Optimal Dynamic Fees for Automated Market Makers: A Stochastic Control Approach to Loss-Versus-Rebalancing

Pith reviewed 2026-06-26 12:17 UTC · model grok-4.3

The pith

The growth-optimal fee for an AMM liquidity provider depends only on instantaneous volatility, is independent of wealth and risk aversion, and rises with variance.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

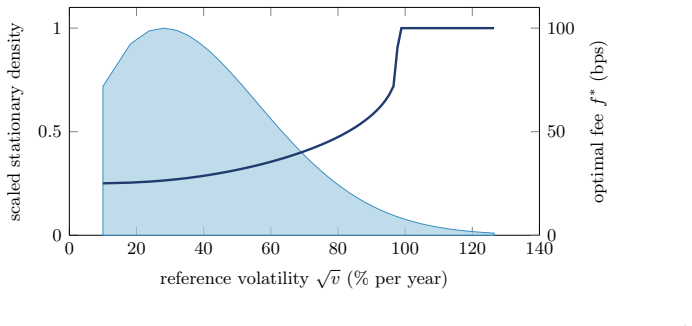

We prove that the growth-optimal fee is independent of the LP's wealth and of its constant relative risk aversion, that it collapses to a static constant when volatility is constant, and that it is strictly increasing in instantaneous variance, so that the optimal schedule is pro-cyclical. When volatility is stochastic, we characterise the optimal fee through a scalar ergodic Hamilton-Jacobi-Bellman equation and a linear Poisson equation, solved by a finite-difference scheme. We further show that the optimal fee is invariant to price jumps under logarithmic preferences.

What carries the argument

The fee enters only the drift of relative wealth and never its diffusion, reducing the problem to an ergodic control problem whose solution is pointwise volatility feedback.

If this is right

- The optimal fee collapses to a static constant under constant volatility.

- The optimal fee is strictly increasing in instantaneous variance.

- The optimal fee is invariant to price jumps under logarithmic preferences.

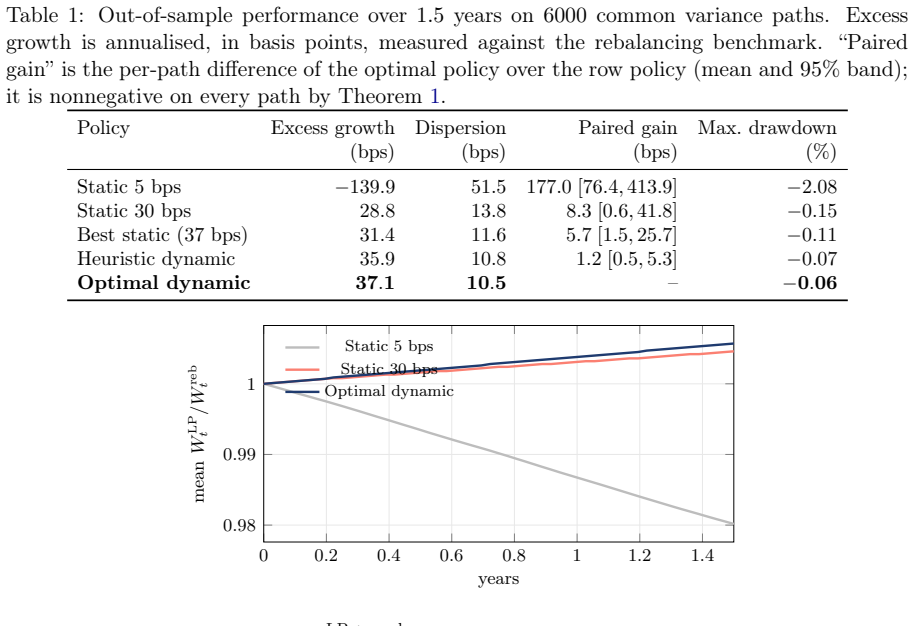

- The optimal dynamic fee weakly dominates static and volatility-linked heuristics in calibrated simulations.

