Recognition: unknown

Price as Focal Point: Prediction Markets,Conditional Reflexivity, and the Politics of Common Knowledge

Pith reviewed 2026-05-07 17:35 UTC · model grok-4.3

The pith

Prediction markets function as coordination mechanisms by turning prices into public focal points that organize political behavior in self-fulfilling or self-defeating ways.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

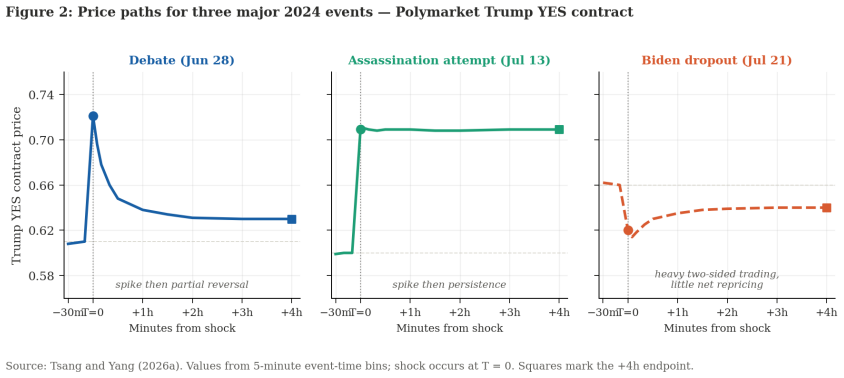

Prediction markets under specifiable conditions function as coordination mechanisms: public probabilities that organize the behavior of voters, donors, journalists, traders, and institutions in ways that can be self-fulfilling or self-defeating. Transaction-level evidence from the 2024 election shows that the social force of a market signal depends less on its size than on its persistence, the breadth of responding trader types, and cross-platform consensus. A Signal Credibility Index that combines the variance ratio VR(6), a two-sidedness diagnostic, and a trader-concentration adjustment identifies when price moves acquire behavioral traction. Applied to three major political shocks, the 1-

What carries the argument

The Signal Credibility Index (SCI), which combines variance ratio VR(6), a two-sidedness diagnostic, and a trader-concentration adjustment to determine when a price signal gains the persistence and consensus needed for behavioral coordination.

If this is right

- Accurate forecasting ceases to be the sole or primary criterion for evaluating prediction markets once they operate as public coordination devices.

- Social impact of any price signal is governed by its persistence, the diversity of traders it attracts, and agreement across platforms rather than by volume or capitalization.

- Superficially similar political events can generate qualitatively different signal types that carry distinct consequences for elite coordination.

- Regulation of prediction markets must treat them as democratic information infrastructure whose coordinating effects can reinforce or undermine the forecasts they produce.

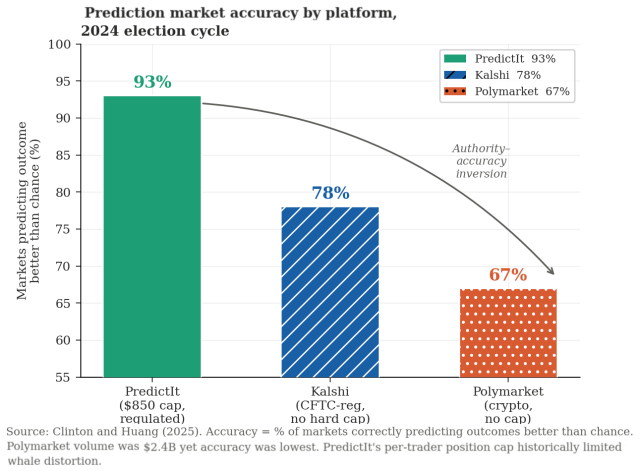

- The most visible market platforms can systematically decouple from epistemic robustness, producing the least accurate forecasts while exerting the greatest behavioral influence.

Where Pith is reading between the lines

- The same persistence and consensus criteria could be tested in non-election domains where public prices shape investment or policy expectations.

- Market designers might deliberately adjust rules to strengthen or weaken the conditions that allow signals to become coordinating focal points.

