Recognition: no theorem link

Statistical Model Checking of the Keynes+Schumpeter Model: A Transient Sensitivity Analysis of a Macroeconomic ABM

Pith reviewed 2026-05-12 04:40 UTC · model grok-4.3

The pith

Statistical model checking delivers reproducible transient sensitivity analysis for the Keynes-Schumpeter macroeconomic agent-based model.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

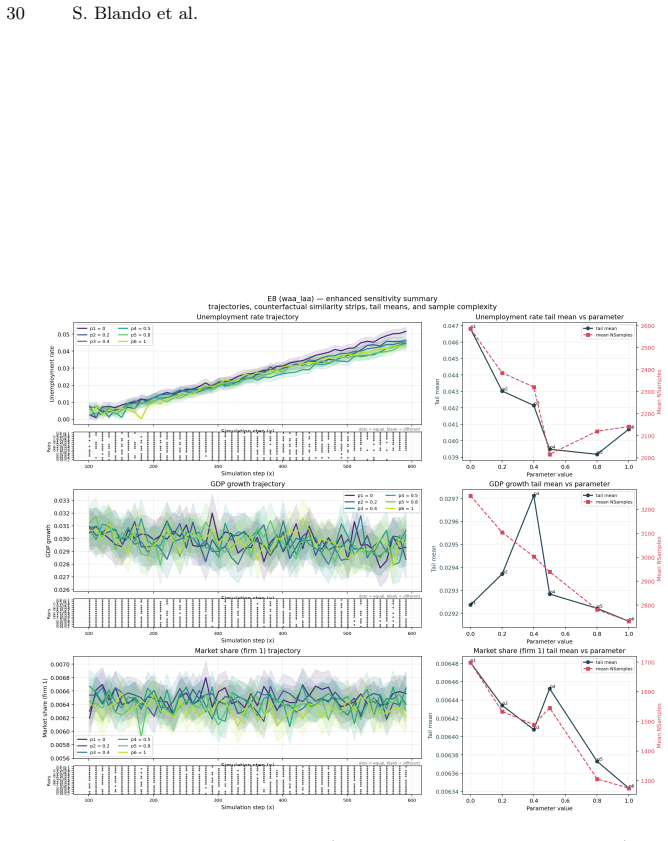

Statistical model checking supports quantitative transient sensitivity analysis of the Keynes+Schumpeter model by driving simulation runs with temporal queries, precision targets, and automatic stopping rules that adapt effort to each parameter setting and observable. Across the tested sweeps the method identifies clear differences: macro-financial and structural parameters produce the strongest short-term changes in unemployment and GDP growth, whereas heuristic-rule parameters yield comparatively muted transients under identical statistical guarantees.

What carries the argument

Statistical model checking driven by reusable temporal queries, observable-specific precision targets, and confidence-based stopping rules applied to the post-warmup phase of the heuristic-switching Keynes+Schumpeter agent-based simulator.

If this is right

- Macro-financial and structural parameter sweeps produce stronger transient effects on unemployment and GDP growth than heuristic-rule sweeps under the same precision policy.

- Uncertainty estimates and the simulation effort required become explicit and comparable across all tested configurations.

- Analysis of substantively rich economic agent-based models can proceed without rewriting the simulator in a dedicated formal language.

- Transient rather than steady-state focus yields new distinctions among parameter families that steady-state Monte Carlo campaigns can miss.

Where Pith is reading between the lines

- The same query-and-precision framework could be reused on other macroeconomic agent-based models to produce comparable sensitivity rankings.

- Policy-relevant short-term fluctuation analysis could be strengthened by systematically varying the post-warmup horizon length to test persistence of the reported contrasts.

- Market-share micro-probes could be expanded to additional firm-level statistics to check whether the macro contrasts are accompanied by consistent micro-level shifts.

Load-bearing premise

The selected temporal queries, precision targets, and 600-step post-warmup window are sufficient to capture the relevant transient dynamics of the model.

What would settle it

A finding that extending the simulation horizon beyond 600 steps or altering the precision targets reverses the ranking of which parameter families produce the strongest transients would show that the chosen analysis window misses important behavior.

