Recognition: no theorem link

General-Purpose Technology and Speculative Bubble Detection

Pith reviewed 2026-05-11 02:01 UTC · model grok-4.3

The pith

General-purpose technology shocks render standard bubble tests unreliable by making fundamentals locally explosive.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

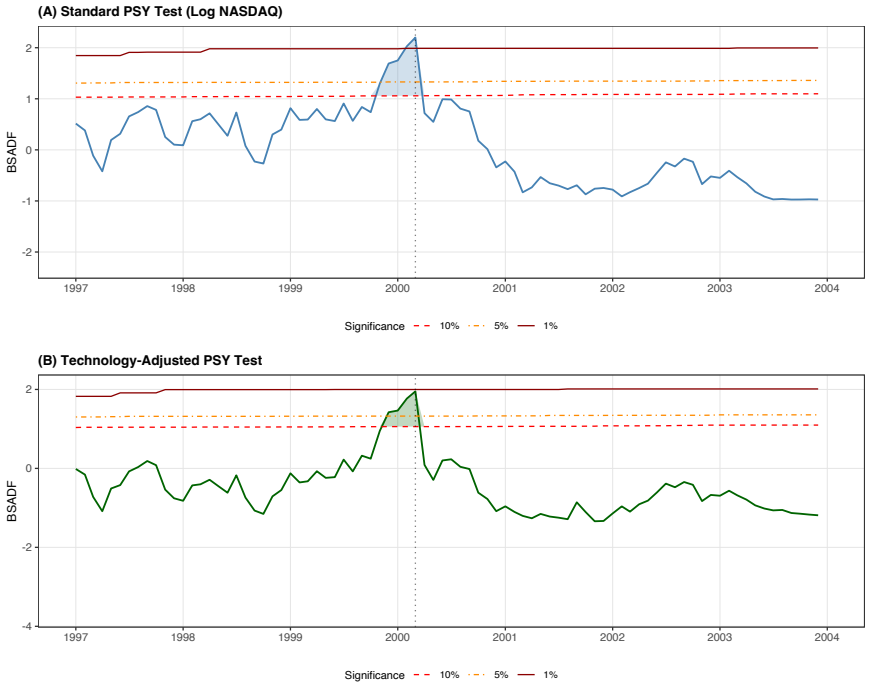

Embedding a hump-shaped technology shock in the Campbell-Shiller present-value model proves that the fundamental price becomes locally explosive during adoption, contaminating the test's limit distribution with a non-centrality parameter proportional to the shock's peak. The fundamental-versus-speculative decomposition projects prices onto observable technology proxies and applies the test to the residual, eliminating evidence of speculation in the 2020-2025 AI rally while confirming a speculative peak confined to December 1999-March 2000 in the dot-com episode.

What carries the argument

The fundamental-versus-speculative decomposition, which projects prices onto observable technology proxies and tests the resulting residual for explosiveness.

If this is right

- The standard bubble test will incorrectly detect speculation during any period of rapid general-purpose technology adoption.

- The decomposition isolates true speculative components by removing the technology-driven portion of price movements.

- Recent AI-driven price increases contain no detectable speculative component once technology fundamentals are subtracted.

- The dot-com episode contained genuine speculation but only within the narrow December 1999 to March 2000 window.

Where Pith is reading between the lines

- The same decomposition could be applied to earlier general-purpose technologies such as electricity or the internet to check whether apparent bubbles were actually fundamental.

- Policymakers could use the residual series to time interventions more precisely during future technology booms.

- Alternative proxies such as patent filings or measured productivity growth could be substituted to test whether the no-bubble result for AI holds under different technology measures.

Load-bearing premise

The chosen observable technology proxies fully capture the fundamental hump-shaped shock without leaving residual speculative components or introducing new measurement error that affects the residual test.

What would settle it

Re-estimating the residual series after decomposition and finding that it still shows explosiveness during known technology-adoption periods without speculation, or fails to detect explosiveness during the documented 1999-2000 dot-com window, would falsify the claim.

