Recognition: unknown

Orthogonal reparametrization of the Nelson-Siegel-Svensson interest rate curve model: conditioning, diagnostics, and identifiability

Pith reviewed 2026-05-10 01:28 UTC · model grok-4.3

The pith

A thin QR decomposition produces orthogonal linear parameters for the Nelson-Siegel-Svensson model with a diagonal conditional Fisher information matrix.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

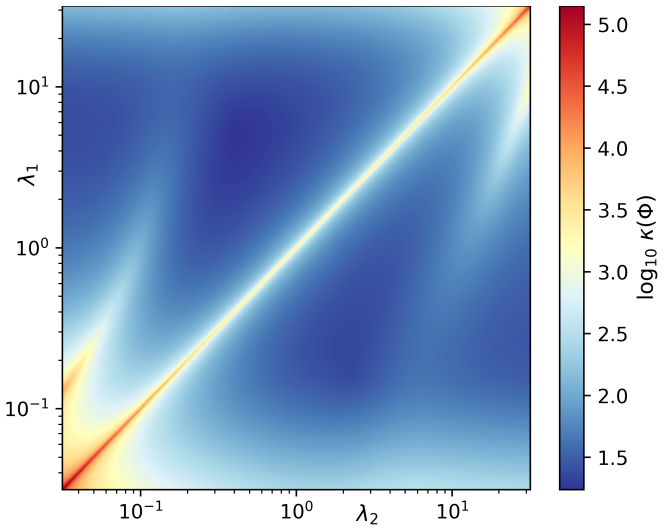

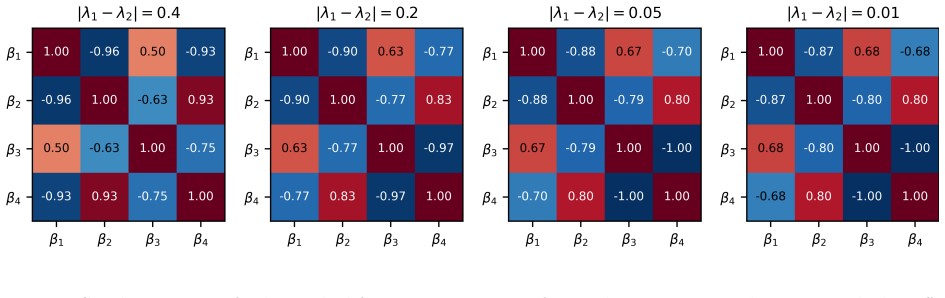

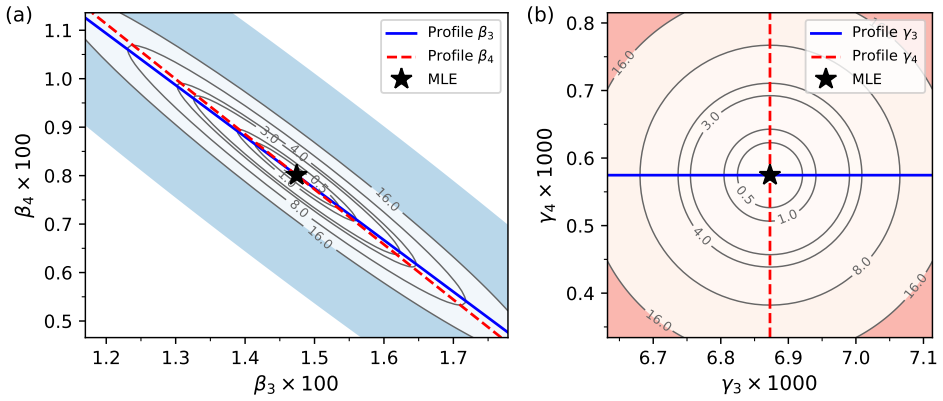

The central claim is that an exact orthogonal reparametrization via thin QR decomposition of the NSS design matrix yields orthogonal linear parameters for which the Fisher information matrix is diagonal conditional on the nonlinear parameters. A finite-horizon analytical version gives closed-form orthogonal basis entries involving exponentials, logs, and the exponential integral. Combined with Jacobian and profile-likelihood analysis, this isolates the conditioning structure from the degenerate manifold λ1=λ2 where two degrees of freedom are lost, and supplies an explicit Schur-complement covariance form for joint estimation.