- Gas costs can be incorporated via an impulse-control dead-band with negligible impact.

Where Pith is reading between the lines

- If implemented in programmable AMMs, this would lead to pro-cyclical fee schedules that charge more during volatile periods.

- The independence from risk aversion suggests the policy maximizes growth even for highly risk-averse providers.

- This framework could apply to other market-making venues where fees affect only expected returns.

- The reduction to a scalar equation makes real-time computation feasible for on-chain execution.

Load-bearing premise

The fee affects only the drift of the LP's relative wealth process and has no effect on its diffusion term.

What would settle it

A numerical experiment or market simulation in which the computed dynamic fee produces a lower long-run growth rate than a well-chosen static fee under stochastic volatility would falsify the optimality claim.

Figures

read the original abstract

We study the fee policy of a liquidity provider (LP) in a constant-product automated market maker (AMM) whose fee can be adjusted continuously, as enabled by programmable hooks. Building on the loss-versus-rebalancing (LVR) framework of Milionis et al. (2022) and its extension to nonzero fees by Milionis et al. (2024), we model the LP's wealth relative to the continuously rebalanced benchmark as a controlled process in which the fee governs two opposing forces: it raises revenue per uninformed trade while discouraging uninformed volume, and it widens the no-arbitrage band, which lowers the rate at which arbitrageurs extract value. Because the fee enters only the drift of relative wealth and never its diffusion, the LP's expected-utility problem reduces to an ergodic control problem whose solution is a pointwise volatility feedback. We prove that the growth-optimal fee is independent of the LP's wealth and of its constant relative risk aversion, that it collapses to a static constant when volatility is constant, and that it is strictly increasing in instantaneous variance, so that the optimal schedule is pro-cyclical. When volatility is stochastic, we characterise the optimal fee through a scalar ergodic Hamilton-Jacobi-Bellman equation and a linear Poisson equation, solved by a finite-difference scheme. We further show that the optimal fee is invariant to price jumps under logarithmic preferences, relate the optimal fee to a stylised model of competition among venues, and treat gas costs through an impulse-control dead-band. In a calibration to liquid large-capitalisation conditions, the optimal dynamic fee weakly dominates every static and volatility-linked heuristic fee on each simulated path, improving the LP's growth rate over the best static fee by a modest but uniformly positive margin, with a dead-band rendering gas costs negligible.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper models an LP's relative wealth process in a constant-product AMM with dynamically adjustable fees enabled by hooks. Building on the LVR framework, it posits that the fee control appears exclusively in the drift term of relative wealth (raising revenue while widening the no-arbitrage band and reducing uninformed volume) and leaves the diffusion coefficient unchanged. This permits reduction of the expected-utility maximization to an ergodic stochastic control problem whose HJB equation admits pointwise optimization over instantaneous variance. The authors prove that the growth-optimal fee is independent of initial wealth and of any constant relative risk aversion parameter, collapses to a constant under constant volatility, and is strictly increasing in instantaneous variance (hence pro-cyclical). When volatility is stochastic they characterize the optimum via a scalar ergodic HJB plus linear Poisson equation solved by finite differences, treat jumps under log utility, incorporate gas costs via impulse control, and calibrate to show modest but uniform outperformance versus static and heuristic fees.

Significance. If the drift-only modeling step is rigorously justified, the independence results and the explicit ergodic HJB characterization constitute a clean theoretical advance for dynamic fee design in programmable AMMs. The finite-difference solution of the scalar ergodic equation and the calibration exercise that reports uniform dominance on every simulated path are concrete, reproducible contributions. The work supplies a falsifiable prediction (optimal fees rise with instantaneous variance) that can be tested against on-chain data once hooks are live.

major comments (2)

- [Abstract and §2 (model derivation)] The reduction to an ergodic control problem whose solution is pointwise volatility feedback rests entirely on the assertion that the fee enters only the drift of relative wealth and never its diffusion coefficient. The abstract states this property but the manuscript provides neither the explicit SDE for the relative-wealth process nor a derivation showing that the quadratic-variation term is independent of the fee (via volume-dependent intensity or via the no-arbitrage band affecting effective exposure). Without this step the claimed wealth- and CRRA-independence, the collapse to a constant under constant volatility, and the strict monotonicity in variance do not follow from the stated HJB.

