Quantum Derivative Pricing for SPDEs via BDSDE Representation

Pith reviewed 2026-07-01 05:53 UTC · model grok-4.3

The pith

Quantum-accelerated multilevel Monte Carlo methods reduce sampling complexity for SPDE derivative pricing and Greeks from quadratic to linear in the error tolerance.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

By representing SPDE derivative pricing problems through their BDSDE equivalents and applying conditional and nested QA-MLMC to the resulting expectations, together with Forward-Backward Taylor discretization that achieves global strong-error order one, the sampling complexity of classical Monte Carlo improves from ilde O(\epsilon^{-2}) to ilde O(\epsilon^{-1}) for both prices and Greeks within additive error \epsilon.

What carries the argument

Conditional and nested quantum-accelerated multilevel Monte Carlo (QA-MLMC) estimators applied to BDSDE representations, supported by Forward-Backward Taylor discretization schemes that deliver global strong-error order-one convergence for pricing and Greek estimators.

If this is right

- Quantum estimators exist for first-order and second-order Greeks using both likelihood-ratio and Malliavin-weight representations.

- The same complexity improvement applies to Heston-type stochastic-volatility models.

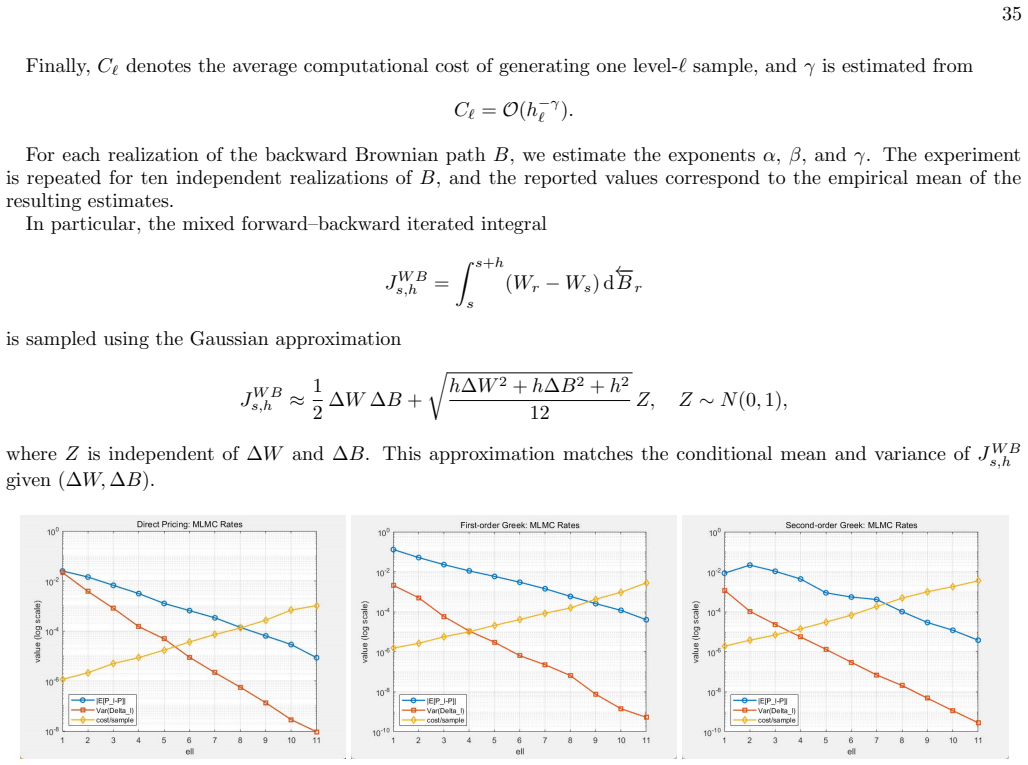

- Numerical experiments confirm that the discretization schemes attain the convergence orders needed for the full quadratic quantum speedup.

- The framework supplies both pricing and sensitivity analysis under a single set of quantum-accelerated estimators.

Where Pith is reading between the lines

- The same BDSDE-plus-QA-MLMC structure could be tested on other high-dimensional path-dependent claims whose classical Monte Carlo cost is dominated by nested expectations.

- If the oracle construction cost scales favorably, the linear sampling regime might combine with quantum linear-system solvers to produce end-to-end quantum pipelines for entire pricing workflows.