What carries the argument

Thin QR decomposition applied to the NSS basis matrix, which orthogonalizes the linear parameters and diagonalizes their conditional Fisher information while preserving the original least-squares solution.

If this is right

- The least-squares fit and uncertainty of the original linear parameters remain unchanged.

- Full first-order covariance in orthogonal coordinates has an explicit Schur-complement form during joint nonlinear estimation of decay parameters.

- Synthetic experiments confirm elimination of correlations among linear parameters and uniform conditional uncertainty.

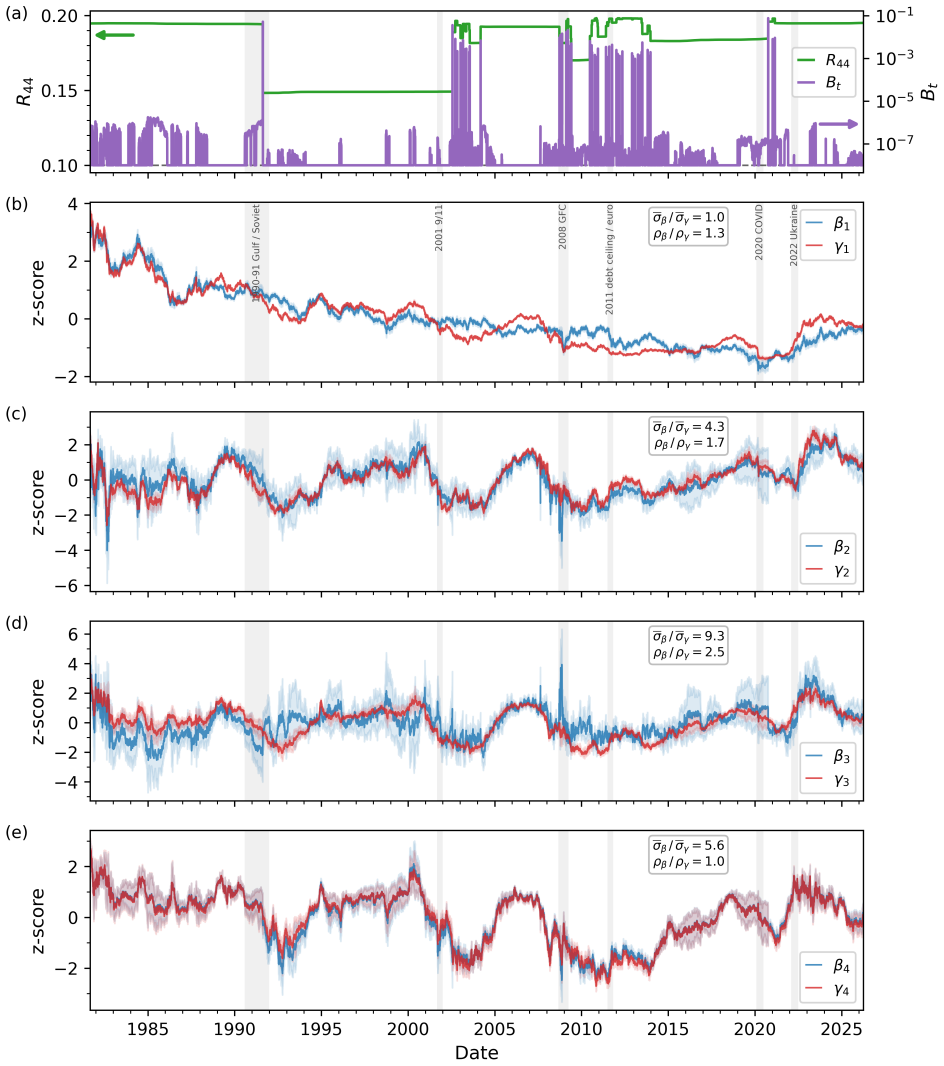

- Daily U.S. Treasury analysis on fixed tenors shows smoother orthogonal parameter series than classical NSS parameters.

Where Pith is reading between the lines

- The approach may extend to other separable nonlinear regression problems with collinear regressors in econometrics.

