Recognition: unknown

The Anatomy of a Decentralized Prediction Market: Microstructure Evidence from the Polymarket Order Book

Pith reviewed 2026-05-07 17:04 UTC · model grok-4.3

The pith

Polymarket's public order-book feed infers the correct trade direction only about 59 percent of the time.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The paper establishes that trade direction inferred from Polymarket's public order-book feed agrees with on-chain ground truth only ~59% of the time (panel mean 0.615, 95% CI [0.58, 0.65]), barely above the 50% chance baseline. On a top-100 subset, effective half-spread changes sign between feed- and on-chain directions on 67% of markets in a first window and 50% in a second, while Kyle's lambda flips on 60% and 43% respectively. The public feed therefore recovers the on-chain sign at rates far below the ~80% achieved by the Lee-Ready algorithm on equity venues. The authors conclude that microstructure work on Polymarket requires sourcing trade direction from on-chain OrderFilled events and,

What carries the argument

The comparison and join of public WebSocket order-book feed data with on-chain OrderFilled events to validate trade direction inference and compute microstructure measures.

Load-bearing premise

The WebSocket order-book feed and on-chain trade records can be reliably joined without significant discrepancies or missing data, and the pre-registered stratified panel of 600 markets represents overall Polymarket behavior.

What would settle it

Replicating the analysis on a new sample of markets and finding that feed-inferred directions agree with on-chain records more than 70 percent of the time, or that microstructure measures maintain consistent signs across data sources.

