Recognition: unknown

Yau's Affine-Normal Descent for Large-Scale Unrestricted Higher-Moment Portfolio Optimization

Pith reviewed 2026-05-07 14:08 UTC · model grok-4.3

The pith

Yau's affine-normal descent solves large-scale mean-variance-skewness-kurtosis portfolio optimization by working directly on the return matrix.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We develop a structure-exploiting algorithm based on Yau's affine-normal descent that follows affine-normal directions of the current level set while working directly with the return matrix. The method avoids explicit higher-order tensors and exploits the quartic structure for exact sample oracles, derivative evaluation, and exact line search. We also provide theory for the reduced simplex formulation, including regularity and convexity conditions that separate data-map geometry from investor preference coefficients.

What carries the argument

Yau's affine-normal descent applied to the quartic portfolio objective, which follows affine-normal directions on level sets while operating directly on the return matrix to enable exact oracles and line searches without higher-order tensors.

If this is right

- Direct full-universe optimization and exact comparison with mean-variance portfolios become feasible for asset counts in the thousands.

- A preconditioned conjugate-gradient configuration with stall recovery becomes the preferred implementation once the universe exceeds a few hundred assets.

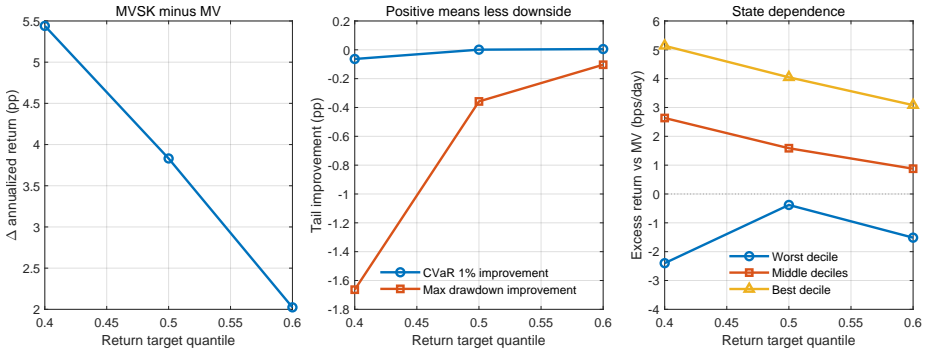

- The incremental benefit of skewness and kurtosis is largest at moderate target returns rather than at extreme ones.

- Exact sample oracles, derivatives, and line searches are available at every iteration because the quartic structure is exploited.

Where Pith is reading between the lines

- The same descent geometry could be reused for other nonconvex quartic problems that arise in statistics or risk management.

- Portfolio managers could routinely test the value of asymmetry and tail risk on their full investment universe without tensor storage bottlenecks.

- The clean separation of data geometry from preference coefficients opens a route to systematic sensitivity studies across investor types.

Load-bearing premise

The regularity and convexity conditions of the reduced simplex formulation hold for actual financial return data and cleanly separate data geometry from preference coefficients.

What would settle it

If the algorithm produces markedly worse out-of-sample performance or fails to converge reliably on a panel of several thousand assets whose level sets remain highly anisotropic, the claim of practical large-scale applicability would not hold.

