Recognition: no theorem link

Sequential Audit Sampling with Statistical Guarantees

Pith reviewed 2026-05-10 17:51 UTC · model grok-4.3

The pith

Sequential audit sampling controls decision error probabilities exactly using finite-population error rates.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

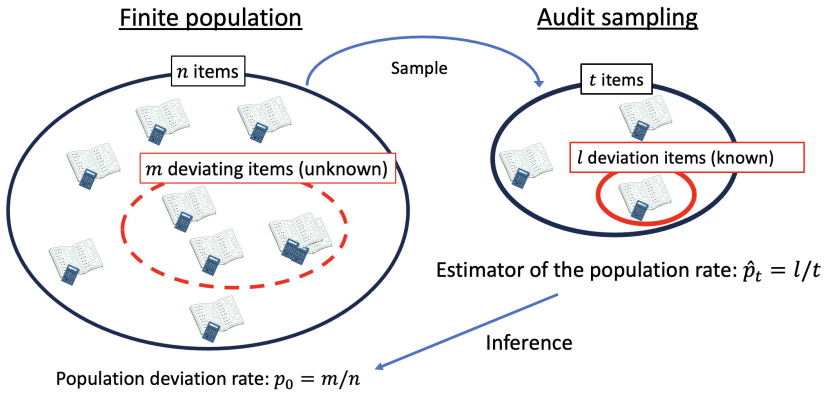

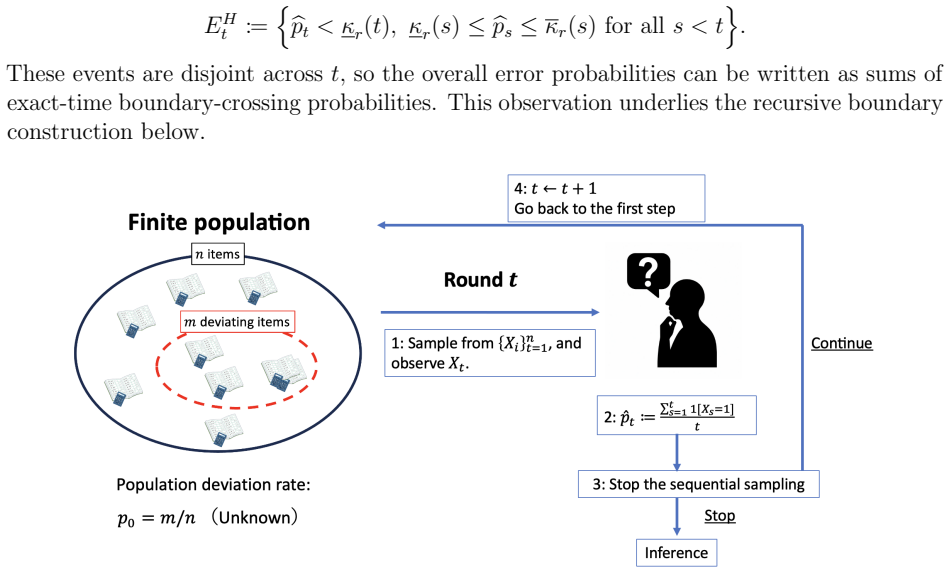

The paper formulates exact sequential boundary conditions for audit sampling from finite populations in terms of finite-population error probabilities under hypotheses defined by a tolerable deviation rate. The exact design provides ex ante control of decision error probabilities, and the simulation-based version approximates those boundaries while allowing computation of expected stopping times.

What carries the argument

Sequential boundary conditions expressed in finite-population error probabilities, calibrated by Monte Carlo simulation at least-favorable deviation rates.

If this is right

- Auditors obtain ex ante guarantees on false acceptance and false rejection rates when extending samples sequentially.

- Expected sample sizes under the procedure can be calculated in advance for audit planning.

- The framework supports direct application to tests of controls and deviation-rate auditing.

- One-sided, two-stage, and truncated variants follow from the same boundary construction.

Where Pith is reading between the lines

- Average audit effort may drop because sampling can stop early once evidence suffices.

- The same finite-population sequential logic could transfer to other inspection or quality-control settings with limited populations.

- For very large populations the finite-population correction becomes negligible and the method approaches classical sequential probability ratio tests.

Load-bearing premise

Monte Carlo simulation at least-favorable deviation rates produces boundaries that reliably approximate the exact finite-population error probabilities for practical sample sizes and populations.

What would settle it

For a small population where exact error probabilities can be enumerated directly, compare the Monte Carlo-calibrated boundaries against the true probabilities and check whether achieved decision error rates stay within target levels.