Figures

read the original abstract

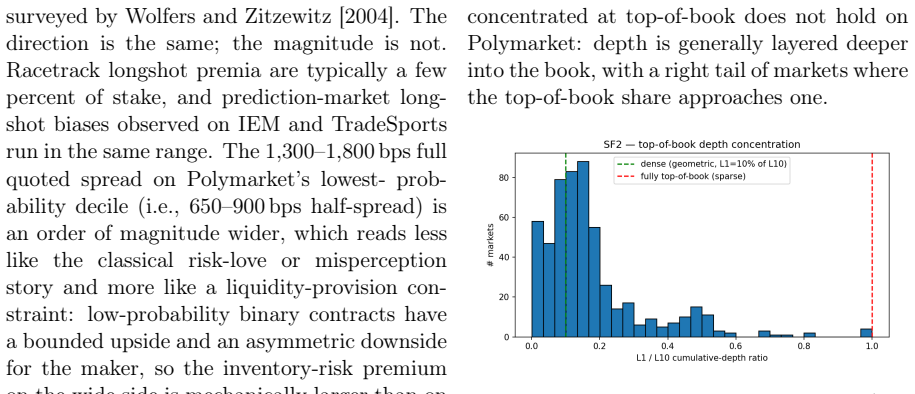

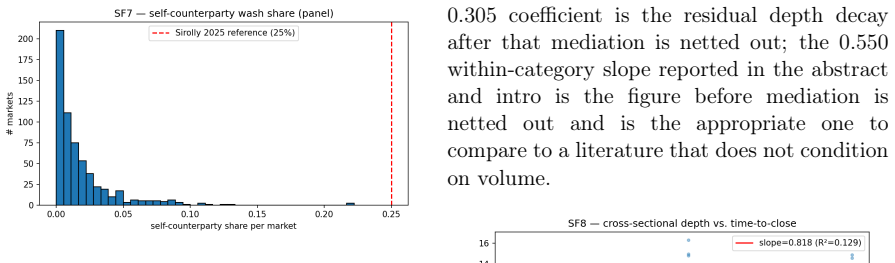

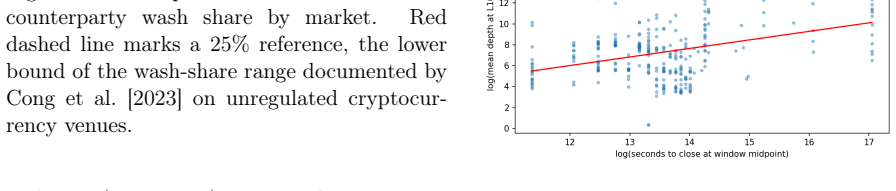

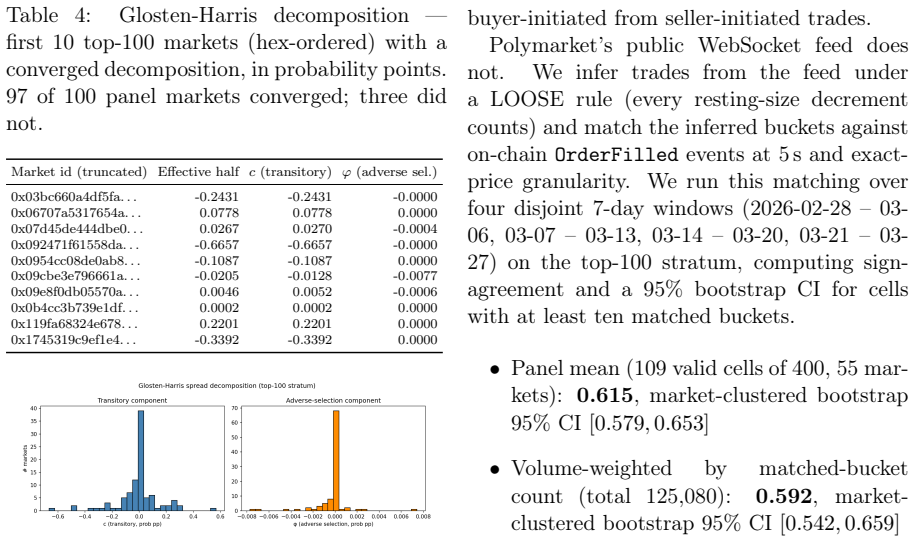

We study the microstructure of Polymarket, the largest on-chain prediction market, using a continuous tick-level archive of the public WebSocket order-book feed (30 billion events over 52 days) joined to the authoritative on-chain trade record. On a pre-registered stratified panel of 600 markets we report eight stylized facts: a longshot spread premium; a depth-concentration profile closer to a uniform geometric grid than to the top-of-book pattern often assumed for prediction markets; a null block-clock alignment effect; broad maker-wallet diversity with a concentrated tail; category-conditional differences in effective spread; a sub-50 ms median archive-ingestion delay with a multi-second tail; a self-counterparty wash share with median 1% and a 22% upper tail, well below the network-classifier benchmarks of Cong et al. (2023) for unregulated cryptocurrency token exchanges (a sanity bound, not an apples-to-apples reference, since the venues face different wash incentives); and a depth decay near resolution with a within-category slope of 0.55 on log seconds-to-close (t=3.85). The paper also contributes a measurement result: trade direction inferred from Polymarket's public order-book feed agrees with on-chain ground truth only ~59% of the time (panel mean 0.615, 95% CI [0.58, 0.65]), barely above the 50% chance baseline. On the comparable subset of the top-100 panel, the effective half-spread changes sign between feed- and on-chain directions on 67% of markets in a first 7-day window and 50% in a second non-overlapping window, with Kyle's lambda flipping on 60% and 43% respectively; neither window recovers the on-chain sign at anything close to the ~80% rate that Lee-Ready achieves on equity venues. Microstructure work on Polymarket therefore needs to source trade direction from on-chain OrderFilled events; we release a replication package that performs the join.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper examines the microstructure of Polymarket using a 30-billion-event WebSocket order-book archive joined to on-chain trade records over 52 days. On a pre-registered stratified panel of 600 markets it reports eight stylized facts (longshot spread premium, depth profile, null block-clock effect, maker diversity, category-conditional effective spreads, sub-50 ms median ingestion delay, low wash-trading share, and depth decay near resolution) and a central measurement result: trade direction inferred from the public order-book feed agrees with on-chain OrderFilled ground truth only ~59% of the time (panel mean 0.615, 95% CI [0.58, 0.65]). The authors conclude that microstructure work on Polymarket requires on-chain direction and release a replication package performing the join.

Significance. If the reported agreement rate and stylized facts hold, the paper supplies a large-scale, directly validated empirical baseline for decentralized prediction-market microstructure that is currently absent from the literature. The pre-registered panel, explicit join procedure, 30-billion-event scale, and released replication package are concrete strengths that lower the cost of follow-on work and allow direct falsification of the 59% benchmark.

minor comments (2)

- The abstract states that the wash-trading share is 'well below the network-classifier benchmarks of Cong et al. (2023)' but does not report the exact Cong et al. figure or the precise definition of 'self-counterparty wash' used in the join; a one-sentence clarification in §4 would remove ambiguity.

- Figure captions and table notes should explicitly state the exact number of markets and events underlying each panel statistic (e.g., 'N=600 markets, 1.2 billion matched trades') to allow readers to assess precision without returning to the text.

Simulated Author's Rebuttal

We thank the referee for their supportive review, detailed summary of the paper's contributions, and recommendation to accept. We are pleased that the pre-registered design, data scale, join procedure, and replication package were highlighted as strengths that facilitate follow-on work.

