Multi-regime Markov-switching models with time-varying transition probabilities: An application to U.S. Treasury yields

Pith reviewed 2026-06-30 20:09 UTC · model grok-4.3

The pith

Multi-regime Markov-switching models recover means, variances and transition probabilities reliably but find GAS score coefficients non-identifiable.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

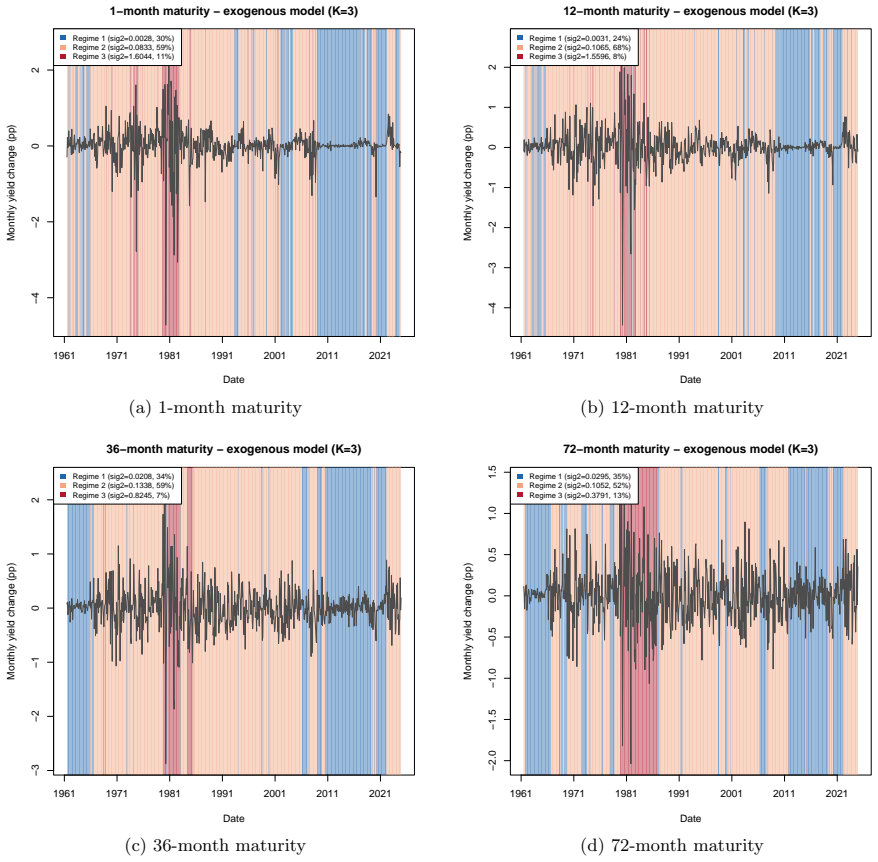

We extend the two-regime common-variance GAS model to the general K-regime case with regime-specific means and variances. Monte Carlo simulations recover regime means, variances and transition probabilities reliably, but the TVTP driving coefficients are harder to identify; the GAS score coefficient is statistically non-identifiable because of a ridge in the joint likelihood surface for sigma squared and A. One-step point forecasts prove robust to TVTP misspecification while filtered regime probabilities are not. In Treasury yield changes an exogenous lagged-level driver dominates constant and lagged-change models, and the GAS specification fails to converge with hat A collapsing to zero.

What carries the argument

The multi-regime TVTP Markov-switching model under constant, exogenous and GAS specifications of the transition matrix, together with the associated Monte Carlo design for checking parameter recovery.

If this is right

- Accurate characterization of regime dynamics requires correct specification of the time-varying transition probabilities.

- Short-horizon point forecasts remain stable across different TVTP choices.

- The GAS score coefficient is liable to collapse to zero in financial series that exhibit the same ridge observed in simulation.

- An exogenous driver based on the lagged yield level improves model fit relative to constant-transition or lagged-change alternatives.

Where Pith is reading between the lines

- Practitioners may prefer simple exogenous drivers over score-driven transitions when modeling interest-rate regimes.

- The non-identifiability of the GAS coefficient may appear in other score-driven regime models applied to persistent financial series.

- Re-running the Monte Carlo design with data-generating processes that include measurement error or structural breaks would test how fragile the recovery results are.

