When Staking Rewards Compound: Measuring the Impact of Ethereum's Pectra Upgrade

Pith reviewed 2026-06-26 07:27 UTC · model grok-4.3

The pith

Compounding staking rewards after Ethereum's Pectra upgrade lifts consensus-layer APR by about 5% for small balances but under 1% for large providers.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

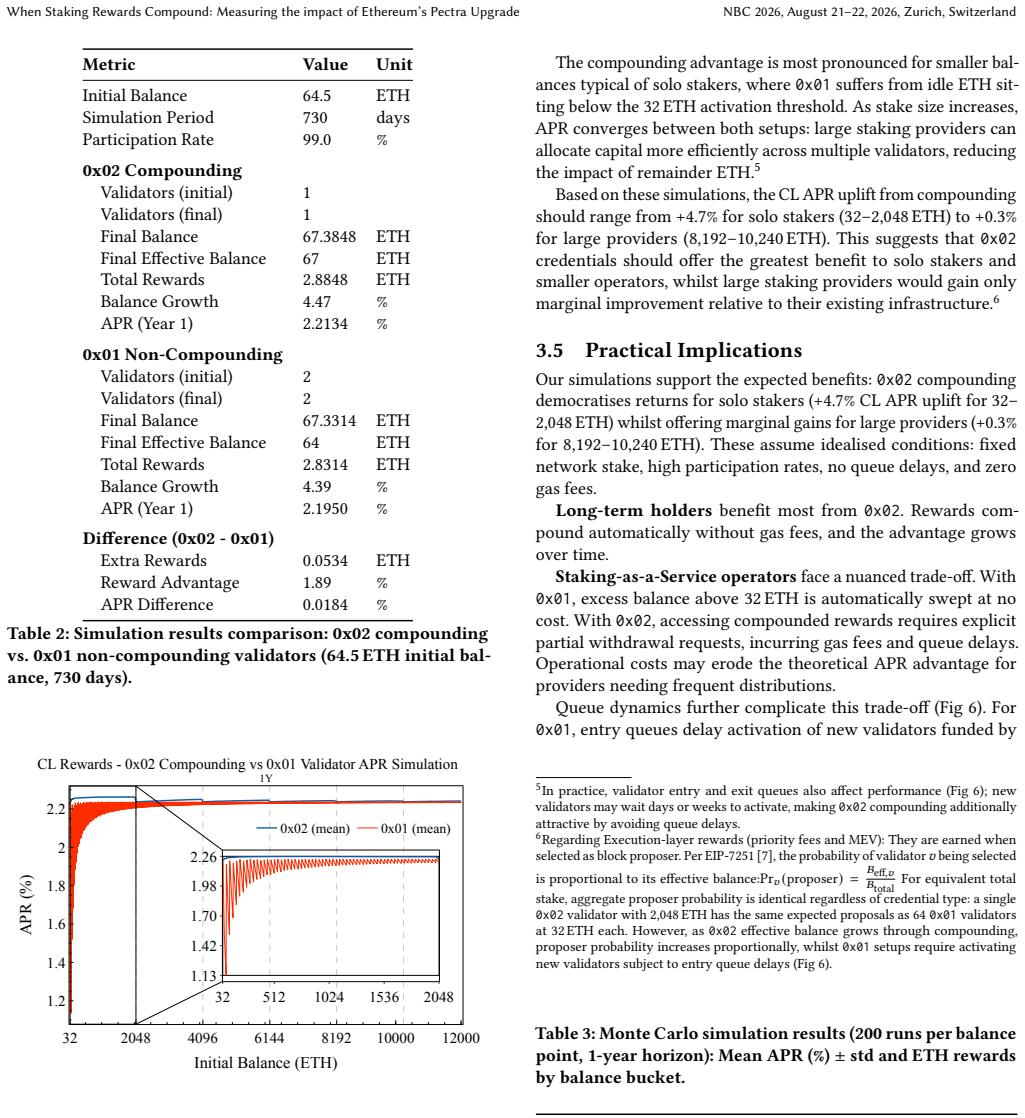

Through simulation, compounding provides roughly +5% relative consensus-layer APR uplift for small balances, diminishing to under 1% for large staking providers. Empirical analysis of all active beacon chain validators shows 0x02 validators achieving modestly higher median CL APR.