Figures

read the original abstract

Agent-based models (ABMs) are increasingly used in macroeconomics, but their analysis still often relies on ad hoc Monte Carlo campaigns with heterogeneous statistical effort across parameter settings. We show how statistical model checking (SMC), implemented through MultiVeStA, can provide a principled analysis layer for a realistic macroeconomic ABM without rewriting the simulator in a dedicated formalism. Our case study is the heuristic-switching Keynes+Schumpeter(K+S) model, analysed hrough a transient sensitivity campaign over one-parameter sweeps, two macro observables (unemployment and GDP growth), and one auxiliary micro-level probe (market share) on the post-warmup phase of a 600-step horizon. The analysis is driven by reusable temporal queries, observable-specific precision targets, and confidence-based stopping rules that automatically determine the simulation effort required by each configuration. Results show a clear contrast across parameter families: macro-financial and structural sweeps produce the strongest transient effects, whereas several heuristic-rule sweeps remain much weaker under the same precision policy. More broadly, the paper shows that SMC can support reproducible and informative quantitative analysis of substantively rich economic ABMs, while making uncertainty estimates and simulation cost explicit parts of the reported results.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript presents an application of statistical model checking (SMC) using the MultiVeStA tool to analyze the transient dynamics of the Keynes+Schumpeter (K+S) agent-based macroeconomic model. Through one-parameter sweeps on macro-financial, structural, and heuristic parameters, it examines sensitivity of unemployment, GDP growth, and market share over a fixed 600-step post-warmup horizon using temporal queries with precision targets and confidence-based stopping rules. The key finding is a contrast in the strength of transient effects across parameter families, with macro-financial and structural sweeps showing stronger effects than heuristic-rule sweeps. The paper argues that this approach enables reproducible quantitative analysis of rich ABMs while explicitly accounting for uncertainty and computational cost.

Significance. If the results hold, this work is significant in demonstrating how SMC can be integrated with existing ABM simulators without requiring a dedicated formal language, addressing the common issue of ad hoc Monte Carlo analyses in macroeconomic ABMs. It provides a method that makes simulation effort and statistical confidence explicit, which could improve reproducibility in the field. The contrast in results across parameter types offers substantive insight into the model's behavior, though its robustness depends on the adequacy of the chosen analysis horizon.

major comments (1)

- Abstract: the analysis is described as covering the 'post-warmup phase of a 600-step horizon' with no mention of convergence diagnostics, comparison to longer runs, or analysis of the model's characteristic timescales. This choice is load-bearing for the central claim, as truncation bias in regimes where transients extend beyond 600 steps could artifactually produce the reported contrasts between macro-financial/structural and heuristic-rule parameter families.

minor comments (1)

- The abstract refers to 'reusable temporal queries' and 'observable-specific precision targets' without specifying their exact formulations or how MultiVeStA integration preserves the original model dynamics; adding these details would strengthen reproducibility claims.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed review. We address the single major comment below and outline revisions that will strengthen the manuscript while preserving the integrity of the reported analysis.

read point-by-point responses

-

Referee: [—] Abstract: the analysis is described as covering the 'post-warmup phase of a 600-step horizon' with no mention of convergence diagnostics, comparison to longer runs, or analysis of the model's characteristic timescales. This choice is load-bearing for the central claim, as truncation bias in regimes where transients extend beyond 600 steps could artifactually produce the reported contrasts between macro-financial/structural and heuristic-rule parameter families.

Authors: We acknowledge that the abstract and main text do not explicitly discuss convergence diagnostics or comparisons to longer horizons. The 600-step post-warmup window was selected to isolate transient dynamics, consistent with the simulation lengths used in prior K+S studies for capturing short-to-medium-term macroeconomic adjustments. Although formal convergence checks and extended runs are absent from the current manuscript, the SMC procedure applies identical precision targets and stopping rules across all parameter sweeps, ensuring that the reported contrasts reflect statistically controlled differences within the studied interval rather than uncontrolled Monte Carlo variation. The relative weakness of heuristic-rule effects is therefore observed under uniform conditions. We will revise the abstract to note the horizon's grounding in the model's established timescales and add a concise methods subsection (or discussion paragraph) that (i) references the characteristic adjustment periods from the K+S literature, (ii) states the absence of explicit truncation diagnostics as a limitation, and (iii) clarifies that future extensions could test longer horizons. These textual changes will make the analysis more transparent without requiring re-execution of the existing SMC campaigns. revision: yes