Load-bearing premise

The Monte Carlo data-generating processes accurately represent the identifiability properties that will hold for real financial series.

What would settle it

Re-estimate the GAS specification on the same Treasury series or on simulated series drawn from the fitted exogenous model and check whether the likelihood surface still exhibits the reported ridge between sigma squared and the score coefficient A.

Figures

read the original abstract

This paper studies Markov-switching (MS) models with time-varying transition probabilities (TVTP) under various specifications of the transition probability matrix. Especially, we extend the two-regime common-variance setting of the Generalized Autoregressive Score (GAS) model from (Bazzi et al., 2017) to the general $K$-regime case with regime-specific means and variances. Our study contains comprehensive Monte Carlo simulations and we developed an open-source R package, \texttt{multiregimeTVTP}, for data simulation and parameter estimation. We find that the regime means, variances, and transition probabilities are reliably recovered, whereas the TVTP driving coefficients are harder to identify. Another finding from our paper is that the GAS score coefficient appears to be statistically non-identifiable, due to a ridge in the joint likelihood surface $(\sigma^2,A)$. In addition, we find that one-step point forecasts are remarkably robust to TVTP misspecification, but filtered regime probabilities are not, so correct specification matters most for characterizing regime dynamics rather than short-horizon forecasting. An empirical application to U.S. Treasury zero-coupon yield changes at four maturities (1961-2024) shows that an exogenous specification driven by the lagged yield level dominates the constant and lagged-change models in fit, while the GAS specification fails to converge, with $\hat{A}$ collapsing to zero, reflecting the same identifiability issue observed in simulation.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript extends the two-regime common-variance GAS Markov-switching model with time-varying transition probabilities (Bazzi et al., 2017) to the general K-regime case allowing regime-specific means and variances. It reports Monte Carlo experiments on parameter recovery across constant, exogenous, and GAS-driven TVTP specifications, releases an open-source R package multiregimeTVTP, finds reliable recovery of regime means/variances/transition probabilities but harder identification of TVTP driving coefficients and a ridge rendering the GAS score coefficient A non-identifiable in the joint (σ^{2}, A) surface, shows one-step forecasts robust to TVTP misspecification while filtered probabilities are sensitive, and applies the models to U.S. Treasury zero-coupon yield changes (1961-2024) where the lagged-yield exogenous specification dominates and GAS fails to converge with  o 0.

Significance. If the reported identifiability patterns and forecast robustness hold, the work supplies concrete practical guidance for applied researchers on when and why TVTP extensions add value versus constant-transition models in financial series, particularly distinguishing forecasting from regime-characterization uses. The release of the multiregimeTVTP R package for simulation and estimation is a clear strength that supports reproducibility and extension by others.

major comments (2)

- [Section 4] Section 4 (Monte Carlo design): the data-generating processes are constructed from the same K-regime MS-TVTP family being estimated. While this correctly demonstrates recovery and the (σ^{2}, A) ridge under correct specification, it leaves open whether the relative difficulty of identifying TVTP coefficients and the non-identifiability of A transfer to realistic departures (heavier tails, omitted factors, or non-Markovian dynamics) that are plausible for Treasury yields; this directly affects the strength of the claim that regime parameters are 'reliably recovered' versus TVTP coefficients being 'harder to identify' when applied to real data.

- [Section 5] Section 5 (empirical results) and the abstract claim on forecast robustness: the statement that 'one-step point forecasts are remarkably robust to TVTP misspecification' rests on the specific misspecification experiments performed in the Monte Carlo section. No additional out-of-sample forecast diagnostics are reported for the Treasury application itself (where GAS fails to converge), so it is unclear whether the robustness conclusion extends to the empirical setting that motivates the study.

minor comments (2)

- [Abstract] Notation: the abstract and text refer to 'the GAS score coefficient' without always reminding the reader that this is the parameter A in the score-driven update; a brief parenthetical on first use would improve clarity.

- [Section 4] Table/figure captions: several Monte Carlo tables report convergence rates and bias but do not explicitly state the number of Monte Carlo replications or the optimization settings used; adding these details would aid reproducibility.