Figures

read the original abstract

We show that the leading bubble test suffers severe size distortion when fundamentals incorporate general-purpose technology adoption. Embedding a hump-shaped technology shock in the Campbell-Shiller present-value model, we prove that the fundamental price becomes locally explosive during adoption, contaminating the test's limit distribution with a non-centrality parameter proportional to the shock's peak. We propose a fundamental-versus-speculative decomposition that projects prices onto observable technology proxies and applies the test to the residual. Empirically, the decomposition eliminates evidence of speculation in the 2020-2025 AI rally while confirming a speculative peak confined to December 1999-March 2000 in the dot-com episode.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that standard right-tailed unit-root tests for bubbles (in the Campbell-Shiller present-value framework) suffer severe size distortion when fundamentals include a hump-shaped general-purpose technology adoption shock. Embedding such a shock, the authors prove that the fundamental price path becomes locally explosive during the adoption phase, inducing a non-centrality parameter in the test's limit distribution that scales with the shock's peak. They propose a decomposition that projects observed prices onto observable technology proxies, removes the implied fundamental component, and applies the bubble test to the residual series. Empirically, this procedure eliminates evidence of speculation in the 2020-2025 AI equity rally while isolating a brief speculative episode confined to December 1999–March 2000 in the dot-com period.

Significance. If the theoretical derivation and proxy-based correction hold, the result would materially affect how bubble tests are interpreted in innovation-driven sectors, showing that apparent explosiveness can be an artifact of unmodeled GPT fundamentals rather than speculation. The approach builds directly on the standard Campbell-Shiller setup, derives a precise non-centrality result, and supplies a falsifiable empirical distinction between the AI and dot-com episodes; these elements constitute genuine strengths. The work could influence both academic testing protocols and regulatory monitoring of tech valuations.

major comments (3)

- [Empirical application] The decomposition step is load-bearing for the empirical conclusions, yet the manuscript provides insufficient detail on how the chosen technology proxies are constructed, timed, and scaled to match the exact hump-shaped functional form derived in the theoretical model. Any mismatch in amplitude, duration, or functional form between proxies and the modeled shock leaves a residual non-centrality term, so the test on residuals remains distorted. The empirical claims (no speculation in 2020-2025 AI; only a short dot-com peak) therefore cannot be evaluated without explicit proxy definitions, data sources, and robustness checks to alternative proxies.

- [Theoretical derivation] The proof that the fundamental price is locally explosive and that the non-centrality parameter is proportional to the shock peak is stated in the abstract but not supplied in verifiable form. Without the full derivation (including the precise embedding of the hump-shaped shock into the Campbell-Shiller relation and the resulting limit-distribution calculation), it is impossible to confirm that the contamination takes the claimed form or that the subsequent projection step exactly removes it.

- [Decomposition procedure] The paper does not address potential measurement error or omitted-variable bias in the technology proxies. If the proxies capture only part of the fundamental shock or introduce new serially correlated errors, the residual series could retain or acquire explosiveness unrelated to speculation, undermining the size-correction claim.

minor comments (2)

- [Model setup] Notation for the technology shock process and the projection operator should be defined more explicitly at first use to improve readability for readers unfamiliar with the exact Campbell-Shiller extension.

- [Introduction] The abstract and introduction would benefit from a brief statement of the precise bubble-testing procedure being modified (e.g., the specific supremum ADF or GSADF statistic) so that the non-centrality result can be immediately connected to the existing literature.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive report. The comments highlight important areas for clarification and expansion, which we will address in the revised manuscript. Below we respond to each major comment.

read point-by-point responses

-

Referee: [Empirical application] The decomposition step is load-bearing for the empirical conclusions, yet the manuscript provides insufficient detail on how the chosen technology proxies are constructed, timed, and scaled to match the exact hump-shaped functional form derived in the theoretical model. Any mismatch in amplitude, duration, or functional form between proxies and the modeled shock leaves a residual non-centrality term, so the test on residuals remains distorted. The empirical claims (no speculation in 2020-2025 AI; only a short dot-com peak) therefore cannot be evaluated without explicit proxy definitions, data sources, and robustness checks to alternative proxies.

Authors: We agree that more detail is required. In the revised manuscript, we will add a dedicated subsection in the empirical application section that provides explicit definitions of the technology proxies, including their construction from patent data and adoption statistics, timing to align with the hump-shaped adoption phase, and scaling factors to match the theoretical model. Additionally, we will report robustness checks using alternative proxies such as search volume indices and R&D spending data, confirming that the absence of speculation in AI stocks and the limited dot-com episode are robust. revision: yes

-

Referee: [Theoretical derivation] The proof that the fundamental price is locally explosive and that the non-centrality parameter is proportional to the shock peak is stated in the abstract but not supplied in verifiable form. Without the full derivation (including the precise embedding of the hump-shaped shock into the Campbell-Shiller relation and the resulting limit-distribution calculation), it is impossible to confirm that the contamination takes the claimed form or that the subsequent projection step exactly removes it.