Circularity Check

No significant circularity; empirical application of external tool

full rationale

The paper applies statistical model checking via the external MultiVeStA tool to an existing macroeconomic ABM for transient sensitivity analysis over parameter sweeps. All results derive from simulation outputs and reusable temporal queries with confidence-based stopping rules rather than any derivations, equations, or fitted parameters that reduce to inputs by construction. No self-definitional steps, predictions forced by fits, or load-bearing self-citations appear in the described chain; the 600-step horizon is a fixed methodological parameter, not a circular element.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The K+S model implementation faithfully represents the intended macroeconomic dynamics.

Reference graph

Works this paper leans on

-

[1]

ACM Transactions on Modeling and Computer Simulation28(1), 1–39 (2018)

Agha, G., Palmskog, K.: A survey of statistical model checking. ACM Transactions on Modeling and Computer Simulation28(1), 1–39 (2018). https://doi.org/10. 1145/3158668

work page 2018

-

[2]

Econo- metrica60(2), 323–351 (1992)

Aghion, P., Howitt, P.: A model of growth through creative destruction. Econo- metrica60(2), 323–351 (1992). https://doi.org/10.2307/2951599

-

[3]

American Economic Journal: Microeconomics4(4), 35–64 (2012)

Anufriev, M., Hommes, C.: Evolutionary selection of individual expectations and aggregate outcomes in asset pricing experiments. American Economic Journal: Microeconomics4(4), 35–64 (2012). https://doi.org/10.1257/mic.4.4.35, https:// www.aeaweb.org/articles?id=10.1257/mic.4.4.35

-

[4]

Journal of Evolutionary Eco- nomics23(3), 663–688 (2013)

Anufriev, M., Hommes, C.H., Philipse, R.H.S.: Evolutionary selection of expec- tations in positive and negative feedback markets. Journal of Evolutionary Eco- nomics23(3), 663–688 (2013). https://doi.org/10.1007/s00191-011-0242-4, https: //doi.org/10.1007/s00191-011-0242-4

-

[5]

The Review of Eco- nomic Studies29(3), 155–173 (1962)

Arrow, K.J.: The economic implications of learning by doing. The Review of Eco- nomic Studies29(3), 155–173 (1962). https://doi.org/10.2307/2295952

-

[6]

Baier, C., Katoen, J.: Principles of model checking. MIT Press (2008). https://doi. org/10.1093/comjnl/bxp025

-

[7]

In: Proceedings of MARS@ETAPS 2026 (2026)

Blando, S., Fagiolo, G., Giachini, D., Vandin, A., Ivanaj, E.: Statistical model checking of the island model: An established economic agent-based model of en- dogenous growth. In: Proceedings of MARS@ETAPS 2026 (2026). https://doi.org/ 10.4204/EPTCS.443.2

-

[8]

Econo- metrica65(5), 1059–1095 (1997)

Brock, W.A., Hommes, C.H.: A rational route to randomness. Econo- metrica65(5), 1059–1095 (1997). https://doi.org/10.2307/2171879, https://www.econometricsociety.org/publications/econometrica/1997/09/01/ rational-route-randomness

-

[9]

Journal of Economic Dynamics and Control69, 375–408 (2016)

Caiani, A., Godin, A., Caverzasi, E., Gallegati, M., Kinsella, S., Stiglitz, J.E.: Agent based-stock flow consistent macroeconomics: Towards a benchmark model. Journal of Economic Dynamics and Control69, 375–408 (2016). https://doi.org/ 10.1016/j.jedc.2016.06.001

-

[10]

https://doi.org/10.1007/s40821-019-00121-0

Capone, G., Malerba, F., Nelson, R.R., Orsenigo, L., Winter, S.G.: History friendly models:retrospectiveandfutureperspectives.EurasianBusinessReview9(1),1–23 (March 2019). https://doi.org/10.1007/s40821-019-00121-0

-

[11]

