Insurance of Agentic AI

Pith reviewed 2026-06-28 05:53 UTC · model grok-4.3

The pith

Agentic AI requires a layered ecosystem of complementary insurance coverages rather than a single monoline product.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

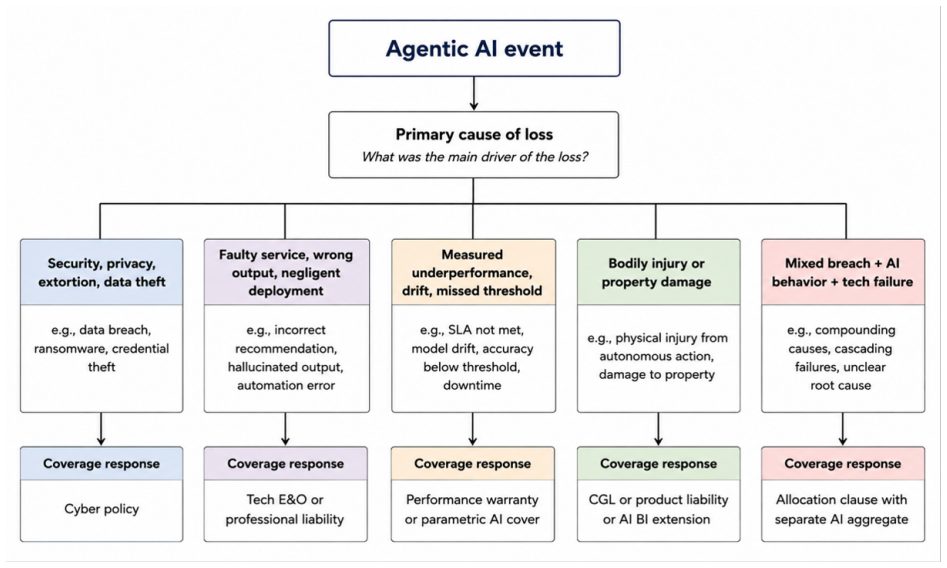

Agentic AI is defined as a continuum of autonomy and delegated authority that can independently generate insured events through external actions, unlike purely informational systems. This creates novel risk pathways including hallucinations, prompt-injection attacks, autonomous decision errors, model drift, dependency failures, and cyber-physical harms. The paper proposes an actuarial framework based on exposure assessment, scenario analysis, dependency mapping, and accumulation-risk management, leading to a coordinated insurance architecture that integrates cyber, technology errors and omissions, product liability, performance-warranty, and affirmative AI-liability coverages through explici

What carries the argument

The coordinated insurance architecture that integrates cyber, technology errors and omissions, product liability, performance-warranty, and affirmative AI-liability coverages through explicit allocation mechanisms and dedicated AI aggregates.

If this is right

- Existing insurance products can be adapted and coordinated to address agentic AI exposures rather than requiring entirely new monoline policies.

- Underwriting and pricing will depend on improved system governance, transparency, and telemetry data from AI deployments.

- Reinsurance will need to incorporate accumulation-risk management across layered policies to handle correlated AI failures.

- The market structure will mirror the evolution of cyber insurance with multiple complementary products instead of a single comprehensive one.

- Regulatory clarity on risk allocation and data requirements will be necessary to enable the proposed architecture.

Where Pith is reading between the lines

- AI developers may need to prioritize logging and control features to make systems eligible for coverage under the layered model.

- This approach could influence standards for AI auditing as insurers require telemetry to assess and price risks.

- Similar layered insurance questions may arise for other autonomous systems such as industrial robots or self-driving vehicles.

- A practical test would be whether market offerings trend toward bundled multi-policy solutions or remain fragmented.

Load-bearing premise

The risks from agentic AI can be distinctly identified, mapped to existing insurance categories, and allocated through explicit mechanisms without creating unmanageable overlaps or uninsurable gaps.

What would settle it

A significant loss event triggered by an agentic AI system where the resulting claims cannot be assigned to any combination of the proposed coverages due to irresolvable overlap, ambiguity in risk pathways, or exposure outside all mapped categories.