Figures

read the original abstract

Financial statement auditing is conducted under a risk-based evidence approach to obtain reasonable assurance. In practice, auditors often perform additional sampling or related procedures when an initial sample does not provide a sufficient basis for a conclusion. Across jurisdictions, current standards and practice manuals acknowledge such extensions, while the statistical design of sequential audit procedures has not been fully explored. This study formulates audit sampling with additional, sequentially collected items as a sequential testing problem for a finite population under sampling without replacement. We define null and alternative hypotheses in terms of a tolerable deviation rate, specify stopping and decision rules, and formulate exact sequential boundary conditions in terms of finite-population error probabilities. For practical implementation, we calibrate those boundaries by Monte Carlo simulation at least-favorable deviation rates. The exact design yields ex ante control of decision error probabilities, and the simulation-based implementation approximates that design while allowing the computation of expected stopping times. The framework is most naturally suited to attribute auditing and deviation-rate auditing, especially tests of controls, and it can be extended to one-sided, two-stage, and truncated designs.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper formulates audit sampling with sequential additions as a sequential hypothesis test for a finite population under sampling without replacement. It defines null and alternative hypotheses in terms of a tolerable deviation rate, specifies stopping and decision rules, and derives exact sequential boundary conditions using finite-population error probabilities. For implementation, boundaries are calibrated via Monte Carlo simulation at least-favorable deviation rates; the exact design is claimed to deliver ex ante type-I and type-II error control while the simulation version approximates it and permits computation of expected stopping times. The framework targets attribute and deviation-rate auditing (especially tests of controls) and admits extensions to one-sided, two-stage, and truncated designs.

Significance. If the Monte Carlo approximation is shown to preserve the nominal error controls, the work supplies a statistically grounded design for sequential audit procedures that current standards acknowledge but do not formally specify. The exact finite-population boundary formulation and the explicit calculation of expected stopping times are clear strengths that could improve both the defensibility and efficiency of audit sampling. The contribution is most relevant to attribute sampling and tests of controls.

major comments (2)

- [Monte Carlo Implementation] Monte Carlo Implementation section: the claim that calibrating boundaries exclusively at least-favorable deviation rates guarantees ex ante control throughout the parameter space is not demonstrated. In discrete hypergeometric-type distributions, the error-probability surface can have local maxima away from the least-favorable points; the manuscript must either prove that control at these points implies global control or supply a counter-example bound (unverified step (1) in the stress-test note).

- [Validation and Numerical Results] Validation and Numerical Results section: no analytic bound on Monte Carlo estimation error is given, nor are exhaustive exact-enumeration comparisons reported for representative finite N. Because the underlying distributions are discrete, modest sampling variability in the estimated boundaries can produce non-negligible jumps in realized cumulative error probabilities; the paper should quantify the approximation error against exact hypergeometric calculations for small-to-moderate populations (unverified step (2)).

minor comments (2)

- [Abstract] Abstract: the statement that the simulation-based implementation 'approximates' the exact design would be strengthened by a quantitative tolerance (e.g., maximum excess error probability) or by reference to the validation results.

- [Methodology] Notation: the definition of the finite-population error probability used for the exact boundaries should be stated explicitly (hypergeometric or equivalent) before the Monte Carlo approximation is introduced.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback on the Monte Carlo calibration and validation aspects of our sequential audit sampling framework. We address each major comment below and describe the revisions we will make to strengthen the manuscript.

read point-by-point responses

-

Referee: [Monte Carlo Implementation] Monte Carlo Implementation section: the claim that calibrating boundaries exclusively at least-favorable deviation rates guarantees ex ante control throughout the parameter space is not demonstrated. In discrete hypergeometric-type distributions, the error-probability surface can have local maxima away from the least-favorable points; the manuscript must either prove that control at these points implies global control or supply a counter-example bound (unverified step (1) in the stress-test note).

Authors: We acknowledge that the manuscript does not contain a formal proof that calibration at the least-favorable deviation rates ensures global ex ante control over the full parameter space. Our existing stress tests suggest these rates produce the highest error probabilities, but this is insufficient without further verification. In the revised version we will add a systematic numerical examination of the error-probability surface over a dense grid of deviation rates for representative finite populations (N = 100, 500, 1000). Should any local maxima exceed the nominal levels, we will either adjust the calibration procedure or supply explicit bounds. These results and any necessary adjustments will be incorporated into the Monte Carlo Implementation section. revision: yes

-

Referee: [Validation and Numerical Results] Validation and Numerical Results section: no analytic bound on Monte Carlo estimation error is given, nor are exhaustive exact-enumeration comparisons reported for representative finite N. Because the underlying distributions are discrete, modest sampling variability in the estimated boundaries can produce non-negligible jumps in realized cumulative error probabilities; the paper should quantify the approximation error against exact hypergeometric calculations for small-to-moderate populations (unverified step (2)).