- Since the moving QR basis remains nearly constant, it could enable efficient online updating of curve fits without full recomputation.

- Clarifying the degenerate manifold could guide model selection between Nelson-Siegel and Svensson extensions in practice.

Load-bearing premise

The primary source of instability is collinearity in the basis functions, and the QR reparametrization fully separates this numerical issue from identifiability problems on the λ1=λ2 manifold without introducing artifacts in joint estimation.

What would settle it

If joint estimation of the decay parameters under the orthogonal coordinates still produces correlated linear parameters or non-uniform uncertainties, or if the QR basis changes substantially over time in real data, the separation of conditioning from identifiability would not hold.

Figures

read the original abstract

The Nelson-Siegel-Svensson (NSS) interest rate curve model yields a separable nonlinear least-squares problem whose inner linear block is often ill-conditioned because the basis functions become nearly collinear. We analyze this instability via an exact orthogonal reparametrization of the design matrix. A thin QR decomposition produces orthogonal linear parameters for which, conditional on the nonlinear parameters, the Fisher information matrix is diagonal. We also derive a finite-horizon analytical orthogonalization: on $[0,T]$, the $4\times 4$ continuous Gram matrix has closed-form entries involving exponentials, logarithms, and the exponential integral $E_1$, yielding an explicit horizon-dependent orthogonal NSS basis. Together with Jacobian-rank and profile-likelihood arguments, this representation clarifies the degenerate manifold $\lambda_1=\lambda_2$, where the Svensson extension loses two degrees of freedom. Orthogonalization leaves the least-squares fit and uncertainty of the original linear parameters unchanged, but isolates the conditioning structure. When the decay parameters are estimated jointly, the full first-order covariance in orthogonal coordinates admits an explicit Schur-complement form. The approach also yields a scalar identifiability diagnostic through the QR element $R_{44}$ and separates model reduction from numerical instability. Synthetic experiments confirm that orthogonal parametrization eliminates correlations among the linear parameters and keeps their conditional uncertainty uniform. A daily U.S. Treasury study on a reduced fixed 9-tenor grid from 1981 to 2026 shows smoother orthogonal parameter series than classical NSS parameters while the moving QR basis remains nearly constant.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes an orthogonal reparametrization of the Nelson-Siegel-Svensson (NSS) model via thin QR factorization of the design matrix (conditional on the nonlinear decay parameters) to resolve ill-conditioning from near-collinear basis functions. It derives a closed-form 4×4 continuous Gram matrix on [0,T] whose entries involve exponentials, logarithms, and the exponential integral E1, yielding an explicit horizon-dependent orthogonal basis. The approach supplies a scalar identifiability diagnostic (vanishing R44 on the λ1=λ2 manifold), an explicit Schur-complement expression for the joint covariance, and separates numerical conditioning from identifiability loss. Synthetic experiments and a daily U.S. Treasury study on a fixed 9-tenor grid (1981–2026) are used to illustrate that the reparametrized linear parameters exhibit zero conditional correlation, uniform uncertainty, and smoother time series while preserving the original fit and uncertainties.

Significance. If the algebraic derivations hold, the work supplies a practical, equivalence-preserving transformation that directly diagonalizes the conditional Fisher information for the linear block of NSS models, a widely used tool in fixed-income analytics. The closed-form orthogonal basis and R44 diagnostic offer concrete tools for both numerical stability and model-reduction decisions. The separation of conditioning artifacts from the genuine two-degree-of-freedom loss on λ1=λ2 is a useful clarification. The explicit Schur-complement covariance and reproducible synthetic/real-data illustrations are strengths that could improve the reliability of joint nonlinear estimation routines.

minor comments (4)

- [Abstract] Abstract: the statement that 'the moving QR basis remains nearly constant' is presented without a quantitative summary statistic (e.g., average Frobenius norm of day-to-day differences in the Q factor or condition-number trajectory); adding such a metric would strengthen the empirical claim.

- The continuous Gram-matrix derivation is asserted to be closed-form, yet the manuscript does not indicate whether the explicit expressions for the four diagonal and six off-diagonal entries (involving E1) are collected in an appendix or supplementary file; providing them would aid verification and implementation.

