Generalized statistical arbitrage concepts and related gain strategies

Pith reviewed 2026-05-24 17:57 UTC · model grok-4.3

The pith

Generalized statistical arbitrage allows strategies to yield positive average gains in sigma-algebra-specified scenarios rather than almost surely.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

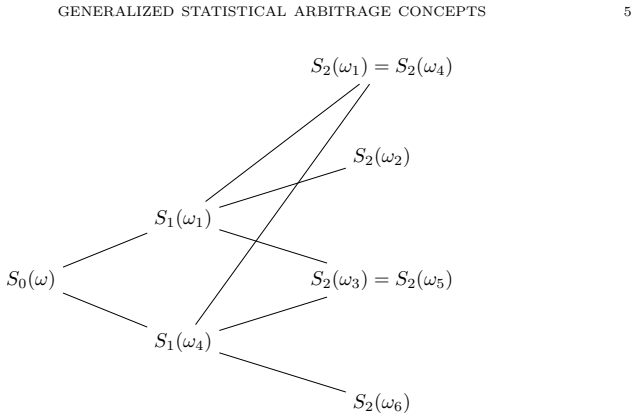

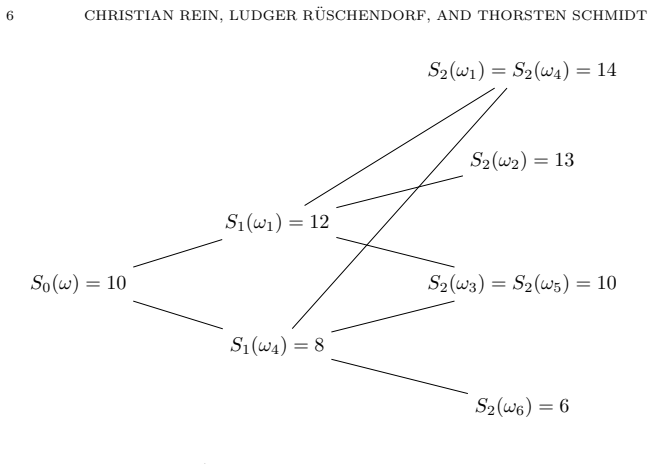

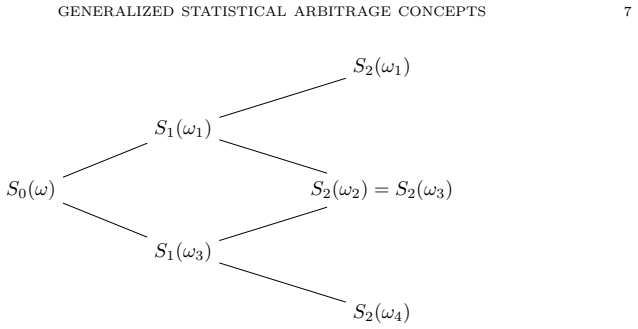

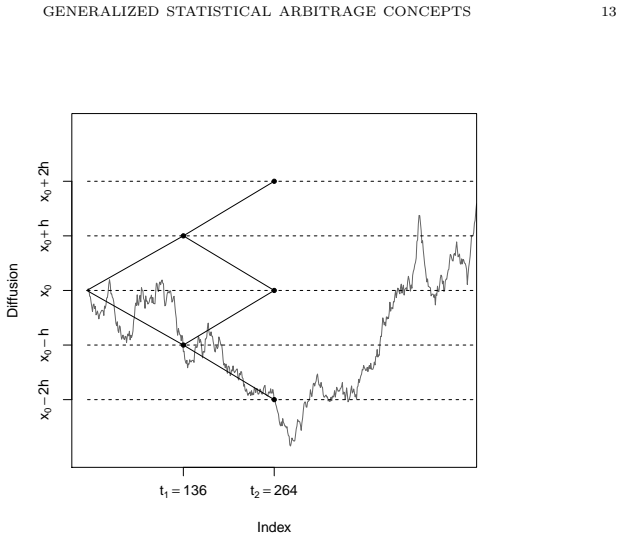

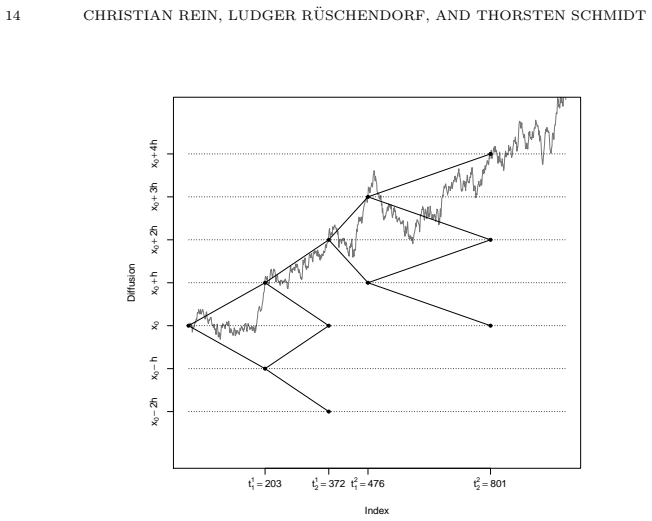

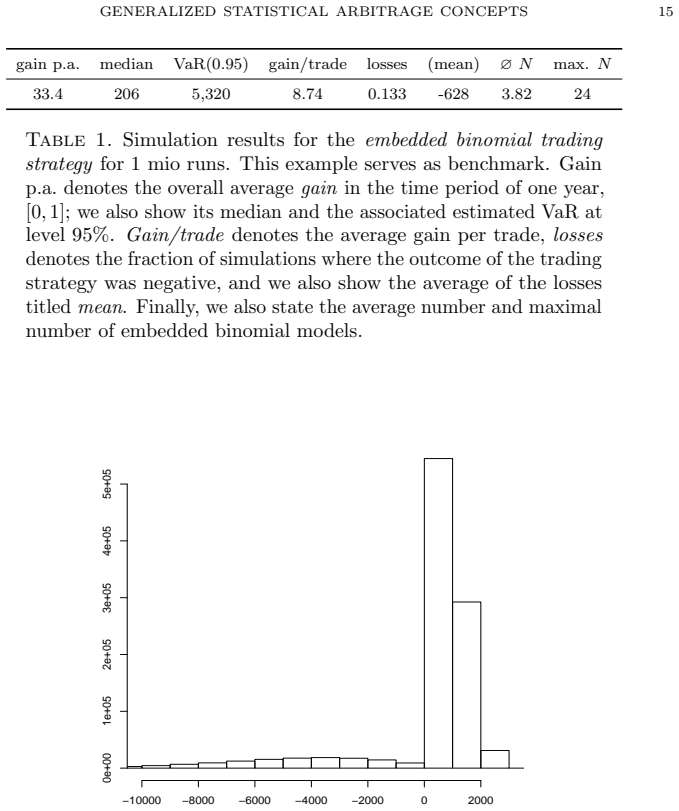

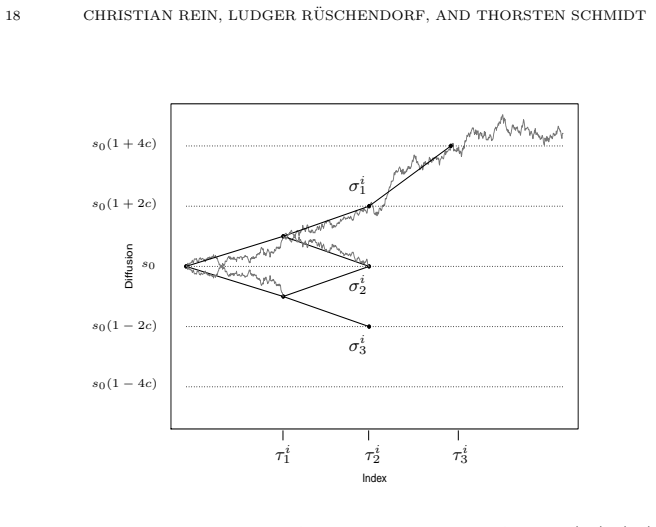

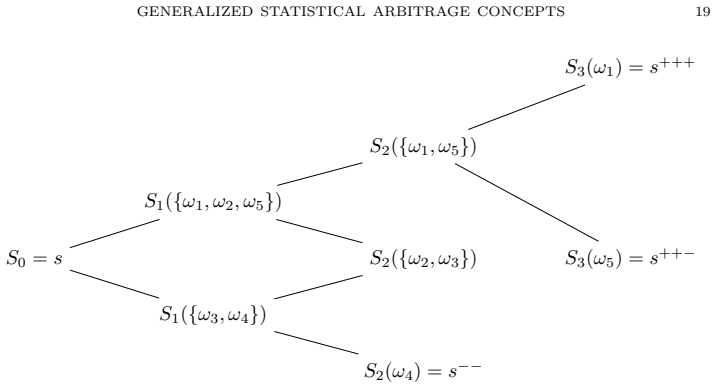

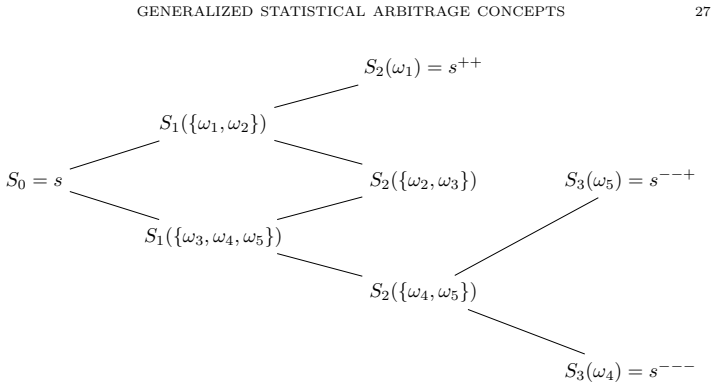

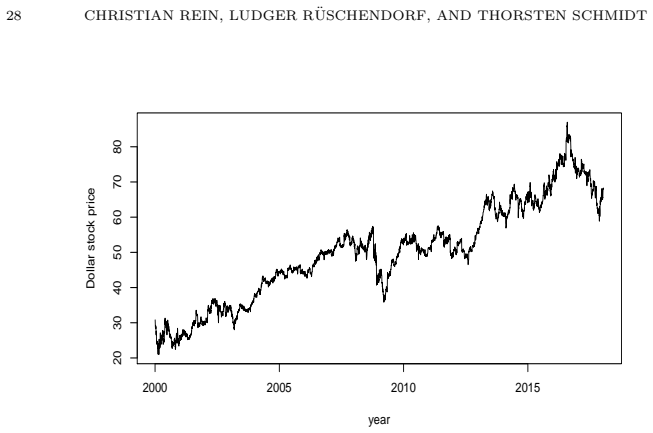

Generalized statistical arbitrage notions are introduced and characterized using an information system given by a sigma-algebra; under standard