- The order-one discretization property may extend the approach to Greeks of even higher order without losing the quadratic quantum advantage.

Load-bearing premise

Efficient quantum circuits or oracles can be built for the conditional and nested expectations that appear in the BDSDE representations, and the Forward-Backward Taylor schemes really attain the stated order-one strong convergence.

What would settle it

A concrete counter-example or numerical test in which the Forward-Backward Taylor discretization fails to achieve global strong-error order one for the price or Greek estimators, or in which no quantum circuit of the assumed size exists for the required conditional expectations.

Figures

read the original abstract

We study quantum speedups of derivative pricing for stochastic partial differential equation (SPDE) models through their backward doubly stochastic differential equation (BDSDE) representations. We develop conditional and nested quantum-accelerated multilevel Monte Carlo (QA-MLMC) methods for estimating the resulting conditional and nested expectations, improving the sampling complexity of classical Monte Carlo methods from $\widetilde{O}(\epsilon^{-2})$ to $\widetilde{O}(\epsilon^{-1})$ within additive error $\epsilon$. We apply the framework to derivative pricing and sensitivity analysis, providing quantum-accelerated estimators for prices as well as first-order and second-order Greeks, likelihood-ratio and Malliavin-weight representations for Greeks, and Heston-type stochastic-volatility models. To enable efficient multilevel coupling, we construct a family of Forward--Backward Taylor discretization schemes for the stochastic integrals arising in the BDSDE representations and establish global strong-error order one convergence for pricing and Greek estimators. Numerical experiments showcase our schemes for first-order and second-order Greeks can reach the required orders for the full quadratic quantum speedups.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops BDSDE representations for derivative pricing and Greek computation in SPDE models, then introduces conditional and nested QA-MLMC estimators that reduce classical Monte Carlo sampling complexity from ilde{O}(\epsilon^{-2}) to ilde{O}(\epsilon^{-1}). It constructs Forward-Backward Taylor discretization schemes claimed to achieve global strong-error order one for both pricing and Greek estimators, applies the framework to Heston-type models and likelihood-ratio/Malliavin representations, and reports numerical experiments confirming the required convergence orders for quadratic quantum speedups.

Significance. If the end-to-end complexity claims hold, the work would extend quantum Monte Carlo advantages to SPDE-based pricing and sensitivity analysis, with the order-one convergence of the Taylor schemes and numerical validation for first- and second-order Greeks constituting concrete strengths. The explicit treatment of nested expectations and stochastic-volatility extensions adds technical value.

major comments (2)

- [Complexity analysis] § on complexity analysis (near the QA-MLMC definition): the sampling-complexity reduction from ilde{O}(\epsilon^{-2}) to ilde{O}(\epsilon^{-1}) is derived under the assumption that each quantum oracle for the conditional/nested BDSDE expectations has gate cost polylog(1/\epsilon) independent of spatial dimension. No explicit gate-complexity bound is supplied for the oracles arising from spatial truncation of the SPDE (finite-element or spectral) to a high-dimensional SDE; this assumption is load-bearing for whether the quadratic advantage survives once oracle construction cost is counted.

- [Discretization and convergence] § on Forward-Backward Taylor schemes and Theorem establishing order-one convergence: while global strong error O(h) is proved for the discretization, the multilevel coupling argument for the nested QA-MLMC estimators is not shown to preserve the same order when the inner conditional expectations are replaced by quantum oracles; this step is required to justify that the full estimator attains the stated ilde{O}(\epsilon^{-1}) complexity.

minor comments (2)

- [Preliminaries] Notation for the BDSDE coefficients and the precise definition of the nested expectation operators could be collected in a single preliminary section to improve readability.

- [Numerical experiments] Numerical experiments report convergence orders for Greeks but do not tabulate the effective dimension of the spatial discretization or the observed gate counts; adding these would strengthen the validation.