- Notation: the orthogonal linear parameters are referred to interchangeably as 'transformed' and 'orthogonal' without a single consistent symbol (e.g., β⊥ or βQR); introducing and using one symbol throughout would reduce reader confusion when comparing conditional covariances.

- The profile-likelihood and Jacobian-rank arguments for the λ1=λ2 degeneracy are invoked but not cross-referenced to the R44 diagnostic in a single location; a short dedicated subsection linking the three approaches would clarify their equivalence.

Simulated Author's Rebuttal

We thank the referee for the positive and accurate summary of our manuscript, which correctly highlights the QR orthogonal reparametrization, the closed-form continuous Gram matrix on [0,T], the R44 identifiability diagnostic, and the separation of conditioning from the λ1=λ2 degeneracy. The recommendation for minor revision is noted. As no specific major comments were provided, we have no points requiring response or revision.

Circularity Check

No significant circularity: reparametrization follows standard QR algebra

full rationale

The paper applies the thin QR factorization to the NSS design matrix conditional on the nonlinear parameters, which by the algebraic definition of the orthonormal Q factor produces a diagonal conditional Gram matrix (and thus Fisher information) without any fitted quantities or self-referential definitions. This is an equivalence transformation that preserves the original fit and uncertainties, and the identifiability diagnostics (R44 vanishing on λ1=λ2, Schur-complement covariance, closed-form continuous Gram matrix with E1) are direct consequences of the same orthogonalization plus standard Jacobian-rank and profile-likelihood arguments. No step reduces a claimed prediction or uniqueness result to its own inputs by construction, and there are no load-bearing self-citations or ansatzes smuggled in. The derivation is self-contained against external linear-algebra benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Thin QR decomposition exists and is unique up to sign for a full-column-rank design matrix

- domain assumption The NSS basis functions are the standard exponential forms with two decay rates

Reference graph

Works this paper leans on

-

[1]

Waggoner

D.F. Waggoner. Spline methods for extracting interest rate curves from coupon bond prices.Federal Reserve Bank of Atlanta Working Paper, No. 97–10, 1997

1997

-

[2]

Parsimoniousmodelingofyieldcurves.Journal of Business, 60(4):473–489,

C.R.NelsonandA.F.Siegel. Parsimoniousmodelingofyieldcurves.Journal of Business, 60(4):473–489,

-

[3]

Svensson

L.E.O. Svensson. Estimating and interpreting forward interest rates: Sweden 1992–1994.IMF Working Paper, WP/94/114, 1994

1992

-

[4]

Zero-coupon yield curves: Technical documentation.BIS Papers, No

Bank for International Settlements. Zero-coupon yield curves: Technical documentation.BIS Papers, No. 25, 2005

2005

-

[5]

Gürkaynak and Brian Sack and Jonathan H

R.S. Gürkaynak, B. Sack, and J.H. Wright. The U.S. Treasury yield curve: 1961 to the present.Journal of Monetary Economics, 54(8):2291–2304, 2007. doi:10.1016/j.jmoneco.2007.06.029

-

[6]

F.X. Diebold and G.S. Rudebusch.Yield Curve Modeling and Forecasting: The Dynamic Nelson–Siegel Approach. Princeton University Press, 2013. doi:10.1515/9781400845415

-

[7]

F.X. Diebold and C. Li. Forecasting the term structure of government bond yields.Journal of Econo- metrics, 130(2):337–364, 2006. doi:10.1016/j.jeconom.2005.03.005

-

[8]

G. Gauthier and J.-G. Simonato. Linearized Nelson–Siegel and Svensson models for the esti- mation of spot interest rates.European Journal of Operational Research, 219(2):442–451, 2012. doi:10.1016/j.ejor.2012.01.004

-

[9]

R. Gimeno and J.M. Nave. A genetic algorithm estimation of the term structure of interest rates. Computational Statistics & Data Analysis, 53(6):2236–2250, 2009. doi:10.1016/j.csda.2008.10.030

-

[10]

J. Annaert, A.G.P. Claes, M.J.K. De Ceuster, and H. Zhang. Estimating the spot rate curve using the Nelson–Siegel model: A ridge regression approach.International Review of Economics & Finance, 27:482–496, 2013. doi:10.1016/j.iref.2013.01.005