no-arbitrage, generalized gain strategies exist that deliver positive average gains precisely under the scenarios selected by this sigma-algebra. Concrete constructions of such strategies, including embedded binomial, follow-the-trend, and partition-type forms, are provided and shown to produce positive performance on both simulated and market data.

What carries the argument

An information system given by a sigma-algebra that selects the relevant market scenarios in which average gains are required.

If this is right

- Generalized statistical no-arbitrage conditions can be characterized for any chosen sigma-algebra.

- Embedded binomial strategies, follow-the-trend strategies, and partition-type strategies qualify as generalized profitable strategies for suitable information systems.

- These strategies exhibit positive performance on simulated data and on real market data, supporting their use in applications.

Where Pith is reading between the lines

- Different choices of sigma-algebra could let an investor encode specific views about which market states matter for average performance.

- The framework may open a route to constructing near-arbitrage opportunities inside markets that satisfy classical no-arbitrage.

- Extending the constructions to include transaction costs or model uncertainty would test how robust the reported performance remains.

Load-bearing premise

The sigma-algebra can be chosen so that the resulting class of scenarios meaningfully extends classical arbitrage while still permitting explicit construction of profitable strategies.

What would settle it

A concrete market model or data set in which, for every non-trivial sigma-algebra, no trading strategy (static or dynamic) produces strictly positive average gains on the selected scenarios.