Simulated Author's Rebuttal

We thank the referee for their careful reading and constructive comments on the manuscript. We address each major comment below with honest responses and indicate planned revisions where appropriate.

read point-by-point responses

-

Referee: [Complexity analysis] § on complexity analysis (near the QA-MLMC definition): the sampling-complexity reduction from ilde{O}(\epsilon^{-2}) to ilde{O}(\epsilon^{-1}) is derived under the assumption that each quantum oracle for the conditional/nested BDSDE expectations has gate cost polylog(1/\epsilon) independent of spatial dimension. No explicit gate-complexity bound is supplied for the oracles arising from spatial truncation of the SPDE (finite-element or spectral) to a high-dimensional SDE; this assumption is load-bearing for whether the quadratic advantage survives once oracle construction cost is counted.

Authors: We acknowledge that the end-to-end complexity claim relies on the polylog gate cost assumption for the quantum oracles, and the manuscript does not supply an explicit bound accounting for the cost of spatial truncation to a high-dimensional SDE. The analysis in the paper focuses on sampling complexity under standard quantum oracle assumptions common in the QA-MLMC literature. For a fixed spatial discretization (constant number of modes or elements), the effective dimension is independent of \epsilon and the oracle costs remain polylog(1/\epsilon) by existing quantum SDE simulation results under Lipschitz conditions. We agree this point merits clarification and will add a remark in the complexity section of the revised manuscript noting the fixed-dimension assumption and that full space-time discretization costs are beyond the current scope. This constitutes a partial revision. revision: partial

-

Referee: [Discretization and convergence] § on Forward-Backward Taylor schemes and Theorem establishing order-one convergence: while global strong error O(h) is proved for the discretization, the multilevel coupling argument for the nested QA-MLMC estimators is not shown to preserve the same order when the inner conditional expectations are replaced by quantum oracles; this step is required to justify that the full estimator attains the stated ilde{O}(\epsilon^{-1}) complexity.

Authors: The referee is correct that the order-one strong convergence is established for the classical Forward-Backward Taylor schemes, and the manuscript does not explicitly verify that the multilevel coupling for the nested QA-MLMC preserves this order once inner expectations are approximated by quantum oracles. The construction ensures oracle accuracy is set to not exceed the discretization error at each level, allowing the variance decay and coupling to carry over. However, we recognize an explicit lemma bridging the classical coupling to the quantum-oracle case is missing. We will add a short argument in the revised manuscript (near the QA-MLMC definition and the convergence theorem) showing that the oracle error bounds suffice to maintain the required multilevel properties and thus the ilde{O}(\epsilon^{-1}) complexity. This will be incorporated as a revision. revision: yes

Circularity Check

No significant circularity; central claims rest on external quantum-oracle assumptions

full rationale

The paper's core contribution is the application of QA-MLMC to BDSDE representations of SPDE pricing problems, together with Forward-Backward Taylor schemes whose strong order-1 convergence is proved. No equation in the provided abstract or description reduces a claimed prediction to a fitted input by construction, nor does any load-bearing step collapse to a self-citation whose content is itself unverified. The stated complexity improvement from ilde{O}(ε^{-2}) to ilde{O}(ε^{-1}) is conditional on the separate assumption that oracles for the conditional/nested expectations can be realized with polylog cost; that assumption is flagged explicitly as the weakest link and is not derived inside the paper. Hence the derivation chain remains non-circular at the level of the enumerated patterns.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Black and M

F. Black and M. Scholes, The pricing of options and corporate liabilities, Journal of Political Economy81, 637 (1973)

1973

-

[2]

S. L. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, The Review of Financial Studies6, 327 (1993)

1993

-

[3]

Fouque, G

J.-P. Fouque, G. Papanicolaou, and R. Sircar,Derivatives in Financial Markets with Stochastic Volatility(Cambridge University Press, Cambridge, 2000)

2000

-

[4]

Bergomi,Stochastic Volatility Modeling, Financial Mathematics Series (Chapman and Hall/CRC, 2015)

L. Bergomi,Stochastic Volatility Modeling, Financial Mathematics Series (Chapman and Hall/CRC, 2015)

2015

-

[5]

Heath, R

D. Heath, R. Jarrow, and A. Morton, Bond pricing and the term structure of interest rates: A new methodology, Econo- metrica60, 77 (1992)

1992

-

[6]

The Dynamics of the Forward Interest Rate Curve with Stochastic String Shocks

P. Santa-Clara and D. Sornette, The dynamics of the forward interest rate curve with stochastic string shocks, The Review of Financial Studies14, 149 (2001), arXiv:cond-mat/9801321

work page internal anchor Pith review Pith/arXiv arXiv 2001

-

[7]