MIT Press (2018), https://mitpress.mit.edu/books/ model-checking-second-edition

Clarke, E.M., Grumberg, O., Kroening, D., Peled, D.A., Veith, H.: Model checking, 2nd Edition. MIT Press (2018), https://mitpress.mit.edu/books/ model-checking-second-edition

work page 2018

-

[12]

In: Handbook of Compu- tational Economics, vol

Dawid, H., Gatti, D.D.: Agent-based macroeconomics. In: Handbook of Compu- tational Economics, vol. 4, pp. 63–156. Elsevier (2018). https://doi.org/10.2139/ ssrn.3112074

work page 2018

-

[13]

Journal of Economic Dy- namics and Control37(8), 1598–1625 (2013)

Dosi, G., Fagiolo, G., Napoletano, M., Roventini, A.: Income distribution, credit and fiscal policies in an agent-based Keynesian model. Journal of Economic Dy- namics and Control37(8), 1598–1625 (2013). https://doi.org/10.1016/j.jedc.2012. 11.008

-

[14]

Journal of Economic Dynamics and Control52, 166–189 (2015)

Dosi, G., Fagiolo, G., Napoletano, M., Roventini, A., Treibich, T.: Fiscal and mon- etary policies in complex evolving economies. Journal of Economic Dynamics and Control52, 166–189 (2015). https://doi.org/10.1016/j.jedc.2014.11.014

-

[15]

Journal of Economic Dynamics and Control34(9), 1748–1767 (2010)

Dosi, G., Fagiolo, G., Roventini, A.: Schumpeter meeting keynes: A policy-friendly model of endogenous growth and business cycles. Journal of Economic Dynamics and Control34(9), 1748–1767 (2010). https://doi.org/10.1016/j.jedc.2010.06.018 18 S. Blando et al

-

[16]

Economic Inquiry58(3), 1487–1516 (2020)

Dosi, G., Napoletano, M., Roventini, A., Stiglitz, J.E., Treibich, T.: Rational heuristics? expectations and behaviors in evolving economies with heterogeneous interacting agents. Economic Inquiry58(3), 1487–1516 (2020). https://doi.org/10. 1111/ecin.12897

work page 2020

-

[17]

Journal of Evolutionary Economics 27(1), 63–90 (2017)

Dosi, G., Napoletano, M., Roventini, A., Treibich, T.: Micro and macro policies in the keynes+schumpeter evolutionary models. Journal of Evolutionary Economics 27(1), 63–90 (2017). https://doi.org/10.1007/s00191-016-0466-4

-

[18]

https://doi.org/10.1007/s11403-019-00258-1, https://doi.org/ 10.1007/s11403-019-00258-1

Fagiolo, G., Giachini, D., Roventini, A.: Innovation, finance, and economic growth: anagent-basedapproach.JournalofEconomicInteractionandCoordination15(3), 703–736 (Jul 2020). https://doi.org/10.1007/s11403-019-00258-1, https://doi.org/ 10.1007/s11403-019-00258-1

-

[19]

In: Computer Simulation Validation, pp

Fagiolo, G., Guerini, M., Lamperti, F., Moneta, A., Roventini, A.: Validation of agent-based models in economics and finance. In: Computer Simulation Validation, pp. 763–787. Springer (2019). https://doi.org/10.1007/978-3-319-70766-2_31

-

[20]

Computational Economics30(3), 195–226 (2007)

Fagiolo, G., Moneta, A., Windrum, P.: A critical guide to empirical validation of agent-based models in economics: Methodologies, procedures, and open prob- lems. Computational Economics30(3), 195–226 (2007). https://doi.org/10.1007/ s10614-007-9104-4

work page 2007

-

[21]

Journal of Artificial Societies and Social Simulation20(1), 1 (2017)

Fagiolo, G., Roventini, A.: Macroeconomic policy in DSGE and agent-based models redux: New developments and challenges ahead. Journal of Artificial Societies and Social Simulation20(1), 1 (2017). https://doi.org/10.18564/jasss.3280

-

[22]

Farmer, J.D., Foley, D.: The economy needs agent-based modelling. Nature 460(7256), 685–686 (2009). https://doi.org/10.1038/460685a

-

[23]