Figures

read the original abstract

Generalized statistical arbitrage concepts are introduced corresponding to trading strategies which yield positive gains on average in a class of scenarios rather than almost surely. The relevant scenarios or market states are specified via an information system given by a $\sigma$-algebra and so this notion contains classical arbitrage as a special case. It also covers the notion of statistical arbitrage introduced in Bondarenko (2003). Relaxing these notions further we introduce generalized profitable strategies which include also static or semi-static strategies. Under standard no-arbitrage there may exist generalized gain strategies yielding positive gains on average under the specified scenarios. In the first part of the paper we characterize these generalized statistical no-arbitrage notions. In the second part of the paper we construct several profitable generalized strategies with respect to various choices of the information system. In particular, we consider several forms of embedded binomial strategies and follow-the-trend strategies as well as partition-type strategies. We study and compare their behaviour on simulated data. Additionally, we find good performance on market data of these simple strategies which makes them profitable candidates for real applications.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces generalized statistical arbitrage concepts tied to trading strategies that produce positive expected gains conditional on scenarios specified by a sigma-algebra (rather than almost surely). This framework is claimed to recover classical arbitrage (when the sigma-algebra is the full one) and to contain Bondarenko’s statistical arbitrage as a special case. The first part characterizes the associated generalized no-arbitrage conditions; the second part constructs explicit strategies (embedded binomial, follow-the-trend, partition-type) and reports their performance on simulated and real market data.

Significance. If the characterizations are rigorous and the constructed strategies demonstrably deliver positive conditional expected gains without introducing inconsistencies with standard no-arbitrage, the work could supply a flexible bridge between theoretical no-arbitrage theory and practical, scenario-conditioned trading rules. The explicit constructions and empirical comparisons constitute a concrete strength.

major comments (3)

- [Characterization of generalized no-arbitrage notions (first part)] The central extension via an arbitrary sigma-algebra is load-bearing for all subsequent claims. The manuscript must supply the precise measure-theoretic condition replacing “no positive gain a.s.” (likely in the characterization section) and prove that it is equivalent to the existence of an equivalent measure on the atoms; without this, it is unclear whether the notion collapses or fails to preserve strategy-construction properties for typical filtrations used in continuous-time models.

- [Introduction / Abstract] The claim that the generalized notion properly contains Bondarenko (2003) requires an explicit choice of sigma-algebra and a proof of inclusion; the abstract states containment but does not indicate the functional relationship that guarantees it.

- [Second part / Empirical study] For the constructed strategies (binomial, follow-the-trend, partition-type), the paper must verify that the reported positive average gains are indeed conditional on the chosen sigma-algebra atoms and are not artifacts of in-sample fitting or data snooping; otherwise the empirical support does not substantiate the theoretical claims.

minor comments (2)

- Notation for the information system (sigma-algebra) and the associated conditional expectations should be introduced once and used consistently; multiple ad-hoc symbols for the same object reduce readability.

- [Abstract] The abstract asserts “good performance on market data” without reporting quantitative metrics (Sharpe ratios, drawdowns, out-of-sample periods); these should be added for reproducibility.

Simulated Author's Rebuttal

We thank the referee for the thorough review and insightful comments on our manuscript. We address each of the major comments below and outline the revisions we plan to make.

read point-by-point responses

-

Referee: [Characterization of generalized no-arbitrage notions (first part)] The central extension via an arbitrary sigma-algebra is load-bearing for all subsequent claims. The manuscript must supply the precise measure-theoretic condition replacing “no positive gain a.s.” (likely in the characterization section) and prove that it is equivalent to the existence of an equivalent measure on the atoms; without this, it is unclear whether the notion collapses or fails to preserve strategy-construction properties for typical filtrations used in continuous-time models.

Authors: We acknowledge the importance of a rigorous measure-theoretic foundation. The manuscript's characterization section introduces the generalized no-arbitrage condition as the non-existence of a trading strategy with positive expected gain conditional on the sigma-algebra. We will revise to include the precise statement replacing the almost-sure condition and provide a proof of equivalence to the existence of an equivalent measure on the atoms of the sigma-algebra. Additionally, we will include a discussion on the applicability to continuous-time models to address potential concerns about the notion's behavior under typical filtrations. revision: yes

-

Referee: [Introduction / Abstract] The claim that the generalized notion properly contains Bondarenko (2003) requires an explicit choice of sigma-algebra and a proof of inclusion; the abstract states containment but does not indicate the functional relationship that guarantees it.

Authors: The abstract and introduction state that the generalized notion contains Bondarenko's statistical arbitrage as a special case. To make this explicit, we will specify the sigma-algebra (namely, the one generated by the relevant market variables at maturity) and add a short proof of the inclusion in a revised version of the introduction. This will clarify the functional relationship. revision: yes

-

Referee: [Second part / Empirical study] For the constructed strategies (binomial, follow-the-trend, partition-type), the paper must verify that the reported positive average gains are indeed conditional on the chosen sigma-algebra atoms and are not artifacts of in-sample fitting or data snooping; otherwise the empirical support does not substantiate the theoretical claims.

