MACROCAST: A Vintage-Consistent Time Series Foundation Model for Real-Time Macroeconomic Forecasting

Pith reviewed 2026-06-30 09:00 UTC · model grok-4.3

The pith

MACROCAST trains the first time series foundation model for macroeconomic forecasting without exposure to future or revised data.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

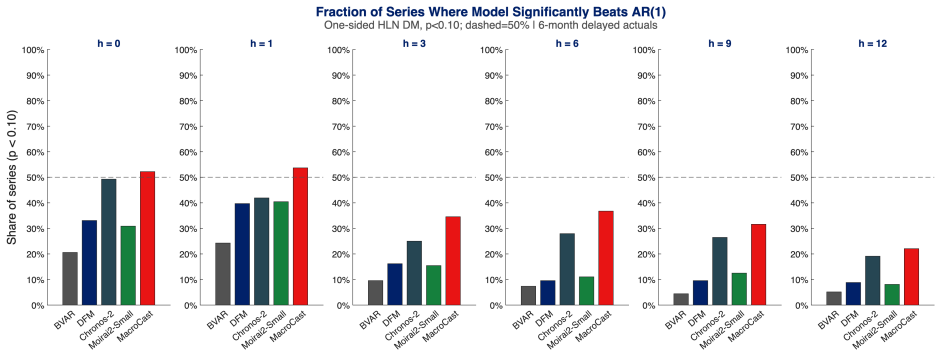

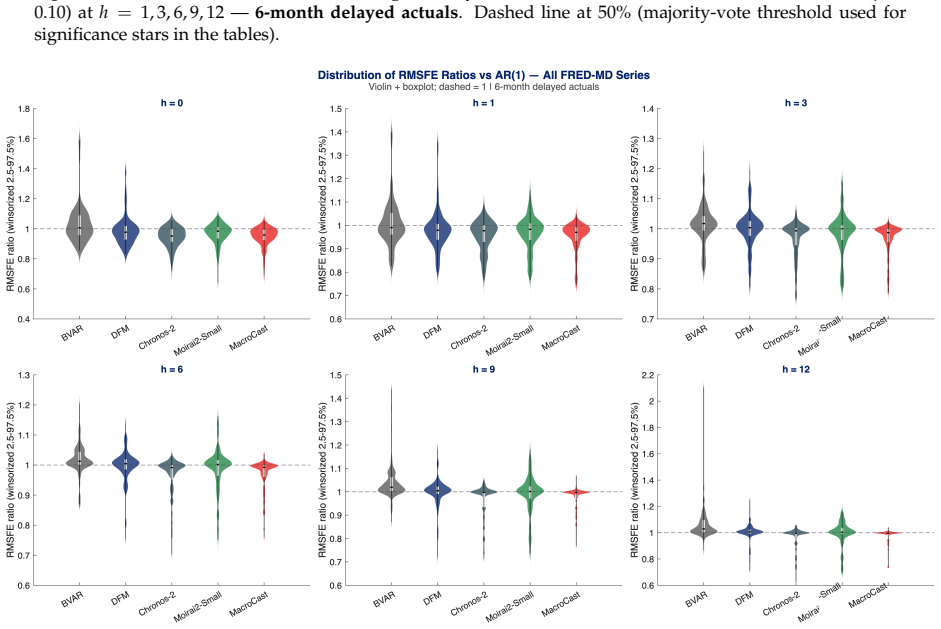

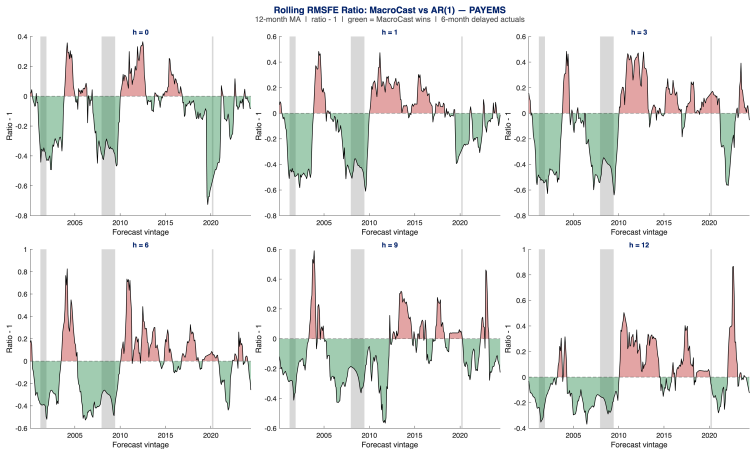

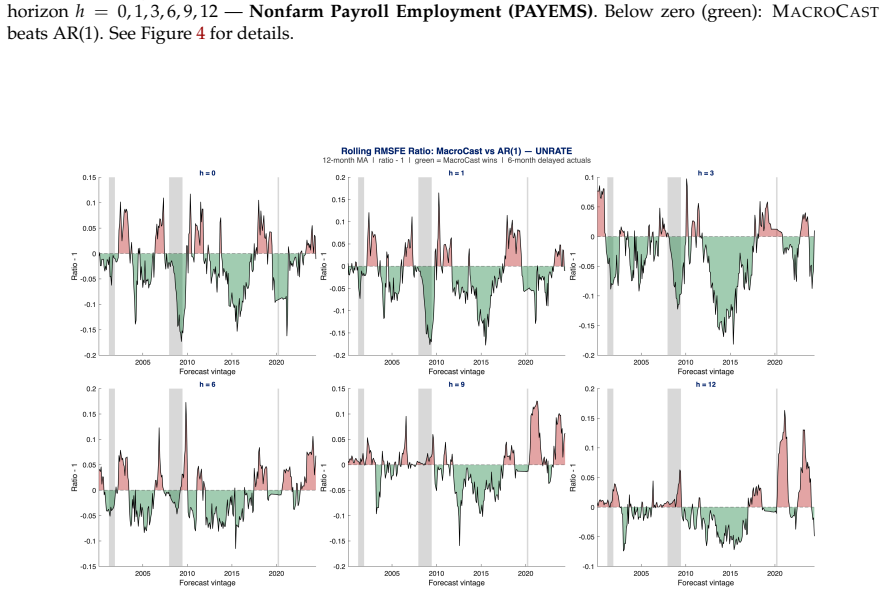

MACROCAST is the first TSFM that rules out both temporal contamination and revision bias entirely: at no stage of training is the model exposed to information that would not have been available to a forecaster in real time, achieved by pretraining on purely synthetic series and fine-tuning on synthetic series drawn from BVARs, dynamic factor models, and ARIMAs estimated on vintage-specific ALFRED data, with competitive performance in genuine real-time out-of-sample tests on FRED-MD.

What carries the argument

Two-stage training on synthetic time series generated from BVARs, dynamic factor models, and ARIMAs estimated exclusively on vintage ALFRED data.

If this is right

- MACROCAST improves on the AR(1) benchmark for roughly 80% of series-horizon pairs.

- It matches or surpasses Chronos-2, the strongest currently available TSFM.

- It outperforms the Bayesian VAR and dynamic factor model benchmarks.

- Pretraining takes one GPU-day and each fine-tuning run takes nine minutes.

Where Pith is reading between the lines

- This vintage-consistent synthetic training approach could be extended to build leakage-free models for other real-time forecasting domains such as finance.

- The reliance on simulation suggests that foundation models for time series may not require large volumes of actual observed data when statistical generators can enforce information constraints.

- Similar methods might allow existing TSFMs to be adapted for real-time use without retraining from scratch on restricted data.

Load-bearing premise

Synthetic time series drawn from BVARs, dynamic factor models, and ARIMAs estimated on vintage ALFRED data sufficiently replicate the statistical properties and real-time information constraints of actual macroeconomic series without introducing simulation artifacts that affect out-of-sample performance.