Modeling interest rate dynamics: an infinite-dimensional approach

R. Cont, Modeling term structure dynamics: an infinite dimensional approach, International Journal of theoretical and applied finance8, 357 (2005), arXiv:cond-mat/9902018

work page internal anchor Pith review Pith/arXiv arXiv 2005

-

[8]

F. E. Benth, J. S. Benth, and S. Koekebakker,Stochastic modelling of electricity and related markets, Vol. 11 (World Scientific, 2008)

2008

-

[9]

J. C. Hull and S. Basu,Options, futures, and other derivatives(Pearson Education India, 2016)

2016

-

[10]

Printems, On the discretization in time of parabolic stochastic partial differential equations, ESAIM: Mathematical Modelling and Numerical Analysis35, 1055 (2001)

J. Printems, On the discretization in time of parabolic stochastic partial differential equations, ESAIM: Mathematical Modelling and Numerical Analysis35, 1055 (2001)

2001

-

[11]

Larsson and V

S. Larsson and V. Thom´ ee,Partial differential equations with numerical methods(Springer, 2003)

2003

-

[12]

Gy¨ ongy, Lattice approximations for stochastic quasi-linear parabolic partial differential equations driven by space-time white noise II, Potential Analysis11, 1 (1999)

I. Gy¨ ongy, Lattice approximations for stochastic quasi-linear parabolic partial differential equations driven by space-time white noise II, Potential Analysis11, 1 (1999)

1999

-

[13]

G. J. Lord and J. Rougemont, A numerical scheme for stochastic pdes with gevrey regularity, IMA journal of numerical analysis24, 587 (2004)

2004

-

[14]

S. C. Brenner and L. R. Scott,The mathematical theory of finite element methods(Springer, 2008)

2008

-

[15]

Bungartz and M

H.-J. Bungartz and M. Griebel, Sparse grids, Acta Numerica13, 147 (2004)

2004

-

[16]

I. Hout, S. Foulon,et al., ADI finite difference schemes for option pricing in the heston model with correlation., International Journal of Numerical Analysis & Modeling7(2010), arXiv:0811.3427v1

work page internal anchor Pith review Pith/arXiv arXiv 2010

-

[17]

Pardoux and S

E. Pardoux and S. Peng, Adapted solution of a backward stochastic differential equation, Systems & control letters14, 55 (1990)

1990

-

[18]

Pardoux and S

E. Pardoux and S. Peng, Backward stochastic differential equations and quasilinear parabolic partial differential equations, inStochastic Partial Differential Equations and Their Applications: Proceedings of IFIP WG 7/1 International Conference University of North Carolina at Charlotte, NC June 6–8, 1991(Springer, 2005) pp. 200–217

1991

-

[19]

Kobylanski, Backward stochastic differential equations and partial differential equations with quadratic growth, Annals of probability , 558 (2000)

M. Kobylanski, Backward stochastic differential equations and partial differential equations with quadratic growth, Annals of probability , 558 (2000)

2000

-

[20]

S. Peng, A generalized dynamic programming principle and Hamilton-Jacobi-Bellman equation, Stochastics: An Interna- tional Journal of Probability and Stochastic Processes38, 119 (1992)

1992

-

[21]

Yong and X

J. Yong and X. Y. Zhou,Stochastic controls: Hamiltonian systems and HJB equations, Vol. 43 (Springer Science & Business Media, 1999)

1999

-

[22]

El Karoui, S

N. El Karoui, S. Peng, and M. C. Quenez, Backward stochastic differential equations in finance, Mathematical finance7, 1 (1997)

1997

-

[23]

Peng, Backward SDE and related g-expectation, Pitman research notes in mathematics series , 141 (1997)

S. Peng, Backward SDE and related g-expectation, Pitman research notes in mathematics series , 141 (1997)

1997

-

[24]

S. Peng, Nonlinear expectations, nonlinear evaluations and risk measures, inStochastic Methods in Finance: Lectures given at the CIME-EMS Summer School held in Bressanone/Brixen, Italy, July 6-12, 2003(Springer, 2004) pp. 165–253. 38

2003

-

[25]

Pardoux and S

´E. Pardoux and S. Peng, Backward doubly stochastic differential equations and systems of quasilinear SPDEs, Probability theory and related fields98, 209 (1994)