Figures

read the original abstract

Agentic artificial intelligence (AI) systems are transforming the risk landscape by extending beyond information generation to autonomous planning, tool invocation, decision execution, and persistent modification of digital and physical environments. These capabilities introduce novel exposures that do not fit neatly within traditional insurance categories such as cyber, professional liability, product liability, or directors and officers coverage. This paper examines the emerging insurance market for agentic AI and develops a framework for understanding its underwriting, pricing, reinsurance, and product-design implications. We characterize agentic AI as a continuum of autonomy and delegated authority, emphasizing the distinction between informational outputs and systems capable of independently generating insured events through external actions. We analyze major risk pathways, including hallucinations, prompt-injection attacks, autonomous decision errors, model drift, dependency failures, and cyber-physical harms, and evaluate how existing insurance products are adapting to address these exposures. The paper further proposes an actuarial framework based on exposure assessment, scenario analysis, dependency mapping, and accumulation-risk management, drawing parallels to the evolution of cyber insurance. Finally, we present a coordinated insurance architecture that integrates cyber, technology errors and omissions, product liability, performance-warranty, and affirmative AI-liability coverages through explicit allocation mechanisms and dedicated AI aggregates. The analysis suggests that the future of agentic-AI insurance lies not in a single monoline product but in a layered ecosystem of complementary coverages supported by improved governance, transparency, telemetry, and regulatory clarity.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that agentic AI systems introduce novel exposures (hallucinations, prompt-injection, autonomous decision errors, model drift, dependency failures, cyber-physical harms) that do not fit traditional insurance categories. It characterizes agentic AI along a continuum of autonomy, analyzes these risk pathways, proposes an actuarial framework based on exposure assessment, scenario analysis, dependency mapping and accumulation-risk management (drawing parallels to cyber insurance), and presents a coordinated architecture integrating cyber, technology E&O, product liability, performance-warranty and affirmative AI-liability coverages via explicit allocation mechanisms and dedicated AI aggregates. The central conclusion is that the future lies in a layered ecosystem of complementary coverages rather than a single monoline product.

Significance. If the proposed allocation mechanisms and dependency mappings can be made concrete and shown to avoid overlaps or gaps, the framework would offer a structured way to extend existing insurance lines to agentic systems and could guide product design, underwriting and reinsurance. The explicit parallel to the historical development of cyber insurance is a useful reference point. The work remains conceptual and qualitative, with no quantitative models or validation, so its significance is primarily in framing the problem for subsequent actuarial and regulatory work.

major comments (2)

- [Abstract and coordinated architecture section] Abstract and coordinated architecture section: the claim that the architecture integrates the listed coverages 'through explicit allocation mechanisms and dedicated AI aggregates' is load-bearing for the layered-ecosystem conclusion, yet the manuscript supplies no allocation rules, risk-to-coverage mapping tables, overlap-resolution procedures, or scenario-level illustrations showing how hallucinations versus autonomous decision errors would be distinctly assigned without double-counting or gaps.

- [Risk pathways and actuarial framework sections] Risk pathways and actuarial framework sections: the listed exposures (hallucinations, prompt-injection, model drift, etc.) are asserted to be mappable to existing categories, but no dependency-mapping examples or accumulation-risk calculations are provided; without these the distinction between informational outputs and externally acting systems cannot be shown to produce insurable, non-overlapping exposures.

minor comments (2)

- The continuum-of-autonomy characterization would benefit from a short table or diagram contrasting low-autonomy informational agents with high-autonomy tool-invoking agents to make the distinction operational for underwriters.

- Several risk categories (e.g., 'cyber-physical harms') are introduced without reference to existing case law or regulatory definitions that insurers already use; adding one or two citations would improve grounding.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments. The report correctly identifies that the manuscript is conceptual and qualitative. We address each major comment below and indicate where revisions will be made to strengthen the presentation of the framework.

read point-by-point responses

-

Referee: [Abstract and coordinated architecture section] Abstract and coordinated architecture section: the claim that the architecture integrates the listed coverages 'through explicit allocation mechanisms and dedicated AI aggregates' is load-bearing for the layered-ecosystem conclusion, yet the manuscript supplies no allocation rules, risk-to-coverage mapping tables, overlap-resolution procedures, or scenario-level illustrations showing how hallucinations versus autonomous decision errors would be distinctly assigned without double-counting or gaps.