What would settle it

A genuine real-time out-of-sample evaluation on FRED-MD vintages in which MACROCAST fails to improve on the AR(1) benchmark for most series-horizon pairs or to match Chronos-2 performance.

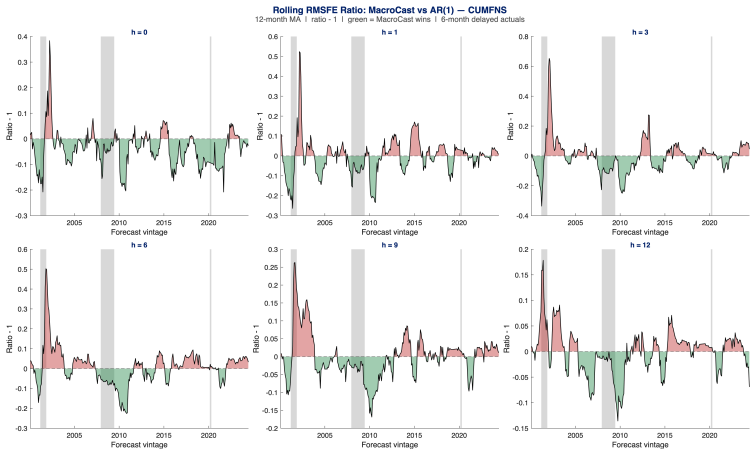

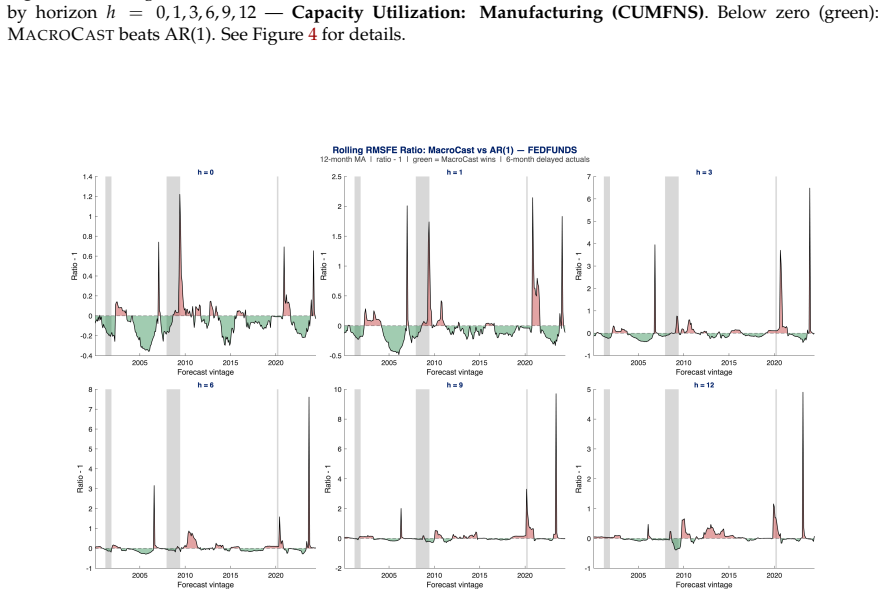

Figures

read the original abstract

We introduce MACROCAST, a lightweight Time Series Foundation Model (TSFM) for real-time macroeconomic forecasting. Existing TSFMs suffer from data leakage in two forms: temporal contamination, as the model may have seen the realized values of the series it forecasts, and revision bias, as training on fully revised data diverges from the preliminary, vintage-specific releases available to real-time forecasters. MACROCAST is, to our knowledge, the first TSFM that rules out both forms of leakage entirely: at no stage of training is the model exposed to information that would not have been available to a forecaster in real time. We train MACROCAST first on purely synthetic time series in approximately one GPU-day and then fine-tune it on synthetic time series drawn from Bayesian VARs, dynamic factor models, and ARIMA specifications estimated on vintage-specific ALFRED data. Because pretraining uses only simulated data and fine-tuning uses only real-time vintages, no observed future or revised value ever enters the model; each fine-tuning run takes nine minutes. Evaluated on the FRED-MD database in a genuine real-time out-of-sample exercise, MACROCAST improves on the AR(1) benchmark for roughly 80% of series-horizon pairs, matches or surpasses Chronos-2 -- the strongest currently available TSFM -- and outperforms the Bayesian VAR and dynamic factor model benchmarks, all in a data-leakage-free manner.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces MACROCAST, a lightweight Time Series Foundation Model (TSFM) for real-time macroeconomic forecasting. It claims to be the first TSFM to eliminate both temporal contamination and revision bias by pretraining exclusively on synthetic time series and fine-tuning on synthetic series generated from BVARs, dynamic factor models, and ARIMAs estimated only on vintage ALFRED releases. Evaluated in a genuine real-time out-of-sample exercise on FRED-MD, it reports improvements over the AR(1) benchmark for roughly 80% of series-horizon pairs, matching or surpassing Chronos-2, and outperforming BVAR and DFM benchmarks, all while ensuring no future or revised data enters training.

Significance. If the leakage-free construction and performance results hold under scrutiny, the work would be a notable contribution to real-time macro forecasting. The vintage-consistent synthetic data pipeline allows scaling a foundation model without violating information constraints, and the reported training efficiency (one GPU-day pretraining, nine-minute fine-tunes) is a practical advantage. Explicit credit is due for the parameter-free leakage elimination by construction and the reproducible real-time evaluation protocol.

major comments (2)

- [Abstract] Abstract: the claim of matching or surpassing Chronos-2 requires explicit confirmation that Chronos-2 was evaluated under identical real-time vintage constraints and leakage-free conditions; otherwise the comparison does not directly support superiority of the proposed method.