- [§4 (numerical solution) and §5 (calibration)] The finite-difference scheme for the ergodic HJB and Poisson equation is presented without verification against a known closed-form case (e.g., constant volatility) or against Monte-Carlo simulation of the controlled process. Because the central claims are quantitative (growth-rate improvement, pro-cyclicality), numerical confirmation that the scheme recovers the analytically known constant-vol solution is required before the calibration results can be trusted.

minor comments (2)

- [Abstract] The abstract claims proofs of independence properties; the manuscript should state explicitly in which theorem or proposition each independence result is established.

- [§2] Notation for the relative-wealth process, the fee control, and the instantaneous variance process should be introduced once in a dedicated subsection rather than piecemeal.

Simulated Author's Rebuttal

We thank the referee for the thorough reading and constructive feedback. The two major comments identify gaps in the presentation of the model derivation and in the validation of the numerical scheme. We address each point below and will revise the manuscript to incorporate the requested material.

read point-by-point responses

-

Referee: [Abstract and §2 (model derivation)] The reduction to an ergodic control problem whose solution is pointwise volatility feedback rests entirely on the assertion that the fee enters only the drift of relative wealth and never its diffusion coefficient. The abstract states this property but the manuscript provides neither the explicit SDE for the relative-wealth process nor a derivation showing that the quadratic-variation term is independent of the fee (via volume-dependent intensity or via the no-arbitrage band affecting effective exposure). Without this step the claimed wealth- and CRRA-independence, the collapse to a constant under constant volatility, and the strict monotonicity in variance do not follow from the stated HJB.

Authors: We agree that an explicit derivation of the relative-wealth SDE is required for the reduction to the ergodic problem to be fully self-contained. Although the modeling step follows directly from the LVR framework in the cited works (Milionis et al. 2022, 2024), the present manuscript does not reproduce the SDE or the argument that the quadratic variation is unaffected by the fee. In the revision we will insert a dedicated subsection in §2 that derives the controlled SDE from first principles, showing that the fee modulates only the drift (via revenue, volume, and no-arbitrage band) while leaving the diffusion coefficient unchanged. This will make the subsequent HJB reduction and the independence results transparent. revision: yes

-

Referee: [§4 (numerical solution) and §5 (calibration)] The finite-difference scheme for the ergodic HJB and Poisson equation is presented without verification against a known closed-form case (e.g., constant volatility) or against Monte-Carlo simulation of the controlled process. Because the central claims are quantitative (growth-rate improvement, pro-cyclicality), numerical confirmation that the scheme recovers the analytically known constant-vol solution is required before the calibration results can be trusted.

Authors: We concur that verification of the finite-difference scheme against the analytically solvable constant-volatility case is necessary to support the quantitative claims. The current manuscript reports only the calibration results without such checks. In the revised version we will add, in §4, (i) a direct comparison of the numerical solution under constant volatility with the closed-form constant fee derived in §3, and (ii) Monte-Carlo paths of the controlled relative-wealth process that confirm the growth-rate improvement matches the ergodic value function. These diagnostics will be placed before the stochastic-volatility calibration. revision: yes

Circularity Check

No significant circularity; central reduction rests on external modeling framework and explicit assumption.