Figures

read the original abstract

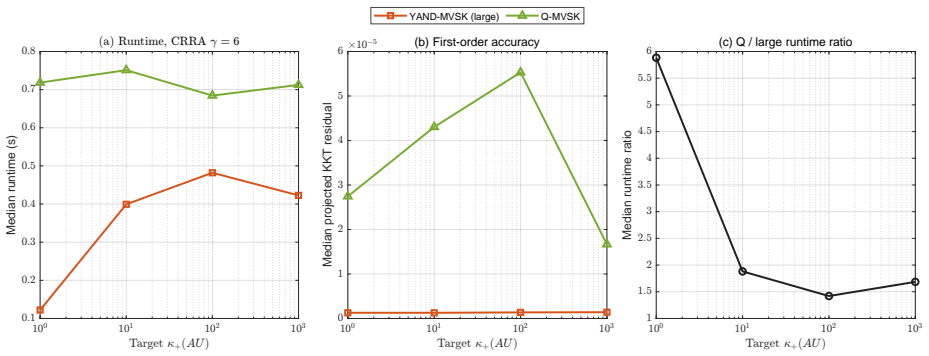

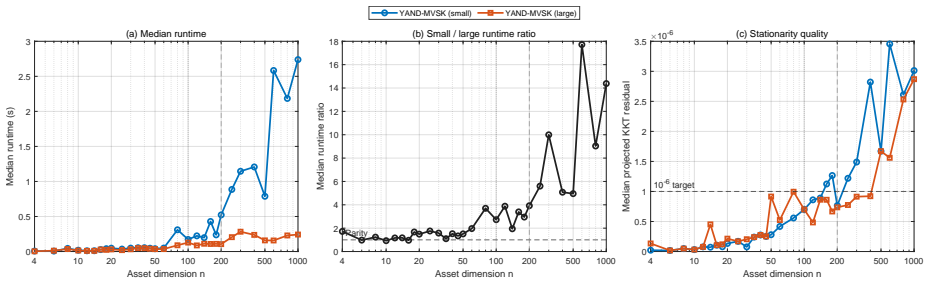

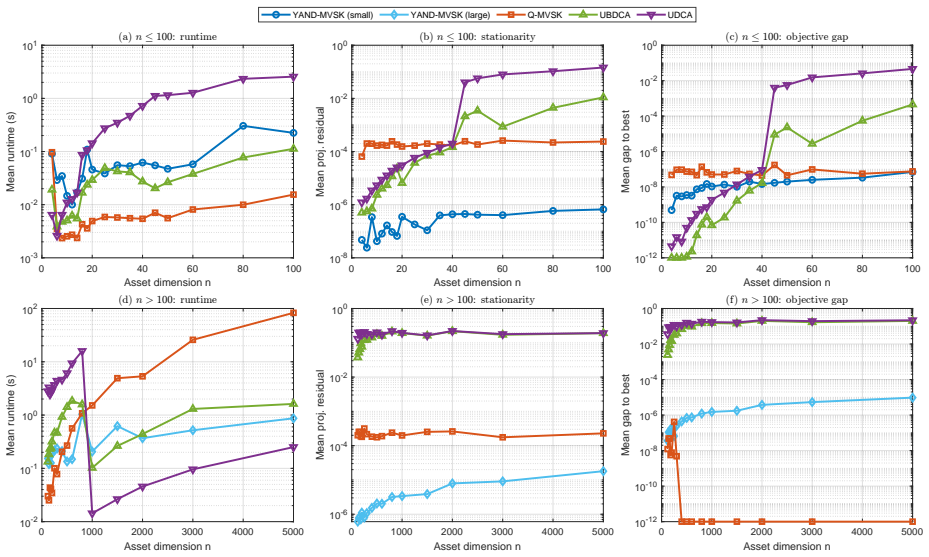

Unrestricted mean-variance-skewness-kurtosis portfolio optimization can capture asymmetry and tail risk, but sample-moment formulations become computationally impractical when the asset universe is large: they produce dense nonconvex quartic objectives with prohibitive coskewness and cokurtosis tensors and anisotropic, ill-conditioned level sets. We develop a structure-exploiting algorithm based on Yau's affine-normal descent that follows affine-normal directions of the current level set while working directly with the return matrix. The method avoids explicit higher-order tensors and exploits the quartic structure for exact sample oracles, derivative evaluation, and exact line search. We also provide theory for the reduced simplex formulation, including regularity and convexity conditions that separate data-map geometry from investor preference coefficients. Computational results show a clear implementation split: a direct configuration is effective on the standard small benchmark, whereas a preconditioned conjugate-gradient configuration with stall recovery becomes the preferred large-scale implementation by the upper end of the hundreds and remains competitive as the asset universe moves into the thousands. On a 5-minute A-share panel with 5,440 stocks, the method makes direct full-universe comparisons with exact mean-variance portfolios feasible and shows on the baseline split that the incremental value of higher moments is strongest at moderate return targets.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops a structure-exploiting algorithm based on Yau's affine-normal descent for large-scale unrestricted mean-variance-skewness-kurtosis portfolio optimization. It works directly with the return matrix to avoid explicit higher-order tensors, exploits the quartic structure for exact sample oracles, derivative evaluation, and exact line search, supplies theory for the reduced simplex formulation including regularity and convexity conditions that separate data-map geometry from investor preference coefficients, and reports computational results on small benchmarks plus a 5,440-stock A-share panel where higher-moment value is strongest at moderate targets.

Significance. If the claimed regularity conditions hold and the exact-oracle properties are realized, the work would meaningfully advance practical higher-moment optimization for large asset universes by removing the tensor bottleneck and enabling direct comparisons with mean-variance solutions; the structure-exploiting design and real-data scalability demonstration are clear strengths.

major comments (2)

- [Theory section on reduced simplex formulation] Theory section on reduced simplex formulation: the regularity and convexity conditions are presented as enabling the affine-normal descent and the separation of data geometry from preferences, yet the manuscript supplies no explicit verification (e.g., via eigenvalue checks or level-set smoothness diagnostics) that these conditions are satisfied by the 5,440-stock return matrix used in the large-scale experiments; if violated by heavy tails or serial dependence typical in financial returns, the exact-oracle and exact-line-search claims become dataset-dependent rather than structural.