Gilmore, S., Reijsbergen, D., Vandin, A.: Transient and steady-state statistical analysis for discrete event simulators. In: Integrated Formal Methods - 13th In- ternational Conference, IFM 2017, Turin, Italy, September 20-22, 2017, Proceed- ings. pp. 145–160 (2017). https://doi.org/10.1007/978-3-319-66845-1\_10, https: //doi.org/10.1007/978-3-319-66845-1_10

-

[24]

Gilmore, S., Tribastone, M., Vandin, A.: An analysis pathway for the quantitative evaluation of public transport systems. In: Albert, E., Sekerinski, E. (eds.) Inte- grated Formal Methods - 11th International Conference, IFM 2014, Bertinoro, Italy, September 9-11, 2014, Proceedings. Lecture Notes in Computer Science, vol.8739,pp.71–86.Springer(2014).https...

-

[25]

Backpropagation through time and the brain.Current Opinion in Neurobiology, 55:82–89, 2019

Guerini, M., Moneta, A.: A method for agent-based models validation. Journal of Economic Dynamics and Control82, 125–141 (2017). https://doi.org/10.1016/j. jedc.2017.06.001

work page doi:10.1016/j 2017

-

[26]

Journal of Economic Dynamics and Control33(5), 1052–1072 (2009)

Heemeijer, P., Hommes, C., Sonnemans, J., Tuinstra, J.: Price stability and volatil- ity in markets with positive and negative expectations feedback: An experimen- tal investigation. Journal of Economic Dynamics and Control33(5), 1052–1072 (2009). https://doi.org/10.1016/j.jedc.2008.09.009, https://doi.org/10.1016/j.jedc. 2008.09.009

-

[27]

Journal of Economic Dynamics and Control35(1), 1–24 (2011)

Hommes, C.: The heterogeneous expectations hypothesis: Some evidence from the lab. Journal of Economic Dynamics and Control35(1), 1–24 (2011). https://doi. org/10.1016/j.jedc.2010.10.003, https://doi.org/10.1016/j.jedc.2010.10.003

-

[28]

In: Hand- book of Computational Economics, vol

Hommes, C.H.: Heterogeneous agent models in economics and finance. In: Hand- book of Computational Economics, vol. 2, pp. 1109–1186. Elsevier (2006). https: //doi.org/10.1016/s1574-0021(05)02023-x

-

[29]

Kirman, A.: Complex Economics: Individual and Collective Rationality. Routledge, London (2011). https://doi.org/10.23941/ejpe.v4i2.81 Statistical Model Checking of the K+S Model 19

-

[30]

Journal of Economic Dynamics and Control90, 366–389 (2018)

Lamperti, F., Roventini, A., Sani, A.: Agent-based model calibration using ma- chine learning surrogates. Journal of Economic Dynamics and Control90, 366–389 (2018). https://doi.org/10.1016/j.jedc.2018.03.011

-

[31]

Journal of Artificial Societies and Social Simulation18(4), 4 (2015)

Lee, J.S., Filatova, T., Ligmann-Zielinska, A., Hassani-Mahmooei, B., Stonedahl, F., Lorscheid, I., Voinov, A., Polhill, J.G., Sun, Z., Parker, D.C.: The complexities of agent-based modeling output analysis. Journal of Artificial Societies and Social Simulation18(4), 4 (2015). https://doi.org/10.18564/jasss.2897

-

[32]

In: Runtime Verification (RV 2010)

Legay, A., Delahaye, B., Bensalem, S.: Statistical model checking: An overview. In: Runtime Verification (RV 2010). LNCS, vol. 6418, pp. 122–135. Springer (2010). https://doi.org/10.1007/978-3-642-16612-9_11

-

[33]

Harvard University Press, Cambridge, MA (1982)

Nelson, R.R., Winter, S.G.: An Evolutionary Theory of Economic Change. Harvard University Press, Cambridge, MA (1982). https://doi.org/10.1086/261177

-

[34]

Pangallo, M., Giachini, D., Vandin, A.: Statistical model checking of netlogo models. CoRRabs/2509.10977(2025). https://doi.org/10.48550/ARXIV.2509. 10977, https://doi.org/10.48550/arXiv.2509.10977

-

[35]