Authors: We agree that an analytic bound on Monte Carlo estimation error is desirable yet difficult to obtain in closed form for the sequential boundary problem. To address the concern directly, we will add exhaustive exact-enumeration comparisons for small-to-moderate populations (N ≤ 300) where complete hypergeometric enumeration remains computationally feasible. For each such N we will report the exact versus Monte Carlo-calibrated boundaries, the resulting type-I and type-II error rates, and the maximum observed discrepancy. For larger N we will increase the number of Monte Carlo replications and include bootstrap confidence intervals on the estimated cumulative error probabilities. These quantitative comparisons will be presented in the Validation and Numerical Results section. revision: yes

Circularity Check

No significant circularity detected in derivation of sequential audit boundaries

full rationale

The paper formulates exact stopping boundaries directly from finite-population error probabilities (hypergeometric-style) to enforce ex ante type-I/II control by construction of the design itself. The Monte Carlo calibration at least-favorable rates is explicitly described as an approximation to this exact design rather than a re-derivation or fit that is then relabeled as a prediction. No self-definitional loops, fitted-input-as-prediction, or load-bearing self-citations appear in the provided abstract or description; the central claim rests on a new sequential formulation for finite populations without reducing to its own inputs or prior author results by construction.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Sampling occurs without replacement from a finite population

- domain assumption Hypotheses are defined via a tolerable deviation rate

Reference graph

Works this paper leans on

-

[1]

Alison Hubbard Ashton and Robert H. Ashton. Sequential belief revision in auditing. The Accounting Review, 63 0 (4): 0 623--641, 1988

1988

-

[2]

ASA 530 : Audit sampling

Auditing and Assurance Standards Board . ASA 530 : Audit sampling. Compiled Australian Auditing Standard, 2021. Compilation prepared December 14, 2021. Available at: https://www.auasb.gov.au/media/ggwcjhpk/asa_530_12_21.pdf. Accessed 2026-04-02

2021

-

[3]

Research document no

Auditing and Assurance Standards Committee . Research document no. 1: Audit and statistical sampling, 2022. Japanese guidance document

2022

-

[4]

Statement no

Auditing Standards Committee . Statement no. 200: Overall objectives of the independent auditor and the conduct of an audit in accordance with auditing standards, 2022 a . Japanese auditing standard

2022

-

[5]

Statement no

Auditing Standards Committee . Statement no. 530: Audit sampling, 2022 b . Japanese auditing standard

2022

-

[6]

Julia Yu, and Jie Zhang

Yang Bao, Bin Ke, Bin Li, Y. Julia Yu, and Jie Zhang. Detecting accounting fraud in publicly traded u.s. firms using a machine learning approach. Journal of Accounting Research, 58 0 (1): 0 199--235, 2020

2020

-

[7]

On the revision of auditing standards, 2002

Business Accounting Council . On the revision of auditing standards, 2002. Japanese policy document

2002

-

[8]

Auditing standards, 2020

Business Accounting Council . Auditing standards, 2020. Japanese auditing standards

2020

-

[9]

Cushing and J.K

B.E. Cushing and J.K. Loebbecke. Comparison of Audit Methodologies of Large Accounting Firms. Studies in accounting research. American Accounting Association, 1986

1986

-

[10]

Elder, Abraham D

Randal J. Elder, Abraham D. Akresh, Steven M. Glover, Julia L. Higgs, and Jonathan Liljegren. Audit sampling research: A synthesis and implications for future research. AUDITING: A Journal of Practice & Theory, 32 0 (Supplement 1): 0 99--129, 05 2013

2013

-

[11]

ISA (NZ) 530 : Audit sampling

External Reporting Board . ISA (NZ) 530 : Audit sampling. Compiled New Zealand auditing standard, 2021. December 2021 compilation. Available at: https://standards.xrb.govt.nz/assets/Uploads/ISA-NZ-530-Dec-21.pdf. Accessed 2026-04-02

2021

-

[12]

Felix and William R

William L. Felix and William R. Kinney. Research in the auditor's opinion formulation process: State of the art. The Accounting Review, 57 0 (2): 0 245--271, 1982

1982

-

[13]

Thematic review: Audit sampling

Financial Reporting Council . Thematic review: Audit sampling. Financial Reporting Council thematic review, 2023. Available at: https://www.frc.org.uk/documents/6618/Thematic_Review_Audit_Sampling.pdf. Accessed 2026-04-02

2023

-

[14]

ISA (UK) 530 : Audit sampling

Financial Reporting Council . ISA (UK) 530 : Audit sampling. Financial Reporting Council standard page, 2025. Updated September 2025. Available at: https://www.frc.org.uk/library/standards-codes-policy/audit-assurance-and-ethics/auditing-standards/isa-uk-530/. Accessed 2026-04-02

2025

-

[15]