What carries the argument

Simulation of consensus-layer reward accrual under compounding rules, paired with direct measurement of median APR across every active beacon chain validator split by withdrawal credential type.

If this is right

- Small-balance stakers receive the largest relative reward increase from automatic compounding.

- Large staking providers see little APR improvement, lowering their incentive to consolidate or migrate.

- Solo stakers adopt the new format at higher rates than providers despite facing greater operational costs.

- Network-wide efficiency gains from fewer validators will arrive slowly unless reward accessibility improves.

Where Pith is reading between the lines

- The size-dependent benefit could tilt preference toward solo staking over pooled services if the modeled uplift holds.

- Whether larger balances also change execution-layer reward opportunities remains untested in the current analysis.

- Tracking validator consolidation rates after the upgrade would show whether providers treat the change as a cost-saving opportunity.

Load-bearing premise

The simulation model accurately captures real-world consensus-layer dynamics and validator behavior without unmodeled factors such as network latency or slashing events that could alter the reported APR differences.

What would settle it

Post-Pectra measurement of actual consensus-layer APR for matched groups of 0x02 versus legacy validators, stratified by balance size and observed over multiple epochs.

Figures

read the original abstract

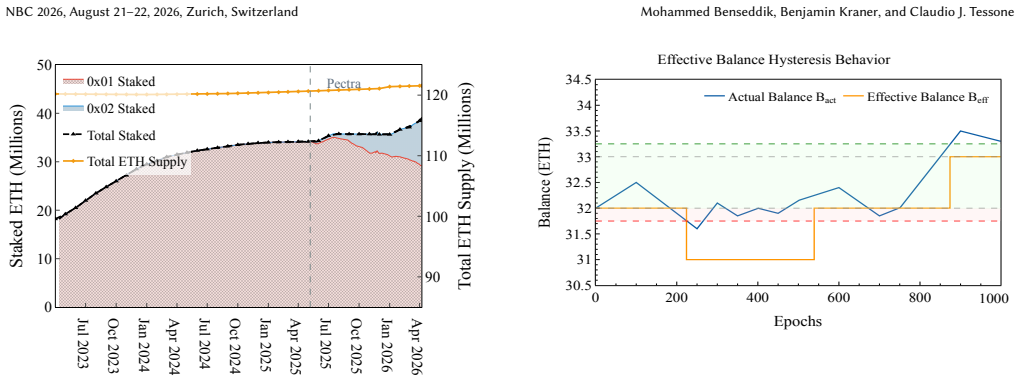

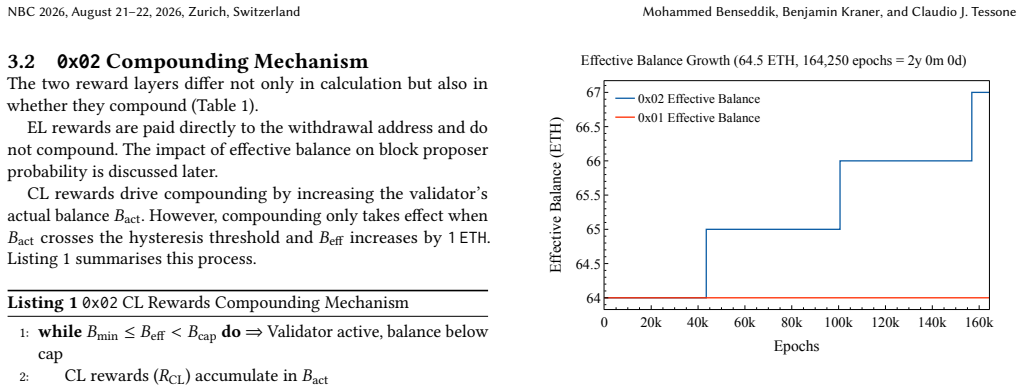

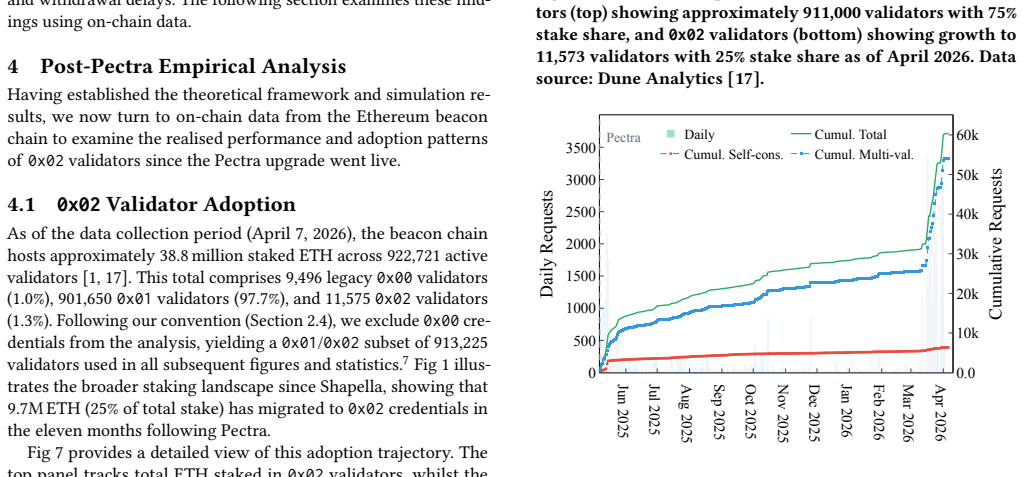

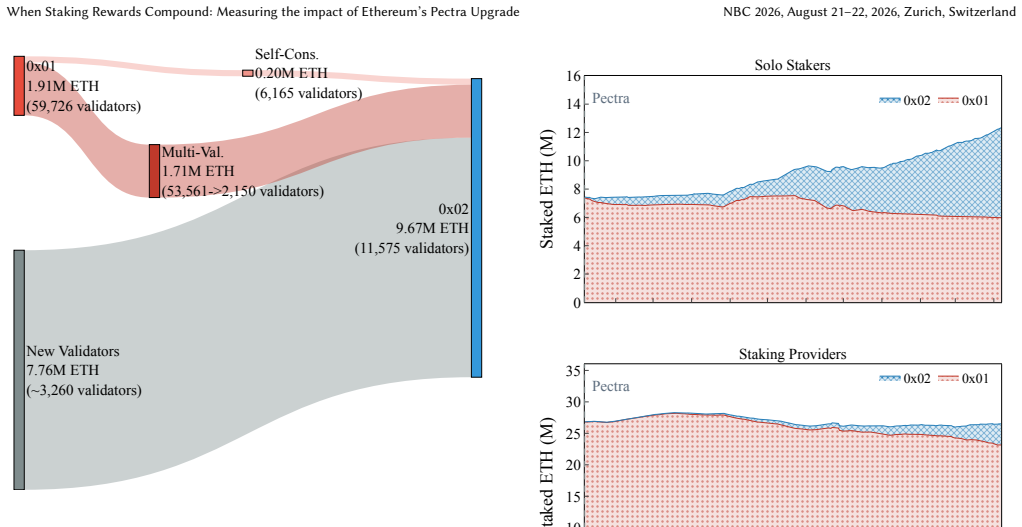

Ethereum's beacon chain hosts over 920,000 active validators, a number inflated by the legacy 32 ETH stake cap. The Pectra upgrade (May 2025) addresses this by introducing 0x02 compounding validators, raising the maximum stake per validator from 32 to 2,048 ETH and enabling automatic reward reinvestment. This paper examines how compounding affects consensus-layer rewards, whether higher balances provide execution-layer advantages, and whether the APR uplift justifies migration for different