full rationale

The paper cites Milionis et al. (2022, 2024) by different authors for the base LVR setup and extends it with a controlled relative-wealth process. The load-bearing claim that 'the fee enters only the drift of relative wealth and never its diffusion' is stated as a direct consequence of the AMM mechanics and fee policy (widening no-arbitrage band, revenue vs. volume trade-off) rather than derived from the target results. The ergodic HJB, pointwise volatility feedback, wealth/CRRA independence, and pro-cyclicality then follow from standard stochastic control arguments applied to that generator; none of these steps reduce by construction to a fit, self-definition, or self-citation chain. The derivation is therefore self-contained against the stated assumptions.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Fee enters only the drift of relative wealth and never its diffusion

Reference graph

Works this paper leans on

-

[1]

Adams, A., Moallemi, C. C., Reynolds, S., Robinson, D. (2024).am-AMM: An Auction-Managed Automated Market Maker. Financial Cryptography and Data Security (FC 2025), Springer LNCS 15751. arXiv:2403.03367. 16

-

[2]

(2024).Uniswap v4 Core

Adams, H., Salem, M., Zinsmeister, N., Reynolds, S., Adams, A., Pote, W., Toda, M., Henshaw, A., Williams, E., Robinson, D. (2024).Uniswap v4 Core. Uniswap Labs technical whitepaper

2024

-

[3]

Angeris, G., Chitra, T. (2020). Improved price oracles: Constant function market makers.Proc. 2nd ACM Conf. on Advances in Financial Technologies (AFT ’20), 80–91

2020

-

[4]

Angeris, G., Kao, H.-T., Chiang, R., Noyes, C., Chitra, T. (2021). An analysis of Uniswap markets. Cryptoeconomic Systems1(1)

2021

-

[5]

Aqsha, A., Bergault, P., Sánchez-Betancourt, L. (2026). Equilibrium reward for liquidity providers in automated market makers.Mathematical Finance, forthcoming. DOI:10.1111/mafi.70030. arXiv:2503.22502

-

[6]

Avellaneda, M., Stoikov, S. (2008). High-frequency trading in a limit order book.Quantitative Finance8(3), 217–224

2008

-

[7]

(2025).Optimal Dynamic Fees in Automated Market Makers

Baggiani, L., Herdegen, M., Sánchez-Betancourt, L. (2025).Optimal Dynamic Fees in Automated Market Makers. arXiv:2506.02869

-

[8]

(2026).Competition between DEXs through Dynamic Fees

Baggiani, L., Herdegen, M., Sánchez-Betancourt, L. (2026).Competition between DEXs through Dynamic Fees. arXiv:2603.09669

-

[9]

Bergault, P., Bertucci, L., Bouba, D., Guéant, O.(2024).Automatedmarketmakers: Mean-variance analysis of LPs payoffs and design of pricing functions.Digital Finance6(2), 225–247

2024

-

[10]

(2025).Optimal Exit Time for Liquidity Providers in Automated Market Makers

Bergault, P., Bieber, S., Sánchez-Betancourt, L. (2025).Optimal Exit Time for Liquidity Providers in Automated Market Makers. arXiv:2509.06510

-

[11]

(2025).Optimal Fees for Liquidity Provision in Automated Market Makers

Campbell, J., Bergault, P., Milionis, J., Nutz, M. (2025).Optimal Fees for Liquidity Provision in Automated Market Makers. arXiv:2508.08152

-

[12]

(2021).The Adoption of Blockchain-based Decentralized Exchanges

Capponi, A., Jia, R. (2021).The Adoption of Blockchain-based Decentralized Exchanges. arXiv:2103.08842

-

[13]

Cartea, Á., Drissi, F., Monga, M. (2023). Predictable losses of liquidity provision in constant func- tion markets and concentrated liquidity markets.Applied Mathematical Finance30(2), 69–93

2023

-

[14]

Cartea, Á., Drissi, F., Monga, M. (2024). Decentralised finance and automated market making: Predictable loss and optimal liquidity provision.SIAM Journal on Financial Mathematics15(3), 931–959

2024

-

[15]