1994

-

[26]

Zhang, A numerical scheme for BSDEs, The annals of applied probability14, 459 (2004)

J. Zhang, A numerical scheme for BSDEs, The annals of applied probability14, 459 (2004)

2004

-

[27]

Bouchard and N

B. Bouchard and N. Touzi, Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations, Stochastic Processes and their applications111, 175 (2004)

2004

-

[28]

A regression-based Monte Carlo method to solve backward stochastic differential equations

E. Gobet, J.-P. Lemor, and X. Warin, A regression-based Monte Carlo method to solve backward stochastic differential equations, The Annals of Applied Probability15, 2172 (2005), arXiv:math/0508491

work page internal anchor Pith review Pith/arXiv arXiv 2005

-

[29]

J. Han, A. Jentzen,et al., Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations, Communications in mathematics and statistics5, 349 (2017), arXiv:1706.04702

work page internal anchor Pith review Pith/arXiv arXiv 2017

-

[30]

J. Han, A. Jentzen, and W. E, Solving high-dimensional partial differential equations using deep learning, Proceedings of the National Academy of Sciences115, 8505 (2018), arXiv:1707.02568

work page internal anchor Pith review Pith/arXiv arXiv 2018

-

[31]

C. Beck, W. E, and A. Jentzen, Machine learning approximation algorithms for high-dimensional fully nonlinear partial differential equations and second-order backward stochastic differential equations, Journal of Nonlinear Science29, 1563 (2019), arXiv:1709.05963

work page internal anchor Pith review Pith/arXiv arXiv 2019

-

[32]

A Numerical scheme for backward doubly stochastic differential equations

A. Aman, A numerical scheme for backward doubly stochastic differential equations, Bernoulli19, 93 (2013), arXiv:1011.6170

work page internal anchor Pith review Pith/arXiv arXiv 2013

-

[33]

Bachouch, E

A. Bachouch, E. Gobet, and A. Matoussi, Empirical regression method for backward doubly stochastic differential equa- tions, SIAM/ASA Journal on Uncertainty Quantification4, 358 (2016)

2016

-

[34]

F. Bao, Y. Cao, A. Meir, and W. Zhao, A first order scheme for backward doubly stochastic differential equations, SIAM/ASA Journal on Uncertainty Quantification4, 413 (2016)

2016

-

[35]

M. B. Giles, Multilevel Monte Carlo path simulation, Operations research56, 607 (2008)

2008

-

[36]

M. B. Giles, Multilevel Monte Carlo for basket options, inProceedings of the 2009 Winter Simulation Conference (WSC) (IEEE, 2009) pp. 1283–1290

2009

-

[37]

Burgos and M

S. Burgos and M. B. Giles, Computing Greeks using multilevel path simulation, inMonte Carlo and Quasi-Monte Carlo Methods 2010(Springer, 2012) pp. 281–296

2010

-

[38]

M. B. Giles and L. Szpruch, Multilevel Monte Carlo methods for applications in finance, High-Performance Computing in Finance , 197 (2018), arXiv:1212.1377

work page internal anchor Pith review Pith/arXiv arXiv 2018

-

[39]

M. B. Giles and A.-L. Haji-Ali, Multilevel nested simulation for efficient risk estimation, SIAM/ASA Journal on Uncertainty Quantification7, 497 (2019), arXiv:1802.05016

work page internal anchor Pith review Pith/arXiv arXiv 2019

-

[40]

Barth, A

A. Barth, A. Lang, and C. Schwab, Multilevel Monte Carlo method for parabolic stochastic partial differential equations, BIT Numerical Mathematics53, 3 (2013)

2013

-

[41]

Iliev, J

O. Iliev, J. Mohring, and N. Shegunov, Renormalization based MLMC method for scalar elliptic SPDE, inInternational Conference on Large-Scale Scientific Computing(Springer, 2017) pp. 295–303

2017

- [42]

-

[43]

M. B. Giles and C. Reisinger, Stochastic finite differences and multilevel Monte Carlo for a class of SPDEs in finance, SIAM journal on financial mathematics3, 572 (2012), arXiv:1204.1442

work page internal anchor Pith review Pith/arXiv arXiv 2012

-

[44]