- [Abstract] The weakest assumption—that synthetic series from vintage-estimated BVAR/DFM/ARIMA models replicate the statistical properties and real-time constraints of actual macro series without simulation artifacts—needs explicit validation tests (e.g., comparison of higher moments or forecast-error distributions between synthetic and actual vintages) to support the out-of-sample performance claims.

minor comments (1)

- The abstract states 'roughly 80% of series-horizon pairs'; reporting the exact number of series, horizons considered, and a breakdown by variable category would improve clarity and allow readers to assess robustness.

Simulated Author's Rebuttal

We thank the referee for the constructive review and recommendation of minor revision. We address each major comment point by point below.

read point-by-point responses

-

Referee: [Abstract] Abstract: the claim of matching or surpassing Chronos-2 requires explicit confirmation that Chronos-2 was evaluated under identical real-time vintage constraints and leakage-free conditions; otherwise the comparison does not directly support superiority of the proposed method.

Authors: We confirm that Chronos-2 was evaluated under the identical real-time vintage constraints and leakage-free conditions as all other models in the genuine out-of-sample exercise on FRED-MD. The uniform protocol ensures no future or revised data enters any benchmark. To make this explicit, we will revise the abstract and add a clarifying sentence in the evaluation section. revision: yes

-

Referee: [Abstract] The weakest assumption—that synthetic series from vintage-estimated BVAR/DFM/ARIMA models replicate the statistical properties and real-time constraints of actual macro series without simulation artifacts—needs explicit validation tests (e.g., comparison of higher moments or forecast-error distributions between synthetic and actual vintages) to support the out-of-sample performance claims.

Authors: We agree this assumption is central and that explicit validation would strengthen the manuscript. Although out-of-sample results are obtained on actual FRED-MD vintages, we will add comparisons of higher moments and forecast-error distributions between synthetic and actual vintages in a new appendix. revision: yes

Circularity Check

No significant circularity; leakage elimination is a design choice with independent evaluation

full rationale

The paper's core contribution is a training procedure (pretraining on purely synthetic series, fine-tuning on vintage-estimated BVAR/DFM/ARIMA synthetics from ALFRED) that by design excludes future realizations and revisions. This is presented as a methodological safeguard rather than a derived result. Performance claims rest on a separate genuine real-time out-of-sample evaluation against AR(1), Chronos-2, BVAR, and DFM benchmarks on FRED-MD, with no evidence that reported improvements reduce to quantities defined inside the model by construction. No self-definitional equations, fitted-input-as-prediction steps, or load-bearing self-citations appear in the abstract or described chain. The 'first to rule out leakage' phrasing is a priority claim, not a mathematical reduction. This matches the default expectation of non-circularity for a methods paper whose evaluation uses external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Synthetic series generated from BVARs, DFMs, and ARIMAs estimated on vintage ALFRED data adequately represent the real-time information environment.