staker types. We analyse adoption patterns across solo stakers and staking providers, investigate the role of consolidation (merging multiple 32 ETH validators into one) in early migration, and identify barriers slowing the transition. Through simulation, we find that compounding provides roughly +5% relative consensus-layer APR uplift for small balances, diminishing to under 1% for large staking providers. Empirical analysis of all active beacon chain validators shows 0x02 validators achieving modestly higher median CL APR. Solo stakers show higher relative adoption but face operational barriers, whilst providers cite infrastructure costs and protocol constraints. The results suggest that without improved reward accessibility and stronger economic incentives, 0x02 migration will remain gradual despite its network efficiency benefits.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper examines Ethereum's Pectra upgrade introducing 0x02 compounding validators (max stake 2048 ETH with automatic reward reinvestment). It claims via simulation that compounding yields roughly +5% relative consensus-layer APR uplift for small balances, diminishing to under 1% for large providers; empirical analysis of all active beacon-chain validators finds modestly higher median CL APR for 0x02 validators. It further analyzes adoption patterns, the role of consolidation, barriers for solo stakers vs. providers, and concludes migration will remain gradual absent stronger incentives.

Significance. If the simulation is fully specified and validated and the empirical comparison includes appropriate controls, the quantitative APR estimates would supply concrete guidance on economic incentives for validator consolidation, informing both individual stakers and protocol-level decisions on network efficiency. The adoption and barrier analysis adds practical context on transition frictions.

major comments (2)

- [Simulation results] Simulation methodology: the reward model, effective-balance update rule, epoch timing, parameterization choices, and any validation against historical beacon-chain data are not disclosed. Without these, the central +5% relative uplift claim for small balances (and its diminution for large providers) cannot be reproduced or distinguished from auxiliary modeling assumptions.