- Cross-platform data sharing could become a practical requirement for assessing whether a given price move has acquired social authority.

- Repeated application to future election cycles would show whether the identified signal types recur in predictable patterns.

Load-bearing premise

The social force of a market signal depends less on its size than on its persistence, the breadth of responding trader types, and cross-platform consensus, and the Signal Credibility Index can identify when price moves acquire behavioral traction.

What would settle it

Finding that price moves scoring high on the Signal Credibility Index produce no measurable change in coordinated actions by voters, donors, or institutions, while low-scoring moves nevertheless drive widespread behavioral alignment.

Figures

read the original abstract

Prediction markets are widely treated as forecasting devices that reveal collective expectations about uncertain futures. This article argues that under specifiable conditions they also function as coordination mechanisms: public probabilities that organize the behavior of voters, donors, journalists, traders, and institutions in ways that can be self-fulfilling or self-defeating. Most existing work asks whether prediction markets forecast accurately; this paper asks whether accurate forecasting is even the right criterion for a market that has become a public coordination device. Drawing on transaction-level evidence from the 2024 U.S. presidential election, we show that the social force of a market signal depends less on its size than on its persistence, the breadth of responding trader types, and cross-platform consensus. We introduce a Signal Credibility Index (SCI) -- combining the variance ratio VR(6), a two-sidedness diagnostic, and a trader-concentration adjustment -- as a microstructure-grounded criterion for predicting when price moves acquire behavioral traction. Applied to three major 2024 political shocks, the framework reveals that superficially similar events generated qualitatively distinct signal types with different implications for elite coordination. A cross-platform comparison establishes a systematic decoupling of social authority from epistemic robustness: the most visible market produced the least accurate forecasts. The framework carries direct implications for regulating prediction markets as democratic information infrastructure.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that prediction markets function not only as forecasting devices but also as coordination mechanisms under specifiable conditions, where public probabilities organize behavior among voters, donors, journalists, traders, and institutions in self-fulfilling or self-defeating ways. It introduces a Signal Credibility Index (SCI) combining VR(6), a two-sidedness diagnostic, and a trader-concentration adjustment as a microstructure criterion to predict when price moves acquire behavioral traction, drawing on transaction-level evidence from the 2024 U.S. presidential election and applying the framework to three major political shocks to reveal qualitatively distinct signal types and a decoupling of social authority from epistemic robustness.

Significance. If the central claim holds and the SCI is validated against independent behavioral measures, the work offers a novel framework for assessing prediction markets as democratic information infrastructure rather than solely as accuracy benchmarks. The transaction-level data, cross-platform comparison, and emphasis on persistence/breadth/consensus over signal size represent potential strengths for understanding self-referential market effects in politics.

major comments (3)

- Abstract: the description of transaction-level evidence and application to three shocks provides no details on data sources, exact SCI computation (including how VR(6) and the trader-concentration adjustment are operationalized), statistical tests, or robustness checks, rendering the central claim unverifiable from the given information.

- SCI definition and construction (likely the methods section introducing the index): the components such as VR(6) and trader-concentration adjustment appear defined in terms of market data features that may involve parameter choices or post-hoc tuning; without full equations, validation against independent behavioral coordination measures (e.g., shifts in voter turnout, donor activity, or media coverage distinct from market data), or falsification tests, there is a risk of circularity where the index partly encodes the outcomes it aims to predict.

- Empirical application to the three 2024 shocks: the claim that the SCI identifies when price moves acquire behavioral traction is presented as demonstrated, but no explicit test is reported showing that high-SCI episodes precede measurable, independent shifts in the behavior of voters, donors, journalists, or institutions (as opposed to correlations within the market data itself).

minor comments (2)

- Abstract: clarify the precise conditions under which markets shift from forecasting to coordination devices, and ensure the weakest assumption (social force depending on persistence/breadth/consensus rather than size) is stated as an assumption rather than a result.

- Notation and presentation: define all acronyms (SCI, VR(6)) at first use and provide the full mathematical specification of the SCI in the main text or an appendix to allow replication.