-

[11]

D. Banholzer, J. Fliege, and R. Werner. Revisiting the fitting of the Nelson–Siegel and Svensson models. Optimization, 73(10):3021–3053, 2024. doi:10.1080/02331934.2024.2389242. 26

-

[12]

De Pooter

M. De Pooter. Examining the Nelson–Siegel class of term structure models.Tinbergen Institute Dis- cussion Paper, No. 2007-043/4, 2007

2007

-

[13]

A.E. Hoerl and R.W. Kennard. Ridge regression: Biased estimation for nonorthogonal problems. Technometrics, 12(1):55–67, 1970. doi:10.1080/00401706.1970.10488634

-

[14]

D.J. Bolder and D. Stréliski. Yield curve modelling at the Bank of Canada.Bank of Canada Technical Report, No. 84, 1999. doi:10.34989/tr-84

-

[15]

Gilli, S

M. Gilli, S. Große, and E. Schumann. Calibrating the Nelson–Siegel–Svensson model.COMISEF Working Paper Series, No. WPS-031, 2010

2010

-

[16]

D.A. Belsley, E. Kuh, and R.E. Welsch.Regression Diagnostics: Identifying Influential Data and Sources of Collinearity. Wiley, New York, 1980. doi:10.1002/0471725153

-

[17]

G.H. Golub and V. Pereyra. The differentiation of pseudo-inverses and nonlinear least squares problems whose variables separate.SIAM Journal on Numerical Analysis, 10(2):413–432, 1973. doi:10.1137/0710036

-

[18]

G.H. Golub and V. Pereyra. Separable nonlinear least squares: The variable projection method and its applications.Inverse Problems, 19(2):R1–R26, 2003. doi:10.1088/0266-5611/19/2/201

-

[19]

A. Ruhe and P.-Å. Wedin. Algorithms for separable nonlinear least squares problems.SIAM Review, 22(3):318–337, 1980. doi:10.1137/1022057

-

[20]

L. Kaufman. A variable projection method for solving separable nonlinear least squares problems.BIT Numerical Mathematics, 15(1):49–57, 1975. doi:10.1007/BF01932995

-

[21]

D.P. O’Leary and B.W. Rust. Variable projection for nonlinear least squares problems.Computational Optimization and Applications, 54(3):579–593, 2013. doi:10.1007/s10589-012-9492-9

-

[22]

D.R. Cox and N. Reid. Parameter orthogonality and approximate conditional inference.Journal of the Royal Statistical Society: Series B, 49(1):1–18, 1987. doi:10.1111/j.2517-6161.1987.tb01422.x

-

[23]

D. Guterding. Sparse modeling approach to the arbitrage-free interpolation of plain-vanilla option prices and implied volatilities.Risks, 11(5):83, 2023. doi:10.3390/risks11050083

-

[24]

Stewart.Matrix Algorithms, Volume 1: Basic Decompositions

G.W. Stewart.Matrix Algorithms, Volume 1: Basic Decompositions. SIAM, Philadelphia, 1998. doi:10.1137/1.9781611971408

-

[25]

M. Melnichenko, R. Murray, W. Killian, J. Demmel, M.W. Mahoney, P. Luszczek, and M. Gates. Anatomy of high-performance column-pivoted QR decomposition. arXiv preprint arXiv:2507.00976,

-

[26]

doi:10.48550/arXiv.2507.00976

-

[27]

Accuracy and Stability of Numerical Algorithms (2nd ed.)