(2015).Algorithmic and High-Frequency Trading

Cartea, Á., Jaimungal, S., Penalva, J. (2015).Algorithmic and High-Frequency Trading. Cambridge University Press

2015

-

[16]

C., Ingersoll, J

Cox, J. C., Ingersoll, J. E., Ross, S. A. (1985). A theory of the term structure of interest rates. Econometrica53(2), 385–407

1985

-

[17]

Evans, A., Angeris, G., Chitra, T.(2021).Optimalfeesforgeometricmeanmarketmakers.Financial Cryptography and Data Security 2021 Workshops, Springer, 65–79

2021

-

[18]

Fan, Z., Marmolejo-Cossío, F., Moroz, D., Neuder, M., Rao, R., Parkes, D. C. (2023). Strategic liquidity provision in Uniswap v3.5th Conf. on Advances in Financial Technologies (AFT 2023), LIPIcs 282, 25:1–25:22

2023

-

[19]

H., Soner, H

Fleming, W. H., Soner, H. M. (2006).Controlled Markov Processes and Viscosity Solutions, 2nd ed. Springer

2006

-

[20]

(2021).A noteon optimalfees forconstant functionmarketmakers.ACM CCS Workshop on Decentralized Finance and Security (DeFi ’21), 9–14

Fritsch, R. (2021).A noteon optimalfees forconstant functionmarketmakers.ACM CCS Workshop on Decentralized Finance and Security (DeFi ’21), 9–14

2021

-

[21]

(2016).The Financial Mathematics of Market Liquidity

Guéant, O. (2016).The Financial Mathematics of Market Liquidity. Chapman & Hall/CRC

2016

-

[22]

Guéant, O., Lehalle, C.-A., Fernandez-Tapia, J. (2013). Dealing with the inventory risk: a solution to the market making problem.Mathematics and Financial Economics7(4), 477–507. 17

2013

-

[23]

Ho, T., Stoll, H. R. (1981). Optimal dealer pricing under transactions and return uncertainty. Journal of Financial Economics9(1), 47–73

1981

-

[24]

J., Dupuis, P

Kushner, H. J., Dupuis, P. (2001).Numerical Methods for Stochastic Control Problems in Contin- uous Time, 2nd ed. Springer

2001

-

[25]

Merton, R. C. (1969). Lifetime portfolio selection under uncertainty: The continuous-time case. Review of Economics and Statistics51(3), 247–257

1969

-

[26]

Milionis, J., Moallemi, C. C., Roughgarden, T., Zhang, A. L. (2022).Automated Market Making and Loss-Versus-Rebalancing. arXiv:2208.06046. Short version: Quantifying loss in automated market makers,ACM CCS DeFi ’22, 71–74

-

[27]

Milionis, J., Moallemi, C. C., Roughgarden, T. (2024). Automated market making and arbitrage profits in the presence of fees.Financial Cryptography and Data Security (FC 2024), Springer LNCS 14744. arXiv:2305.14604

-

[28]

C., Roughgarden, T

Milionis, J., Moallemi, C. C., Roughgarden, T. (2024). A Myersonian framework for optimal liq- uidity provision in automated market makers.15th Innovations in Theoretical Computer Science (ITCS 2024), LIPIcs 287

2024

-

[29]

(2025).Loss-Versus-Rebalancing under Deterministic and Generalized Block-Times

Nezlobin, A., Tassy, M. (2025).Loss-Versus-Rebalancing under Deterministic and Generalized Block-Times. arXiv:2505.05113

-

[30]

(2009).Continuous-time Stochastic Control and Optimization with Financial Applica- tions

Pham, H. (2009).Continuous-time Stochastic Control and Optimization with Financial Applica- tions. Springer

2009

-

[31]

Sirignano, J., Spiliopoulos, K. (2018). DGM: A deep learning algorithm for solving partial differen- tial equations.Journal of Computational Physics375, 1339–1364. 18

2018

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.