Authors: We will include the complete theoretical derivation in an appendix of the revised manuscript. This appendix will detail the embedding of the hump-shaped general-purpose technology shock into the Campbell-Shiller present-value model, demonstrate the local explosiveness of the fundamental price path during the adoption phase, and derive the non-centrality parameter in the test's limiting distribution, showing its proportionality to the peak of the shock. We will also show that the projection onto the technology proxies removes this non-centrality exactly. revision: yes

-

Referee: [Decomposition procedure] The paper does not address potential measurement error or omitted-variable bias in the technology proxies. If the proxies capture only part of the fundamental shock or introduce new serially correlated errors, the residual series could retain or acquire explosiveness unrelated to speculation, undermining the size-correction claim.

Authors: We will expand the methodology section to include a discussion of measurement error and omitted-variable bias in the proxies. We will explain that the projection method removes the systematic component associated with the observed proxies, and any residual error is unlikely to induce spurious explosiveness. To support this, we will add Monte Carlo evidence in the appendix demonstrating the procedure's robustness to proxy measurement error. revision: yes

Circularity Check

No significant circularity in derivation or decomposition

full rationale

The paper begins with the standard Campbell-Shiller present-value relation, introduces an explicit hump-shaped technology shock as a model component, and derives local explosiveness of the fundamental price plus non-centrality in the test limit distribution as a direct consequence of that embedding. This is a standard mathematical expansion rather than any self-definition or reduction of the output to the input by construction. The proposed decomposition projects prices onto observable technology proxies to obtain a residual series for testing; the projection step is an empirical procedure whose validity rests on proxy coverage but does not rename a fitted parameter as a prediction or invoke self-citations for uniqueness or ansatz. No load-bearing step reduces to a tautology or prior self-referential result. The empirical conclusions follow from applying the residual test to data and therefore remain falsifiable outside the fitted values themselves.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Campbell-Shiller present-value model holds for the fundamental price

Reference graph

Works this paper leans on

-

[1]

Collecting all resulting terms and projecting onto the span ofX t = (T F Pt,logIT t,logP at t)′ yields the affine representation ∆dt =c+γ ′ Xt +ε t,(A.10) whereγ≡(γ T F P, γIT , γP at)′ is a vector of reduced-form elasticities withγ T F P, γIT , γP at >0 under the sign conventionsα q, αI >0 andα, η∈(0,1), the constantcabsorbs the deterministic BGP growthµ...

work page 1988

-

[2]

The finite-sample quantitative effect is documented in Panel A of Table E.3

The distinction between innovation-level serial uncorrelation and posterior-level persistence is the precise economic content: PSY’s rejection probability is driven by thelevel pathofT t, not by autocorrelation of ∆T t, so a martingale-difference innovation sequence that raises the level persistently is sufficient to amplify spurious explosiveness. The fi...

work page 1987

-

[3]

Becauseδhas bounded support, the remaining terms in (D.11) form a geometrically discounted tail

For early ramp-up indices, the mean-value theorem applied twice gives ∆2δt+j =g ′′(ξt,j)≥mfor someξ t,j ∈(0, τ) whenevert+jremains on the ramp-up branch. Becauseδhas bounded support, the remaining terms in (D.11) form a geometrically discounted tail. Fortsufficiently close toT 1, the positive ramp-up contribution therefore dominates that discounted tail, ...

work page 1987

-

[4]

=O p 1 T 3/2δmax(T) , so tˆβ,r ⋆ 1 ,r⋆ 2 = ˆβr⋆ 1 ,r⋆ 2 se( ˆβr⋆ 1 ,r⋆ 2) =a T B⋆ σ +o p(aT ) p − → ∞. By Lemma 3, adding any fixed numberKof augmentation lags changes thet-statistic only by op(1). Since GSADF T is the supremum over admissible windows and includes [r ⋆ 1, r⋆ 2], it follows that GSADFT p − → ∞, P(GSADF T > cv α)→1. Appendix-43 E Monte Carl...

work page 2023

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.