Authors: We agree that the manuscript presents the coordinated architecture and allocation mechanisms at a high conceptual level without supplying concrete rules, tables, or scenario illustrations. This reflects the paper's focus on outlining an overall ecosystem rather than operational implementation details. To address the point, we will revise the coordinated architecture section to include a high-level risk-to-coverage mapping table and one illustrative scenario (hallucination versus autonomous decision error) showing assignment logic. These additions will clarify the intended allocation approach without claiming empirical validation. revision: yes

-

Referee: [Risk pathways and actuarial framework sections] Risk pathways and actuarial framework sections: the listed exposures (hallucinations, prompt-injection, model drift, etc.) are asserted to be mappable to existing categories, but no dependency-mapping examples or accumulation-risk calculations are provided; without these the distinction between informational outputs and externally acting systems cannot be shown to produce insurable, non-overlapping exposures.

Authors: The manuscript asserts mappability through qualitative analysis of risk pathways and draws on the cyber-insurance parallel but does not include explicit dependency-mapping examples or accumulation calculations. This is consistent with the paper's scope as a framing exercise rather than a quantitative actuarial study. We will add simplified dependency-mapping examples in the actuarial framework section to illustrate how informational versus externally acting exposures can be distinguished and assigned, thereby supporting the non-overlapping claim at a conceptual level. revision: yes

Circularity Check

No circularity; descriptive framework without derivations or self-referential reductions

full rationale

The paper offers a conceptual analysis and proposed architecture for agentic-AI insurance, characterizing risks and suggesting layered coverages by explicit parallels to the historical development of cyber insurance. No equations, fitted parameters, predictions, or derivation chains appear in the abstract or described content. The central claim rests on external precedent and descriptive mapping rather than any self-definition, fitted-input renaming, or load-bearing self-citation that reduces the result to its own inputs by construction. The absence of mathematical steps or self-referential premises makes the work self-contained against the listed circularity patterns.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Agentic AI systems introduce novel exposures that do not fit neatly within traditional insurance categories such as cyber, professional liability, product liability, or directors and officers coverage.

Forward citations

Cited by 3 Pith papers

-

The Internet of Agentic AI: Communication, Coordination, and Collective Intelligence at Scale

Outlines a vision and key research challenges for scalable networks of autonomous AI agents drawing on multi-agent systems, networks, and security.

-

AI Tokenomics: The Economics of Tokens, Computation, and Pricing in Foundation Models

Develops a framework linking token-level technical costs to workflow-level economic value and market design in AI foundation models.

-

Understanding Censorship in Large Language Models: From Mechanisms to Governance

Synthesizes mechanisms of LLM censorship across the model lifecycle and argues that the key issue is making moderation proportionate, accountable, pluralistic, and auditable rather than debating whether moderation sho...

Reference graph

Works this paper leans on

-

[1]

Cyberedge plus.https://www.aig.com/content/dam/aig/america-canada/us/ documents/business/cyber/cyberedge-plus.pdf, 2024

AIG. Cyberedge plus.https://www.aig.com/content/dam/aig/america-canada/us/ documents/business/cyber/cyberedge-plus.pdf, 2024. Accessed 2026-06-02

2024

-

[2]

Concrete Problems in AI Safety

D. Amodei, C. Olah, J. Steinhardt, P. Christiano, J. Schulman, and D. Man´ e. Concrete problems in AI safety. arXiv:1606.06565, 2016

work page internal anchor Pith review Pith/arXiv arXiv 2016

-

[3]

Claude 4 system card.https://www-cdn.anthropic.com/ 6be99a52cb68eb70eb9572b4cafad13df32ed995.pdf, 2025

Anthropic. Claude 4 system card.https://www-cdn.anthropic.com/ 6be99a52cb68eb70eb9572b4cafad13df32ed995.pdf, 2025. Accessed 2026-06-02

2025

-

[4]

Armilla AI. Armilla launches affirmative AI liability insurance with lloyd’s underwriter chaucer.https://www.armilla.ai/resources/ armilla-launches-affirmative-ai-liability-insurance-with-lloyds-underwriter-chaucer,

-

[5]