Pianini,D.,Sebastio,S.,Vandin,A.:Distributedstatisticalanalysisofcomplexsys- tems modeled through a chemical metaphor. In: International Conference on High Performance Computing & Simulation, HPCS 2014, Bologna, Italy, 21-25 July,

work page 2014

-

[36]

pp. 416–423. IEEE (2014). https://doi.org/10.1109/HPCSIM.2014.6903715, https://doi.org/10.1109/HPCSim.2014.6903715

-

[37]

Richiardi, M., Leombruni, R., Saam, N.J., Sonnessa, M.: A common protocol for agent-based social simulation. Journal of Artificial Societies and Social Simulation 9(1), 15 (2006), https://www.jasss.org/9/1/15.html

work page 2006

-

[38]

Performance Evaluation70(6), 457–475 (2013)

Sebastio, S., Vandin, A.: Multivesta: Statistical model checking for discrete event simulators. Performance Evaluation70(6), 457–475 (2013). https://doi.org/10. 4108/icst.valuetools.2013.254377

-

[39]

Computational and Math- ematical Organization Theory23(1), 94–121 (2017)

Secchi, D., Seri, R.: Controlling for false negatives in agent-based models: a review of power analysis in organizational research. Computational and Math- ematical Organization Theory23(1), 94–121 (2017). https://doi.org/10.1007/ s10588-016-9218-0, https://doi.org/10.1007/s10588-016-9218-0

-

[40]

The Quarterly Journal of Economics69(1), 99–118 (1955)

Simon, H.A.: A behavioral model of rational choice. The Quarterly Journal of Economics69(1), 99–118 (1955). https://doi.org/10.2307/1884852

-

[41]

Tesfatsion, L., Judd, K.L.: Handbook of Computational Economics: Agent-Based Computational Economics, vol. 2. Elsevier, Amsterdam (2006). https://doi.org/ 10.1109/mci.2008.929849

-

[42]

Computational Economics60(4), 1507–1527 (2022)

Tieleman, S.: Towards a validation methodology for macroeconomic agent-based models. Computational Economics60(4), 1507–1527 (2022). https://doi.org/10. 1007/s10614-021-10191-w

work page 2022

-

[43]

Science185(4157), 1124–1131 (1974)

Tversky, A., Kahneman, D.: Judgment under uncertainty: Heuristics and biases. Science185(4157), 1124–1131 (1974). https://doi.org/10.1126/science.185.4157. 1124, https://doi.org/10.1126/science.185.4157.1124

-

[44]

Vandin, A.: Statistical model checking of python agent-based models: An integra- tion of multivesta and mesa. In: Steffen, B. (ed.) Bridging the Gap Between AI and Reality - Second International Conference, AISoLA 2024, Crete, Greece, Octo- ber 30 - November 3, 2024, Proceedings. Lecture Notes in Computer Science, vol. 15217, pp. 398–419. Springer (2024)....

-

[45]

Journal of Economic Dynamics and Control143(10 2022)

Vandin, A., Giachini, D., Lamperti, F., Chiaromonte, F.: Automated and dis- tributed statistical analysis of economic agent-based models. Journal of Economic Dynamics and Control143(10 2022). https://doi.org/10.1016/j.jedc.2022.104458 20 S. Blando et al

-

[46]

Sequential Tests of Statistical Hypotheses

Wald, A.: Sequential tests of statistical hypotheses. The Annals of Mathematical Statistics16(2), 117–186 (1945). https://doi.org/10.1214/aoms/1177731118

-

[47]

Wiley (2009), https: //books.google.it/books?id=X3ZQ7yeDn2IC

Wooldridge, M.: An Introduction to MultiAgent Systems. Wiley (2009), https: //books.google.it/books?id=X3ZQ7yeDn2IC

work page 2009

-

[48]

In: Computer Aided Verification (CAV 2002)

Younes, H.L.S., Simmons, R.G.: Probabilistic verification of discrete event systems using acceptance sampling. In: Computer Aided Verification (CAV 2002). LNCS, vol. 2404, pp. 223–235. Springer (2002) A Summary Tables This appendix collects the full observable-wise summary tables supporting the compactdiscussioninSection6.Tables4–6reporttheper-experiments...

work page 2002

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.