- [Empirical analysis] Empirical median comparison: the reported higher median CL APR for 0x02 validators is presented without controls for stake size, client, geography, or other confounders, so the modest difference cannot be attributed to compounding rather than selection effects.

minor comments (2)

- [Abstract] Abstract and results sections omit error bars, empirical sample sizes, and simulation validation details.

- [Simulation assumptions] The simulation assumptions paragraph does not discuss potential unmodeled factors such as network latency or slashing events.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback on our manuscript. We address each major comment point by point below and commit to revisions that directly respond to the concerns.

read point-by-point responses

-

Referee: [Simulation results] Simulation methodology: the reward model, effective-balance update rule, epoch timing, parameterization choices, and any validation against historical beacon-chain data are not disclosed. Without these, the central +5% relative uplift claim for small balances (and its diminution for large providers) cannot be reproduced or distinguished from auxiliary modeling assumptions.

Authors: We agree that the simulation methodology was insufficiently specified in the submitted version. In the revision we will insert a dedicated methods subsection that fully documents the reward accrual model (including base and sync rewards), the effective balance update rule at each epoch, epoch timing and slot assumptions, all parameter values (e.g., reward curves, balance caps), and any calibration or validation steps performed against historical beacon-chain data. This addition will make the reported +5% relative uplift and its size-dependent decay fully reproducible. revision: yes

-

Referee: [Empirical analysis] Empirical median comparison: the reported higher median CL APR for 0x02 validators is presented without controls for stake size, client, geography, or other confounders, so the modest difference cannot be attributed to compounding rather than selection effects.