Circularity Check

No significant circularity

full rationale

The paper performs purely empirical measurements and reports descriptive stylized facts from raw data joins (WebSocket feed to on-chain OrderFilled events) on a pre-registered stratified panel. No equations, fitted parameters, derivations, or self-citations appear in the load-bearing claims; the key result (trade-direction agreement ~59%) is a direct empirical comparison to ground truth with reported CIs and released replication code. All eight stylized facts are data summaries without reduction to prior inputs by construction.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption The on-chain OrderFilled events provide the authoritative record of trades and their directions

- domain assumption The WebSocket feed captures all public order book events without significant loss

Reference graph

Works this paper leans on

-

[1]

High-frequency trading and price discovery

Jonathan Brogaard, Terrence Hendershott, and Ryan Riordan. High-frequency trading and price discovery. Review of Financial Studies, 27 0 (8): 0 2267--2306, 2014

2014

-

[2]

Crypto wash trading

Lin William Cong, Xi Li, Ke Tang, and Yang Yang. Crypto wash trading. Management Science, 69 0 (11): 0 6427--6454, 2023

2023

-

[3]

Philipp D. Dubach. Replication package: The anatomy of a decentralized prediction market, 2026. URL https://doi.org/10.5281/zenodo.19811426

-

[4]

The accuracy of trade classification rules: Evidence from nasdaq

Katrina Ellis, Roni Michaely, and Maureen O'Hara. The accuracy of trade classification rules: Evidence from nasdaq. Journal of Financial and Quantitative Analysis, 35 0 (4): 0 529--551, 2000

2000

-

[5]

Market Liquidity: Theory, Evidence, and Policy

Thierry Foucault, Marco Pagano, and Ailsa R \"o ell. Market Liquidity: Theory, Evidence, and Policy. Oxford University Press, 2013

2013

-

[6]

Glosten and Lawrence E

Lawrence R. Glosten and Lawrence E. Harris. Estimating the components of the bid/ask spread. Journal of Financial Economics, 21 0 (1): 0 123--142, 1988

1988

-

[7]

Logarithmic market scoring rules for modular combinatorial information aggregation

Robin Hanson. Logarithmic market scoring rules for modular combinatorial information aggregation. Journal of Prediction Markets, 1 0 (1): 0 3--15, 2007

2007

-

[8]

Empirical Market Microstructure: The Institutions, Economics, and Econometrics of Securities Trading

Joel Hasbrouck. Empirical Market Microstructure: The Institutions, Economics, and Econometrics of Securities Trading. Oxford University Press, 2007

2007

-

[9]

Huang and Hans R

Roger D. Huang and Hans R. Stoll. The components of the bid-ask spread: A general approach. Review of Financial Studies, 10 0 (4): 0 995--1034, 1997

1997

-

[10]

Charles M. C. Lee and Mark J. Ready. Inferring trade direction from intraday data. Journal of Finance, 46 0 (2): 0 733--746, 1991

1991

-

[11]

Why do security prices change? a transaction-level analysis of NYSE stocks

Ananth Madhavan, Matthew Richardson, and Mark Roomans. Why do security prices change? a transaction-level analysis of NYSE stocks. Review of Financial Studies, 10 0 (4): 0 1035--1064, 1997

1997

-

[12]

Charles F. Manski. Interpreting the predictions of prediction markets. Economics Letters, 91 0 (3): 0 425--429, 2006

2006

-

[13]

Market Microstructure Theory

Maureen O'Hara. Market Microstructure Theory. Blackwell Publishing, 1995

1995

-

[14]

Lionel Page and Robert T. Clemen. Do prediction markets produce well-calibrated probability forecasts? The Economic Journal, 123 0 (568): 0 491--513, 2013

2013

-

[15]

SoK : Market microstructure for decentralized prediction markets ( DePMs )

Nahid Rahman, Joseph Al-Chami, and Jeremy Clark. SoK : Market microstructure for decentralized prediction markets ( DePMs ). arXiv preprint arXiv:2510.15612, 2025. URL https://arxiv.org/abs/2510.15612

-

[16]

Explaining the favorite-long shot bias: Is it risk-love or misperceptions? Journal of Political Economy, 118 0 (4): 0 723--746, 2010

Erik Snowberg and Justin Wolfers. Explaining the favorite-long shot bias: Is it risk-love or misperceptions? Journal of Political Economy, 118 0 (4): 0 723--746, 2010

2010

-

[17]

Thaler and William T

Richard H. Thaler and William T. Ziemba. Anomalies: Parimutuel betting markets: Racetracks and lotteries. Journal of Economic Perspectives, 2 0 (2): 0 161--174, 1988

1988

-

[18]

The Anatomy of a Blockchain Prediction Market: Polymarket in the 2024 U.S. Presidential Election

Kwok Ping Tsang and Zichao Yang. The anatomy of Polymarket : Evidence from the 2024 presidential election. arXiv preprint arXiv:2603.03136, 2026. URL https://arxiv.org/abs/2603.03136

work page internal anchor Pith review arXiv 2024

-

[19]

Prediction markets

Justin Wolfers and Eric Zitzewitz. Prediction markets. Journal of Economic Perspectives, 18 0 (2): 0 107--126, 2004

2004

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.