Reference graph

Works this paper leans on

-

[1]

Todd E. Clark and Michael W. McCracken , doi =. Reality Checks and Comparisons of Nested Predictive Models , url =. 2012 , bdsk-url-1 =. https://doi.org/10.1198/jbes.2011.10278 , journal =

-

[2]

Clark and Michael W

Todd E. Clark and Michael W. McCracken , doi =. Nested forecast model comparisons: A new approach to testing equal accuracy , url =. Journal of Econometrics , keywords =. 2015 , bdsk-url-1 =

2015

-

[3]

Frank Schorfheide and Dongho Song , title=

-

[4]

Clark and Massimiliano Marcellino and Elmar Mertens , title=

Andrea Carriero and Todd E. Clark and Massimiliano Marcellino and Elmar Mertens , title=. Review of Economics and Statistics , volume=

-

[5]

Primiceri , title=

Michele Lenza and Giorgio E. Primiceri , title=. Journal of Applied Econometrics , doi=

-

[6]

2024 , Owner =

Artificial Intelligence and Inflation Forecasts , Author =. 2024 , Owner =

2024

-

[7]

Rao and Karlsson, Sune , journal =

Kadiyala, K. Rao and Karlsson, Sune , journal =. Forecasting with generalized bayesian vector auto regressions , volume =

-

[8]

Bayesian Inference in Dynamic Econometric Models , Author =

-

[9]

An introduction to Bayesian inference in econometrics , Author =

-

[10]

Journal of Business Economics and Statistics , Year =

Nowcasting GDP in real-time: A density combination approach , Author =. Journal of Business Economics and Statistics , Year =

-

[11]

2014 , Owner =

Nowcasting the Business Cycle in an Uncertain Enviroment , Author =. 2014 , Owner =

2014

-

[12]

Journal of Computer and System Sciences , Year =

Database-friendly random projections: Johnson-Lindenstrauss with binary coins , Author =. Journal of Computer and System Sciences , Year =. doi:http://dx.doi.org/10.1016/S0022-0000(03)00025-4 , ISSN =

-

[13]

Journal of Business & Economic Statistics , Year =

Bayesian Dynamic Factor Models and Portfolio Allocation , Author =. Journal of Business & Economic Statistics , Year =. doi:10.1080/07350015.2000.10524875 , Eprint =

-

[14]

Journal of Forecasting , Year =

Model uncertainty, thick modelling and the predictability of stock returns , Author =. Journal of Forecasting , Year =. doi:10.1002/for.958 , ISSN =

-

[15]

Journal of Business & Economic Statistics , Year =

Comparing Density Forecasts via Weighted Likelihood Ratio Tests , Author =. Journal of Business & Economic Statistics , Year =. doi:10.1198/073500106000000332 , Eprint =

-

[16]

Modeling and Forecasting Realized Volatility , Author =. Econometrica , Year =. doi:10.1111/1468-0262.00418 , ISSN =

-

[17]

Journal of the American Statistical Association , Year =

The Distribution of Realized Exchange Rate Volatility , Author =. Journal of the American Statistical Association , Year =. doi:10.1198/016214501750332965 , Eprint =

-

[18]

Journal of Business & Economic Statistics , Year =

Should Macroeconomic Forecasters Use Daily Financial Data and How? , Author =. Journal of Business & Economic Statistics , Year =. doi:10.1080/07350015.2013.767199 , Eprint =

-

[19]

