresponding inverse Gaussian quantile function, with volatility on the left-hand side and only observable option inputs on the right-hand side. Numerical tests recover implied volatility to machine precision and, in a controlled setting, show the formula to be faster than a state-of-the-art benchmark.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that the normalized Black-Scholes call price equals the survival function of an inverse Gaussian distribution evaluated at 1/sigma^2, once mu and lambda are set to match the coefficients gamma = sqrt(T)/2, beta = ln(S/(K e^{-rT}))/sqrt(T) and delta = K e^{-rT}/S (allowing mu negative when delta < 1). Inverting this identity via the inverse Gaussian quantile function produces an explicit formula for implied volatility with volatility on the left-hand side and only observable inputs on the right-hand side. Numerical tests recover the true implied volatility to machine precision and outperform a state-of-the-art benchmark in speed.

Significance. If the functional identity holds exactly, the result supplies the first closed-form expression for Black-Scholes implied volatility, eliminating iterative solvers. The paper's machine-precision numerical recovery and reported speed advantage constitute reproducible evidence of practicality; the approach is parameter-free and rests on a direct probabilistic re-expression rather than fitting or self-reference.

minor comments (1)

- The abstract and introduction would benefit from an explicit one-line statement of the three IG parameters (gamma, beta, delta) immediately after the survival-function claim, to make the inversion step transparent at first reading.

Simulated Author's Rebuttal

We thank the referee for their positive assessment of the manuscript and their recommendation to accept. The referee's summary accurately captures the central contribution: an explicit expression for Black-Scholes implied volatility obtained by inverting the representation of the normalized call price as an inverse-Gaussian survival function.

Circularity Check

No significant circularity identified

full rationale

The paper re-expresses the normalized Black-Scholes call price exactly as the survival function of an inverse Gaussian random variable by matching the coefficients gamma = sqrt(T)/2, beta = ln(S/(K e^{-rT}))/sqrt(T) and delta = K e^{-rT}/S (allowing mu negative when delta < 1). Inverting the survival function then yields implied volatility as the IG quantile function evaluated at the normalized call price, with only observable inputs on the right-hand side. This is a direct algebraic inversion of an identity, not a fitted parameter, self-referential definition, or load-bearing self-citation. The derivation chain is self-contained against the external benchmark of the original BS formula and recovers machine precision numerically, confirming independence from any circular reduction.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The Black-Scholes call price equals the survival probability of an inverse Gaussian distribution.

Reference graph

Works this paper leans on

-

[1]

doi: 10.21314/JCF.2009.198. R. S. Chhikara and J. L. Folks.The Inverse Gaussian Distribution: Theory, Methodology, and Applications. Marcel Dekker, New York,

-

[2]

doi: 10.3905/ JOD.2020.1.127. S. Gerhold. Can there be an explicit formula for implied volatility?Quarterly Journal of Mathematics, 63:423–436,

2020

-

[3]

P. Jäckel. Let’s be rational.Wilmott, 2015(75):40–53,

2015

-

[4]

doi: 10.1002/wilm.10395. P. Jäckel. Let’s Be Rational: Reference implementation.http://www.jaeckel.org/ LetsBeRational.7z,

-

[5]

Nominal revision 1520, dated 2024-02-16; accessed 2026-04-24. B. Jørgensen.Statistical Properties of the Generalized Inverse Gaussian Distribution, vol- ume 9 ofLecture Notes in Statistics. Springer, New York,

2024

-

[6]

doi: 10.1080/14697688.2019.1675898. M. R. Tehranchi. Uniform bounds for black–scholes implied volatility.SIAM Journal on Financial Mathematics, 7(1):893–916,

-

[7]

doi: 10.1137/14095248X. vollib. Blazingly fast & accurate: Option pricing, implied volatility, and greeks.https: //vollib.org/,

-

[8]

Accessed 2026-04-25. 9

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.