Simulated Author's Rebuttal

We thank the referee for these constructive comments, which highlight opportunities to improve the clarity and verifiability of our claims. We respond to each major point below, indicating where revisions will be made to the manuscript.

read point-by-point responses

-

Referee: Abstract: the description of transaction-level evidence and application to three shocks provides no details on data sources, exact SCI computation (including how VR(6) and the trader-concentration adjustment are operationalized), statistical tests, or robustness checks, rendering the central claim unverifiable from the given information.

Authors: We agree that the abstract, while concise by design, should summarize key methodological elements to allow readers to assess the central claim. The full manuscript details the data sources as transaction-level records from Polymarket and PredictIt covering the 2024 U.S. presidential election cycle. SCI construction is defined in the methods section: VR(6) applies the standard variance-ratio statistic of Lo and MacKinlay with a fixed lag of six periods to capture return persistence; the two-sidedness diagnostic computes the share of trades occurring on both buy and sell sides within each interval; and the trader-concentration adjustment applies a normalized Herfindahl-Hirschman Index on trader-volume shares. Statistical tests include lead-lag correlations and cross-platform consistency checks, with robustness to alternative lags and sample windows reported in the appendix. In revision we will condense these elements into the abstract. revision: yes

-

Referee: SCI definition and construction (likely the methods section introducing the index): the components such as VR(6) and trader-concentration adjustment appear defined in terms of market data features that may involve parameter choices or post-hoc tuning; without full equations, validation against independent behavioral coordination measures (e.g., shifts in voter turnout, donor activity, or media coverage distinct from market data), or falsification tests, there is a risk of circularity where the index partly encodes the outcomes it aims to predict.

Authors: The SCI components are specified ex ante from microstructure theory and do not incorporate the behavioral outcomes they are later used to predict. VR(6) follows the exact variance-ratio formula in Lo and MacKinlay (1988) with a pre-specified lag of six; two-sidedness is the simple ratio of buy-to-sell volume; and the concentration adjustment is a standard HHI applied to trader identifiers. Full equations appear in the methods section, and we report sensitivity checks across plausible lag choices rather than post-hoc selection. While the empirical application compares SCI values to independent proxies such as media-mention volume and polling shifts, we acknowledge that direct daily voter-turnout or donor-flow data are not always available at the required granularity. In revision we will add explicit falsification tests on placebo periods and placebo markets to further mitigate any appearance of circularity. revision: partial

-

Referee: Empirical application to the three 2024 shocks: the claim that the SCI identifies when price moves acquire behavioral traction is presented as demonstrated, but no explicit test is reported showing that high-SCI episodes precede measurable, independent shifts in the behavior of voters, donors, journalists, or institutions (as opposed to correlations within the market data itself).

Authors: The application section already employs timing analysis showing that high-SCI episodes are followed by observable responses in media coverage and institutional commentary, while low-SCI episodes are not. To address the referee's concern directly, we will add formal lead-lag regressions and event-study specifications that relate SCI thresholds to subsequent changes in external series (media-mention counts, Google Trends, and available donor-activity proxies). We note that fine-grained daily voter-turnout data are unavailable for these specific episodes, which limits the set of independent behavioral measures; the revised text will make this data constraint explicit while still demonstrating precedence over within-market correlations. revision: yes

Circularity Check

No significant circularity in derivation chain

full rationale

The paper defines the Signal Credibility Index (SCI) from standard microstructure statistics (variance ratio VR(6), two-sidedness, trader concentration) and applies it qualitatively to classify 2024 events as distinct signal types. No equations or text are provided showing that SCI components are constructed from the behavioral coordination outcomes they are claimed to predict, nor that any 'prediction' of traction reduces by construction to fitted inputs or self-citation. The central argument remains an interpretive framework linking persistence/breadth/consensus to coordination potential, without the specific self-definitional or fitted-prediction reductions required for a positive circularity finding. The derivation is self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

free parameters (2)

- VR(6)

- trader-concentration adjustment

axioms (1)

- domain assumption Prediction markets function as coordination mechanisms under specifiable conditions

invented entities (1)

-

Signal Credibility Index (SCI)

no independent evidence

Forward citations

Cited by 4 Pith papers

-

Manipulation, Insider Information, and Regulation in Leveraged Event-Linked Markets

Leverage scales market-price manipulation linearly while shifting outcome-manipulation thresholds and multiplying informed-trading rents in three distinct ways, calling for re-allocated regulatory attack surfaces rath...