G. Brassard, P. Hoyer, M. Mosca, and A. Tapp, Quantum amplitude amplification and estimation, arXiv preprint quant- ph/0005055 (2000)

-

[45]

S. Heinrich, Quantum summation with an application to integration, Journal of Complexity18, 1 (2002), arXiv:quant- ph/0105116

-

[46]

Quantum speedup of Monte Carlo methods

A. Montanaro, Quantum speedup of Monte Carlo methods, Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences471, 20150301 (2015), arXiv:1504.06987

work page internal anchor Pith review Pith/arXiv arXiv 2015

-

[47]

R. Kothari and R. O’Donnell, Mean estimation when you have the source code; or, quantum Monte Carlo methods, in Proceedings of the 2023 Annual ACM-SIAM Symposium on Discrete Algorithms (SODA)(SIAM, 2023) pp. 1186–1215, arXiv:2208.07544

- [48]

-

[49]

J. Blanchet, M. Szegedy, and G. Wang, Quadratic speed-up in infinite variance quantum Monte Carlo, arXiv preprint arXiv:2401.07497 (2024)

-

[50]

J. Blanchet, Y. Hamoudi, M. Szegedy, and G. Wang, Quantum speedup of non-linear Monte Carlo problems, Advances in Neural Information Processing Systems38, 18736 (2026), arXiv:2502.05094

- [51]

-

[52]

X. Li and J.-P. Liu, Quantum algorithms for Gibbs expectation of non-log-concave and heavy-tailed distributions, arXiv preprint arXiv:2604.00656 (2026)

-

[53]

Quantum computational finance: Monte Carlo pricing of financial derivatives

P. Rebentrost, B. Gupt, and T. R. Bromley, Quantum computational finance: Monte Carlo pricing of financial derivatives, Physical Review A98, 022321 (2018), arXiv:1805.00109

work page internal anchor Pith review Pith/arXiv arXiv 2018

-

[54]

N. Stamatopoulos, D. J. Egger, Y. Sun, C. Zoufal, R. Iten, N. Shen, and S. Woerner, Option pricing using quantum computers, Quantum4, 291 (2020), arXiv:1905.02666

- [55]

-

[56]

N. Guseynov, N. Liu, C. S. Pun, and T. Vaidya, End-to-end PDE-based quantum algorithms for multi-asset option pricing 39 under local and stochastic volatility, arXiv preprint arXiv:2605.26610 (2026)

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[57]

Fujita, K

M. Fujita, K. Miyamoto, and J. Sekine, Application of quantum Monte Carlo integration to Markovian backward stochastic differential equations, JSIAM Letters16, 105 (2024)

2024

- [58]

-

[59]

S. Bravyi, R. Manson-Sawko, M. Zayats, and S. Zhuk, Quantum simulation of a noisy classical nonlinear dynamics, arXiv preprint arXiv:2507.06198 (2025)

-

[60]

S. Yang and J.-P. Liu, Circuit-efficient randomized quantum simulation of non-unitary dynamics with observable-driven and symmetry-aware designs, arXiv preprint arXiv:2509.08030 (2025)

- [61]

-

[62]

Quantum algorithms for stochastic nonlinear differential equations

S. Bravyi, A. Byrne, M. Zayats, and S. Zhuk, Quantum algorithms for stochastic nonlinear differential equations, arXiv preprint arXiv:2606.08349 (2026)

work page internal anchor Pith review Pith/arXiv arXiv 2026

- [63]

-

[64]

Bally and A

V. Bally and A. Matoussi, Weak solutions for SPDEs and backward doubly stochastic differential equations, Journal of Theoretical Probability14, 125 (2001)

2001

-

[65]

R. C. Merton, Theory of rational option pricing, The Bell Journal of Economics and Management Science4, 141 (1973)

1973

-

[66]

M. B. Giles, Multilevel Monte Carlo methods, Acta numerica24, 259 (2015), arXiv:1304.5472

work page internal anchor Pith review Pith/arXiv arXiv 2015

-

[67]

M. R. Jerrum, L. G. Valiant, and V. V. Vazirani, Random generation of combinatorial structures from a uniform distribu- tion, Theoretical computer science43, 169 (1986)

1986

-

[68]

Broadie and P

M. Broadie and P. Glasserman, Estimating security price derivatives using simulation, Management Science42, 269 (1996)

1996

-

[69]