Authors: We accept that the current median comparison does not isolate the compounding effect from selection. We will revise the empirical section to include a controlled analysis—either a linear regression of CL APR on validator type with covariates for effective balance, client software, and available geographic or operator metadata, or a matched-sample comparison that balances on stake size. The revised text will clearly state the limitations of the uncontrolled median and present the controlled results. revision: yes

Circularity Check

No circularity: claims rest on forward simulation and direct beacon-chain measurement

full rationale

The paper reports APR uplift figures exclusively from forward simulation of compounding mechanics and from direct empirical measurement of all active beacon-chain validators. No equations, fitted parameters, or self-citations are presented that would reduce the reported +5% uplift (or the 0x02 median comparison) to a quantity defined by the same data or by prior author work. The central quantitative claims therefore remain independent of the inputs they are derived from.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

beaconcha.in. 2025. Ethereum Beacon Chain Explorer. Online. https://beaconcha. in/ Accessed: Jan. 12, 2026

2025

-

[2]

Tim Beiko et al . 2023. The Eth2 Book — Economics: Base Reward. Online. https://eth2book.info/capella/part3/economics/. Accessed: Jan. 12, 2026

2023

-

[3]

Mohammed Benseddik, Benjamin Kraner, and Claudio J. Tessone. 2026. Ethereum Pectra Paper – Replication Package. https://github.com/benseddikmo/eth_pectra_ paper_replication_package. Data, figures, and analysis code

2026

-

[4]

Consensys. 2025. The Pectra Upgrade and the Evolution of L2s. On- line. https://consensys.io/ethereum-pectra-upgrade/linea-and-how-pectra- impacts-ethereums-scalability. Accessed: Jan. 12, 2026

2025

-

[5]

Entropy Advisors. 2025. Ethereum Pectra Upgrade Dashboard. Dune Analyt- ics. Available: https://dune.com/entropy_advisors/ethereum-pectra-upgrade. Accessed: Jan. 13, 2026

2025

-

[6]

Ethereum Foundation. 2023. ETH Withdrawals FAQ. Online. https://notes. ethereum.org/@launchpad/withdrawals-faq. Accessed: Jan. 11, 2026

2023

-

[7]

Ethereum Foundation. 2024. EIP-7251: Increase Max Effective Balance. Ethereum Improvement Proposal. Available: https://eips.ethereum.org/EIPS/eip-7251. Accessed: Jan. 12, 2026

2024

-

[8]

Ethereum Foundation. 2024. Ethereum Roadmap — Pectra Upgrade. Online. https://ethereum.org/en/roadmap/pectra/ Accessed: Jan. 12, 2026

2024

-

[9]

Ethereum Foundation. 2025. All Core Devs - Consensus (ACDC) Call 152: Discussion on Validator Consolidation Challenges. YouTube. Available: https://www.youtube.com/watch?v=1IA-NZa4VZ8. Accessed: Jan. 12, 2026

2025

-

[10]

Ethereum Foundation. 2025. EIP-8068: Neutral Effective Balance Design. Ethereum Improvement Proposal (Draft). Available: https://eips.ethereum.org/ EIPS/eip-8068. Accessed: Jan. 12, 2026

2025

-

[11]

Ethereum Foundation. 2025. Ethereum Consensus Specifications: Electra Bea- con Chain. Online. https://ethereum.github.io/consensus-specs/specs/electra/ beacon-chain/#new-process_pending_consolidations. Accessed: Jan. 11, 2026

2025

-

[12]

Ethereum Foundation. 2025. Timeline of All Ethereum Forks (2014 to Present). Online. https://ethereum.org/ethereum-forks/. Accessed: Jan. 06, 2026

2025

-

[13]

Ethereum Foundation Blog. 2025. Pectra Mainnet Announcement. Online. Avail- able: https://blog.ethereum.org/2025/04/23/pectra-mainnet. Accessed: Jan. 12, 2026

2025

-

[14]

Ethereum Research. 2023. Increase the Max Effective Balance: A Modest Proposal. Online. https://ethresear.ch/t/increase-the-max-effective-balance-a-modest- proposal/15801. Accessed: Jan. 12, 2026

