Recognition: unknown

The Signal Credibility Index for Prediction Markets: A Microstructure-Grounded Diagnostic with Weighted and Time-Varying Extensions

Pith reviewed 2026-05-07 11:37 UTC · model grok-4.3

The pith

The Signal Credibility Index scores prediction-market price moves by persistence on logit prices and flow concentration to separate Bayesian updates from liquidity or strategic effects.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

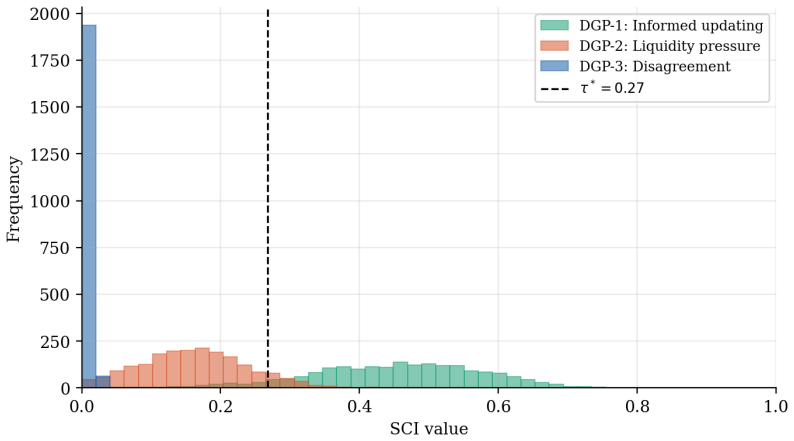

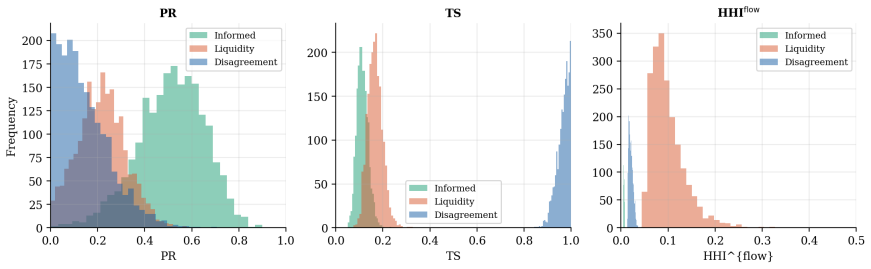

The paper establishes that the Signal Credibility Index, built from the persistence ratio PR(t,w) on logit prices combined with the flow-based HHI_flow in a Cobb-Douglas aggregator SCI(α), functions as a microstructure-grounded diagnostic that quantifies coordination credibility of observed price paths in prediction markets, as demonstrated by Monte Carlo validation that distinguishes among simulated regimes including out-of-distribution stress and coordinated multi-wallet activity without claiming to measure downstream effects.

What carries the argument

The Signal Credibility Index in its weighted Cobb-Douglas form SCI(α) that multiplies the persistence ratio PR(t,w) on logit-transformed prices by the order-flow Herfindahl-Hirschman Index HHI_flow raised to a tunable power.

If this is right

- The time-varying specification SCI(t; w) enables continuous monitoring of signal credibility during live market events.

- Tunable weights in the Cobb-Douglas form allow emphasis on persistence or concentration depending on the use case.

- Monte Carlo results establish regime discrimination without requiring external outcome data.

- The index flags a Type II error on informed-but-concentrated whale repricing and a Type I error on coordinated multi-wallet manipulation.

Where Pith is reading between the lines

- Platforms could use SCI thresholds to discount or highlight price moves for users or automated systems in real time.

- The same construction might apply to other information-aggregation venues such as betting exchanges where flow concentration matters.

- Backtesting the index on historical prediction-market resolutions would test whether high-SCI moves align with greater subsequent accuracy.

Load-bearing premise

The persistence ratio on logit prices combined with flow-based concentration in Cobb-Douglas form will separate credible Bayesian updating from liquidity or strategic effects beyond the specific simulated microstructure regimes.