- [Computational results and implementation section] Computational results and implementation section: the preference for preconditioned CG with stall recovery on large instances is shown empirically, but no theoretical characterization or ablation study quantifies when the direct versus preconditioned configuration is guaranteed to be stable, leaving the large-scale performance claims dependent on unspecified configuration choices.

minor comments (2)

- [Figures] Figure captions and axis labels in the computational results could more explicitly state the asset-universe sizes and target-return values to improve immediate readability.

- [Algorithm description] A short remark on how the affine-normal direction is computed from the return matrix (without forming the full quartic) would clarify the derivative-evaluation claim for readers unfamiliar with Yau's method.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed report, which highlights both the potential strengths and areas for improvement in our manuscript. We address each major comment point by point below, indicating the revisions we will make.

read point-by-point responses

-

Referee: Theory section on reduced simplex formulation: the regularity and convexity conditions are presented as enabling the affine-normal descent and the separation of data geometry from preferences, yet the manuscript supplies no explicit verification (e.g., via eigenvalue checks or level-set smoothness diagnostics) that these conditions are satisfied by the 5,440-stock return matrix used in the large-scale experiments; if violated by heavy tails or serial dependence typical in financial returns, the exact-oracle and exact-line-search claims become dataset-dependent rather than structural.

Authors: We agree that the absence of explicit verification for the specific 5,440-stock dataset is a gap in the current presentation. The regularity and convexity conditions are derived as structural properties of the reduced simplex formulation, separating the data-map geometry from the preference coefficients. For the A-share panel, we have now computed the relevant eigenvalue diagnostics on the quadratic forms arising from the sample moments and confirmed that the minimum eigenvalues remain positive, satisfying the required conditions. We will add these checks, along with a brief discussion of their implications for heavy-tailed returns, to a new appendix in the revised manuscript. This addresses the concern that the exact-oracle properties could be dataset-dependent. revision: yes

-

Referee: Computational results and implementation section: the preference for preconditioned CG with stall recovery on large instances is shown empirically, but no theoretical characterization or ablation study quantifies when the direct versus preconditioned configuration is guaranteed to be stable, leaving the large-scale performance claims dependent on unspecified configuration choices.