2023

-

[15]

Ittay Eyal and Emin Gün Sirer. 2018. Majority is not enough: Bitcoin mining is vulnerable.Commun. ACM61, 7 (2018), 95–102

2018

-

[16]

hanniabu.eth. 2025. Ethereum Validator Queue. Online. https://www. validatorqueue.com/. Accessed: Jan. 12, 2026

2025

-

[17]

hildobby. 2025. Ethereum Staking Dashboard. Online. Available: https://dune. com/hildobby/eth2-staking. Accessed: Dec. 18, 2025

2025

-

[18]

Urban J Jermann. 2023. A macro finance model for proof-of-stake ethereum. A vailable at SSRN 4335835(2023)

2023

-

[19]

Benjamin Kraner, Sheng-Nan Li, Andreia Sofia Teixeira, and Claudio J. Tessone

-

[20]

InIEEE International Conference on Blockchain, Blockchain 2022, Espoo, Finland, August 22-25, 2022

Agent-based Modelling of Bitcoin Consensus without Block Rewards. InIEEE International Conference on Blockchain, Blockchain 2022, Espoo, Finland, August 22-25, 2022. IEEE, IEEE, 29–36. doi:10.1109/Blockchain55522.2022.00015

-

[21]

Burak Öz, Benjamin Kraner, Nicoló Vallarano, Bingle Stegmann Kruger, Florian Matthes, and Claudio Juan Tessone. 2023. Time Moves Faster When There is Nothing You Anticipate: The Role of Time in MEV Rewards. InProceedings of the 2023 Workshop on Decentralized Finance and Security, DeFi 2023, Copenhagen, Denmark, 30 November 2023, Kaihua Qin and Fan Zhang (...

-

[22]

Lucas Saldanha. 2024. EIP-7804: Withdrawal Credential Update Request. Ethereum Improvement Proposal (Draft). https://eips.ethereum.org/EIPS/eip- 7804 Accessed: Jan. 11, 2026

2024

-

[23]

Caspar Schwarz-Schilling, Sheng-Nan Li, and Claudio J Tessone. 2022. Stochastic modelling of selfish mining in proof-of-work protocols.Journal of Cybersecurity and Privacy2, 2 (2022), 292–310

2022

-

[24]

Caspar Schwarz-Schilling, Joachim Neu, Barnabé Monnot, Aditya Asgaonkar, Ertem Nusret Tas, and David Tse. 2022. Three attacks on proof-of-stake ethereum. InInternational Conference on Financial Cryptography and Data Security. Springer, 560–576

2022

- [25]

-

[26]

Takaya Sugino, Benjamin Kraner, James Angel, Shin’ichiro Matsuo, and Rohil Paruchuri. 2025. An Analysis of Financial Stability Risk Propagation Through When Staking Rewards Compound: Measuring the impact of Ethereum’s Pectra Upgrade NBC 2026, August 21–22, 2026, Zurich, Switzerland Leveraged Staking Activities. InInternational Conference on Financial Cryp...

2025

-

[27]

The Defiant. 2025. Ethereum Validator Exit Queue Spikes 150% as Kiln Unstakes All Its ETH. Online. Available: https://thedefiant.io/news/hacks/ethereum- validator-exit-queue-spikes-150-as-kiln-unstakes-all-its-eth. Accessed: Jan. 12, 2026

2025

-

[28]

Justin Traglia. 2024. Ethereum Consensus Specifications: Phase 0 — Beacon Chain. Online. Available: https://github.com/ethereum/consensus-specs. Accessed: Jan. 12, 2026

2024

-

[29]

Tao Yan, Shengnan Li, Benjamin Kraner, Luyao Zhang, and Claudio J Tessone

-

[30]

A Data Engineering Framework for Ethereum Beacon Chain Rewards: From Data Collection to Decentralization Metrics.Scientific Data12, 1 (2025), 519

2025

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.