Authors: We agree that it is essential to confirm the conditional nature of the gains in the empirical section. The strategies are designed so that the positive expected gains hold conditionally on the atoms by construction. In the revised manuscript, we will include additional tables or figures showing the conditional expected gains on the sigma-algebra atoms for both simulated and market data. We will also emphasize the use of out-of-sample testing and robustness checks to rule out data snooping effects. revision: yes

Circularity Check

No significant circularity; derivation is self-contained

full rationale

The paper introduces definitions of generalized statistical arbitrage via an arbitrary sigma-algebra on scenarios, explicitly recovering classical arbitrage as the special case of the full sigma-algebra and extending the external Bondarenko (2003) notion. Characterization of the associated no-arbitrage conditions and explicit construction of strategies (embedded binomial, follow-the-trend, partition-type) proceed from standard measure-theoretic inequalities on conditional expectations without reducing any claimed prediction or uniqueness result to a fitted parameter, self-citation chain, or definitional tautology. No load-bearing self-citation, ansatz smuggling, or renaming of known results is exhibited.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Avellaneda, M. and Lee, J.-H. (2010), ‘Statistical arbitrage in the US equities market’, Quantitative Finance 10(7), 761–782

work page 2010

-

[2]

Bernardo, A. E. and Ledoit, O. (2000), ‘Gain, loss, and asset pricing’, Journal of political economy 108(1), 144–172

work page 2000

-

[3]

Bondarenko, O. (2003), ‘Statistical arbitrage and securities prices’, The Review of Financial Studies 16(3), 875–919

work page 2003

-

[4]

Borodin, A. N. and Salminen, P. (2012), Handbook of Brownian motion-facts and formulae, Birkh¨ auser. ˇCern` y, A. and Hodges, S. (2002), The theory of good-deal pricing in financial markets, in ‘Mathematical Finance—Bachelier Congress 2000’, Springer, pp. 175–202

work page 2012

-

[5]

Cochrane, J. H. and Saa-Requejo, J. (2000), ‘Beyond arbitrage: Good-deal asset price bounds in incomplete markets’, Journal of political economy 108(1), 79–119

work page 2000

-

[6]

Delbaen, F. and Schachermayer, W. (1994), ‘A general version of the fundamental theorem of asset pricing’, Mathematische Annalen 300(1), 463–520

work page 1994

-

[7]

Delbaen, F. and Schachermayer, W. (1995 b), ‘The no-arbitrage property under a change of num´ eraire’,Stochastics and Stochastic Reports 53(3-4), 213–226

work page 1995

-

[8]

Delbaen, F. and Schachermayer, W. (2006), The mathematics of arbitrage , Springer Science & Business Media

work page 2006

-

[9]

Elliott, R. J., Van Der Hoek, J. and Malcolm, W. P. (2005), ‘Pairs trading’, Quanti- tative Finance 5(3), 271–276

work page 2005

-

[10]

Gatev, E., Goetzmann, W. N. and Rouwenhorst, K. G. (2006), ‘Pairs trading: Performance of a relative-value arbitrage rule’, The Review of Financial Studies 19(3), 797–827. G¨ onc¨ u, A. (2015), ‘Statistical arbitrage in the Black–Scholes framework’,Quantitative Finance 15(9), 1489–1499

work page 2006

-

[11]

Hansen, L. P. and Jagannathan, R. (1991), ‘Implications of security market data for models of dynamic economies’, Journal of political economy 99(2), 225–262

work page 1991

-

[12]

Hogan, S., Jarrow, R., Teo, M. and Warachka, M. (2004), ‘Testing market efficiency using statistical arbitrage with applications to momentum and value strategies’, Journal of Financial economics 73(3), 525–565

work page 2004

-

[13]

Kassberger, S. and Liebmann, T. (2017), ‘Additive portfolio improvement and utility-efficient payoffs’, Mathematics and Financial Economics 11(2), 241–262

work page 2017

-

[14]

Krauss, C. (2017), ‘Statistical arbitrage pairs trading strategies: Review and outlook’, Journal of Economic Surveys 31(2), 513–545. Freiburg University, Dep. of Mathematics, Ernst-Zermelo Str. 1, 79104 Freiburg, Germany. E-mail address : ch.rein@gmx.net, ruschen@stochastik.uni-freiburg.de Freiburg Institute of Advanced Studies (FRIAS), Germany. Universit...

work page 2017

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.