AXA XL. AXA XL unveils new cyber insurance extending coverage to help businesses manage emerging GenAI risks.https://axaxl.com/press-releases/ axa-xl-unveils-new-cyber-insurance-extending-coverage-to-help-businesses-manage-emerging-gen-ai-risks,

-

[6]

E. M. Bender, T. Gebru, A. McMillan-Major, and S. Shmitchell. On the dangers of stochastic parrots: Can language models be too big? InProceedings of the 2021 ACM Conference on Fairness, Accountability, and Transparency, pages 610–623, 2021

2021

-

[7]

Bengio, G

Y. Bengio, G. Hinton, A. Yao, D. Song, P. Abbeel, T. Darrell, Y. N. Harari, Y.-Q. Zhang, L. Xue, S. Shalev-Shwartz, et al. Managing extreme AI risks amid rapid progress.Science, 384(6698):842–845, 2024

2024

-

[8]

Bolot and M

J. Bolot and M. Lelarge. Cyber insurance as an incentive for internet security. In M. E. Johnson, editor,Managing Information Risk and the Economics of Security, pages 269–290. Springer, New York, 2009

2009

-

[9]

On the Opportunities and Risks of Foundation Models

R. Bommasani, D. A. Hudson, E. Adeli, R. Altman, S. Arora, et al. On the opportunities and risks of foundation models. arXiv:2108.07258, 2021

work page internal anchor Pith review Pith/arXiv arXiv 2021

-

[10]

Carlini and D

N. Carlini and D. Wagner. Towards evaluating the robustness of neural networks. In2017 IEEE Symposium on Security and Privacy, pages 39–57, 2017

2017

-

[11]

Chaucer Group and Armilla AI. Chaucer and armilla AI launch vanguard AI coordinated insurance structure.https://www.chaucergroup.com/news/ press-release-chaucer-and-armilla-ai-launch-vanguard-ai-coordinated-insurance-structure,

-

[12]

J. Chen, Q. Zhu, and T. Ba¸ sar. Dynamic contract design for systemic cyber risk management of interdependent enterprise networks.Dynamic Games and Applications, 11(2):294–325, 2021

2021

-

[13]

European Insurance and Occupational Pensions Authority. Methodological principles of insurance stress testing: Cyber component.https://www.eiopa.europa.eu/publications/ methodological-principles-insurance-stress-testing-cyber-component_en, 2024. Accessed 2026-06-02

2024

-

[14]

Regulation (eu) 2024/1689 laying down harmonised rules on artificial intelli- gence.https://eur-lex.europa.eu/eli/reg/2024/1689/oj/eng, 2024

European Union. Regulation (eu) 2024/1689 laying down harmonised rules on artificial intelli- gence.https://eur-lex.europa.eu/eli/reg/2024/1689/oj/eng, 2024. Accessed 2026-06- 02

2024

-

[15]

I. J. Goodfellow, J. Shlens, and C. Szegedy. Explaining and harnessing adversarial examples. InInternational Conference on Learning Representations, 2015

2015

-

[16]

L. A. Gordon and M. P. Loeb. The economics of information security investment.ACM Transactions on Information and System Security, 5(4):438–457, 2002

2002

- [17]

- [18]

- [19]

-

[20]

Liu and Q

S. Liu and Q. Zhu. Mitigating moral hazard in insurance contracts using risk preference design. Operations Research Letters, 62:107322, 2025

2025

-

[21]

Generative AI: Evolving risk and insurance considerations.https://www.marsh.com/ en/services/cyber-risk/insights/generative-ai-evolving-considerations.html,

Marsh. Generative AI: Evolving risk and insurance considerations.https://www.marsh.com/ en/services/cyber-risk/insights/generative-ai-evolving-considerations.html,

-

[22]

Mosaic x aisure powered by munich re.https://www

Mosaic Insurance and aiSure. Mosaic x aisure powered by munich re.https://www. mosaicinsurance.com/wp-content/uploads/2026/02/26-02-25-Mosaic-x-aiSure.pdf,

2026

-

[23]

Cybersecurity insurance report

National Association of Insurance Commissioners. Cybersecurity insurance report. https://content.naic.org/sites/default/files/inline-files/2025_Cybersecurity_ Insurance%20Report.pdf, 2025. Accessed 2026-06-02