Simulated Author's Rebuttal

We thank the referee for the constructive comments. We respond to each major comment below, indicating planned revisions where appropriate.

read point-by-point responses

-

Referee: [Section 4] Section 4 (Monte Carlo design): the data-generating processes are constructed from the same K-regime MS-TVTP family being estimated. While this correctly demonstrates recovery and the (σ^{2}, A) ridge under correct specification, it leaves open whether the relative difficulty of identifying TVTP coefficients and the non-identifiability of A transfer to realistic departures (heavier tails, omitted factors, or non-Markovian dynamics) that are plausible for Treasury yields; this directly affects the strength of the claim that regime parameters are 'reliably recovered' versus TVTP coefficients being 'harder to identify' when applied to real data.

Authors: We agree the Monte Carlo design isolates identifiability issues (including the (σ², A) ridge) under correct specification, which is valuable for understanding the model's properties. The empirical results are consistent with these findings, as the GAS specification fails to converge with  → 0. However, we acknowledge that the design does not directly test robustness to realistic misspecifications such as heavier tails or non-Markovian dynamics. In revision we will add a dedicated limitations paragraph discussing this scope and its implications for generalizing the recovery claims to real data. revision: partial

-

Referee: [Section 5] Section 5 (empirical results) and the abstract claim on forecast robustness: the statement that 'one-step point forecasts are remarkably robust to TVTP misspecification' rests on the specific misspecification experiments performed in the Monte Carlo section. No additional out-of-sample forecast diagnostics are reported for the Treasury application itself (where GAS fails to converge), so it is unclear whether the robustness conclusion extends to the empirical setting that motivates the study.

Authors: The robustness claim for one-step forecasts is explicitly based on the Monte Carlo misspecification experiments. In the Treasury application we report only in-sample fit comparisons among converging specifications (constant and exogenous TVTP), noting GAS non-convergence. We will add out-of-sample one-step forecast evaluation for the converging models in the revised empirical section to directly assess whether the Monte Carlo robustness pattern holds in the motivating data. revision: partial

Circularity Check

No significant circularity detected

full rationale

The paper extends the two-regime GAS model of Bazzi et al. (2017) to K regimes and reports Monte Carlo recovery rates plus an empirical Treasury-yield application. All load-bearing claims (reliable recovery of means/variances/transition probabilities, non-identifiability of the GAS score coefficient via the observed ridge in (σ²,A), robustness of one-step forecasts) are obtained from fresh simulations drawn from the authors' own DGP and from real data; they do not reduce to any fitted parameter renamed as a prediction, to a self-citation chain, or to an ansatz smuggled through prior work. The citation to Bazzi et al. merely identifies the baseline being generalized and carries no uniqueness theorem or definitional load for the new results.

Axiom & Free-Parameter Ledger

free parameters (2)

- TVTP driving coefficients

- GAS score coefficient A

axioms (1)

- domain assumption The data-generating process in the Monte Carlo experiments belongs to the same parametric family as the estimated models.

Reference graph

Works this paper leans on

-

[1]

doi: 10.1080/07350015.1994.10524546. Marcelle Chauvet.An econometric characterization of business cycle dynamics with factor structure and regime switching. University of Pennsylvania, 1995. Stephen F Gray. Modeling the conditional distribution of interest rates as a regime-switching process.Journal of financial economics, 42(1):27–62, 1996. Rene Garcia a...

-

[2]

doi: 10.1016/j.econlet.2012.10.035. G. D. Berentsen, J. Bulla, A. Maruotti, and B˚ ard Støve. Modelling clusters of corporate defaults: Regime- switching models significantly reduce the contagion source.Journal of the Royal Statistical Society: Series C (Applied Statistics), 71:698 – 722, 2022. doi: 10.1111/rssc.12551. Francis X Diebold, Joon-Haeng Lee, a...

-

[3]

Drew Creal, Siem Jan Koopman, and Andr´ e Lucas

URLhttps://ideas.repec.org/p/fip/fedkrw/98-09.html. Drew Creal, Siem Jan Koopman, and Andr´ e Lucas. Generalized autoregressive score models with applications. Journal of applied econometrics, 28(5):777–795, 2013. M. Neale, S. Clark, C. Dolan, and Michael D. Hunter. Regime switching modeling of substance use: Time- varying and second-order markov models a...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.