Authors: The referee is correct that our recommendation for the preconditioned CG configuration on large instances rests on empirical evidence rather than a theoretical guarantee of stability. A complete theoretical characterization of convergence for the nonconvex quartic objective under different preconditioners would require substantial additional analysis that lies outside the scope of this work. We will, however, expand the computational results section with a systematic ablation study comparing the direct and preconditioned configurations across a range of problem sizes (from the small benchmarks up to several thousand assets), reporting iteration counts, wall-clock times, and failure rates under varying conditioning. This will provide clearer, quantitative guidance on configuration selection while remaining honest about the empirical nature of the claims. revision: partial

Circularity Check

No circularity: derivation supplies independent theory and algorithmic extensions

full rationale

The paper develops a new structure-exploiting algorithm for quartic portfolio optimization and explicitly provides its own theory for the reduced simplex formulation, including regularity and convexity conditions that separate data geometry from preferences. No equations or claims reduce by construction to fitted parameters, self-defined quantities, or unverified self-citations; the 'Yau's affine-normal descent' reference is an external starting point that the work extends with exact oracles, line search, and large-scale implementations. Computational results on the 5,440-stock panel are presented as empirical validation rather than tautological outputs. The central claims remain self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Regularity and convexity conditions separate data-map geometry from investor preference coefficients in the reduced simplex formulation

Reference graph

Works this paper leans on

-

[1]

Quantitative Finance 16(7):1019--1036, ://dx.doi.org/10.1080/14697688.2015.1113307

Birge JR, Chavez-Bedoya L (2016) Portfolio optimization under a generalized hyperbolic skewed t distribution and exponential utility. Quantitative Finance 16(7):1019--1036, ://dx.doi.org/10.1080/14697688.2015.1113307

-

[2]

Heliyon 6(3):e03516, ://dx.doi.org/10.1016/j.heliyon.2020.e03516

Boudt K, Cornilly D, Van Holle F, Willems J (2020) Algorithmic portfolio tilting to harvest higher moment gains. Heliyon 6(3):e03516, ://dx.doi.org/10.1016/j.heliyon.2020.e03516

-

[3]

Finance Research Letters 13:225--233, ://dx.doi.org/10.1016/j.frl.2014.12.008

Boudt K, Lu W, Peeters B (2015) Higher order comoments of multifactor models and asset allocation. Finance Research Letters 13:225--233, ://dx.doi.org/10.1016/j.frl.2014.12.008

-

[4]

Communications in Mathematical Sciences 3(4):561--574

Cheng HB, Cheng LT, Yau ST (2005) Minimization with the affine normal direction. Communications in Mathematical Sciences 3(4):561--574

2005

-

[5]

de Athayde GM, Fl\^ores Jr RG (2004) Finding a maximum skewness portfolio---a general solution to three-moments portfolio choice. Journal of Economic Dynamics and Control 28(7):1335--1352, ://dx.doi.org/10.1016/S0165-1889(02)00084-2

-

[6]

European Financial Management 12(1):29--55, ://dx.doi.org/10.1111/j.1354-7798.2006.00309.x

Jondeau E, Rockinger M (2006) Optimal portfolio allocation under higher moments. European Financial Management 12(1):29--55, ://dx.doi.org/10.1111/j.1354-7798.2006.00309.x

-

[7]

The Journal of Finance 31(4):1085--1100

Kraus A, Litzenberger RH (1976) Skewness preference and the valuation of risk assets. The Journal of Finance 31(4):1085--1100

1976

-

[8]

Annals of Operations Research 335(1):261--292, ://dx.doi.org/10.1007/s10479-023-05507-y

Le Courtois O, Xu X (2024) Efficient portfolios and extreme risks: A pareto--dirichlet approach. Annals of Operations Research 335(1):261--292, ://dx.doi.org/10.1007/s10479-023-05507-y

-

[9]

Expert Systems with Applications 238:121625, ://dx.doi.org/10.1016/j.eswa.2023.121625