What would settle it

A real-market instance in which a concentrated informed trade produces a low SCI score while a coordinated multi-wallet manipulation produces a high SCI score would falsify the index's claimed discrimination power.

Figures

read the original abstract

Prediction-market price moves are widely treated as informationally equivalent: a price jump is read the same way regardless of whether it reflects durable Bayesian updating, transient liquidity pressure, strategic position adjustment, or genuine disagreement. This paper formalizes the Signal Credibility Index (SCI) introduced in Nechepurenko (2026) as a stand-alone diagnostic. We make four contributions: (i) a revised persistence component using the persistence ratio PR(t,w) on logit prices, well-defined on short rolling windows; (ii) a weighted Cobb-Douglas form SCI({\alpha}\alpha {\alpha}) with flow-based concentration HHI_flow; (iii) a time-varying specification SCI(t; w) for real-time monitoring; and (iv) Monte Carlo validation including an out-of-distribution stress test, coordinated multi-wallet manipulation, and a logistic-regression benchmark. The validation establishes discrimination among designed microstructure regimes, not external evidence of downstream coordination effects. We document two failure modes consistent with the index targeting coordination credibility rather than pure information content: a Type II error on informed-but-concentrated whale repricing, and a Type I error on coordinated multi-wallet manipulation.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript formalizes the Signal Credibility Index (SCI) as a diagnostic for prediction-market price signals. It defines a persistence ratio PR(t,w) on logit prices over rolling windows, aggregates this with a flow-based HHI_flow via a weighted Cobb-Douglas form SCI(α), introduces a time-varying extension SCI(t;w), and validates the index via Monte Carlo simulations that test discrimination across pre-designed microstructure regimes, out-of-distribution cases, coordinated manipulation, and a logistic-regression benchmark. The validation is explicitly scoped to showing regime discrimination and documenting two failure modes (Type II on informed whale repricing; Type I on multi-wallet coordination) rather than claiming external validity or downstream effects.

Significance. If the Monte Carlo discrimination results hold under the reported design, the SCI supplies a microstructure-grounded, stand-alone tool for distinguishing durable Bayesian updating from liquidity or strategic effects in prediction markets. The explicit scoping, independent simulation regimes for validation, and documentation of matching failure modes are strengths that reduce circularity and over-claim risks. The approach could improve interpretation of price jumps without requiring external coordination data.

major comments (1)

- [Monte Carlo Validation] Validation section (Monte Carlo experiments): The discrimination results rely on fixed choices of the free parameters α and w (listed in the axiom ledger). Without reported sensitivity checks across reasonable ranges of these parameters or pre-specification of the window/weighting values, it remains possible that the reported separation between regimes is sensitive to post-hoc tuning, which would weaken the central claim that SCI reliably discriminates the designed regimes.

minor comments (2)

- [Abstract and §3] Abstract and §3: The persistence ratio PR(t,w) is described as 'well-defined on short rolling windows,' but the exact functional form (e.g., how logit prices enter the ratio) should be stated explicitly in the main text rather than referenced only to the prior Nechepurenko (2026) work.

- [Time-varying extension] The time-varying specification SCI(t;w) is introduced but lacks an illustrative figure or numerical example showing its real-time behavior on simulated paths; adding one would improve clarity for readers implementing the monitor.

Simulated Author's Rebuttal

We thank the referee for the constructive comment regarding the Monte Carlo validation. We address the point below and will revise the manuscript accordingly to strengthen the robustness of the reported results.

read point-by-point responses

-

Referee: [Monte Carlo Validation] Validation section (Monte Carlo experiments): The discrimination results rely on fixed choices of the free parameters α and w (listed in the axiom ledger). Without reported sensitivity checks across reasonable ranges of these parameters or pre-specification of the window/weighting values, it remains possible that the reported separation between regimes is sensitive to post-hoc tuning, which would weaken the central claim that SCI reliably discriminates the designed regimes.