Econometrica , Year =

An Improved Heteroskedasticity and Autocorrelation Consistent Covariance Matrix Estimator , Author =. Econometrica , Year =

-

[20]

Journal of Monetary Economics , Year =

Do macro variables, asset markets, or surveys forecast inflation better? , Author =. Journal of Monetary Economics , Year =

-

[21]

An algorithmic theory of learning: Robust concepts and random projection , Author =. Machine Learning , Year =. doi:10.1007/s10994-006-6265-7 , ISSN =

-

[22]

GDP Measurement: A Forecast Combination Perspective , Author =

Improving U.S. GDP Measurement: A Forecast Combination Perspective , Author =. Recent Advances and Future Directions in Causality, Prediction, and Specification Analysis , Publisher =. 2013 , Editor =. doi:10.1007/978-1-4614-1653-1_1 , ISBN =

-

[23]

Journal of Business & Economic Statistics , Year =

Real-Time Measurement of Business Conditions , Author =. Journal of Business & Economic Statistics , Year =. doi:10.1198/jbes.2009.07205 , Eprint =

-

[24]

Federal Reserve Bank of Minneapolis Quarterly Review , Year =

Are Phillips curves useful for forecasting inflation? , Author =. Federal Reserve Bank of Minneapolis Quarterly Review , Year =

-

[25]

Journal of Econometrics , Year =

Forecasting economic time series using targeted predictors , Author =. Journal of Econometrics , Year =. doi:http://dx.doi.org/10.1016/j.jeconom.2008.08.010 , ISSN =

-

[26]

The Quarterly Journal of Economics , Year =

Measuring Economic Policy Uncertainty , Author =. The Quarterly Journal of Economics , Year =. doi:10.1093/qje/qjw024 , Eprint =

-

[27]

Journal of Econometrics , Year =

Pooling , Author =. Journal of Econometrics , Year =. doi:http://dx.doi.org/10.1016/0304-4076(81)90057-9 , ISSN =

-

[28]

Banbura, Marta and Giannone, Domenico and Reichlin, Lucrezia , Journal =. Large. 2010 , Number =. doi:10.1002/jae.1137 , ISSN =

-

[29]

Barberis , Journal =

N. Barberis , Journal =. Investing for the. 2000 , Pages =

2000

-

[30]

Journal of the Royal Statistical Society, Series A , Year =

New methods of quality control , Author =. Journal of the Royal Statistical Society, Series A , Year =

-

[31]

Journal of the American Statistical Association , Year =

A Bayesian Analysis for Change Point Problems , Author =. Journal of the American Statistical Association , Year =

-

[32]

International Journal of Forecasting , Year =

Forecasting \ GDP\ growth using mixed-frequency models with switching regimes , Author =. International Journal of Forecasting , Year =. doi:http://dx.doi.org/10.1016/j.ijforecast.2014.04.002 , ISSN =

-

[33]

Journal of Time Series Analysis , Year =

Large Sample Properties of Parameter Estimates for Periodic ARMA Models , Author =. Journal of Time Series Analysis , Year =. doi:10.1111/1467-9892.00246 , ISSN =

-

[34]

Bates, J. M. and Granger, C. W. J. , Journal =. Combination of. 1969 , Pages =

1969

-

[35]

Journal of Applied Econometrics , Year =

The Contribution of structural break models to forecasting macroeconomic series , Author =. Journal of Applied Econometrics , Year =. doi:10.1002/jae.2387 , ISSN =

-

[36]

Bayesian Model Comparison , Doi =

Model Switching and Model Averaging in Time-Varying Parameter Regression Models , Author =. Bayesian Model Comparison , Doi =. 2014 , Series =. http://www.emeraldinsight.com/doi/pdf/10.1108/S0731-905320140000034004 , Url =

-

[37]

, Journal =

Berkowitz, J. , Journal =. Testing. Journal of Business & Economic Statistics , Owner =. 2001 , Number =

2001

-

[38]