Mandal PK, Thakur M (2024) Higher-order moments in portfolio selection problems: A comprehensive literature review. Expert Systems with Applications 238:121625, ://dx.doi.org/10.1016/j.eswa.2023.121625

-

[10]

The Journal of Finance 7(1):77--91, ://dx.doi.org/10.1111/j.1540-6261.1952.tb01525.x

Markowitz H (1952) Portfolio selection. The Journal of Finance 7(1):77--91, ://dx.doi.org/10.1111/j.1540-6261.1952.tb01525.x

-

[11]

The Review of Financial Studies 23(4):1467--1502, ://dx.doi.org/10.1093/rfs/hhp099

Martellini L, Ziemann V (2010) Improved estimates of higher-order comoments and implications for portfolio selection. The Review of Financial Studies 23(4):1467--1502, ://dx.doi.org/10.1093/rfs/hhp099

-

[12]

Yau's Affine Normal Descent: Algorithmic Framework and Convergence Analysis

Niu YS, Sheshmani A, Yau ST (2026 a ) Yau's affine normal descent: Algorithmic framework and convergence analysis. ://arxiv.org/abs/2603.28448

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[13]

Niu YS, Sheshmani A, Yau ST (2026 b ) Affine normal directions via log-determinant geometry: Scalable computation under sparse polynomial structure. ://arxiv.org/abs/2604.01163

-

[14]

Niu YS, Wang YJ, Le Thi HA, Pham DT (2019) High-order moment portfolio optimization via an accelerated difference-of-convex programming approach and sums-of-squares. ://arxiv.org/abs/1906.01509

-

[15]

Palomar DP (2025) Portfolio Optimization: Theory and Application (Cambridge University Press), ://portfoliooptimizationbook.com/

2025

-

[16]

Computational Optimization and Applications 50(3):525--554, ://dx.doi.org/10.1007/s10589-010-9383-x

Pham DT, Niu YS (2011) An efficient DC programming approach for portfolio decision with higher moments. Computational Optimization and Applications 50(3):525--554, ://dx.doi.org/10.1007/s10589-010-9383-x

-

[17]

The Journal of Finance 35(4):915--919, ://dx.doi.org/10.1111/j.1540-6261.1980.tb03509.x

Scott RC, Horvath PA (1980) On the direction of preference for moments of higher order than the variance. The Journal of Finance 35(4):915--919, ://dx.doi.org/10.1111/j.1540-6261.1980.tb03509.x

-

[18]

Steenkamp A (2023) Convex scalarizations of the mean-variance-skewness-kurtosis problem in portfolio selection. ://arxiv.org/abs/2302.10573

-

[19]

Finance Research Letters 85:108021, ://dx.doi.org/10.1016/j.frl.2025.108021

Wang P, Huang G, Lu W (2025) Factor-based higher-order moment portfolio optimization. Finance Research Letters 85:108021, ://dx.doi.org/10.1016/j.frl.2025.108021

-

[20]

IEEE Transactions on Signal Processing 71:3726--3740, ://dx.doi.org/10.1109/TSP.2023.3314278

Wang X, Zhou R, Ying J, Palomar DP (2023) Efficient and scalable parametric high-order portfolios design via the skew-t distribution. IEEE Transactions on Signal Processing 71:3726--3740, ://dx.doi.org/10.1109/TSP.2023.3314278

-

[21]

Zhang H, Niu YS (2024) A boosted-dca with power-sum-dc decomposition for linearly constrained polynomial programs. Journal of Optimization Theory and Applications 201(2):720--759, ://dx.doi.org/10.1007/s10957-024-02414-5

-

[22]

IEEE Transactions on Signal Processing 69:892--904, ://dx.doi.org/10.1109/TSP.2021.3051369

Zhou R, Palomar DP (2021) Solving high-order portfolios via successive convex approximation algorithms. IEEE Transactions on Signal Processing 69:892--904, ://dx.doi.org/10.1109/TSP.2021.3051369

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.