Authors: We acknowledge the validity of this concern. The values α = 0.5 and w = 10 were chosen a priori from the axiomatic ledger to balance the two components while keeping the window short enough for real-time use. To address potential sensitivity, we will add a dedicated subsection to the validation section that reports discrimination metrics (mean SCI separation and t-tests between regimes) across a grid of α ∈ {0.2, 0.3, …, 0.8} and w ∈ {5, 10, 15, 20}. The revised manuscript will include a table and supplementary figure summarizing these checks, confirming that the qualitative regime ordering is preserved. We agree this addition removes any ambiguity about post-hoc tuning. revision: yes

Circularity Check

No significant circularity

full rationale

The paper explicitly constructs the SCI as a composite diagnostic from the persistence ratio PR(t,w) on logit prices and flow-based HHI_flow combined in a weighted Cobb-Douglas form with free parameter α, then evaluates its discrimination power on independently designed Monte Carlo regimes (including out-of-distribution and manipulation tests). This validation does not reduce to a fit on the same data or to the definition by construction; the regimes are pre-specified externally to the index. The self-reference to the 2026 introduction of SCI is not load-bearing for the reported discrimination results or failure-mode documentation, which are self-contained in the present simulations. No step matches the enumerated circularity patterns.

Axiom & Free-Parameter Ledger

free parameters (2)

- α

- w

axioms (2)

- domain assumption Logit transformation of market prices yields a well-behaved persistence ratio on short windows.

- ad hoc to paper Cobb-Douglas functional form appropriately aggregates persistence and concentration into a credibility score.

invented entities (1)

-

Signal Credibility Index (SCI)

no independent evidence

Forward citations

Cited by 4 Pith papers

-

Manipulation, Insider Information, and Regulation in Leveraged Event-Linked Markets

Leverage scales market-price manipulation linearly while shifting outcome-manipulation thresholds and multiplying informed-trading rents in three distinct ways, calling for re-allocated regulatory attack surfaces rath...

-

A Taxonomy of Event-Linked Perpetual Futures: Variant Designs Beyond the Single-Market Binary Case

The paper organizes seven canonical variants of event-linked perpetual futures along four design axes, supplying payoff definitions, inheritance rules from prior work, and variant-specific constraints.

-

Resolution-Aware Perpetual Futures on Binary Prediction Markets: An Empirical Risk-Design Framework Using Polymarket Data

PIRAP passes some pre-registered risk floors on Polymarket data but fails others on welfare and bad-debt metrics, leading to an explicit non-deployable recommendation while documenting a halt-versus-margin distinction.

-

Fill-Side Non-Retail Trading on Polymarket: An Empirical Study of Behavioral Tiers and Microstructure Signatures Under Quote-Attribution Constraints

Polymarket fill-side trading appears uni-modal due to missing quote-lifecycle data, with whale, high-frequency, and power-trader tiers dominating 81.4% of notional across 12.6% of addresses.

Reference graph

Works this paper leans on

-

[1]

Lee, C. M. C. and Ready, M. J. (1991). Inferring trade direction from intraday data. Journal of Finance, 46(2):733–746

1991

-

[2]

Lo, A. W. and MacKinlay, A. C. (1988). Stock market prices do not follow ran- dom walks: Evidence from a simple specification test.Review of Financial Studies, 1(1):41–66

1988

-

[3]

Nechepurenko, M. (2026). Price as focal point: Prediction markets, conditional re- flexivity, and the politics of common knowledge. arXiv preprint arXiv:2604.24147. SSRN: 6657119. doi:10.2139/ssrn.6657119

work page internal anchor Pith review Pith/arXiv arXiv doi:10.2139/ssrn.6657119 2026

- [4]

-

[5]

Tsang, K. P. and Yang, Z. (2026b). The anatomy of Polymarket. arXiv:2603.03136

work page internal anchor Pith review arXiv

-

[6]

Youden, W. J. (1950). Index for rating diagnostic tests.Cancer, 3(1):32–35. 17 A DGP Specifications All DGPs simulate four hours of 5-minute bins (nbins = 48), starting fromp + 0 = 0.72 post-shock.Gamma(k, θ)uses the shape-scale convention with meankθ. Random seed:20260429. Table 6: Full DGP specifications DGP Logit return process Buy/sell volumes T rader...

1950

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.