N.J. Higham.Accuracy and Stability of Numerical Algorithms. SIAM, Philadelphia, 2nd edition, 2002. doi:10.1137/1.9780898718027

-

[28]

T.J. Rothenberg. Identification in parametric models.Econometrica, 39(3):577–591, 1971. doi:10.2307/1913267

-

[29]

L. Ljung and S.T. Glad. On global identifiability for arbitrary model parametrizations.Automatica, 30(2):265–276, 1994. doi:10.1016/0005-1098(94)90029-9

-

[30]

E.A. Catchpole and B.J.T. Morgan. Detecting parameter redundancy.Biometrika, 84(1):187–196, 1997. doi:10.1093/biomet/84.1.187

-

[31]

A. Raue, C. Kreutz, T. Maiwald, J. Bachmann, M. Schilling, U. Klingmüller, and J. Timmer. Structural and practical identifiability analysis of partially observed dynamical models by exploiting the profile likelihood.Bioinformatics, 25(15):1923–1929, 2009. doi:10.1093/bioinformatics/btp358. 27

-

[32]

M.J. Simpson and O.J. Maclaren. Profile-Wise Analysis: A profile likelihood-based workflow for iden- tifiability analysis, estimation, and prediction with mechanistic mathematical models.PLOS Compu- tational Biology, 19(9):e1011515, 2023. doi:10.1371/journal.pcbi.1011515

-

[33]

The strong coupling constant: state of the art and the decade ahead,

M.I. Español and M. Pasha. Variable projection methods for separable nonlinear inverse problems with general-form Tikhonov regularization.Inverse Problems, 39(8):084002, 2023. doi:10.1088/1361- 6420/acdd1b

-

[34]

D.B. Comerso Salzer, M.I. Español, and G. Jeronimo. Variable projection methods for solving reg- ularized separable inverse problems with applications to semi-blind image deblurring. arXiv preprint arXiv:2601.05224, 2026. doi:10.48550/arXiv.2601.05224

-

[35]

M.I. Español and G. Jeronimo. Local convergence analysis of a variable projection method for reg- ularized separable nonlinear inverse problems.SIAM J. Matrix Anal. Appl., 46(2):858–878, 2025. doi:10.1137/24M1639087

-

[36]

G.H. Golub, M. Heath, and G. Wahba. Generalized cross-validation as a method for choosing a good ridge parameter.Technometrics, 21(2):215–223, 1979. doi:10.1080/00401706.1979.10489751

-

[37]

P.C. Bellec, J.-H. Du, T. Koriyama, P. Patil, and K. Tan. Corrected generalized cross-validation for finite ensembles of penalized estimators.J. R. Stat. Soc. Ser. B Stat. Methodol., 87(2):289–318, 2025. doi:10.1093/jrsssb/qkae092

-

[38]

P.C. Hansen. Analysis of discrete ill-posed problems by means of the L-curve.SIAM Review, 34(4):561– 580, 1992. doi:10.1137/1034115

-

[39]

S.D. Campbell, C. Li, and J. Im. Measuring agency MBS market liquidity with transaction data.FEDS Notes, Board of Governors of the Federal Reserve System, 2014. doi:10.17016/2380-7172.0007

-

[40]

Björck.Numerical Methods for Least Squares Problems

Å. Björck.Numerical Methods for Least Squares Problems. SIAM, Philadelphia, 1996. doi:10.1137/1.9781611971484

-

[41]

R. Litterman and J. Scheinkman. Common factors affecting bond returns.Journal of Fixed Income, 1(1):54–61, 1991. doi:10.3905/jfi.1991.692347

-

[42]

D. Guterding and W. Boenkost. The Heston stochastic volatility model with piecewise constant pa- rameters: efficient calibration and pricing of window barrier options.Journal of Computational and Applied Mathematics, 343:353–362, 2018. doi:10.1016/j.cam.2018.04.054

-

[43]

J.H.E. Christensen, F.X. Diebold, and G.D. Rudebusch. The affine arbitrage-free class of Nelson–Siegel term structure models.Journal of Econometrics, 164(1):4–20, 2011. doi:10.1016/j.jeconom.2011.02.011

-

[44]

J.F. Caldeira, W.C. Cordeiro, E. Ruiz, and A.A.P. Santos. Forecasting the yield curve: the role of additional and time-varying decay parameters, conditional heteroscedasticity, and macro-economic factors.J. Time Ser. Anal., 46(2):258–285, 2025. doi:10.1111/jtsa.12769

-

[45]

D.B. Resnik and M. Hosseini. Disclosing artificial intelligence use in scientific research and publica- tion: When should disclosure be mandatory, optional, or unnecessary?Accountability in Research, 33(2):2481949, 2026. doi:10.1080/08989621.2025.2481949. 28

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.