Propositions about the psychology of professional judgment in public accounting

Michael Gibbins. Propositions about the psychology of professional judgment in public accounting. Journal of Accounting Research, 22 0 (1): 0 103--125, 1984

1984

-

[16]

Gillett and Marietta Peytcheva

Peter R. Gillett and Marietta Peytcheva. Differential evaluation of audit evidence from fixed versus sequential sampling. Behavioral Research in Accounting, 23 0 (1): 0 65--85, 2011

2011

-

[17]

Nishtha Hooda. Audit Data . UCI Machine Learning Repository, 2018. DOI : https://doi.org/10.24432/C5930Q

-

[18]

Jane M. Horgan. A list‐sequential sampling scheme with applications in financial auditing. IMA Journal of Management Mathematics, 14 0 (1): 0 31--48, 2003

2003

-

[19]

2023--2024 handbook of international quality management, auditing, review, other assurance, and related services pronouncements

International Auditing and Assurance Standards Board . 2023--2024 handbook of international quality management, auditing, review, other assurance, and related services pronouncements. IAASB handbook webpage, 2024. Published August 29, 2024. Available at: https://www.iaasb.org/publications/2023-2024-handbook-international-quality-management-auditing-review...

2023

-

[20]

Isa 500 series

International Auditing and Assurance Standards Board . Isa 500 series. IAASB project page, 2026. Current project page describing information-gathering on ISA 501, ISA 505, and ISA 530, including issues related to the appropriate use and consistent application of audit sampling. Available at: https://www.iaasb.org/consultations-projects/isa-500-series. Acc...

2026

-

[21]

Masahiro Kato and Kei Nakagawa. Statistical formulation and theoretical guarantees for audit sampling procedures using sequential testing. SIG-FIN, 2025 0 (FIN-035): 0 117--124, 10 2025. ISSN 2436-5556. doi:10.11517/jsaisigtwo.2025.fin-035_117. URL https://cir.nii.ac.jp/crid/1390024323625617408

-

[22]

William R. Kinney. Decision theory aspects of internal control system design/compliance and substantive tests. Journal of Accounting Research, 13: 0 14--29, 1975

1975

-

[23]

Robert Knechel and Jr

W. Robert Knechel and Jr. Messier, William F. Sequential auditor decision making: Information search and evidence evaluation. Contemporary Accounting Research, 6 0 (2): 0 386--406, 1990

1990

-

[24]

Sequential Tests for Hypergeometric Distributions and Finite Populations

Tze Leung Lai. Sequential Tests for Hypergeometric Distributions and Finite Populations . The Annals of Statistics, 7 0 (1): 0 46 -- 59, 1979

1979

-

[25]

ISA 530 : Audit sampling

Malaysian Institute of Accountants . ISA 530 : Audit sampling. Official Malaysian Institute of Accountants standard PDF, 2018. Issue date January 2009; updated June 2018 according to the MIA standards page. Available at: https://mia.org.my/wp-content/uploads/2022/04/ISA_530.pdf. Accessed 2026-04-02

2018

-

[26]

Practical Financial Statement Auditing

Seijin Minami, Takuya Takahashi, and Takahashi Kazunori. Practical Financial Statement Auditing. CHUOKEIZAI-SHA, 4 edition, 2022. In Japanese

2022

-

[27]

AS 2315 : Audit sampling

Public Company Accounting Oversight Board . AS 2315 : Audit sampling. PCAOB auditing standard webpage, 2024. Current official standard page. Available at: https://pcaobus.org/oversight/standards/auditing-standards/details/AS2315. Accessed 2026-04-02

2024

-

[28]

David M. Ritzwoller, Joseph P. Romano, and Azeem M. Shaikh. Randomization inference: Theory and applications, 2025. a rXiv: 2406.09521

-

[29]

Government Accountability Office and Council of the Inspectors General on Integrity and Efficiency

U.S. Government Accountability Office and Council of the Inspectors General on Integrity and Efficiency . Financial audit manual, volume 1. GAO-25-107705, 2025. June 2025. Available at: https://www.gao.gov/assets/gao-25-107705.pdf. Accessed 2026-04-02

2025

-

[30]

Sequential Tests of Statistical Hypotheses

Abraham Wald. Sequential Tests of Statistical Hypotheses . The Annals of Mathematical Statistics, 16 0 (2): 0 117 -- 186, 1945

1945

-

[31]

Sequential tests for hypergeometric distribution

Xiaoping Xiong. Sequential tests for hypergeometric distribution. PhD thesis, Purdue University, 1993. Ph.D. dissertation

1993

-

[32]

A class of sequential conditional probability ratio tests

Xiaoping Xiong. A class of sequential conditional probability ratio tests. Journal of the American Statistical Association, 90 0 (432): 0 1463--1473, 1995

1995

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.