Studies in Nonlinear Dynamics and Econometrics , Year =

Beta Autoregressive Transition Markov-switching Models for Business Cycle Analysis , Author =. Studies in Nonlinear Dynamics and Econometrics , Year =

-

[39]

and Casarin, R

Billio, M. and Casarin, R. , Journal =. Identifying. 2010 , Pages =

2010

-

[40]

Journal of Econometrics , Year =

Time-varying combinations of predictive densities using nonlinear filtering , Author =. Journal of Econometrics , Year =

-

[41]

The European Journal of Finance , Year =

Combining forecasts: some results on exchange and interest rates , Author =. The European Journal of Finance , Year =

-

[42]

1975 , Address =

Discrete Multivariate Analysis: Theory and Practice , Author =. 1975 , Address =

1975

-

[43]

Economic Journal , Year =

Uncertainty and disagreement in economic prediction: the Bank of England survey of external forecasters , Author =. Economic Journal , Year =

-

[44]

Journal of Econometrics , Year =

Exploiting the errors: A simple approach for improved volatility forecasting , Author =. Journal of Econometrics , Year =. doi:http://dx.doi.org/10.1016/j.jeconom.2015.10.007 , ISSN =

-

[45]

Economic Journal , Year =

The Theory of Rational Heterogeneous Expectations: Evidence from Survey Data on Inflation Expectations , Author =. Economic Journal , Year =

-

[46]

Brooks, S. P. , Booktitle =. Bayesian analysis of animal abundance data via. 1999 , Editor =

1999

-

[47]

Brooks, S. P. , Journal =. Markov chain. 1997 , Pages =

1997

-

[48]

Brooks, S. P. and Catchpole, E. A. and Morgan, B. J. T. , Journal =. 1999 , Note =

1999

-

[49]

Assessing convergence of

Brooks, S P and Roberts, G O , Journal =. Assessing convergence of. 1999 , Pages =

1999

-

[50]

Transmission of Volatility and Trading Activity in the Global Interdealer Foreign Exchange Market: Evidence from Electronic Broking Services (EBS) Data , Author =

-

[51]

Canova, Fabio and Ciccarelli, Matteo , title=

-

[52]

Computational Statistics and Data Analysis , Year =

Modelling and forecasting wind speed intensity for weather risk management , Author =. Computational Statistics and Data Analysis , Year =

-

[53]

2005 , Owner =

Inference in Hidden Markov Models , Author =. 2005 , Owner =

2005

-

[54]

, Author =

Bayes and Empirical Bayes Methods for Data Analysis. , Author =. 1996 , Address =

1996

-

[55]

Sims , title=

Christopher A. Sims , title=. Business Cycles, Indicators, and Forecasting , editor =

-

[56]

Journal of the Royal Statistical Society: Series A (Statistics in Society) , Year =

Realtime nowcasting with a Bayesian mixed frequency model with stochastic volatility , Author =. Journal of the Royal Statistical Society: Series A (Statistics in Society) , Year =. doi:10.1111/rssa.12092 , ISSN =

-

[57]

Journal of Business & Economic Statistics , Year =

Andrea Carriero and Todd E. Clark and Massimiliano Marcellino , title =. Journal of Business & Economic Statistics , year =. doi:10.1080/07350015.2015.1040116 , owner =

-

[58]

Biometrika , Year =

On Gibbs Sampling for State Space Models , Author =. Biometrika , Year =

-

[59]

Electronic Journal of Statistics , Year =

Online data processing: Comparison of Bayesian regularized particle filters , Author =. Electronic Journal of Statistics , Year =

-

[60]

Journal of Forecasting , Year =

Nowcasting from disaggregates in the face of location shifts , Author =. Journal of Forecasting , Year =. doi:10.1002/for.1140 , ISSN =

-

[61]

Biometrics , Year =

Integrated Recovery/recapture Data analysis , Author =. Biometrics , Year =

-

[62]

Biometrics , Year =

Model selection in ring-recovery models using score tests , Author =. Biometrics , Year =

-

[63]