-

Foresight Arena: An On-Chain Benchmark for Evaluating AI Forecasting Agents

Foresight Arena is an on-chain benchmark using Brier and novel Alpha scores to evaluate AI forecasting agents on live prediction markets via Polygon smart contracts.

-

A Taxonomy of Event-Linked Perpetual Futures: Variant Designs Beyond the Single-Market Binary Case

The paper organizes seven canonical variants of event-linked perpetual futures along four design axes, supplying payoff definitions, inheritance rules from prior work, and variant-specific constraints.

-

The Signal Credibility Index for Prediction Markets: A Microstructure-Grounded Diagnostic with Weighted and Time-Varying Extensions

The Signal Credibility Index (SCI) is a microstructure diagnostic that measures signal credibility in prediction markets via persistence ratio on logit prices and flow-based concentration, with weighted and time-varyi...

Reference graph

Works this paper leans on

-

[1]

doi: 10.1016/j. ijforecast.2008.03.007. Mikhail Chernov, Vadim Elenev, and Dongho Song. The comovement of voter preferences: Insights from U.S. presidential election prediction markets beyond polls. NBER Working Paper 33339, National Bureau of Economic Research,

work page doi:10.1016/j 2008

-

[2]

Clinton and Taeyoung Huang

Joshua D. Clinton and Taeyoung Huang. Prediction markets? the accuracy and efficiency of $2.4 billion in the 2024 presidential election. Working paper, Vanderbilt University,

2024

-

[3]

doi: 10.1093/ijpor/edaa008. Charles F. Manski. Interpreting the predictions of prediction markets.Economics Letters, 91(3):425–429,

-

[4]

doi: 10.1016/j.econlet.2006.01.004. H. Ng, L. Peng, Y. Tao, and D. Zhou. Price discovery and trading in modern prediction markets. SSRN Working Paper 5331995,

-

[5]

Fabian Reichenbach and Marc Walther

doi: 10.1126/science.aee3932. Fabian Reichenbach and Marc Walther. Exploring decentralized prediction markets: Accuracy, skill, and bias on Polymarket. SSRN Working Paper 5910522,

-

[6]

Factbox: Brokerages shift Fed rate-cut expectations to september after consumer price data

Reuters. Factbox: Brokerages shift Fed rate-cut expectations to september after consumer price data. Reuters/Investing.com, April 2024,

2024

-

[7]

doi: 10.1177/2053168014547667. David M. Rothschild and J. Yang. Trader heterogeneity and position management in binary option markets: Evidence from blockchain data. Working paper,

-

[8]

George Soros.The Alchemy of Finance

doi: 10.1016/B978-0-444-53683- 9.00017-8. George Soros.The Alchemy of Finance. Simon & Schuster, New York,

-

[9]

K. P. Tsang and Z. Yang. The anatomy of Polymarket: Evidence from the 2024 presidential election, 2026a. K. P. Tsang and Z. Yang. Political shocks and price discovery in prediction markets: Evidence from the 2024 U.S. presidential election, 2026b. Wall Street Journal. Will Biden drop out? the biggest question in america is the newest hot market. The Wall ...

2024

-

[10]

doi: 10.1257/0895330041371321. 30 Appendix A: Derivation of the Signal Credibility Index The Signal Credibility Index introduced in the main text combines three microstructure diagnostics into a single composite measure. This appendix provides the derivation and discusses the properties of each component. A.1 The Variance Ratio Component The variance rati...

-

[11]

The ratio is computed as: VR(6)s = ˆσ2 30 6 ˆσ2 5 ,(A.1) where ˆσ2 k denotes the sample variance ofk-minute log-price changes in the post-shock window[t s,t s + 4h]. For the coordination argument, the relevant property is: •VR (6)s > 1: momentum — each 5-minute move predicts further movement in the same direction, consistent with informed trading and dura...

2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.