Fourni´ e, J.-M

E. Fourni´ e, J.-M. Lasry, J. Lebuchoux, P.-L. Lions, and N. Touzi, Applications of malliavin calculus to monte carlo methods in finance, Finance and Stochastics3, 391 (1999)

1999

-

[70]

M. B. Giles, Vibrato monte carlo sensitivities, inMonte Carlo and Quasi-Monte Carlo Methods 2008(Springer, 2009) pp. 369–382

2008

-

[71]

Bismut,Large Deviations and the Malliavin Calculus, Progress in Mathematics, Vol

J.-M. Bismut,Large Deviations and the Malliavin Calculus, Progress in Mathematics, Vol. 45 (Birkh¨ auser Boston, 1984)

1984

-

[72]

K. D. Elworthy and X.-M. Li, Formulae for the derivatives of heat semigroups, Journal of Functional Analysis125, 252 (1994)

1994

-

[73]

Fourni´ e, J.-M

E. Fourni´ e, J.-M. Lasry, J. Lebuchoux, and P.-L. Lions, Applications of malliavin calculus to monte carlo methods in finance. II, Finance and Stochastics5, 201 (2001)

2001

-

[74]

Gobet and A

E. Gobet and A. Kohatsu-Higa, Computation of greeks for barrier and look-back options using malliavin calculus, Electronic Communications in Probability8, 51 (2003)

2003

-

[75]

R. Lord, R. Koekkoek, and D. van Dijk, A comparison of biased simulation schemes for stochastic volatility models, Quantitative Finance10, 177 (2010)

2010

-

[76]

Kac, On distributions of certain wiener functionals, Transactions of the American Mathematical Society65, 1 (1949)

M. Kac, On distributions of certain wiener functionals, Transactions of the American Mathematical Society65, 1 (1949). 40 Supplementary Materials Appendix A: Terminal-value SPDE and Its BDSDE Representation It is well known that the Feynman-Kac formula provides a classical probabilistic representation for solutions of linear parabolic PDEs [76]. Given a t...

1949

-

[77]

Proof of Proposition 3 Proposition(Strong-error order for the direct pricing payoff).Fix(t, x)∈[0, T]×R d and a uniform grid{t k}N k=0 withh= (T−t)/N

Direct Pricing Estimator a. Proof of Proposition 3 Proposition(Strong-error order for the direct pricing payoff).Fix(t, x)∈[0, T]×R d and a uniform grid{t k}N k=0 withh= (T−t)/N. Let Ptk = Φ(t, tk)G X t,x tk +Y tk , whereY tk is the exact accumulated payoff Ytk = Z tk t Φ(t, r) F(r, X t,x r ) +d(r)H(r, X t,x r ) dr+ Z tk t Φ(t, r)H(r, X t,x r ) d← −B r. L...

-

[78]

Moreover,S int satisfies the accumulated stability estimate defined in Definition 4

The strong-error orders ofS X,S Φ andS int arep X , pΦ, pint respectively. Moreover,S int satisfies the accumulated stability estimate defined in Definition 4

-

[79]

3.Gis globally Lipschitz, i.e., there existsL G >0such that|G(x)−G(y)| ≤L G|x−y|

There existsM >0, independent ofh, such thatΦ (h) k andG(X t,x tk )are uniformly bounded inL 4 W,B byM. 3.Gis globally Lipschitz, i.e., there existsL G >0such that|G(x)−G(y)| ≤L G|x−y|. Then the payoff approximation satisfies the joint strong-error bound sup 0≤k≤N Ptk −P (h) k L2 =O(h p), p= min{p X , pΦ, pint}. Proof.First, for each 0≤k≤N, we have Ptk −P...

-

[80]

First-order Greek Estimators a. Proof of Proposition 6 Proposition(Strong-error order for the first-order Greek payoff).Fix(t, x)∈[0, T]×R d and1≤i≤dand define P (i) tk =Φ(t, tk)∇G(X t,x tk )⊤J t,x tk ei +Y (i) tk , where Y (i) tk = Z tk t Φ(t, s)∇ x F(s, X t,x s ) +d(s)H(s, X t,x s ) ⊤ J t,x s ei ds+ Z tk t Φ(t, s)∇ xH(s, X t,x s )⊤J t,x s ei d← −B s. Le...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.