Boundary estimation in ring-recovery models , Author =. J.R. Statist.Soc. B , Year =

-

[64]

1992 , Address =

Aspects of boundary estimation in ring-recovery models , Author =. 1992 , Address =

1992

-

[65]

Journal of Econometrics , Year =

Moving average stochastic volatility models with application to inflation forecast , Author =. Journal of Econometrics , Year =. doi:http://dx.doi.org/10.1016/j.jeconom.2013.05.003 , ISSN =

-

[66]

Modeling energy price dynamics: \ GARCH\ versus stochastic volatility , Author =. Energy Economics , Year =. doi:http://dx.doi.org/10.1016/j.eneco.2015.12.003 , ISSN =

-

[67]

Journal of Business & Economic Statistics , Year =

Time Varying Dimension Models , Author =. Journal of Business & Economic Statistics , Year =. doi:10.1080/07350015.2012.663258 , Eprint =

-

[68]

Journal of Business & Economic Statistics , Year =

The Stochastic Volatility in Mean Model With Time-Varying Parameters: An Application to Inflation Modeling , Author =. Journal of Business & Economic Statistics , Year =. doi:10.1080/07350015.2015.1052459 , Eprint =

-

[69]

Journal of Financial Econometrics , Year =

On the Observed-Data Deviance Information Criterion for Volatility Modeling , Author =. Journal of Financial Econometrics , Year =. doi:10.1093/jjfinec/nbw002 , Eprint =

-

[70]

Journal of Business & Economic Statistics , Year =

A New Model of Trend Inflation , Author =. Journal of Business & Economic Statistics , Year =. doi:10.1080/07350015.2012.741549 , Eprint =

-

[71]

International Economic Review , Year =

An Econometric Characterization of Business Cycle Dynamics with Factor Structure and Regime Switching , Author =. International Economic Review , Year =

-

[72]

Handbook of Economic Forecasting , Publisher =

Forecasting Output , Author =. Handbook of Economic Forecasting , Publisher =. 2013 , Editor =. doi:http://dx.doi.org/10.1016/B978-0-444-53683-9.00003-7 , ISSN =

-

[73]

International Journal of Forecasting , Year =

Business cycle monitoring with structural changes , Author =. International Journal of Forecasting , Year =. doi:http://dx.doi.org/10.1016/j.ijforecast.2009.08.003 , ISSN =

-

[74]

Journal of Econometrics , Year =

Estimation and comparison of multiple change-point models , Author =. Journal of Econometrics , Year =. doi:http://dx.doi.org/10.1016/S0304-4076(97)00115-2 , ISSN =

-

[75]

Journal of Econometrics , Year =

Calculating posterior distributions and modal estimates in Markov mixture models , Author =. Journal of Econometrics , Year =. doi:http://dx.doi.org/10.1016/0304-4076(95)01770-4 , ISSN =

-

[76]

Siddhartha Chib , Journal =. Marginal Likelihood from the. 1995 , Number =. doi:10.1080/01621459.1995.10476635 , Eprint =

-

[77]

Understanding the Metropolis-Hastings Algorithm , Author =. The American Statistician , Year =. doi:10.1080/00031305.1995.10476177 , Eprint =

work page internal anchor Pith review Pith/arXiv arXiv doi:10.1080/00031305.1995.10476177 1995

-

[78]

Statistica Neerlandica , Year =

Accept�reject Metropolis�Hastings sampling and marginal likelihood estimation , Author =. Statistica Neerlandica , Year =. doi:10.1111/j.1467-9574.2005.00277.x , ISSN =

-

[79]

Siddhartha Chib and Ivan Jeliazkov , Journal =. Marginal Likelihood From the. 2001 , Number =. doi:10.1198/016214501750332848 , Eprint =

-

[81]

Journal of Econometrics , year =

Siddhartha Chib and Federico Nardari and Neil Shephard , title =. Journal of Econometrics , year =. doi:http://dx.doi.org/10.1016/j.jeconom.2005.06.026 , keywords =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.