2025

-

[24]

AI Agents: Technical and policy context

National Institute of Standards and Technology. AI Agents: Technical and policy context. https://www.regulations.gov/document/NIST-2025-0035-0001, 2025. Accessed 2026-06- 02

2025

-

[25]

New report on the challenges of monitoring deployed AI systems.https://www.nist.gov/news-events/news/2026/03/ new-report-challenges-monitoring-deployed-ai-systems, 2026

National Institute of Standards and Technology. New report on the challenges of monitoring deployed AI systems.https://www.nist.gov/news-events/news/2026/03/ new-report-challenges-monitoring-deployed-ai-systems, 2026. Accessed 2026-06-02

2026

-

[26]

ChatGPT Agent system card.https://cdn.openai.com/pdf/ 6bcccca6-3b64-43cb-a66e-4647073142d7/chatgpt_agent_system_card_launch.pdf,

OpenAI. ChatGPT Agent system card.https://cdn.openai.com/pdf/ 6bcccca6-3b64-43cb-a66e-4647073142d7/chatgpt_agent_system_card_launch.pdf,

-

[27]

Operator system card.https://openai.com/index/operator-system-card/,

OpenAI. Operator system card.https://openai.com/index/operator-system-card/,

-

[28]

Operator system card.https://cdn.openai.com/operator_system_card.pdf,

OpenAI. Operator system card.https://cdn.openai.com/operator_system_card.pdf,

-

[29]

Organisation for Economic Co-operation and Development. Explanatory memorandum on the updated OECD definition of an AI system.https://www.oecd.org/en/publications/ explanatory-memorandum-on-the-updated-oecd-definition-of-an-ai-system_ 623da898-en.html, 2024. Accessed 2026-06-02

2024

-

[30]

Romanosky, L

S. Romanosky, L. Ablon, A. Kuehn, and T. Jones. Content analysis of cyber insurance policies: How do carriers price cyber risk?Journal of Cybersecurity, 5(1):tyz002, 2019

2019

-

[31]

Intriguing properties of neural networks

C. Szegedy, W. Zaremba, I. Sutskever, J. Bruna, D. Erhan, I. Goodfellow, and R. Fergus. Intriguing properties of neural networks. arXiv:1312.6199, 2013

work page internal anchor Pith review Pith/arXiv arXiv 2013

-

[32]

The Geneva Association. Advancing accumulation risk management in cy- ber insurance.https://www.genevaassociation.org/sites/default/files/ research-topics-document-type/pdf_public/report_advancing_accumulation_risk_ management_in_cyber_insurance_0.pdf, 2024. Accessed 2026-06-02

2024

-

[33]

Cyberrisk coverage form.https://piaffinity.travelers.com/iw-documents/ apps-forms/cyberrisk/cyb-16001.pdf, 2024

Travelers. Cyberrisk coverage form.https://piaffinity.travelers.com/iw-documents/ apps-forms/cyberrisk/cyb-16001.pdf, 2024. Accessed 2026-06-02

2024

-

[34]

Errors and omissions vs

Vouch. Errors and omissions vs. AI insurance.https://www.vouch.us/blog/ errors-omissions-vs-ai, 2024. Accessed 2026-06-02

2024

-

[35]

Zhang and Q

R. Zhang and Q. Zhu. Attack-aware cyber insurance of interdependent computer networks. Technical Report 16-18, NET Institute, 2016. Accessed 2026-06-03

2016

-

[36]

R. Zhang and Q. Zhu. Flipin: A game-theoretic cyber insurance framework for incentive- compatible cyber risk management of internet of things. arXiv:1911.10100, 2019

-

[37]

Zhang and Q

R. Zhang and Q. Zhu. Optimal cyber-insurance contract design for dynamic risk management and mitigation.IEEE Transactions on Computational Social Systems, 9(4):1087–1100, 2021

2021

- [38]

- [39]

-

[40]

Zhu and T

Q. Zhu and T. Ba¸ sar. Game-theoretic methods for robustness, security, and resilience of cy- berphysical control systems: Games-in-games principle for optimal cross-layer resilient control systems.IEEE Control Systems, 35(1):46–65, 2015

2015

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.